![]()

This report provides our projections of General Fund revenues and

expenditures for 2003-04 through 2008-09. It includes our independent assessment of the outlook for California's economy, demographics,

revenues, and expenditures.

Chapter 1 contains our principal findings and conclusions. Chapter 2 presents our economic and demographic projections, Chapter 3 our revenue

forecasts, and Chapter 4 our expenditure projections.

Our fiscal projections reflect current-law spending requirements and tax

provisions. They are not predictions of future policy decisions by the Legislature, nor are they

our recommendations as to what spending and revenue levels should be.

This report, in its ninth year of publication, reflects the historical mission of

the Legislative Analyst's Office to assist the Legislature with its fiscal planning by

assessing the revenues and expenditures of the state. The report is part of an

ongoing series and is updated periodically.

Chapter 1: The Budget Outlook 1

Chapter 2: Economic and Demographic Projections 11

Chapter 3: Revenue Projections 21

Chapter 4: Expenditure Projections 27

As was the case last year, California's policymakers will face a substantial challenge in crafting next year's General Fund budget. According to our updated projections, the state is facing a year-end shortfall of $10.2 billion in 2004-05 assuming the vehicle license fee (VLF) rate increase remains in effect, and substantially more if the rate is rolled back and the state resumes backfill payments to localities. Over the longer term, absent corrective actions, the state faces annual current-law operating deficits (that is, excesses of expenditures over revenues) that remain over $9 billion through the end of the forecast period—and $14 billion if the VLF rate is rolled back.

The persistent nature of the out-year

operating shortfalls—even in the face of an

improving economy—indicates that the state will not be

able to "grow its way out" of its budget problems

on the natural. The "good news," though, is that

the projected operating shortfalls do start to

narrow over time. This means that once the basic gap

between annual expenditures and revenues is closed by ongoing solutions, we would expect future

revenue growth to be sufficient to cover program

costs over the forecast period.

In the paragraphs below, we (1) briefly review the 2003-04 budget signed by the Governor

in August, (2) discuss the subsequent budget-related developments that have occurred, and

(3) present our updated budget projections for 2003-04 through 2008-09.

In confronting the 2003-04

budget, policymakers faced an enormous fiscal

shortfall that the administration estimated was as high

as $38 billion. This shortfall was the product of

three years' worth of major imbalances between

revenues and expenditures, which first opened up when revenues plunged during the 2001

economic downturn and stock market decline.

As Figure 1 shows, the majority of the

2003-04 budget solutions were clearly one-time in

nature, consisting of borrowing, deferrals, funding

shifts, and revenue accelerations. The budget plan

did include ongoing savings from various program

reductions and a VLF rate increase (the latter

triggered by the "insufficient funds" provision in

current law).

Figure 1 Main Elements of 2003-04

Budget Plana �

Borrowing and Deferrals ($18.3 billion) �

Deficit financing, pension obligation bonds. �

Local mandates, education, and transportation deferrals. �

Special funds loans. �

Program Savings ($9.2 billion) �

Education. �

Medical services and reimbursement rates. �

Social services cost-of-living adjustments. �

New/Accelerated Revenues ($4.5 billion) �

Tribal gaming. �

Tobacco securitization. �

VLF Rate Increase ($3.4 billion) �

Shifts to Other Funds ($4.1 billion) �

Federal funds. �

Fees. �

a

Dollar estimates as of time budget was enacted.

Ongoing Operating Shortfalls Not Fully

Addressed. Assuming that all of the budgetary

savings and borrowing actions included in the 2003-04 budget plan would be realized, that plan

estimated that the huge 2003-04 shortfall would be closed and the state

would end the year with a reserve of about

$2.2 billion. However, since so much of the adopted 2003-04

budget solution involved borrowing, deferrals, and

other one-time actions, it also was acknowledged that

the disappearance of such solutions the next year would leave a large

"budget hole" and thus a major operating shortfall

of roughly $10 billion would automatically reemerge

in 2004-05. The added debt-service costs

associated with repayment of the deficit financing and

pension bonds that the budget plan authorized also

contributed to the projected shortfall in 2004-05. Taking

into account the carryover $2.2 billion reserve

projected for the end of 2003-04, the year-end

2004-05 budget shortfall was expected to be about

$8 billion, absent further corrective actions.

