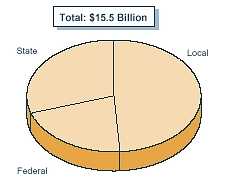

• Transportation in California is funded from a variety of state, local, and federal fund sources.

State Funds

• State funds consist primarily of the state excise tax on gasoline and diesel fuels and truck weight fees.

• Additional fund sources include most of the state sales tax on diesel fuel, a small portion of the state sales tax on gasoline, bond proceeds, and appropriations of General Fund revenue.

• In 1999-00, state funds are estimated to provide about $4.5 billion

for transportation purposes.

Federal Funds

• Federal transportation funds are apportioned to California based on the state's contribution to the federal Highway Trust Fund through federal taxes on gasoline and diesel fuel.

• In 1999-00, California is estimated to receive about $3.3 billion in federal transportation funds.

Local Funds

• Over one-third of local funds for transportation are derived from optional local sales taxes (on all sales, not just gasoline) dedicated for transportation purposes.

• In 1999-00, we estimate that local funds will constitute half, or about $7.5 billion of all revenues for transportation.

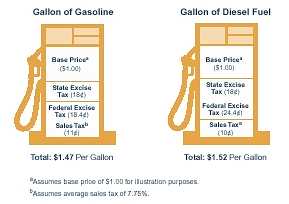

• State and federal transportation revenues are collected

primarily through the state and federal excise (per gallon) taxes on gasoline

and diesel fuel.

• Californians pay the following taxes at the pump:

• 18 cents in state tax for each gallon of gasoline and diesel

fuel (generally referred to as the "gas" tax).

• 18.4 cents in federal tax for each gallon of gasoline.

• 24.4 cents in federal tax for each gallon of diesel fuel.

• 7.25 percent uniform state and local sales tax, plus

optional local sales taxes for transportation or other purposes varying by county.

The majority of the uniform state and local sales tax proceeds are not

used for transportation purposes.

• The state also collects weight fees on commercial vehicles (trucks)

based on the unladen weight of the vehicle.

2000-01

(Dollars in Billions)

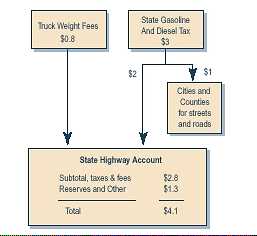

• The state receives about 65 percent of the revenues from the state

gasoline and diesel excise taxes, while cities and counties receive about 35 percent

for local streets and roads.

• The state's share of the gasoline and diesel tax revenues, along with

truck weight fees, are deposited in the State Highway Account (SHA).

• The California State Constitution (Article XIX) restricts the use of

state gasoline tax revenues for certain purposes. These monies may only be used

to plan, construct, maintain, and operate public streets and highways; and to

plan, construct, and maintain mass transit tracks and related fixed facilities

(such as stations). The gasoline tax revenues cannot be used to operate

or maintain mass transit systems or to purchase or maintain rolling stock (trains,

buses, or ferries).

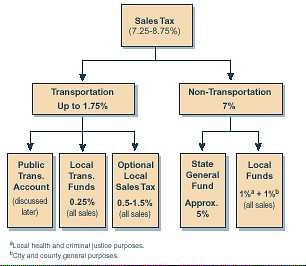

What the Sales Tax Rate Includes

• In addition to state and federal excise taxes paid on each gallon of

gasoline and diesel fuel, California imposes sales tax on most purchases, including

gasoline and diesel fuel.

• Statewide, there is a uniform sales tax of 7.25 percent on most purchases.

This sales tax rate can go up to 8.75 percent when optional sales taxes

are included. The sales tax rates paid in California are a combination of several

tax rates levied by the state and individual local governments.

• State Tax Rate. This is a 6 percent uniform rate which

includes a 5 percent General Fund rate, plus two one-half cent (totaling 1 percent)

special fund rates for local health care and criminal justice purposes. • Uniform Local Tax Rate. A 1.25 percent uniform rate is

levied in all counties. Of this total, 1 percent is allocated to cities and

counties for general purposes, while the remaining 0.25 percent is dedicated

to transportation.

• Optional Local Tax Rates. Local governments are authorized

to levy additional local sales taxes, with voter approval, for a variety of

purposes. These taxes are generally imposed in quarter-cent or half-cent increments

and generally cannot exceed 1.5 percent. (San Francisco and San Mateo Counties

are authorized to levy up to 1.75 percent to 2 percent in optional taxes, respectively.)

How Sales Tax Revenues Are Used

• Public Transportation Account. A small portion of the

sales tax on gasoline and the majority of the sales tax on diesel fuel is provided

to this account (as discussed in greater detail later). This account supports

mass transportation activities.

• Local Transportation Funds. A 0.25 percent uniform tax

on all sales is dedicated to transportation uses, primarily for transit.

• Optional Local Sales Tax. Optional sales taxes (0.5 percent

to 1.5 percent) may be imposed by local governments for transportation purposes.

These activities include highway construction, street and road maintenance,

and subsidies for transit operations.

• State General Fund. Essentially 5 percent of the uniform

sales tax is dedicated to the state General Fund.

• Local Funds. A 2 percent uniform sales tax provides revenues

for local purposes. One percent is dedicated to local health and criminal justice

purposes. The remaining 1 percent is for city and county general purposes.

2000-01

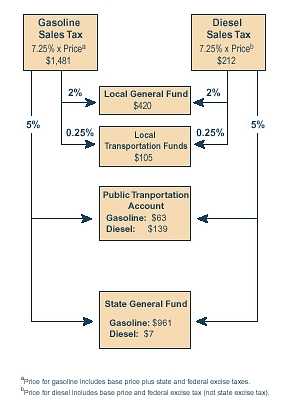

(Dollars in Millions) • Nontransportation Purposes. As the figure shows, the bulk

of sales tax revenues from the sale of gasoline and diesel goes to nontransportation

purposes. Of the total sales tax revenues ($1.7 billion) from these products

in 2000-01, about 82 percent ($1.4 billion) will go to local and state general

fund purposes. This includes $420 million for local general fund purposes and

almost 1 billion for state general fund purposes.

• Transportation Purposes. The portion of statewide sales

tax revenues dedicated to transportation will total about $307 million

in 2000-01 and goes to local transportation ($105 million) and the public

transportation account ($202 million). These funds are derived as follows:

• For each gallon of gasoline, the state sales tax of 4.75 percent

on 9 cents of the state excise tax—equivalent to 0.4275 cents per gallon

of gasoline (about $63 million in 2000-01)—goes to the Public Transportation

Account (PTA). The PTA is the primary source of state funds for mass transportation

purposes, and the only state transportation fund which can currently be used

to purchase rolling stock (that is, buses, trains, or ferries).

• State sales tax of 4.75 percent on the price of each gallon of

diesel fuel (including the federal excise tax, but not the state excise tax)

goes to the PTA (about $139 million in 2000-01).

• State sales tax of 0.25 percent on all sales is deposited

in the Local Transportation Fund (LTF) which is generally restricted to local

transit needs (about $1.1 billion in 2000-01 including about $105 million

from gasoline and diesel fuel sales).

| Transportation

Equity Act for the 21st Century

Major Provisions |

| (1998-2004) |

| Funding |

|

|

|

|

| Highways |

|

|

|

| Transit |

|

|

• Basis for State's Share. The state's share of funding for the major highway and transit programs is based on a variety of factors, including highway lane miles, congestion, population, and air quality. The state and local agencies may also apply for discretionary grants on an annual basis.

• State's Share of Federal Funds. Federal funds constitute about one-fifth of the state's transportation funding in 1999-00. (See figure on page 18.)