In This Report

LAO Contact: Ross Brown

January 21, 2016

Cap-and-Trade Revenues:

Strategies to Promote Legislative Priorities

Executive Summary

Cap–and–Trade Regulation Key to Meeting Emissions Goal. California’s cap–and–trade program to significantly reduce greenhouse gas (GHG) emissions by 2020 has two major components: (1) the regulation and (2) auction revenue. The relationship between these two components is complex, from both a policy and legal perspective. From a policy standpoint, the regulation is intended to ensure the state meets its GHG goals and provide an incentive for cost–effective emission reductions. A well–designed cap–and–trade regulation also generates auction revenue even though generating revenue is not a primary goal of the program.

Requirement to Spend Auction Revenues on GHG Reductions Creates Policy Challenges. Under current law (and potentially under future court decisions), the state can only spend auction revenue on activities that facilitate GHG reductions. However, this requirement creates some significant policy challenges. First, spending auction revenue on GHG reductions is likely not necessary to meet the state’s GHG goals and likely increases the overall costs of emission reduction activities. This is because, in certain cases, spending on GHG reductions interacts with the regulation in a way that changes the types of emission reduction activities, but not the overall level of emission reductions. Second, the requirement to spend on GHG reductions limits the Legislature’s flexibility to use the revenue in a ways that could achieve other goals, such as (1) offsetting higher costs for households and businesses associated with higher energy prices; (2) promoting other climate–related policy goals, such as climate adaptation activities; or (3) promoting other legislative priorities unrelated to climate policy.

Strategies to Promote Legislative Priorities. In light of these challenges, we present alternative strategies designed to help the Legislature promote its priorities more efficiently under two alternative scenarios:

- Under a Requirement to Spend on GHG Reductions. Strategies that can be utilized under a legal framework which requires that revenues be spent on activities that facilitate the reduction of GHGs include (1) targeting uncapped emission sources, (2) targeting cost–effective emission reduction activities, (3) prioritizing other legislative goals, and (4) offsetting other state spending. Each of these strategies would help promote different legislative priorities and present different levels of legal risk.

- Removal of Requirements to Spend on GHG Reductions by Reauthorizing Cap–and–Trade With Two–Thirds Vote. Removing the legal requirement to spend on GHG reductions would (1) provide the Legislature maximum flexibility to provide rebates or tax reductions to offset costs for households and businesses and/or use the funds to address its highest policy priorities, and (2) reduce legal uncertainty regarding the regulation beyond 2020. Moreover, as long as a well–designed cap–and–trade regulation is in place, the state will likely meet its GHG emission targets from major sources of emissions.

Introduction

California’s cap–and–trade program is one of the primary policies intended to help achieve the state’s greenhouse gas (GHG) reduction goals. In this report, we describe and assess the relationship—from both a legal and policy perspective—between the cap–and–trade regulation and the auction revenues that are generated as a result of the program. Based on our assessment, we present general approaches to cap–and–trade spending for the Legislature to consider that could enhance its ability to: (1) promote cost–effective GHG reductions, (2) reduce costs for energy users, and (3) promote the highest legislative priorities.

On January 7, 2016, the Governor released a $3.1 billion cap–and–trade expenditure plan for 2016–17. We do not analyze the specific proposals included in the Governor’s plan in this report. We plan to release a more detailed analysis of the Governor’s specific proposals in the coming weeks as part of our 2016–17 budget analysis.

Background

California’s Climate Change Policies

Climate Change and GHGs. Greenhouse gases are gases that trap heat within the earth’s atmosphere, thereby increasing the earth’s temperature. Both natural phenomena and human activities (principally burning fossil fuels) produce GHGs. Scientific experts indicate that higher concentrations of GHGs resulting from human activities are increasing global temperatures, and that such global temperature rises (commonly referred to as global warming or climate change) will likely cause significant problems, such as sea level rise, extended droughts, and heat–related illnesses.

AB 32 and the Scoping Plan. The Global Warming Solutions Act of 2006 (Chapter 488 [AB 32, Núñez/Pavley]), commonly referred to as AB 32, established the goal of reducing GHG emissions statewide to 1990 levels by 2020. The legislation directed the Air Resources Board (ARB) to adopt regulations to achieve the maximum technologically feasible and cost–effective GHG emission reductions by 2020. In addition, to the extent feasible, ARB must:

- Design regulations, including distribution of emission allowances (discussed below), in a manner that is equitable and minimizes costs and maximizes benefits to California.

- Ensure that activities undertaken to comply with regulations do not disproportionately impact low–income communities.

- Ensure that activities complement efforts to achieve regional air quality standards.

- Minimize emissions that are shifted out of state because companies move the production of goods outside of California due to higher costs associated with climate change regulations (referred to as “leakage”).

The ARB is required to develop a Scoping Plan to achieve the emission targets and update the plan periodically. The first Scoping Plan was approved by ARB in 2008 and the first update to the Scoping Plan was approved in 2014. As shown in Figure 1, the Scoping Plan includes a wide variety of regulations intended to help the state meet its GHG goal, including cap–and–trade, the low carbon fuel standard, energy efficiency programs, and the renewable portfolio standard. Scoping Plan regulations are projected to reduce emissions by 78 million metric tons of carbon dioxide equivalent in 2020—roughly 15 percent below what annual emissions are estimated to have been without the regulations.

Figure 1

Regulations Expected to Help State Meet 2020 Greenhouse Gas Emissions Goal

|

Regulations |

MMTCO2E Reduction |

|

Cap–and–trade |

23 |

|

Low carbon fuel standard |

15 |

|

Energy efficiency and conservation |

12 |

|

33 percent renewable portfolio standard |

12 |

|

Refrigerant tracking, reporting, and repair deposit program |

5 |

|

Advanced clean cars |

3 |

|

Reductions in vehicle miles traveled (SB 375) |

3 |

|

Landfill methane control |

2 |

|

Other regulations |

5 |

|

Total |

78 |

|

MMTCO2E = million metric tons of carbon dioxide equivalent. |

|

Cap–and–Trade. About 30 percent of the projected GHG emission reductions in 2020 come from the ARB’s cap–and–trade regulation. The cap–and–trade regulation places a “cap” on aggregate GHG emissions from large GHG emitters, such as large industrial facilities, electricity generators and importers, and transportation fuel suppliers. Capped sources of emissions are responsible for roughly 85 percent of the state’s GHG emissions. The cap declines over time, ultimately arriving at the target emission level in 2020. To implement the cap–and–trade program, ARB issues carbon allowances equal to the cap, and each allowance is essentially a permit to emit one ton of carbon dioxide equivalent. Entities can also “trade” (buy and sell on the open market) the allowances in order to obtain enough to cover their total emissions. Some entities are forced to reduce their emissions because, in theory, the number of allowances available is less than the number of emissions that would otherwise occur. Entities can also purchase “offsets” to cover their emissions. Offsets are GHG emission reduction projects undertaken by entities not subject to the state’s cap–and–trade program, such as forestry projects that reduce GHGs. Offsets were used to cover about 4 percent of emissions in 2013 and 2014.