As Figure 2 shows, there have been both positive and negative developments on the budget front since the summer that we have taken into account in updating our fiscal projections.

|

Figure 2 Developments Since the

2003-04 Budget�s Enactment |

|

|

|

Underlying Revenue Outlook Improving . . . |

|

�

Economy and stock market up. �

Recent tax collections higher-than-expected. |

|

. . . But New Tax Revenues Consumed by Other Budget

Related-Factors |

|

�

One-half of added revenues goes to Proposition 98. �

Pension obligation bonds invalidated by Superior Court. �

Tribal gaming revenues overestimated. �

Major deficiencies in Department of Corrections and Medi-Cal. �

Costs for Southern California fires. �

Shortfall in other budget savings. |

On the positive side, recent economic developments and cash receipts trends have been more favorable than expected. These positive developments, which are discussed in Chapter 2, include (1) a sharp improvement in business investment spending documented in the third quarter's gross domestic product report, which should benefit California firms; (2) healthy business earnings reports; and (3) higher state tax collections from withholding and quarterly estimated income tax payments during the first four months of 2003-04. As a result of these and other developments, we have revised upward our projections of major tax revenues by modestly over $2 billion in both 2003-04 and 2004-05.

On the negative side, however, the added revenues from these positive developments have been more than offset by added costs in the state budget. These include the effects on pension-related costs of an adverse court ruling involving the planned pension obligation bond sale, various costs related to the Southern California fires, higher Proposition 98 spending (triggered by the gains in revenues), and budget deficiencies in corrections, Medi-Cal, and state operations. In addition to these costs, we expect tribal gaming revenues to be considerably less than previously assumed.

Taking into account both the positive economic and revenue developments and the more-than-offsetting cost increases, the budget outlook is modestly worse than previously thought for 2003-04 and 2004-05 although modestly better over the longer term. Despite these recent developments, however, the key point for policymakers is the same as before—namely, the state faces a major mismatch between revenues and expenditures, and this will ultimately need to be addressed through spending reductions and/or revenue enhancements if the state is to regain fiscal balance.

Figure 3 presents our updated estimates of the General Fund's condition for 2002-03 through 2004-05. These estimates take into account our revised projections of current-law revenues and expenditures discussed in Chapter 3 and Chapter 4, respectively. The basis for our estimates, including their underlying methodology and assumptions, is summarized in the accompanying box (see page 7). The estimates shown in Figure 3 assume that the VLF rate increase (effective October 1, 2003) remains in effect in both 2003-04 and 2004-05, as provided for in current law. Our projections indicate the following.

|

Figure 3 LAO Projections of General

Fund Condition |

|||

|

2002-03 Through 2004-05a |

|||

|

|

2002-03 |

Forecast |

|

|

2003-04 |

2004-05 |

||

|

Prior-year fund balance |

-$1,983 |

$1,513 |

$2,003 |

|

Revenues and transfers |

70,852 |

74,165 |

74,968 |

|

Deficit financing bond |

10,675 |

� |

� |

|

Total

resources available |

$79,544 |

$75,678 |

$76,971 |

|

Expenditures |

$78,031 |

$73,675 |

$85,727 |

|

Ending fund balance |

$1,513 |

$2,003 |

-$8,756 |

|

Encumbrances |

$1,402 |

$1,402 |

$1,402 |

|

Reserve |

$111 |

$601 |

-$10,158 |

|

|

|||

|

a

Detail may not total due to rounding. |

|||

Vehicle License Fee (VLF)BackgroundThe state law enacting a VLF rate reduction beginning in 1999 included three accompanying

provisions which are of significance to the current fiscal outlook: (1)

it required that the state backfill local governments for their revenue losses resulting from the lowered rates, (2)

it required that the VLF rate be increased whenever there were insufficient moneys in the General Fund to pay for the backfill, and (3)

it stated that, from 2000-01 through 2003-04, California Work Opportunity and Responsibility

to Kids

(CalWORKs)

cost-of-living adjustments (COLAs) would be granted only in fiscal years in which VLF tax relief is granted.

