Given the size and complexity of the state's budget, California frequently faces litigation in a variety of policy areas. Usually, the magnitude of the state's fiscal exposure associated with this litigation is small or moderate. This year, three legal challenges pose a potentially larger fiscal concern:

During the 1970s and early 1980s, there were extensive efforts in the courts, federal government, and the states to improve special education services for children with disabilities. These efforts sought to ensure that children receive special education services reflecting their individual needs, and that school districts avoid categorizing children by handicap. To facilitate these changes, the California Legislature enacted its Master Plan for Special Education (MPSE) (ChapterĀ797, Statutes of 1980 [SB 1970, Rodda]).

In 1981, the Riverside County Superintendent of Schools filed a claim for reimbursement of the "state-mandated" costs of complying with the master plan's requirements. Article XIII B, Section 6, of the California Constitution generally requires the state to reimburse local governments if the state has required local governments to provide a "new program" or "higher level of service." Riverside's mandate claim--which extends to all local agencies providing special education services--has slowly worked its way through most of the claims reimbursement process, after twice going to court over the interpretation of Article XIII B.

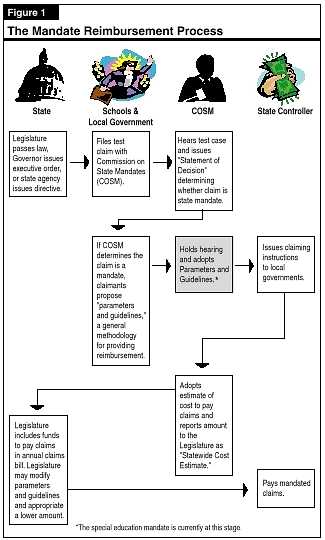

Pursuant to state law, local claims for mandate reimbursement are evaluated by the COSM, a quasijudicial body comprised of representatives of the Department of Finance, State Treasurer, State Controller, Office of Planning and Research, local school boards, cities or counties, and the public. FigureĀ1 (see next page) provides an overview of the mandate reimbursement process. For any mandate, the COSM typically takes three important actions--it adopts:

In 1992, an appellate court found that most of the MPSE was a federal mandate, not subject to the reimbursement provisions in the State Constitution. The court instructed COSM, however, to review state and federal law to determine the extent to which any specific activities in the state's MPSE surpassed the requirements of federal law.

In November 1998, the COSM issued a statement of decision identifying eight minor components of the MPSE as state mandates. While any single school district's costs to comply with these eight requirements would be very low, given the number of years since the initial special education claim and the number of school districts potentially eligible for reimbursement (up to 1,000), there has been significant concern about the possible magnitude of the state liability.

Within months of COSM issuing a decision establishing that a state requirement is a mandate, COSM usually adopts P&Gs specifying the general reimbursement methodology. Shortly thereafter, the magnitude of the state's liability becomes apparent as local agencies begin filing reimbursement claims. In this case, however, there has been substantial

controversy delaying COSM's adoption of the P&Gs. Specifically, the state contends that annual state budget appropriations for special education should count as an "offset" in the reimbursement methodology, while the claimants contend that these general appropriations should not be counted. (We discuss this "offset" issue below.)

In December 1999, after 13 months of debate, the special education claimants and state representatives agreed to (1)Āpostpone until June 29, 2000 the final COSM hearing on the adoption of the mandate's P&Gs and (2)Āattempt to negotiate a settlement. The parties' agreement, however, specifies that either party can end negotiations and request resumption of the hearing on the P&Gs if it believes the negotiations to be ineffective. The parties also agreed to report to COSM on the status of their negotiations on MarchĀ15, 2000.

In recent months, there have been numerous reports citing a potential state special education mandate liability of $1.6Ābillion. Below, we discuss the source of this number and explain why we belief the state's liability would be much lower, if anything.

Shortly after COSM issued its decision finding eight activities to be state mandates, the school district claimants submitted their proposed P&Gs. The Department of Finance (DOF), in turn, estimated the cost of the mandate for a sample year, 1996-97, using the proposed P&G methodology. In developing its estimate, the DOF indicated that their estimate constituted a "maximum possible" cost estimate because it used assumptions favorable to school districts when needed data were not available. In addition, the DOF asserted that the proposed methodology used in the claimant's P&Gs was overly generous to districts in several respects. As FigureĀ2 (see next page) indicates, the DOF estimated the cost of reimbursing claimants under their proposed methodology to be about $140Āmillion for the sample year.

