May 16, 2002

The Governor's May Revision addresses an enormous increase in the state's budget shortfall through a variety of spending reductions, tax increases, fund transfers, and additional borrowing. Overall, it is a credible plan which serves as a reasonable starting point for the Legislature as it considers its own priorities for 2002-03. At the same time, the proposal contains some risks and even with its adoption, the state would face additional shortfalls in the future.

As a result of a major decline in anticipated tax receipts, coupled with additional expenditure requirements for Proposition 98, the Governor has made substantial revisions to his January budget proposal. These involve significant amounts of new borrowing, new expenditure reductions, and tax increases. This report discusses the administration's revised revenue and expenditure projections, outlines the Governor's May Revision proposal for addressing the budget shortfall, and identifies key considerations for the Legislature as it evaluates the new budget plan.

Our Bottom Line. The May Revision provides a credible framework for addressing what has become an enormous budget problem. The administration estimates that it would result in a balanced budget by year end 2002-03. In large part, the plan appears to be workable and based on realistic estimates. However, it reflects a great many policy assumptions that the Legislature will need to carefully review to assure that the budget plan it ultimately adopts will reflect its priorities. It also contains various uncertainties and implications for future budgets.

Facing an economic downturn and declining revenues, the Governor's January budget had proposed a variety of actions to cover an estimated $12.5 billion budget shortfall. (The Legislature addressed part of this shortfall in the third extraordinary session by reducing current-year spending and replacing General Fund support for various capital projects with lease payment financing. In addition, the State Treasurer has restructured state debt payments resulting in General Fund savings in the current and budget years.) Since January, the revenue situation has deteriorated further, with total receipts in 2001-02 and 2002-03 now expected by the administration to fall by a combined $9.5 billion from the January budget forecast. In addition, expenditures are expected to exceed the January proposal by about $1.6 billion for the same period. These developments have pushed the cumulative budget shortfall higher by another $11.1 billion, to $23.6 billion.

New May Revision Proposals. In response to this major deterioration, the Governor has significantly revised his January budget, proposing a wide range of new spending reductions, tax increases, expanded borrowing, and funding shifts. Figure 1 shows, in broad terms, how the administration proposes to address the $23.6 billion shortfall. Compared to January, the May Revision includes:

|

Figure 1 Governor's Proposed Budget

Solutions |

|||

|

(In Billions) |

|||

|

Type of Solution |

January

2002 |

Additional |

Total |

|

Spending reductions |

$5.2 |

$2.4 |

$7.6 |

|

Loans/transfers/othera |

3.0 |

2.2 |

5.2 |

|

Tobacco settlement securitization |

2.4 |

2.1 |

4.5 |

|

Tax increases and accelerations |

0.2 |

3.7 |

3.9 |

|

Fund shifts |

0.6 |

0.7 |

1.3 |

|

Federal funding increases |

1.1 |

0.0 |

1.1 |

|

Total

proposed solutions |

$12.5 |

$11.1 |

$23.6 |

|

|

|||

|

a

Includes a variety of spending deferrals and revenue changes. |

|||

How Overall Proposal Addresses Shortfall. Reflecting the above changes, the Governor's updated plan would address about one-third of the total $23.6 billion shortfall through spending cuts. About one-fifth would be addressed through loans and transfers from special funds, and another one-fifth would be covered through the securitization of future tobacco settlement receipts. Finally, about one-sixth of the total solution is related to tax increases and accelerations.

Figure 2 shows the administration's projection of the General Fund condition, taking into account the proposals embedded in the May Revision. It shows that the General Fund would end the current year with a deficit of $1.6 billion. After taking into account the Governor's numerous budget-year revenue and expenditure proposals, 2002-03 would have a cumulative year-end reserve of $516 million.

|

Figure 2 Governor�s May Revision

General Fund Condition |

||

|

(In Millions) |

||

|

|

2001-02 |

2002-03 |

|

Prior-year fund balance |

$2,986 |

-$123 |

|

Revenues and transfers |

73,775 |

78,603 |

|

Total

resources available |

$76,761 |

$78,480 |

|

Expenditures |

$76,884 |

$76,491 |

|

Ending fund balance |

-$123 |

$1,989 |

|

Encumbrances |

1,473 |

1,473 |

|

Reserve

|

-$1,596 |

$516 |

|

|

||

|

Detail may not total due to rounding. |

||

Figure 3 shows the programmatic distribution of the 2002-03 General Fund expenditure total proposed in the May Revision. It indicates that virtually all major program areas except for Proposition 98 funding for K-12 education and community colleges would experience significant program reductions in 2002-03.