Several VLF-related actions were taken in conjunction with the 2003-04 budget which are having

an impact on General Fund expenditures. In June 2003, the Director of Finance made the determination

that there were insufficient moneys in the General Fund for the backfill, thereby terminating backfill

payments and triggering a rate increase (from 0.65 percent to 2 percent) for VLF payments due on or after October

1, 2003. Backfill payments to local governments (with a few minor exceptions) ceased after June 20,

2003, saving the General Fund about $4 billion in 2003-04. The revenue loss to local governments during

the time period between when the backfill ceased and additional revenues from the rate increase started

flowing is being treated as a loan. The loan is scheduled to be repaid by mid-2006.

The 2003-04 budget included language which sets the VLF backfill at $1,000 for 2003-04, regardless

of the tax rate's level. Presumably, this language would hold the backfill to $1,000, absent legislative

action, even if the tax rate were rolled back this year. Also, because tax relief was eliminated, the CalWORKs

COLA for 2003-04 was suspended.

Our VLF Expenditure Forecast

Given the large operating shortfalls that we are projecting through 2008-09, we are assuming that

the "insufficient moneys" provision holds through the forecast period, and the higher VLF rate therefore

remains in effect as provided for in current law. Thus, our estimates include no VLF backfill payments

other than a loan repayment in 2006-07. We also include no 2003-04 COLA for CalWORKs recipients,

again reflective of current law.

What Happens if New Administration Rolls Back the VLF Rate?

The Governor-elect has stated his intent to roll back the VLF tax rate once he takes office. The fiscal impact of this rollback, particularly

in 2003-04, would depend on exactly how such a reduction were implemented. Figure 4 shows the potential effects

in 2003-04 under three alternative scenarios regarding the timing of the rollback and which

governmental level—the state or localities—bears the revenues losses from the rollback.

In Scenario A, the rate is rolled back effective February 1, 2004, but legislation is not passed which restores the backfill to local

governments. Under this scenario, local governments would shoulder the full cost of the rate reduction in

2003-04—$1.8 billion. In Scenario

B, the rate reduction is also effective February 1, 2004 but legislation is

passed restoring the backfill. Under this scenario, the State General Fund would bear the costs of the tax

reduction. In Scenario C, the rate reduction would apply retroactively to everyone that paid the higher rate in

2003-04, through a rebate mechanism. Assuming that the backfill is also restored, the 2003-04 cost to the

General Fund would be about $3.2 billion.

Figure 4 Potential Impacts of VLF

Rate Rollback in 2003-04a (In Billions) Vehicle

Owner Governmental

Cost State Localb Scenario A�Rate reduction effective February 1,

2004 but no backfill in 2003-04. $1.8 � $1.8 Scenario B�Rate reduction effective February 1,

2004 and backfill restored through legislation. 1.8 $1.8 � Scenario C�Rate reduction made 3.2 3.2 � a

Fiscal effects in subsequent years are identical for all

scenarios at $4.2 billion in 2004-05, $4.4 billion in 2005-06, $4.6

billion in 2006-07, $4.8 billion in 2007-08, and $5 billion in 2008-09. b

The cost shown is in addition to the $960 million reduction in

backfill payments already being

In all three scenarios, the out-year costs of a VLF rollback would be identical, as current law would

again require backfill payments to local governments beginning on July 1, 2004. These

backfill payments would be about $4.2 billion in 2004-05, increasing modestly in subsequent years.