The California School Boards Association, in turn, adjusted the DOF estimate for annual changes in inflation and the number of special district students served over the two decades to arrive at a total liability of $1.6Ābillion. This estimate cited by the school board association contains both the favorable assumptions of the DOF estimate and the overly generous methodology implicit in that estimate.

Our review of the DOF estimate found that the assumptions used result in costs that are overestimated by as much as one-third.

| Figure 2 | ||

| Special Education Mandates Identified by the Commission on State Mandates in 1998 | ||

| (In Millions) | ||

| Annual Costa | ||

| Maximum Age Limit. Provide special education services for students who become 22 years old while receiving services. Federal law requires services until age 21. | $7.9 | |

| Specialist Caseload Maximums. Monitor specialist caseloads to ensure they do not exceed a specified number of students. Federal law does not specify caseload maximums. | 4.3 | |

| Community Advisory Committees. Establish local advisory committees that include specified school personnel. Federal law does not require the local committees. | 2.6 | |

| Extended School Year. Provide at least 20 days of extra school for all special education students requiring an extended year (even if the full 20 days are not required by a student's individual plan). Federal law requires extended school year if required by a student's individual plan. | 51.0 | |

| Interim Placement. Involve a student's instructional team in the interim placement of a special education student who transfers to another district. Federal law permits fewer people involved in the decision under certain circumstances. | 8.1 | |

| Governance Structure. Involve representatives of parents and teachers on local Special Education Local Plan Areas (regional administrative agencies). Federal law contains no such mandate. | 0.7 | |

| Written Parental Consent. Obtain written parental consent of a student's IEP. Federal law does not require written consent. | 3.6 | |

| Resource Specialist Program. Provide instructional aides to at least 80 percent of certain specialists. Federal law requires staffing as identified in a student's individual plan. | 60.7 | |

| Total | $138.8 | |

| a Department of Finance estimate of maximum reimbursement amount (1996-97). | ||

Actual costs would be even lower if the COSM reflected some of the DOF's proposed changes to the claimants P&G methodology. Even with these reductions, however, the past-years' cost of the mandates would still be quite large, probably in the range of $500Āmillion to $1Ābillion, with additional annual costs of at least tens of millions of dollars.

Under mandate law, funds which the state provides to help local governments implement a mandate are called "offsetting revenues" and reduce the state's liability on a dollar-for-dollar basis. Counting as an offset some of the billions of dollars the state appropriates for special education in the annual budget act, therefore, could reduce or eliminate the state's fiscal liability. This issue of counting previous state appropriations for special education is central to the negotiations between the school districts and the administration. Few previous mandate claims, however, have relied upon this provision and its legal parameters have not been fully explored.

In general, the claimants contend that the state's previous appropriations should not be counted because the state, when enacting the MPSE, agreed to pay all increased program costs not reimbursed by the federal government. Claimants argue that the state has broken its commitment to maintain local special education costs "frozen" at their 1979 levels and that school districts have had to spend their state funds to meet the special education requirements set forth in federal law.

Claimants also contend that the state funding provided in the MPSE legislation and annual budget acts does not meet the statutory definition of an offset.

Specifically, they argue that Government Code

Section 17556 (e) requires offsetting revenues be identified as "specifically intended to fund the costs of the state mandate" and that the funds be included

in the same statute that creates the mandate.

In fall 1999, we submitted two reports to COSM and the Legislature regarding this special education mandate. Below, we summarize information we provided regarding the claimants' allegations.

In the development of any significant legislation, differing statements regarding its intent typically emerge. To ascertain the legislative and administrative intent with regards to the financing elements of the MPSE, we examined the fiscal system enacted in the measure and the bill analyses commenting on the development of that fiscal system. Our review found no evidence that the Legislature committed to pay all increased special education costs. Rather, the fiscal model contained in the MPSE treats special education--like other education programs--as a shared responsibility of state and local government. This shared responsibility is particularly apparent from the two elements featured prominently in the MPSE financing model: the (1) enrollment cap and (2) deficit factor.

Legislature Capped Number of Students Funded. For any school agency providing special education services, the MPSE specified that the state would not reimburse costs to provide services for more than 10Āpercent of its general student population. The DOF bill analyses at the time referred to this percentage cap as "one of the most significant fiscal aspects" of the master plan because the enrollment cap was set at a level that was lower than:

Thus, the enrollment cap was a clear attempt by the Legislature to limit state fiscal liability and to share some special education program costs with local agencies.