|

Figure 3 Summary of May Revision

Spending Proposals |

|||

|

(Dollars in Millions) |

|||

|

Program/Agency |

2001-02 |

2002-03 |

|

|

Amount |

Percent |

||

|

Education Programs |

|

|

|

|

K-12�Proposition

98 |

$26,474 |

$29,306 |

10.7% |

|

Community

Colleges�Proposition 98 |

2,577 |

2,808 |

9.0 |

|

UC/CSU |

7,201 |

6,912 |

-4.0 |

|

Health and Social Services |

22,103 |

20,934 |

-5.3 |

|

Youth and Adult Corrections |

5,544 |

5,339 |

-3.7 |

|

Business/Transportation/Housing |

645 |

223 |

-65.4 |

|

Resources/Environmental Protection |

1,981 |

1,144 |

-42.3 |

|

All Other |

10,359 |

9,825 |

-5.2 |

|

Totals |

$76,884 |

$76,491 |

-0.5% |

Overall, the administration has made relatively modest downward revisions to its January economic forecast. The updated projection assumes that the U.S. and California economies have already emerged from the 2001 recession, but that the pace of the renewed expansion will be modest through much of 2002. Key positive forces in the outlook are low interest rates, continued modest increases in consumer spending, and large gains in U.S. government spending on defense and home security. One negative factor is that the hoped-for rebound in business spending on computer-related products is taking longer to materialize than assumed in January. The administration's forecast now assumes that the pick-up in business spending will not occur until late 2002. This is a significant adverse factor for California, given the large presence of high-tech industries in this state. It implies that the economic expansion will be slightly less robust in 2002 than had been assumed in January.

On an average annual basis, real U.S. gross domestic product is projected to increase by 2.1 percent in 2002 and by 3.6 percent in 2003. In California, personal income is forecast to increase just 1.5 percent in 2002—reflecting the negative effect of continuing declines in stock options on wages during the year—before accelerating to 6 percent in 2003. The updated personal income forecast compares to the January budget's forecasts of a 2.6 percent increase in 2002 and a 7.5 percent increase in 2003.

Although the administration's downward economic adjustments contained in the May Revision are relatively modest, its downward revision to revenues is substantial. The key elements of the administration's revenue revisions are summarized in Figure 4. It indicates that:

|

Figure 4 May Revision Revenue

Changes |

||

|

(In Billions) |

||

|

|

2001‑02 |

2002‑03 |

|

January revenue forecast |

$77.1 |

$79.3 |

|

May Revision revenue changes: |

|

|

|

Change

in baseline forecast |

-$3.7 |

-$5.8 |

|

Policy-related

changes |

0.4 |

5.1 |

|

May Revision forecast |

$73.8 |

$78.6 |

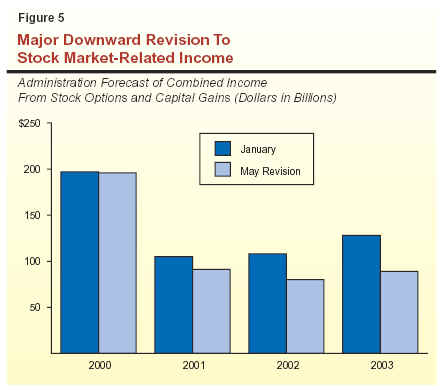

The large downward revision to baseline revenues in both the current and budget years reflects major reductions in personal income tax (PIT) receipts. The May Revision estimate of PIT revenues is below the administration's January forecast by $4.6 billion in the current year and $5.8 billion in the budget year. These declines are consistent with the much weaker-than-expected receipts from the PIT in the January through April period. The declines are partly related to a much reduced estimate of income from stock options and capital gains in 2001 through 2003. As shown in Figure 5, the combined income from these sources is now expected to be $91 billion in 2001 and $80 billion in 2002, or significantly less than the January budget projections of $105 billion and $108 billion for the same two years, respectively.