Cap–and–trade is a market–based approach to reducing emissions. (The other common market–based approach is a carbon tax.) Market–based approaches differ from other regulatory approaches, such as traditional command–and–control regulations. Under traditional regulations for reducing emissions, government requires every business to install a certain type of emission reduction technology or meet a certain minimum emissions standard. In contrast, a market–based approach adds a financial cost to producing GHGs, which provides a financial incentive for private businesses and consumers to reduce emissions. The private sector has flexibility to determine which emission reduction activities are least costly. (For more details on market–based approaches, see our 2012 report Evaluating the Policy Trade–Offs of California’s Cap–and–Trade Program.)

What About Emission Goals and Cap–and–Trade Post–2020? The administration and Legislature have both expressed an interest in achieving significant post–2020 GHG reductions. For example, Executive Orders establish goals of reducing statewide emissions to 40 percent below 1990 levels by 2030 and 80 percent below 1990 levels by 2050 and direct ARB and other state agencies to implement measures, pursuant to statutory authority, to achieve these goals. In addition, the Legislature has adopted major policies intended to achieve substantial GHG reductions beyond 2020. For example, Chapter 547 of 2015 (SB 350, de León) requires (1) that a minimum of 50 percent of all electricity sold by utilities be from renewable sources and (2) doubling energy efficiency savings in electricity and natural gas by 2030.

We note that, without new legislation, there is some legal uncertainty regarding ARB’s authority to: (1) enforce regulations to achieve more stringent post–2020 GHG targets and (2) extend the cap–and–trade program beyond 2020. According to ARB, AB 32 provides the authority to do both. However, based on our informal discussions with Legislative Counsel, it appears unlikely that AB 32 provides such authority. Although AB 32 states the intent of the Legislature that the statewide GHG emissions limit remain in existence and be used to “maintain and continue” reductions in emissions beyond 2020, post–2020 GHG targets below 1990 levels are not specified in statute, and AB 32 states that the GHG limit shall remain in effect unless otherwise amended or repealed. In addition, AB 32 explicitly authorizes ARB to implement a market–based mechanism through 2020, and it is unlikely that the authority provided elsewhere in AB 32 allows ARB to continue to operate the cap–and–trade program after 2020.

Cap–and–Trade Auction Revenue

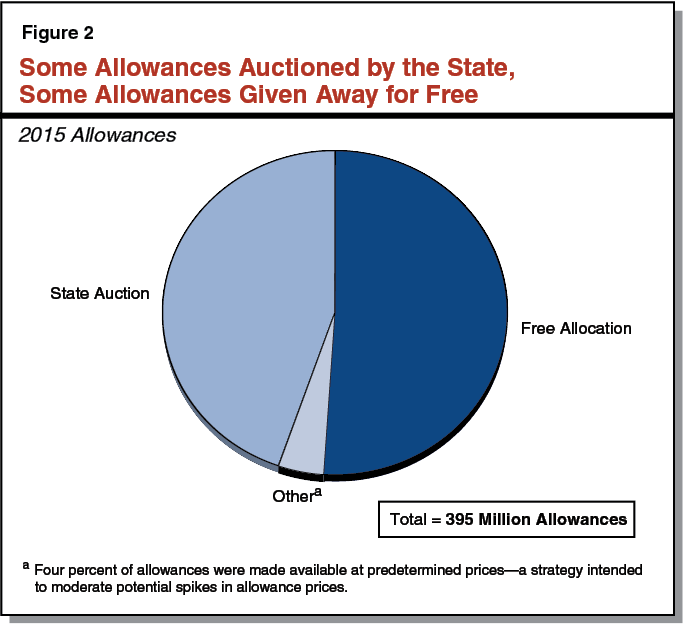

Some Allowances Auctioned, Some Given Away for Free. One important aspect of implementing a cap–and–trade program is determining how to distribute allowances. In theory, allowances can be issued in one of three general ways: (1) they can be given away for free, (2) they can be auctioned by the state, or (3) some portion can be freely allocated while the other portion is auctioned. As shown in Figure 2, ARB auctioned about 45 percent of 2015 allowances and gave 51 percent away for free. (Four percent of allowances are made available at predetermined prices—a strategy intended to moderate potential spikes in allowance prices.) Of the 51 percent of allowances given away for free, most were given to investor–owned utilities (IOUs) (16 percent), certain industrial emitters (14 percent), natural gas suppliers (11 percent), and publicly owned utilities (7 percent). State law and regulation require IOUs to auction their allowances and most of the resulting revenue must be credited to their industrial, small businesses, and residential electricity customers.

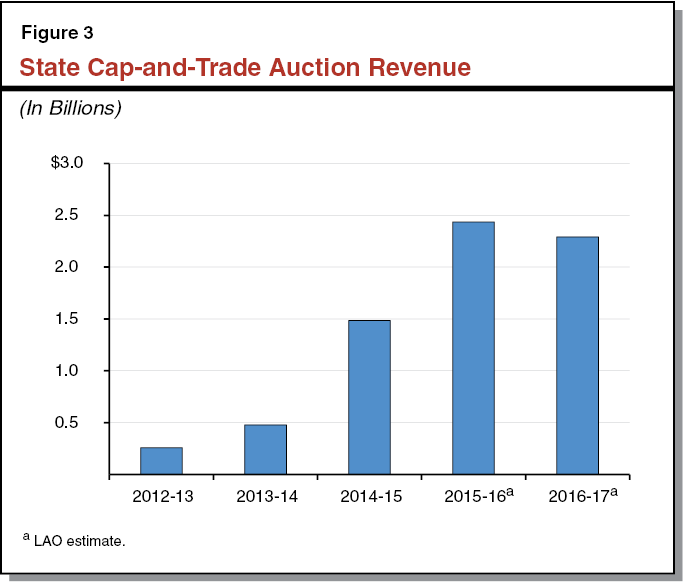

Auctions Generate Billions of Dollars in State Revenue. The ARB has conducted 13 quarterly cap–and–trade auctions since November 2012—generating roughly $3.5 billion in state revenue. Beginning January 1, 2015, transportation fuel suppliers were required to obtain allowances for the GHG emissions associated with the combustion of their fuels. Since transportation fuel suppliers are not given free allowances, the number of state–auctioned allowances has increased significantly over the past year—resulting in recent auctions raising significantly higher amounts of state revenue than past auctions. We project the state will generate about $2.4 billion in auction revenue in 2015–16 and $2.3 billion in 2016–17, assuming that auction prices stay at similar levels to recent auctions. We note, however, that the amount of future auction revenue—especially revenue beyond the next couple of years—is subject to substantial uncertainty. Figure 3 shows actual auction revenues for 2012–13 through 2014–15, as well as our projected revenues for 2015–16 and 2016–17.