Deficit Factor Limited State Costs. The state's Master Plan also included a powerful state fiscal "safety valve," allowing the state to unilaterally and unconditionally reduce its total special education costs in any year. Specifically, Article 10 of ChapterĀ797:

From this review, we saw no evidence that the state guaranteed to pay all future cost increases for special education.

The Master Plan legislation provided $619Āmillion in state aid for special education. This amount reflected an approximately $160Āmillion increase in state support for special education over the prior year, and a $90Āmillion increase in state aid over the amount required by then current law. This $90Āmillion increase was the basis for the statements in bill analyses (developed by this office, other legislative fiscal staff, and the DOF) that the bill included sufficient sums to offset the cost of any state mandate included in the legislation.

The use of the $90Āmillion was not specifically earmarked by the Legislature to cover the costs of the eight "state-mandated" activities because:

As described above, $1.6Ābillion appears to be a significantly overstated estimate of the cost to reimburse claimants under the terms of their own P&Gs. Moreover, there is a strong argument for modifying the reimbursement methodology to include part of the annual state special education appropriation. Counting these revenues as an offset would reduce or eliminate any remaining state mandate liability.

We note, however, that--at the urging of COSM--discussions regarding the development of the P&G reimbursement methodology are occurring behind closed doors. In addition, the Legislature is not represented on COSM. Thus, it is possible that COSM may enact a P&G methodology for this mandate that does not reflect the Legislature's perspective. It is also possible that the claimants and administration could reach an agreement calling for alternative education relief provided in the budget. Given this, we discuss options available to the Legislature under either of these scenarios.

As noted above, it is not clear that the state has any fiscal responsibility to pay a mandate claim for special education. If, however, the commission finds some state liability, the Legislature has significant options available to it. Specifically, the Legislature could:

We discuss these options below.

Modify P&Gs. As shown earlier in FigureĀ1, to request an appropriation to reimburse local agencies, COSM must submit to the Legislature a claim's P&Gs and a statewide estimate of the mandate's cost. Government Code Section 17612 specifies that the Legislature may amend, modify, or supplement these P&Gs and appropriate a different sum for reimbursing local agencies. Such an action must be done carefully, however. If the Legislature deletes funding for a mandate, a local agency may file an action in court to declare the mandate (in this case, the eight state-mandated activities) unenforceable and/or bring other legal actions seeking reimbursement for mandated costs. Thus, any change to the P&Gs or mandate reimbursement amount must be supported by sound legal reasoning.

Alter Timing of Reimbursement. Ordinarily, the state pays all prior years' cost of a mandate at once. Given the potential magnitude of the state's liability, however, the Legislature may wish to consider scheduling any mandate's repayment over a series of years. While the state would accrue interest on any claim paid more than a year after COSM adopts its statewide cost estimate, state law specifies that interest is charged at the Pooled Money Investment Account rate. Accordingly, the state's interest cost for postponing full payment on the mandate claim would be the same as its earnings from leaving the funds in the Pooled Money Investment Account. Thus, the state would not incur any real costs to schedule repayment of the claim over time, but would gain some funding flexibility.

Eliminate Future Mandate Liability. In 1997, the Legislature streamlined special education funding in order to increase local flexibility and reduce the impact of funding rules on local program decisions. The creation of new reimbursable mandates would partially negate these reforms by establishing funding formulas that could influence local program practices. To minimize the impact of these mandates on local decisions and to eliminate the state's liability for mandate costs in the future, the Legislature could enact legislation to make optional or eliminate the eight programs identified by COSM as state mandates.

Impact on PropositionĀ98 Guarantee. Our review indicates that the Legislature could fund special education mandate costs from funds already required under the guarantee. For example, past mandate costs could be repaid over several years from one-time PropositionĀ98 funds that are available in the budget process in most years. Future costs could be accommodated within the amounts provided annually under the existing PropositionĀ98 formula.

It is also possible that the negotiations between the administration and claimants could result in a proposal to drop the mandate claim and provide alternative education funding in the budget. There are two reasons such an approach may be proposed by the administration and claimants.

Thus, a budgeted solution--providing schools funds through the state budget rather than the mandate claims reimbursement process--may be preferable to the administration and claimants.