Of the $5.1 billion in policy-related May Revision increases in resources in 2002-03 noted earlier, about $2.4 billion is associated with increased tax revenues, $2.1 billion is due to an increase in the amount of future tobacco settlement revenues that the state is proposing to securitize, and the remaining $600 million is related to higher transfers (mostly from the Traffic Congestion Relief Fund).

As shown in Figure 6, the main tax-related provisions include:

|

Figure 6 May Revision Revenue

Proposals |

|

|

(In Millions) |

|

|

Revenue Increases |

Fiscal

Impact |

|

Cigarette taxes |

$475 |

|

�

Increase of $0.50 per pack |

|

|

Net operating loss deduction |

1,200 |

|

�

Two-year suspension |

|

|

Federal conformity measure |

255 |

|

�

Financial institutions' bad debts |

|

|

Withholding on certain transactions |

225 |

|

�

Various real estate sales |

|

|

Compliance and revenue accelerations |

281 |

|

�

Settlement, penalty waiver, protest, |

|

|

Subtotal |

$2,436 |

|

Expenditure

Decreases |

|

|

Vehicle license fee offseta |

$1,276 |

|

�

Increase in rate to 1.5 percent |

|

|

Total |

$3,712 |

|

|

|

|

a

Includes trailer coach fees for the General Fund. |

|

The May Revision also proposes a one-year rollback in the VLF rate reduction enacted previously—from 67 percent to 25 percent for calendar year 2003. This reduction will result in a temporary increase in the VLF paid by vehicle owners in 2003. If adopted, the change will result in a $1.3 billion reduction in General Fund expenditures needed to backfill local governments' VLF revenue losses during 2002-03. The state would also experience a reduction of $1.1 billion in backfill expenditures in 2003-04.

Current-Year and Budget-Year Revenue Outlook Reasonable. The administration's revenue forecast for the next 14 months is similar to our own projection. We estimate that revenues in the current year will fall about $500 million below the May Revision estimate, mostly reflecting lower PIT receipts and higher PIT refunds in May and June. In the budget year, however, we are forecasting that revenues will modestly exceed the budget projection by roughly $400 million. While we share the administration's assumption that the economic recovery will be modest in 2002, we also believe that revenue growth will be slightly stronger than the administration's forecast for two reasons: (1) we believe that the economic recovery will produce modestly larger increases in sales and corporation tax receipts than is assumed by the administration, and (2) the current increases in premiums being charged by insurers for all major lines of insurance will result in larger growth in the insurance tax next year. We also note that our office has lower PIT receipts resulting from stock options and capital gains in both 2001-02 and 2002-03. However, this is partially offset by higher receipts from other income sources.

Prior-Year Revenues Overstated. When it prepared the May Revision, the Department of Finance accrued about $600 million in bank and corporation refunds claimed by businesses in the current fiscal year back to 2000-01, on the grounds that the refunds were attributable to corporate activity that fell within the prior year. This adjustment should have the impact of raising collections in 2001-02 and reducing collections in 2000-01 by an equivalent $600 million. However, while the administration appropriately increased the current-year revenue totals, it did not make a corresponding reduction to 2000-01. As a result, the administration's incoming balance for the current year is $600 million too high, and the 2002-03 projected year-end General Fund reserve is overstated by $600 million.

Under the May Revision proposal, General Fund spending would fall 0.5 percent in 2002-03. Figure 7 summarizes the Governor's major proposals in different program areas. Some of these proposals are discussed in greater detail below, as well as the May Revision proposal for Proposition 98—K-14 reductions.