State Constitution Likely Requires Revenue Be Used to Reduce GHGs. There is currently a court case challenging whether the state can continue collecting revenue from auctions. In a lawsuit against ARB, plaintiffs argue that the Legislature did not provide ARB the authority to auction allowances and collect state revenue. (Plaintiffs do not dispute ARB’s authority to operate a cap–and–trade program and give allowances away.)

They further argue that even if the Legislature gave ARB the authority to collect auction revenue, such revenue constitutes an illegal tax. The California Constitution requires that any increases in state taxes be approved by a two–thirds vote of the Legislature. Previous court decisions have determined that certain types of “charges,” such as regulatory fees, are not considered taxes and require only a simple majority vote. The plaintiffs argue that auction revenues are tax revenues and, since AB 32 was not passed with a two–thirds vote, the state is collecting auction revenues illegally. In November 2013, the superior court ruled that the charges from the auction have characteristics of a tax as well as a fee, but that, on balance, the charges constitute legal regulatory fees. This ruling has been appealed, and final decisions from the appellate courts on these issues may take years.

If the courts’ final decision on these questions is to determine that ARB has the authority to collect auction revenue, it is likely that the courts would establish some limits on how revenues can be used. Previous court decisions require the state to use regulatory fee revenue to advance the goals of the regulatory program. In addition, the superior court ruling identified the state’s intent to use the revenue to advance the goals of AB 32 (discussed below) as a significant factor in upholding ARB’s authority to conduct the auctions. Therefore, the courts would likely require the state to target spending to GHG reduction activities since that is the primary goal of AB 32. The extent to which the courts might allow the state to use the funds in a way that is intended to achieve other AB 32 goals (such as improving air quality and minimizing costs for households) or for activities with less certain effects on GHGs is unclear.

State Law Requires Auction Revenue Be Used to Reduce GHGs. Statutes enacted in 2012 direct the use of auction revenue. For example, Chapter 807 of 2012 (AB 1532, Perez) requires auction revenues be used to further the purposes of AB 32. Revenues must be used to facilitate GHG emission reductions in California. In addition to reducing GHGs, to the extent feasible, funds must be used to achieve other goals, such as:

- Maximize overall economic, environmental, and public health benefits to the state.

- Complement efforts to improve air quality.

- Lessen the effects of climate change on the state (also known as climate adaptation).

- Direct investment toward the most disadvantaged communities and households in the state.

To address this last goal, Chapter 830 of 2012 (SB 535, de León) requires that at least 25 percent of auction revenue be used to benefit disadvantaged communities (as determined by the Office of Environmental Health Hazard Assessment) and at least 10 percent be spent on projects located within disadvantaged communities.

Administration Required to Develop Investment Plan. The administration is required to produce several reports, which are intended to ensure funds are spent in a way that is legal and consistent with legislative priorities. For example, every three years, the Department of Finance must develop an investment plan that identifies feasible and cost–effective GHG emission reduction investments. Among other things, the Three–Year Investment Plan must:

- Analyze gaps, where applicable, in current state strategies to meeting the state’s GHG emission reduction goals.

- Identify priority investments that will facilitate the achievement of feasible and cost–effective GHG reductions.

The administration released its first investment plan in 2013 and is in the process of completing its second investment plan.

How Has Auction Revenue Been Spent So Far? As illustrated in Figure 4, auction revenue has been used to fund various programs and projects. For revenue collected in 2015–16 and beyond, statute continuously appropriates (1) 25 percent for the state’s high–speed rail project, (2) 20 percent for affordable housing and sustainable communities grants (with at least half of this amount for affordable housing), (3) 10 percent for intercity rail capital projects, and (4) 5 percent for low carbon transit operations. The remaining 40 percent is available for annual appropriation by the Legislature. Statute also requires that an outstanding loan of $400 million in auction revenues to the General Fund be repaid to the high–speed rail project when needed by the project.

Figure 4

Cap–and–Trade Expenditures

(In Millions)

|

Program |

2013–14 |

2014–15 |

2015–16a |

|

High–speed rail |

— |

$250 |

$600 |

|

Affordable housing and sustainable communities |

— |

130 |

480 |

|

Transit and intercity rail capital |

— |

25 |

240 |

|

Transit operations |

— |

25 |

120 |

|

Low carbon transportation |

$30 |

200 |

90 |

|

Low–income weatherization and solar |

— |

75 |

70 |

|

Agricultural energy and operational efficiency |

10 |

25 |

40 |

|

Urban water efficiency |

30 |

20 |

20 |

|

Sustainable forests and urban forestry |

— |

42 |

— |

|

Waste diversion |

— |

25 |

— |

|

Wetlands and watershed restoration |

— |

25 |

— |

|

Other administration |

2 |

10 |

31 |

|

Totals |

$72 |

$852 |

$1,691 |

|

aBased on LAO projection of $2.4 billion in revenue in 2015–16. The fund balance is projected to be $1.6 billion by the end of 2015–16. |

|||

Cap–and–Trade Regulation Key to Meeting Emissions Goal

The state’s cap–and–trade program has two major components: (1) the cap–and–trade regulation and (2) auction revenue. Below, we discuss how the cap–and–trade regulation is designed to ensure the state meets its GHG emission goals in a cost–effective manner.