Should the administration and claimants propose to drop the mandate claim in exchange for increased state funding in the budget, the Legislature would have full authority over the proposal. For example, the Legislature could modify the level of funding proposed, or the use of its resources. Similarly, the Legislature could provide school funding in the budget using one-time funds (which do not affect the PropositionĀ98 guarantee) or through an ongoing program which is included within the guarantee.

For four years in the early 1990s, the state faced annual budget gaps of $4Ābillion to $14Ābillion. To close these gaps, the Legislature and administration raised fees and taxes, cut programs, deferred costs, transferred costs to the federal government, and shifted property taxes from local governments to schools.

While the formulas underlying the property tax shifts were very complex, the concept was simple: shifting property taxes from local governments to schools reduced, on a dollar-for-dollar basis, the amount the state was required to spend for schools. In this way, the property tax shifts played a critical role in helping the state resolve its severe budget difficulties.

Because the property tax shifts were implemented on a permanent basis, cities, counties, and special districts continue to receive a smaller share of property taxes than they did before the tax shifts--and schools receive a larger share. In the budget year, the property tax shifts redirect about $4Ābillion of property taxes from local governments to schools. This increased local funding offsets a commensurate amount of state education spending.

Shortly after the property tax shifts were enacted, local governments sought to overturn the actions in court on the grounds that (1) the state lacked the authority under Article XIII A of the State Constitution to reallocate property taxes to increase school funding and (2) the shifts violated local governments' "home rule" authority in the State Constitution. The courts rejected these arguments.

In December 1997, the County of Sonoma initiated a different challenge to the property tax shifts. Specifically, the County of Sonoma (joined later by most other counties) filed a claim with the COSM, arguing that the property tax shifts represent a reimbursable mandate. In its filings, Sonoma County argued that the state transferred part of its school funding responsibility to local governments and, thus, under Article XIII B, Section 6, is eligible for reimbursement. In November 1998, the commission issued its decision, rejecting the test claim on the basis that a reduction of revenue previously allocated to a local government does not qualify as a reimbursable mandate. Specifically, the commission found that there was "no local expenditure" within the meaning of the Constitution because the disputed property taxes are transferred directly to schools. That is, local governments never "see" these monies; they are withheld by the county auditor and deposited into a school fund.

In March 1999, the County of Sonoma petitioned the Sonoma County Superior Court to set aside the commission's decision regarding the property tax shifts. In October 1999, the court concluded that the property tax shifts created a new program or higher level of service because they compel local governments to accept partial financial responsibility for a state program--schools. The court also found that the commission erred in concluding that the Constitution requires local governments to spend tax proceeds for a program as a prerequisite for reimbursement. The court said "It is sufficient that the financial responsibility or cost of the program be shifted from the State to the local government." Accordingly, the court ordered the commission to find that the property tax shifts constitute a reimbursable mandate and to make a determination as to the amount of money that should be reimbursed. The state is appealing this decision. No court date had been announced at the time this analysis was prepared.

The ruling by the Sonoma County Superior Court represents a major change from previous interpretations of the state reimbursement requirement. In the past, the state has reimbursed local governments' costs to implement a new program or higher level of service. Under this ruling, the state would be responsible for reimbursing a loss of revenue. Many legal experts are skeptical as to whether the court's rulings will be upheld on appeal. If the ruling is upheld, however, the state's fiscal liability could be high, given the billions of property taxes that have been shifted to schools under the property tax shift laws.

Magnitude of Revenues Potentially Affected. Although the test claim was submitted by the County of Sonoma, the mandate ruling would apply to all local governments sustaining property tax shift losses: cities, counties, and special districts. In addition, state law specifies that test claims, submitted before the end of a calendar year, extend to costs dating from the prior fiscal year. Thus, local governments could be eligible for reimbursement for property taxes shifted since 1996-97. By the end of the budget year, the amount of property taxes shifted since 1996-97 would total over $13Ābillion.

Offsetting Revenues. Since the first proposal for a property tax shift, the Legislature has worked to mitigate its fiscal effect. Both the 1992-93 and the 1993-94 property tax shifts were enacted in tandem with relief measures. In addition, as the state's fiscal condition has improved, the Legislature has enacted additional relief measures. An earlier publication by our office, Shifting Gears: Rethinking Property Tax Shift Relief (February 1999), provided an accounting and perspective on these relief measures. In 1998-99, for example, we estimated that mitigation measures enacted by the state offset more than 60Āpercent of local government property tax shift losses.