|

Figure 7 Key Expenditure-Related

May Revision Budget Proposals |

|

Education |

|

�

Defer $1.1 billion

in undisbursed K-14 Proposition 98 current-year appropriations to the

budget year. |

|

�

Suspend Governor�s January child care reform proposal. |

|

�

Reduce higher education funding for research, K-12

outreach, equipment, K-12 staff development, and other programs ($170.6 million

UC, $70.3 million CSU). |

|

Health Services |

|

�

Eliminate funding for

certain Medi-Cal optional benefits ($263 million). |

|

�

Rescind recent

expansion of Medi-Cal eligibility to some two-parent working families

($92.1 million). |

|

�

Reduce Medi-Cal county administration funding by 20 percent

($88 million). |

|

�

Postpone Healthy Families Program expansion to parents. |

|

Social Services |

|

�

Reduce county

administration funding for CalWORKs, Foster Care program, Food Stamps

program, and the |

|

�

Suspend federal COLA for SSI/SSP ($54.3 million). |

|

�

Funds 50 percent of federal penalty levied on the

state due to the delay in implementing a statewide automated child

support collections system ($89.7 million increase, half covered by

counties, half by General Fund). |

|

Criminal Justice |

|

�

Increase the Department

of Corrections budget to address workers� compensation shortfall,

increased costs for contracted medical services, and improvements in

inmate medical services consistent with the Plata lawsuit ($179.5 million

increase). |

|

�

Reduce Office of Criminal Justice Planning local

assistance grant programs by 50 percent ($19.4 million). |

|

Local Government |

|

�

Defer budget-year payments to local agencies for various

state mandate claims ($168 million). |

|

�

Redirect to schools

$120 million of property taxes from special districts and

redevelopment agencies. |

|

�

Reduce county

administered health and social services programs, as referenced above. |

|

�

Reduce local grants and

subventions for local law enforcement grants ($116 million),

Williamson Act ($39 million), booking fees reimbursements ($38 million),

high-technology law enforcement equipment ($17 million), and

libraries ($12 million). |

|

Statewide |

|

�

Eliminate 4,000

positions ($10 million). |

|

�

Reduce operating

expenditures at least 10 percent (unallocated) in most department

budgets. |

The May Revision proposes a complicated set of adjustments to General Fund spending for Proposition 98 programs in both the current and budget years. These adjustments are driven primarily by a revised estimate of the Proposition 98 guarantee for 2002-03. The estimated budget-year guarantee is almost $1.2 billion higher than the January estimate, and accounts for most of the $1.6 billion growth in that portion of the state's budgetary problem that is due to increased expenditure estimates. Two factors contribute to the increase in the guarantee. First, a change in estimated per-capita personal income for California causes an increase in the guarantee of about $830 million. The remainder of the increase (about $350 million) is due to higher Department of Finance estimates for K-12 average daily attendance (ADA).

The Governor's proposal essentially involves shifting selected General Fund amounts that would have applied towards the 2001-02 guarantee instead to 2002-03. This shift is possible under the terms of Proposition 98—provided the current-year adjustments are enacted by June 30— because the current level of appropriations for 2001-02 greatly exceeds the minimum funding requirement for that year. Most of the proposed shifts fall into two categories. First, the May Revision proposes a one-month postponement of disbursements in five programs from June to July. This expenditure deferral totals over $1.1 billion. Second, the May Revision adopts an option that we described in our Analysis of the 2002-03 Budget Bill to substitute balances available in the Proposition 98 Reversion Account for an equal amount of General Fund spending that was being counted toward the 2001-02 guarantee (but was in excess of the minimum funding requirement for that year). The May Revision proposes shifting $503 million in this manner. All of these shifts permit the state to meet the constitutional funding requirements for K-14 education in both fiscal years, minimize specific program cuts relative to the combined two-year spending total proposed in January, and also cover added revenue limit payments required in both years due to ADA increases.

The May Revision also takes advantage of a $738 million increase in federal funds from the recent No Child Left Behind Act to help support existing programs and augment program funding in selected areas. Based on our preliminary review, some of the administration's proposals appear to be reasonable uses of the federal funds. The Legislature, however, has considerable discretion to appropriate these federal funds in alternative ways that help address its K-12 priorities.

Of the $2.4 billion in additional reductions proposed in the Governor's May Revision proposal, around $1 billion is in the health services program area. For example, significant reductions are proposed to Medi-Cal, which include reducing the optional medical and dental services that would be available to some adults, imposing further reductions in the rates paid to physicians, cutting the funding available for hospitals which disproportionately provide services for the poor, imposing a 20 percent cut in spending for county administration, tightening eligibility reporting rules, and rescinding a recent expansion of eligibility to poor families. The budget plan also continues to rely on $400 million in additional federal funding that may not become available to offset General Fund expenditures.

Some reductions were also made in social services, including not "passing along" the federal Supplemental Security Income/State Supplementary Program federal cost-of-living adjustment and significant reductions in county administration for various social service programs.