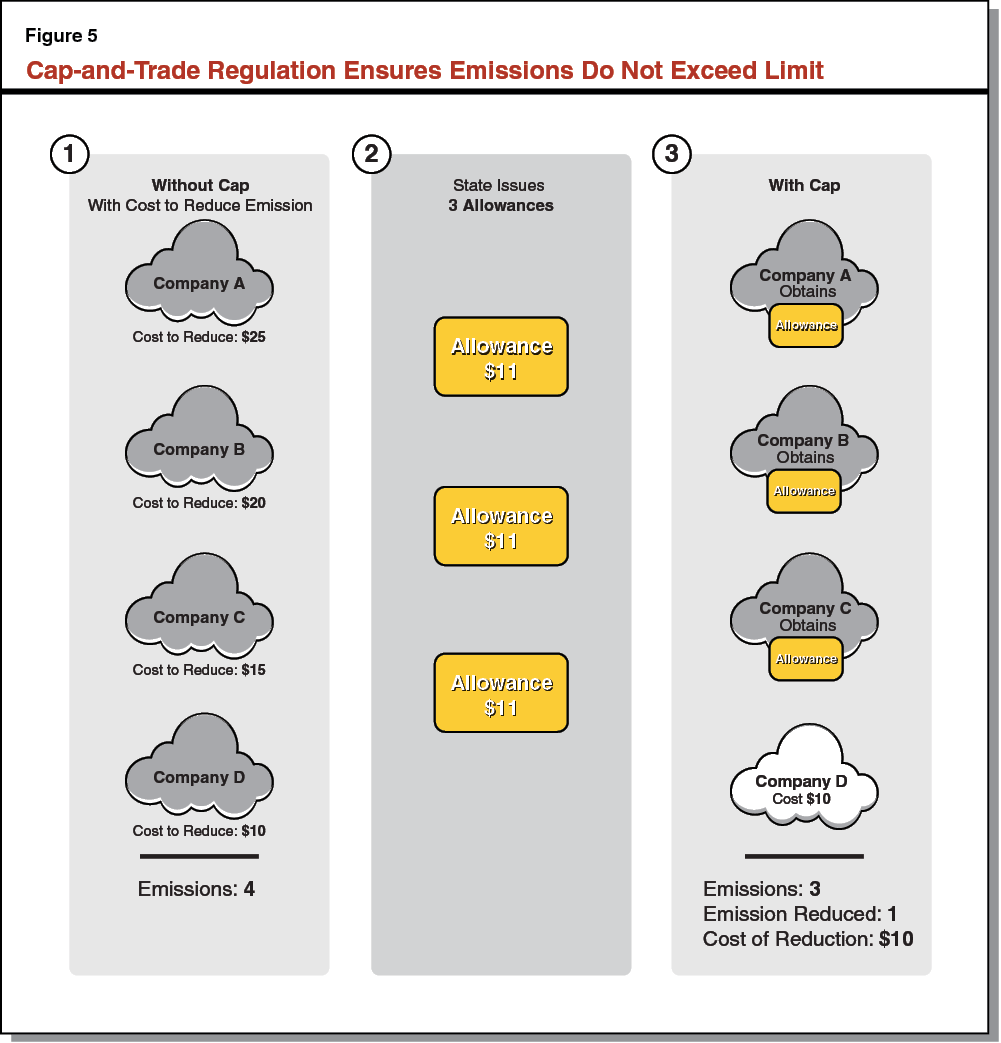

Cap Ensures California Meets 2020 GHG Target From Largest Sources of Emissions. From a GHG emissions perspective, one of the primary advantages of a cap–and–trade regulation is that the cap ensures total GHGs from major sources of emissions do not exceed the limit established by the state. This is because the state issues a limited number of allowances, and large emitters are required to obtain an allowance for each emission. Therefore, as long as GHG emissions are accurately measured and the regulation is adequately enforced, the number of emissions cannot exceed the number of allowances (or the cap).

Figure 5 shows a simplified example of how a cap–and–trade program ensures emissions do not exceed the number of allowances issued by the state. Without establishing a cap, Companies A, B, C, and D would each have one emission. To establish a cap, the state issues three allowances. As a result, only three companies can obtain an allowance and continue to emit, while one company is forced to reduce its emission.

Allowance Price Provides Incentive for Cost–Effective Emission Reductions. From an economic perspective, the primary advantage of a cap–and–trade program is that it creates a financial incentive to identify the least costly emission reduction activities. The supply and demand of allowances in a trading market generally determine the price of an allowance. In our example, each company would only purchase an allowance if the allowance price (in this case, $11) is lower than their cost to reduce their emission. As shown in the example in Figure 5, some emitters (Company D in this case) will reduce emissions because it is less costly ($10) for them to do so than purchase an allowance. Remaining emitters will purchase an allowance and continue to emit because allowances are cheaper than reducing emissions. In theory, the level of overall emission reductions is achieved at the lowest cost possible—$10 in our example. This is because the allowance price provides an economic incentive to find the mix of emission reductions and allowance purchases that minimize costs. (We note that although Companies A, B, and C incur costs to purchase allowances, economists generally do not consider these to be net economic costs to society, partly because the allowances do not result in a reduction in emissions.)

It is important to note that, while covered entities (such as electricity generators and transportation fuel suppliers) pay the direct costs of purchasing allowances, at least a portion of the costs are passed on to customers and other businesses in the form of higher product prices. As a result, a wide variety of businesses and households have a financial incentive to use less GHG–intensive products. For example, transportation fuel suppliers must purchase allowances associated with the emissions from gasoline consumption, but those costs are generally passed on to consumers in the form of higher gasoline prices. As gasoline prices increase, businesses and households have an incentive to reduce gasoline consumption. The higher prices are key to ensuring that businesses and consumers have an incentive to consume fewer GHG–intensive products. However, it also means that households and businesses that continue to consume these products, such as gasoline, will pay more for those goods and services.

Auctions Are Generally the Preferred Method of Distributing Allowances . . . In theory, the method of distributing allowances has no direct effect on the overall level of emissions or cost of emission reductions. This is because the overall level of emissions cannot exceed the number of allowances issued, regardless of how the allowances are initially distributed. Also, each company still has an incentive to reduce emissions if doing so is less than the price of an allowance.

However, the distribution of allowances can have significant indirect effects, such as on the overall level of emissions outside of California, and how the costs and benefits of the program are distributed. In general, economists recommend auctioning allowances rather than giving them away for free. This is because auctions are considered a more transparent, equitable, and efficient method of distributing allowances. (For more detailed information on the potential benefits of auctioning allowances, please see the nearby box.) The primary exception to this recommendation is giving away allowances for free to certain industries to prevent leakage. Free allocations to prevent leakage can help ensure the program is reducing overall emissions by ensuring emissions are not simply shifted to other states or countries.