As discussed earlier in this document, however, previous test claims before the commission and the court have not clarified the terms under which state support constitutes an "offsetting revenue" for purposes of mandate reimbursement. A strict reading of the Government Code suggests that offsetting revenues should be appropriated in the legislation that creates the mandate and should be explicitly earmarked for the purpose of mandate relief. In this case, however, some of the property tax shift relief measures were enacted after the property tax shifts (such as trial court funding reform and the Citizens Option for Public Safety program) and the provision which provides the greatest amount of revenues, the half-cent public safety sales tax, was enacted as a voter approved proposition (Proposition 172). Thus, if the Sonoma County Superior Court opinion is upheld on appeal, it is possible that the commission may not consider all the state's mitigation measures as an offset to the state's liability.

Given the history of other complicated mandate claims (such as the special education mandate discussed earlier), resolution of this claim could take years. While it is possible that the superior court's ruling may be overturned, given the magnitude of revenues at stake it is important for the Legislature to monitor the lawsuit and take action to minimize its potential liability.

Changes to State Law Regarding Offsets. In order to clarify how the commission should consider state subventions to local governments in the context of mandate reimbursement, we recommend the Legislature reexamine Government Code Section 17556. For example, the Legislature may wish to modify the provision to specify that offsetting revenues may be provided in legislation enacted after the legislation which imposes the mandate, or through the annual budget process.

Existing Local Relief Programs. In any legislation to extend or modify an existing program which was enacted to mitigate the impact of the property tax shifts, the Legislature may wish to include language stating this intent. Similarly, the Legislature may wish to include language in legislation directing COSM to consider this relief in any calculation of property tax shift mandate liability. Our earlier publication, Shifting Gears: Rethinking Property Tax Shift Relief, provided a list of programs which were enacted with the clear or implied goal of mitigating the property tax shifts.

New Local Relief Programs. Over the years, the Legislature has provided local relief in many ways, such as: one-time grants, annual subventions, and by assuming partial (or full) financial responsibility for local programs. Under the State Constitution, a legislative act to discontinue a grant or subvention program typically does not create a reimbursable state mandate. Discontinuing state support for a program for which the state has assumed responsibility, on the other hand, can constitute a mandate. Given the Sonoma County Court ruling and its associated large state fiscal liability, we recommend the Legislature use care to preserve a significant amount of control over the level of state funding for local assistance programs. Accordingly, in evaluating any new local fiscal relief program, we recommend that the Legislature be cognizant of whether the state could eliminate the program in the future without imposing another mandate.

Local Finance Reform. As we discuss extensively in another analysis in this part--Reconsidering AB 8: Exploring Alternative Ways to Allocate Property Taxes--California's system of property tax allocation and local finance has significant flaws. In ChapterĀ94, Statutes of 1999 (AB 676, Brewer), the Legislature stated its intent to revamp the tax allocation system and improve local finance. This pending mandate claim, and its associated large state fiscal liability, brings uncertainty to the current discussions regarding finance reform. This is because reaching agreement on reform:

This mandate claim dispute, however, need not impede progress towards reform. For example, if the Legislature developed a local reform proposal which included constitutional changes, the Legislature could specify the resolution of this property tax shift mandate claim in the measure placed before the voters. (In that way, the two matters--finance reform and the mandate claim--could be resolved together.) Similarly, if the Legislature wished to enact local reform by establishing pilot projects in some communities, the Legislature could specify that the reform program would be available to only those local governments which waive their right for property tax shift reimbursement. Finally, the Legislature could enact a statewide reform measure, but place a "poison pill" in the measure to protect the state's fiscal interests. For example, the Legislature could specify that some funding for the reform proposal is eliminated if any local government submits a claim for property tax shift reimbursement. Thus, while the pending lawsuit complicates matters, it need not stop progress toward needed reform.

ChapterĀ453, Statutes of 1990 (AB 1109, Katz) imposed a Smog Impact Fee of $300 on out-of-state vehicles when the vehicle is registered for the first time in California. According to ChapterĀ453, the fee was implemented to ". . . ensure equity between owners of California-certified vehicles and other vehicles, provide funding for environmental programs, and to promote good health and safety standards."

In October 1999, the California Court of Appeals ruled that the Smog Impact Fee violated the commerce clause of the United States Constitution (Article I, Section 8, clause 3) and Article XIX of the California Constitution. The court's judgment provided for fee refunds for the four people who were parties to the court action. The state is not appealing this decision.