Impact on CalWORKs Costs. The rollback of

the VLF rate would have no impact on General Fund

expenditures on CalWORKs in 2003-04. The additional costs

would be covered from federal reserve funds.

However, there would be costs of roughly $223 million

in 2004-05 and about $130 million in subsequent

years, as the federal reserves are depleted and the

added CalWORKs costs are borne by the General Fund.

|

||||||||||||||||||||||||||||||||||||||

Based on our updated projections, 2003-04 General Fund revenues will total $74.2 billion, expenditures will be $73.7 billion, and the year will end with a positive reserve balance of $601 million. This compares to the $2.2 billion reserve that was anticipated when the 2003-04 budget was enacted. If the VLF rate were rolled back and refunds were provided to motorists that have paid the higher rate since it went back into effect, current-year expenditures would be $3.2 billion higher than the baseline, and the year would end with a deficit of $2.6 billion, absent corrective actions. Please see nearby box for a discussion of the VLF situation and its potential fiscal impacts.

For 2004-05, revenues are projected to be $75 billion, or $10.7 billion less than the projected expenditure total of $85.7 billion. As a result of the reemergence of the mismatch between revenues and expenditures, the budget faces a year-end deficit of $10.2 billion, absent corrective actions. If the VLF rate increase were rolled back and the backfill resumed beginning this year (2003-04), the cumulative impact on the 2004-05 reserve would be a $7.4 billion deterioration—the $3.2 billion noted above for the current year and another $4.2 billion in 2004-05. (This assumes no other offsetting savings were achieved.) In addition, California Work Opportunity and Responsibility to Kids (CalWORKs) cost-of-living adjustment (COLA) costs would increase by $223 million. Thus, the rollback would increase the projected cumulative year-end shortfall for 2004-05 to $17.8 billion.

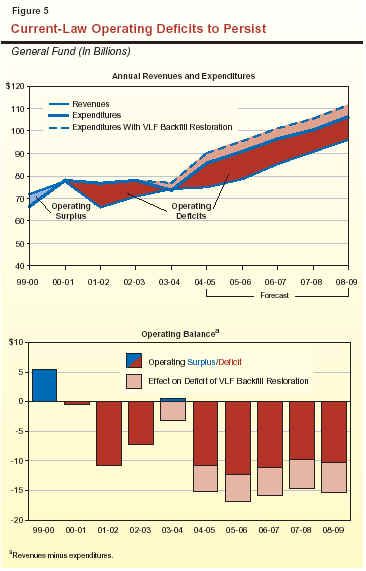

Figure 5 presents our revenue and expenditure forecasts through 2008-09, both with and without a rollback in the VLF rate. It indicates that, for example, assuming no rollback, the operating deficit grows to a peak of $12.3 billion in 2005-06. This primarily reflects the large scheduled repayment of a transportation loan and the resumption of local mandate reimbursements in that year. In the following three years, the gap narrows somewhat, as ongoing revenue growth modestly outpaces ongoing growth in program expenditures. As of 2008-09, however, the gap would still remain in the range of $10 billion assuming the VLF increase remains in place, and $15 billion if it is rolled back (the difference due to the amount of the backfill).

This is the third consecutive year that we have projected in our fiscal forecast a persistent current-law budget shortfall extending throughout the forecast period. This indicates that the state has not yet met the fundamental challenge of getting expenditures and revenues in line. In the preceding two reports, we also identified a group of budget-balancing principles, strategies, and tools that we again offer, as summarized in Figure 6 (see next page). Although the specific numbers in this year's report differ from those provided previously, we believe that these items still merit the Legislature's attention. This is because the state's basic budget problem is still essentially the same—namely, current-law expenditures exceed current-law revenues.