Economic Advisory Committee Recommended Auctioning Allowances

Economists generally recommend auctioning cap–and–trade allowances, rather than giving them away for free. For example, an economic advisory committee established by the Air Resources Board in 2010 recommended relying principally on auctioning as the mechanism for distributing allowances. Some of the advantages of auctions include:

- Easier Treatment for New Entrants. Auctions treat new and existing companies equally because they all have to purchase allowances. New companies see the same cost as competitors when entering the market. In contrast, giving allowances away for free could create an advantage for existing companies if free allowances are based on previous production in California.

- Maintains Price Signal. Under auctions, companies that have to pay for allowances will often pass those costs on to customers in the form of higher prices. From an economic perspective, this is an advantage because it provides an incentive for households and businesses to identify cost–effective opportunities to reduce emissions. In contrast, free allocations based on a company’s production can prevent product prices from rising and, thereby, reduce these price signals. This can result in higher overall emission reduction costs because consumers who have opportunities to undertake low–cost emission reductions no longer have a financial incentive to do so.

- Avoids Windfall Profits for Companies. In certain circumstances, giving allowances away for free can result in “windfall profits” for certain companies if the value of the allowances they receive is significantly greater than the costs of complying with the regulation. This may be viewed as an unfair distribution of allowance value. Windfall profits for companies will not occur under auctions.

- Opportunities to Reduce Taxes. Auction revenue can be used to provide economic benefits. For example, revenue could be used to reduce broad–based taxes (such as income or sales taxes), which could help reduce negative impact on economic activity.

The one instance in which the committee recommended giving allowances away for free was to prevent leakage for certain industries. Allocating free allowances to certain companies based on their level of production can reduce companies’ incentive to shift production to other states. Under this approach, the state effectively provides these companies a subsidy for each unit of production in California—in the form of free allowances—to encourage them to continue to produce in California. While this can be an effective strategy for reducing leakage, the committee also noted that the state could accomplish the same objective by auctioning the allowances and using the resulting revenue to encourage production in California.

. . . But Generating Additional Revenue Not a Primary Goal of Cap–and–Trade. While auctioning allowances is generally the preferred method for distributing at least a portion of allowances, the primary goal of a cap–and–trade program is to provide an economy–wide incentive for businesses and consumers to undertake cost–effective emission reductions. For this reason, from an economic perspective, auction revenues are often thought of as a byproduct of cap–and–trade programs and not their primary goal.

Requirement to Spend Auction Revenue on GHG Reductions Creates Policy Challenges

As discussed above, state law requires that auction revenue be spent on activities that facilitate the reduction of GHGs. In the past, our office recommended the Legislature use the revenue to reduce GHGs—a recommendation that was largely based on our understanding of the likely legal restrictions on the use of the funds. We continue to believe that targeting funding to GHG reduction activities is a reasonable strategy to reduce legal risk because the funds are being used to achieve the primary regulatory goal of AB 32. In addition, funding projects that reduce GHGs can produce significant benefits, such as improved regional air quality.

However, this approach creates significant policy challenges because (1) spending a substantial amount of auction revenue on GHG reductions in the capped sector is likely not necessary to meet the state’s GHG goals and likely increases overall costs and (2) the requirement to spend on GHG reductions limits legislative flexibility to achieve other goals. We discuss these policy challenges in more detail below.

Spending Auction Revenue on GHGs Unnecessary and More Costly

Spending auction revenue on GHG emission reductions from capped sources interacts with the cap–and–trade regulation in somewhat complicated and perhaps unexpected ways. Below, we discuss these interactions and the implications for overall GHG emission reductions and costs.