As a result of the court's decision, the Governor directed the Department of Motor Vehicles (DMV) to stop collecting the fee and indicated his intent to refund all persons who paid the Smog Impact Fee. Below, we discuss the:

To date, over $500Āmillion in smog impact fees have been collected (see FigureĀ3). Through 1997-98, the proceeds of the fee were deposited into the General Fund (about $410Āmillion in total). Beginning in 1998-99, proceeds of the fee were deposited into the High Polluter Repair and Removal Account (HPRRA), pursuant to ChapterĀ802, Statutes of 1997 (AB 208, Migden).

| Figure 3 | |

| Smog Impact Fee Collections | |

| (In Millions) | |

| Fiscal Year | Amount |

| 1990-91 | $31.2 |

| 1991-92 | 50.2 |

| 1992-93 | 44.3 |

| 1993-94 | 44.9 |

| 1994-95 | 49.6 |

| 1995-96 | 56.1 |

| 1996-97 | 63.3 |

| 1997-98 | 70.1 |

| 1998-99a | 76.5 |

| 1999-00a | 21.3 |

| Total | $507.6 |

| a Fee collections deposited in the High Polluter Repair and Removal Account. | |

Two programs currently use funding from the HPRRA:

After the Smog Impact Fee was declared unconstitutional, the state directed some proceeds from the Smog Abatement Fee (paid by owners of newer cars in lieu of biennial smog check) into the HPRRA to fund both the LIRAP and VRP. Thus, funding for these programs is not affected by the court's decision.

When prior account balances and earned interest are accounted for, we estimate the HPRRA contains approximately $100Āmillion that could be used to fund refunds of the Smog Impact Fee.

Currently there are six bills related to the Smog Impact Fee pending before the Legislature. As FigureĀ4 (see next page) indicates, most of these bills repeal the provisions of law creating the fee and provide fee refunds. In addition, the Governor's budget includes $672Āmillion ($562Āmillion from the General Fund and $103Āmillion from the HPRRA) for Smog Impact Fee refunds--a level of funding consistent with the proposals pending before the Legislature. This amount assumes that refunds would be provided to all eligible persons.

| Figure 4 | |

| Smog Impact Fee Major Provisions of Pending Legislation |

|

| As of January 28, 2000 | |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| (Same provisions as AB 1702 above.) | |

|

|

|

|

|

|

|

|

|

|

|

|

In reviewing these various proposals, the Legislature has numerous options as to how to structure the refund program. We discuss some of these options below.

Amount of Interest to Include in the Refund. The Revenue and Taxation Code provides certain interest rate calculations for tax payments. These rates vary in amount--some are equal to a set amount (for instance, 3Āpercent of the total tax payment) and others are calculated (for example, equal to the state's Pooled Money Investment Account rate). Because there is no interest rate specified for the Smog Impact Fee, we believe the Legislature has the discretion to set this interest rate.

Source of Funding for the Refunds. As we mentioned previously, the state's liability to pay these refunds could be in excess of $650Āmillion. (This amount will vary depending on the interest rate used to calculate the refund.) Given that the HPRRA contains only about $100Āmillion, any large scale refund program will require a significant contribution from the General Fund.

Implementing the Fee Refund. The bills pending before the Legislature when this analysis was prepared included different methods of notifying consumers of the fee refund and disbursing the refund to consumers. We believe the Legislature has many options for notifying consumers and paying the refund. For example, the state could send letters to all consumers identified by the DMV as having paid the fee, or the state could allow consumers to contact DMV and request a refund. Regardless of how consumers are made aware of the refund program, we believe requiring some type of verification is appropriate. In addition, we believe the refund check should be paid by the State Controller, given that office's expertise in reviewing claims and disbursing revenues.

Three legal challenges pose some fiscal concern to the state. Two of these--special education and the Smog Impact Fee--may be resolved during the budget year. As we discuss above, the cost of addressing these issues depends, to a significant extent, on policy choices of the Legislature. For instance, in the case of special education, the Legislature has significant authority to alter the magnitude and timing of any funding provided, as well as the extent to which the funding affects the PropositionĀ98 guarantee. In addition, while the resolution of the property tax shift claim may be years away, the Legislature could act now to reduce any potential fiscal liability. Finally, six bills are currently before the Legislature, each proposing a different approach to the Smog Impact Fee issue. The magnitude of the state's fiscal liability will depend on the Legislature's choices regarding the terms of the refund, the interest rate paid, and the extent of fee-payer verification required.