|

Figure 6 Basic Budget-Balancing

Principles, Strategies, and Tools |

|

Key Principles |

|

�

Wide range of budget solutions should be considered. |

|

�

Out-year repercussions should be assessed. |

|

�

Budget solutions should �make sense.� |

|

�

Current-year solutions should play a key role. |

|

Basic Strategies |

|

�

Determine the relative roles of spending and revenue

options. |

|

�

Identify the appropriate contributions of different

program areas. |

|

�

Establish the desired mix of one-time versus ongoing

solutions. |

|

�

Be cautious about additional borrowing. |

|

Individual Tools |

|

�

Spending-related options. |

|

�

Eliminate or modify programs. |

|

�

Suspend/reduce COLAs. |

|

�

Shift funding from the General Fund. |

|

�

Implement improvements and efficiencies. |

|

�

Revert or disencumber funds. |

|

�

Revenue-related options. |

|

�

Eliminate or modify tax expenditures. |

|

�

Broaden basic tax bases. |

|

�

Raise tax rates. |

|

�

Transfer special fund balances. |

|

�

Improve tax compliance and collections. |

Among other things, we recommend that the Legislature:

In the coming months, our office will be assisting the Legislature in developing possible budget-balancing expenditure and revenue strategies and options to help address both the large projected 2004-05 shortfall and the ongoing operating imbalances projected for future years.

Basis for Our EstimatesAs noted in past reports, our revenue and expenditure forecasts are based primarily on

the requirements of current law, including constitutional and statutory funding requirements

(such as the Proposition 98 funding guarantee). Our estimates also reflect projected changes in

caseloads, federal reimbursements, and other factors affecting program costs.

For the current forecast, we have also taken into account language included in the

2003-04 budget plan stating the Legislature's intent that the administration

not include certain funding adjustments in developing the 2004-05 budget. These include funding for: (1) University of

California (UC) and California State University (CSU) salary increases and enrollment growth; Our basic estimates included in Figure 3 assume that the VLF rate increase, triggered by

the insufficient funds provision of current law, remains in place through the forecast. Because

the Governor-elect has stated his intent to roll back the increase, we discuss the incremental impact

of that change separately. Our out-year estimates also include scheduled loan repayments to

special funds as well as payments to cover accumulated local government mandate claims.

Projections, Not Predictions. Our estimates are not predictions of what the Legislature

and Governor will adopt as policies and funding levels in future budgets. Rather, our estimates

are intended to be a reasonable "baseline" projection of what would happen if current-law

policies were allowed to operate in the future. In this regard, we believe that our forecast provides a

meaningful starting point for legislative deliberations involving the state's budget. |

As indicated earlier, the 2003-04 budget relied on a variety of different types of borrowing-related actions to help close the budget gap. Among others, these included the use of deficit financing and pension bonds, direct loans from special funds, deferrals of spending obligations such as for transportation and local mandates, tobacco bonds to accelerate the state's receipt of future revenues, and refinancing of existing general obligation bond principal repayments. Altogether, we estimate that there was close to $20 billion of these and other different types of borrowing incorporated in the adopted 2003-04 budget plan. This budget-related borrowing is in addition to the more traditional types of borrowing that use general obligation and lease-revenue bonds to finance the state's outlays for infrastructure and other capital needs, as well as the internal and external borrowing needed for cash-flow purposes.

Budget-related borrowing of course helps the General Fund's condition in the years when it

is undertaken. However, it generally is a one-time savings, and thus creates a "budgetary hole" to

fill the next year. In addition, the effect of borrowing eventually becomes a drag on the budget,

because debt service expenses for past spending will interfere with providing

current public services.

A significant portion of the General Fund operating shortfalls that we project for 2004-05

and beyond is associated with such debt repayments. For example, in 2005-06, debt service on

the deficit financing bond and the scheduled payment of the transportation loan totals about

$3.9 billion, or one-third of the projected operating shortfall for that year.

There is no "hard and fast rule" to identify what amount of borrowing is "right" for the

Legislature to use in addressing budget shortfalls. As a general policy, however, we believe that

budget-related borrowing—particularly from private markets—should be relied on only as a last

resort. Actions to bring spending and revenues into line should be the top priority.