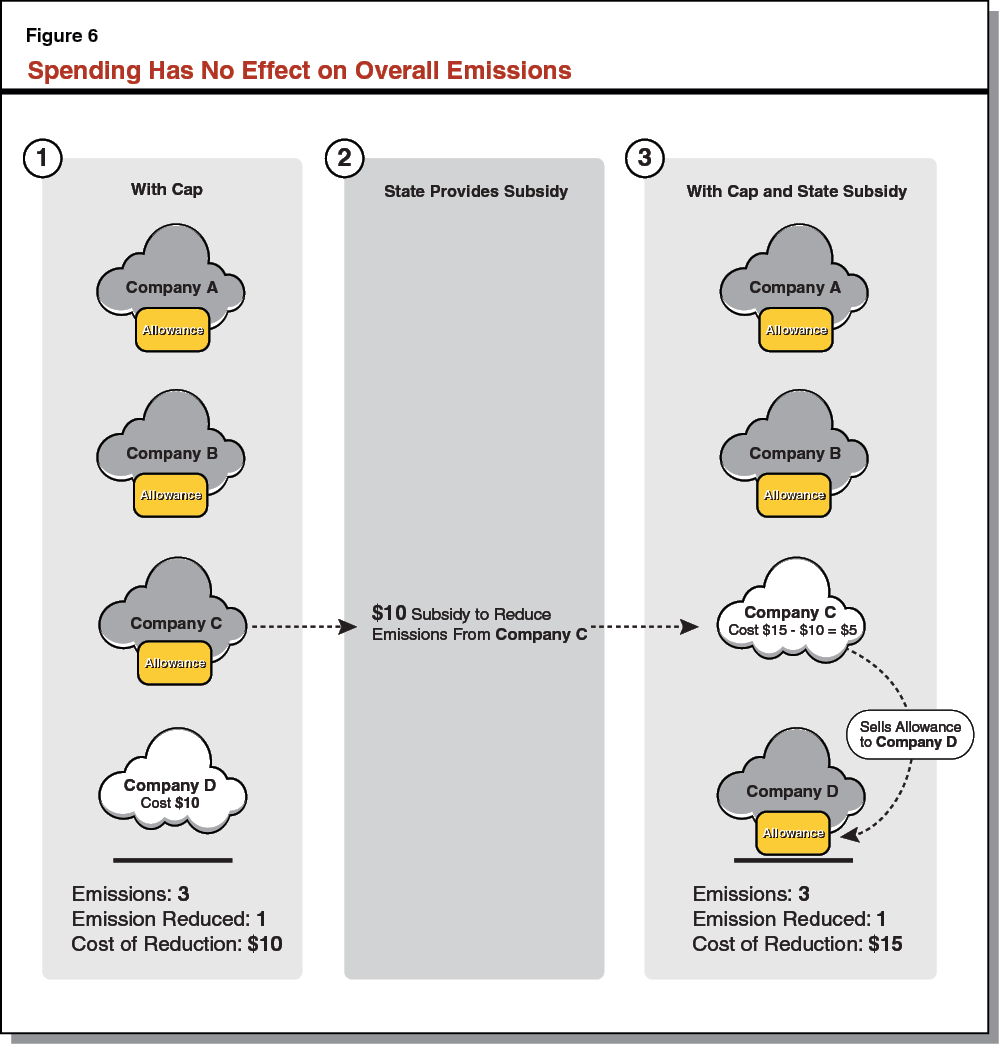

Spending on Capped Sources Likely Has No Net Effect on Overall Emissions. At first glance, subsidizing emission reductions from capped sources might appear to encourage additional emission reductions. However, as long as the cap is limiting emissions from these sources, spending on activities that reduce emissions from these sources will likely have no net effect on overall emissions. Figure 6 builds on the example in Figure 5 and illustrates how subsidizing reductions from capped sources results in no net change in emissions. Specifically, as shown in Figure 6:

- Without Subsidy, Company D Reduces Emission and Others Purchase Allowances. As shown in Figure 6, without state spending on GHG emission reductions, Company D will reduce emissions for a cost of $10. Companies A, B, and C will purchase allowances and continue to emit.

- State Subsidizes Emission Reduction From Company C. Company C could reduce its emissions at a cost of $15. However, the state offers a $10 subsidy for Company C to reduce its emission. For example, the subsidy might be a grant to install a more energy–efficient production technology. Consequently, Company C can reduce emissions for $5, rather than $15.

- Company C Reduces Emissions and Sells Allowance to Company D. With the subsidy, it is now cheapest for Company C to reduce its emission. So, it chooses to sell its allowance. Company D has an incentive to purchase the allowance as long as it is cheaper than the cost of reducing its emission ($10). Company D purchases the allowance from Company C—for $9, for example—and continues to emit.

- Despite State Spending, There Is No Additional Decrease in Emissions. The net effect of subsidizing an emission reduction from Company C is that Company D will obtain the allowance and continue to emit instead of Company C.

As long as the cap is limiting emissions, subsidizing an emission reduction from one capped source will simply free–up allowances for other emitters to use. The end result is a change in the sources of emissions, but no change in the overall level of emissions.

In contrast to spending on reductions from capped sources, spending on reductions from uncapped sources—such as agriculture, landfill methane emissions, and emissions from refrigerants—is likely to reduce overall emissions. Net reductions could occur in the uncapped sectors because there would be no trading of allowances that would allow the subsidized emission reduction to be offset by an increase in emissions from a different source.

Spending on GHG Reductions From Capped Sources Likely Increases Overall Costs. As discussed above, the cap–and–trade regulation generally creates a financial incentive for producers and consumers to find the least costly mix of emission reductions. Therefore, using state funds to encourage a different mix of GHG emission reductions would likely be more costly. For example, the overall emission reduction costs in Figure 6 are $10 without the state subsidy. The overall emission reduction costs with the state subsidy—including both state spending and private spending—are $15.

In some limited circumstances, the incentives provided by cap–and–trade might fail to encourage cost–effective emission reduction activities. In such instances, targeting auction revenue to certain GHG reduction activities in the capped sector might be able to improve overall cost–effectiveness, as we discuss in more detail later in this report.

Limits Flexibility to Efficiently Achieve Other Legislative Goals

The Legislature has a wide variety of goals and priorities, in addition to reducing GHG emissions. Programs funded with auction revenue are, in part, intended to promote some of these other goals and priorities (such as improving air quality and limiting costs for low–income households). However, under current law (and potentially under future court decisions), the state can only fund projects that provide those benefits if those projects also reduce GHGs. This limits the state’s flexibility to achieve non–GHG benefits as efficiently as possible.

Limits Flexibility to Reduce Costs for Energy Users. As noted earlier, AB 32 directs ARB to design regulations in a way that minimizes costs and ensures activities undertaken to comply with the regulations do not disproportionately impact low–income communities. Currently, some programs funded with auction revenue provide financial benefits to households, but such benefits only go to the small portion of households that participate in the program. For example, in 2014–15, the ARB’s Clean Vehicle Rebate Project provided $111 million in rebates to 52,000 individuals that purchased electric vehicles. These households represent less than one–half of 1 percent of the nearly 13 million households in California. In addition, any financial benefits provided to households through many of the other programs that receive significant amounts of funding (such as transit and high–speed rail) are relatively indirect and difficult to measure.

Ideally, there would be more direct ways to reduce costs for households. For example, the state could use auction revenue to provide an annual rebate check to California households and/or businesses affected by cap–and–trade. The amount of the rebate could be a lump sum amount not dependent on the household’s energy use. This would maintain the financial incentive to use less GHG–intensive products and meet the state’s climate change goal. In addition, the Legislature would have the flexibility to determine the amount of the rebate going to each household to ensure that low–income households do not bear a disproportionate amount of the costs.

A similar approach is currently being implemented by the state’s IOUs. State law and regulation directs the IOUs to use revenue raised from selling their free allowances to provide a semiannual “Climate Credit” on customers’ bills. The Climate Credit is intended to offset the higher costs of electricity associated with cap–and–trade. However, it is unclear if such an approach would be practical or legal to implement more broadly. The IOUs present a somewhat unique situation because the state has substantial regulatory authority over IOUs. As a result, it can direct IOUs to use the revenue to offset customer costs. In addition, since the revenue is collected by the IOUs, it is not technically state revenue and might not have the same potential legal restrictions associated with state regulatory fees.

Limits Flexibility to Achieve Climate–Related Policy Goals. The current requirement to spend auction revenue on activities that reduce GHGs limits the state’s flexibility to use the funds in a way that maximizes the state’s ability to lessen the effects of climate change. For example, many of the activities that might be needed to prepare for the effects of climate change—such as public health strategies to prevent heat illnesses, enhanced emergency management activities, and protecting infrastructure from rising sea levels—likely do not reduce GHG emissions.

In addition, auction revenue currently is being used to fund a variety of activities that are intended to improve air quality (as well as reduce GHGs), such as rebates for electric vehicles and funding for public transit. The state could be missing opportunities to fund activities that produce significant local air quality benefits but that have no significant effect on GHGs. For example, using the funds to encourage companies to upgrade air pollution control technologies that reduce nitrous oxides or particulate matter might provide substantial air quality benefits, but such activities might have little or no GHG benefit. Moreover, to the extent the Legislature is interested in maximizing air quality benefits for disadvantaged communities, the current requirement potentially limits flexibility to fund the most effective air quality projects in these communities.