In contrast to health and social services, the Department of Corrections received budgetary increases, mainly due to a one-time increase in workers' compensation costs, increased costs for contract medical services, and implementation of statewide improvements in inmate health-care services consistent with the Plata lawsuit.

The May Revision does not reduce local government VLF revenues, but redirects to schools about $120 million of property taxes from special districts and redevelopment agencies. The May Revision also reduces local government subventions and grants by over $200 million, cuts county-administered health and social services programs by over $200 million, and requires counties to pay for a portion of federal penalties for the child support and Food Stamps programs (about $150 million). The budget plan defers funding for about $1.6 billion of local agency mandate reimbursement claims, roughly half of which would have been paid to cities and counties.

In evaluating the May Revision proposal, the Legislature may find it helpful to focus on three general questions:

Overall, we believe that the budget proposal provides a credible framework for addressing the huge budget shortfall facing the state in 2002-03. For example, its estimate of the budget problem's magnitude is realistic, and is based on generally reasonable estimates of the economy, revenues, and state costs in the current and budget years.

Although it is generally a workable plan, the budget faces several important risks and vulnerabilities, including potentially lower-than-anticipated federal receipts. When combined with the $600 million overstatement of prior-year bank and corporation tax receipts discussed earlier, these factors could push the May Revision spending plan into a deficit of over several hundreds of millions of dollars. In addition, the budget does not recognize certain expenses, such as over $1.6 billion in local mandate claims (including past-year claims), which will likely add to cost pressures in future years.

While we believe that the budget proposal is a credible plan, it clearly embodies the Governor's priorities for addressing the shortfall. A key question for the Legislature is thus how the policies embodied in the May Revision match up against its own priorities. This involves both the general distribution of solutions among spending cuts, tax increases, and borrowing, as well as the specific solutions proposed by the Governor for addressing the shortfall. Some examples of the latter include the Governor's proposed use of federal funds for K-12 education, the cuts in health and juvenile justice programs, and the decision to increase the amount of borrowing through securitization of future tobacco settlement receipts. Regarding tax increases, an important question is whether the Governor's proposed changes are preferable to, for example, a reduction in some tax expenditures such as credits, deductions, and exemptions.

In our February publication The 2002-03 Budget: Perspectives and Issues, we reported that the state faced not only a substantial year-end 2002-03 projected deficit, but also an longer-term imbalance between revenues and expenditures. We indicated that even if the Governor's January budget plan were adopted, an operating deficit in the range of $7 billion would likely persist for some time, absent corrective action.

Given the enormity of the budget gap currently facing the state, the Governor's top priority in crafting the May Revision was rightly focused on eliminating the projected $23.6 billion budget-year deficit. And, as indicated previously, his plan provides a credible framework for approaching this immediate problem. However, the state still has an underlying budget problem that will have to be dealt with in the following year. The exact size of this problem is difficult to accurately predict at this time, given that it will significantly depend on how strongly the state's economy and revenues perform over the next year. However, we believe that the magnitude of this imbalance could be much larger than what we estimated in February.

Given this, the Legislature may wish, as it reviews the May Revision plan, to look

for opportunities to reduce the out-year problem

in conjunction with dealing with the more immediate and higher-priority 2002-03 problem.

The Governor's plan itself takes a step in this

direction, in that a portion of its budget

solutions have beneficial impacts beyond the budget

year. For example, his VLF, NOL, and cigarette tax proposals have 2003-04 effects. Similarly,

certain of the Governor's expenditure solutions, such

as most of his health-related reductions, have

2003-04 effects. Along these same lines, the Legislature may find that it makes sense

to implement as part of its budget decisions some

additional multiyear solutions, such as extending for a limited period of time some of the

one-time measures contained in the Governor's plan.

| Acknowledgments

This report was prepared by , and reviewed by Brad Williams, Keely Martin Bosler, and Jon David Vasch�, with contributions from others in the office. The Legislative Analyst's Office (LAO) is a nonpartisan office which provides fiscal and policy information and advice to the Legislature. |

LAO Publications

To request publications call (916) 445-4656. This report and others, as well as an E-mail subscription service, are available on the LAO's Internet site at www.lao.ca.gov. The LAO is located at 925 L Street, Suite 1000, Sacramento, CA 95814. |