Limits Flexibility to Promote Legislative Priorities Unrelated to Climate Policy. The Legislature has many other goals and priorities, in addition to those identified in climate–related legislation. For example, at the time this report was prepared, the Legislature was in a special session to identify a permanent and sustainable increase in funding for transportation. Improving the state’s transportation infrastructure could provide significant economic and social benefits. The current requirement potentially limits flexibility to fund certain projects from auction revenues that have the greatest mobility benefits if the GHG effects associated with such projects are unclear. The requirement also limits flexibility to address other legislative priorities, which could include: (1) tax reductions; (2) greater fiscal stability; and/or (3) spending on other priority programs, such as improved health care services, education facilities, or public safety programs.

Post–2020 Uncertainty Creates Additional Challenges

As discussed above, there is currently some dispute about the ARB’s current statutory authority to: (1) enforce regulations to achieve a more stringent post–2020 GHG target and (2) extend the cap–and–trade program beyond 2020. Below, we discuss some of the potential problems created by this legal uncertainty.

Costly Private Investment Decisions. Regulatory uncertainty about long–term GHG limits and regulations can make it difficult for covered entities today to make cost–effective long–term investments. For example, a company might have an opportunity to purchase a more expensive, but more efficient, technology that reduces GHGs reductions beyond 2020. If the company purchases the more expensive technology that is not ultimately needed to comply with state regulations, it would face increased costs unnecessarily. Alternatively, if the company does not purchase the more efficient technology and the state subsequently adopts more stringent GHG reduction requirements, then the company might have to find more expensive ways to comply in the future.

Difficulty Evaluating State Spending Options. If cap–and–trade is extended beyond 2020, then spending auction revenues now on activities that reduce emissions from capped sources will likely have no net effect on long–term emissions. If the program is not extended, then spending on post–2020 emission reductions from capped sources could reduce long–term emissions. Clarifying whether cap–and–trade will be extended beyond 2020 would give the Legislature a better understanding of how its near–term spending decisions will affect GHG emissions in the long run.

Options For Legislative Consideration

As long as the Legislature has GHG reduction goals, we think relying heavily on market–based regulatory approaches, such as a cap–and–trade program, would help achieve such goals in a cost–effective manner. Although a well–designed cap–and–trade program generally includes auctioning at least some allowances, generating revenue is not a primary goal of the program. Further, spending billions of dollars of auction revenue on GHG reductions from capped sources is not necessary to accomplish GHG goals, and doing so limits flexibility to limit costs for households and businesses and achieve other legislative priorities.

In our view, these findings have significant implications for how the Legislature might want to approach cap–and–trade and the expenditure of auction revenue. Below, we provide strategies designed to help the Legislature promote its priorities more efficiently under two alternative scenarios: (1) under a legal framework that requires cap–and–trade revenue be spent on GHG reductions and (2) removal of the legal requirement to spend revenue on GHG reductions by reauthorizing the cap–and–trade program with a two–thirds vote.

Under a Requirement to Spend on GHG Reductions

We first discuss strategies for using auction revenue assuming the Legislature continues to operate under a legal framework for cap–and–trade which requires the funds be spent on activities that facilitate the reduction of GHGs. The extent to which the Legislature relies on each of these strategies depends on: (1) legislative policy priorities and (2) an assessment of the legal risk associated with each option. In general, the more the funds are being used for things other than the primary purpose of AB 32—achieving the 1990 GHG limit—or on projects that have less certain GHG benefits, the greater the risk of violating future court restrictions on the use of the funds. We continue to recommend the Legislature consult with Legislative Counsel about the legal risks associated with different spending options.

Spend in Uncapped Sector to Achieve Net GHG Reductions. The ARB projects that existing regulations will encourage enough emission reductions—from capped and uncapped sources—to meet the state’s overall 2020 GHG target. To the extent additional GHG reductions are a priority, the Legislature could target funds to achieve GHG emission reductions from uncapped sources. As discussed above, spending on emission reductions from uncapped sources would likely result in net emission reductions. In addition, there is limited legal risk associated with this option because the funds would be targeted to GHG reductions that would not otherwise occur. To ensure funds are being used to maximize emission reductions, the Legislature should target funds to projects and programs with the greatest emission reduction per dollar spent.

Target Spending to Reduce Overall Costs. To the extent reducing the overall costs of emission reduction activities is a priority, the Legislature could target spending to cost–effective emission reduction activities that cap–and–trade and other existing regulations and programs do not already encourage. For example, cap–and–trade might not provide adequate incentive in the private sector for research and development activities on GHG–reducing technologies because the benefits of such activities can “spill over” to other companies that can profit by implementing developments made by others in their own products. As a result, private companies do not always invest in research and development activities at a level that is socially optimal. Thus, there could be a rationale for providing some state funding in this area.

Using auction revenue to encourage more cost–effective emission reductions should be based on an analysis of (1) gaps in other regulations and programs and (2) how state funds can be best targeted to address these gaps. State law currently requires the administration to provide such an analysis as part of its Three–Year Investment Plan. However, in our view, the administration’s analysis to date has been lacking. The administration’s draft investment plan released in December 2015 provides limited data or analysis that can be used to identify gaps in existing programs and regulations, the extent to which additional state funding is needed, or how funding could be targeted to address these gaps in a cost–effective manner. (For more information on the ways in which the administration’s approach to the Second Investment Plan is lacking, see our September 2015 online report Framework for Cap–and–Trade Investment Plan Needs Further Development.)

The Legislature could consider requiring the administration to provide a more robust analysis of the ways in which existing regulations and programs do not provide adequate incentive for consumers and businesses to make cost–effective reductions. Such an analysis can be difficult because it relies on a strong understanding of complex economic market conditions that exist for different types of emissions. To help ensure a robust analysis, the Legislature could require the administration to establish an expert panel of economists and other outside experts to provide guidance on identifying market conditions in which current federal and state programs fail to provide adequate incentives for energy technologies. This information could then be used to: (1) target auction revenues to programs that best address these market conditions and (2) direct state agencies to evaluate project applicants based on their ability to address these market conditions.

Prioritize Other Legislative Goals. If the priority is to address other climate–related goals, the Legislature may want to consider directing the administration to give greater weight to some of these other benefits when allocating funds. For example, GHG reductions are one of the primary evaluation criteria used to evaluate Transit and Intercity Rail Capital Program applications. Benefits to disadvantaged communities, such as reduced air pollution, are a secondary evaluation criteria. The Legislature could direct state agencies to give greater weight to other goals when evaluating applications for funding, such as air quality or preparing for the effects of climate change in disadvantaged communities. The Legislature would have to balance the potential benefits of achieving greater non–GHG benefits against the potential greater legal risk of targeting the money less towards GHG reductions.

Offset Other Types of State Spending to Enable Greater Budget Flexibility. If the priority is to achieve greater flexibility, the Legislature could use auction revenue to offset spending from other sources of state funds, including special funds and the General Fund, that are currently being used for GHG reduction–related activities. Using revenues to offset other state spending could free up state funds to be used for other legislative priorities, which could include reducing fees or taxes. For example, the Legislature could consider using the additional revenue to offset special fund spending on certain climate related activities, such as the Alternative and Renewable Fuels and Vehicle Technology Program. Similarly, using auction revenue to offset General Fund spending on activities such as energy conservation activities in state buildings would make additional General Fund dollars available for other legislative priorities. The current amount of potential General Fund offsets is unclear. Our past efforts have found limited General Fund expenditures on activities that reduce GHGs.

Removal of Requirements to Spend on GHG Reductions by Reauthorizing Cap–and–Trade With Two–Thirds Vote

Alternatively, the Legislature could reauthorize the cap–and–trade program with a two–thirds vote and clarify that ARB has the authority to conduct auctions. It could reauthorize the program only through 2020 or, to the extent the Legislature determines it would like to use cap–and–trade to achieve post–2020 GHG reductions, it could authorize the program beyond 2020. In either case, authorizing the program with a two–thirds vote would (1) give the Legislature greater flexibility to return the revenue directly to households and businesses and/or use the funds to address its highest priorities and (2) reduce legal uncertainty about the future of the program. Under this approach, the state would still meet its GHG emissions target from capped sources for as long as a well–designed cap–and–trade regulation was in place.

Flexibility to Return Funds Directly to Households and/or Businesses. Since generating revenue for other state programs is not the primary goal of a cap–and–trade program, the Legislature might want to consider returning most or all of the revenue to households and businesses in the form of rebates or tax reductions. This option is likely unavailable under the current legal framework because it has no clear connection to GHG reductions. However, it would help promote the Legislature’s goal of minimizing costs for households. It would be important to provide the rebates or tax reductions in a way that does not interfere with the price signal provided by the cap–and–trade program. This could be done by issuing a rebate check directly to California households and businesses in an amount not tied to their energy consumption or GHG production, which is similar in concept to the Climate Credit provided to IOU customers. An alternative approach would be to use the funds to reduce taxes. For example, the funds could be used to reduce the state sales tax rate which would provide financial benefits to all California households. The Legislature could also use the funds to expand the state’s Earned Income Tax Credit (EITC). (For more details on the considerations of structuring a state EITC, please see our 2014 report Options for a State Earned Income Tax Credit.) This would have the benefit of minimizing costs for low–income households, as well as the potential policy benefit of increasing incentives for full–time labor force participation.

Flexibility to Use Revenue to Promote Highest Legislative Priorities. To the extent the Legislature determines additional revenue is needed to achieve other policy priorities, reauthorizing cap–and trade with a two–thirds vote would provide greater flexibility to use the funds in a way that efficiently promote its highest priorities whether those are climate change–related or not. For example, the Legislature could use the revenue to fund the highest priority transportation infrastructure projects or increase rates for certain health care services.

If additional climate–related activities are a high priority, the Legislature would also have the flexibility to target some revenue to achieve these benefits. For example, the Legislature could target the funds to activities that provide the greatest air quality benefits for disadvantaged communities or best prepare the state for the effects of climate change. It could also use a portion of the funds for GHG reductions, such as reductions from uncapped sources or cost–effective GHG reductions that other regulations are not achieving.

We note that not all projected auction revenues have been appropriated by the Legislature. Therefore, absent any adverse court rulings against the state, a significant amount of revenue collected under the current cap–and–trade authority will be available for GHG reduction activities. We estimate that roughly $1.6 billion in auction revenue will be available by the end of 2015–16. As indicated earlier, the Governor’s proposed budget includes a plan to spend these funds, as well as additional cap–and–trade auction revenues collected in 2016–17.

Might Be Needed to Remove Post–2020 Legal Uncertainty. As discussed above, uncertainty about ARB’s current authority to operate a cap–and–trade program beyond 2020 can lead to problems, such as costly investment decisions. Therefore, the Legislature should consider clarifying whether ARB has the authority to continue to operate a cap–and–trade program beyond 2020 or not. In our view, to the extent the Legislature has post–2020 GHG goals, it should consider relying on market–based approaches such as a cap–and–trade regulation (or a carbon tax) to achieve a significant portion of the GHG reductions. Market–based approaches are generally the most cost–effective strategies for reducing emissions.

If the Legislature determines that it wants to provide ARB authority to operate cap–and–trade beyond 2020, it is unclear whether providing such authority would require a simple majority vote, or whether a two–thirds vote would be needed. In 2010, voters approved Proposition 26, which required a two–thirds vote of the Legislature to pass some state charges that previously could be passed with a majority vote. It is unclear whether cap–and–trade auction revenue is one of the types of charges that now requires a two–thirds vote. If the Legislature authorized the program beyond 2020 with only a majority vote, it is possible the courts would determine this a violation of Proposition 26. The Legislature could remove legal uncertainty about the ability to operate cap–and–trade beyond 2020 if it extended the program with a two–thirds vote.

Conclusion

With regard to the Legislature’s GHG emission goals (including post–2020 goals), we believe that relying heavily on market–based approaches such as cap–and–trade would help to achieve GHG reductions in a cost–effective manner. Market–based approaches generally result in additional state revenue, even though that is typically not the primary goal of the program. In this report, we present strategies for using the revenue under two alternative scenarios: (1) under a legal framework that requires the state to spend auction revenue on GHG reduction activities and (2) removing the legal requirement to spend on GHG reductions by reauthorizing the cap–and–trade with a two–thirds vote. Removing the legal requirement that all resulting auction revenue be spent on activities that reduce GHGs would provide the Legislature maximum flexibility to (1) return the revenue to households and businesses in California to offset costs associated with higher energy prices under the program and/or (2) use the revenue to address other policy priorities. Moreover, as long as a well–designed cap–and–trade program is in place, the state will likely meet its GHG emission targets from major sources of emissions.