This is not to say that there are no instances where some borrowing makes sense.

Examples might be when the size of a deficit is simply too large to handle all at once, or when a

budget shortfall will likely be quickly eliminated by a strongly rebounding economy. We do not

believe that either of these situations currently exists. Engaging in budget-related borrowing to avoid

spending cuts and tax increases, or to finance additional spending and tax cuts—is a slippery slope.

Given the large amount of budget-related borrowing already authorized, we caution

against the state engaging in new borrowing—particularly from private markets—to cover the

projected 2004-05 operating shortfall.

Economic and demographic developments are typically two of the most important determinants of California's fiscal condition through their impacts on both tax revenues and state expenditures. This chapter presents our economic and demographic projections for 2003 through 2009, which will affect California's fiscal condition during fiscal years 2003-04 through 2008-09.

We believe that California, like the nation,

has "turned the corner" economically and is

now embarking on a period of faster and more-balanced expansion as 2003 comes to a close.

This acceleration is due to (1) a long-awaited improvement in business investment

in computers, software, and other high-tech goods produced and designed in this state; and

(2) ongoing strength in home construction and consumer spending. A key assumption in

our outlook is that this faster economic expansion

will finally result in an improvement in the jobs outlook, which has lagged thus far during

the current rebound.

Our forecast assumes that the massive October fires in Southern California, while having

tragic personal and economic consequences for

those directly affected, will not have a major net

adverse impact on the overall state economy. We

anticipate that the loss in wealth and income in the

regions affected will be roughly balanced by a surge

in rebuilding financed by federal funds and

private insurance payments. Figure 1 (see next

page) summarizes the details of our economic

forecast. In subsequent sections, we discuss in more

detail major factors underlying our projections.

Figure 1 The LAO�s Economic

Forecast Percentage Change (Unless Otherwise Indicated) 2003 2004 2005 2006 2007 2008 2009 United States Real

gross domestic product 3.0% 4.2% 3.7% 3.7% 3.5% 2.9% 2.8% Personal

income 3.2 5.3 5.7 5.9 5.8 5.3 5.3 Wage

and salary jobs -0.3 1.1 2.4 1.8 1.5 1.1 1.2 Consumer

Price Index 2.4 2.0 2.4 2.5 2.6 2.6 2.7 Unemployment

rate (%) 6.1 6.1 5.9 5.8 5.7 5.6 5.6 Housing

starts (000) 1,775 1,680 1,640 1,620 1,640 1,620 1,590 California Personal

income 4.2% 5.9% 6.3% 6.2% 6.0% 5.9% 5.9% Wage

and salary jobs -0.4 1.3 2.6 2.2 1.9 1.7 1.6 Taxable

sales 2.4 5.9 6.3 6.2 5.9 5.7 5.7 Consumer

Price Index 2.8 2.3 2.7 2.7 2.8 2.8 2.9 Unemployment

rate (%) 6.6 6.1 5.6 5.5 5.6 5.5 5.5

New

housing permits (000) 188 179 180 178 175 173 170

2003 Through 2009

Although the recession officially concluded

in late 2001, the ensuing recovery was weak and unbalanced through 2002 and into early 2003.

Low interest rates and federal tax reductions kept consumer spending and housing activity on

an upward track. However, business spending and hiring remained soft during this period,

reflecting chronic overcapacity in many key industries,

weak foreign demand, and a loss of confidence by corporate executives who make

investment decisions.

The improvement in business spending finally materialized in the third quarter of this year

(see Figure 2). This increase, coupled with sharp

gains in consumer spending and strong housing construction, boosted real gross domestic

product (GDP) by a 7.2 percent annual rate in the

July-through-September period. Of particular importance to California was the

jump experienced in spending on computers and software, as the business sector began to

upgrade systems that had not been replaced since 1999.

Gross domestic product data on consumption and business investment are not available at the state level, so it is not possible to directly determine how the recent national improvement in GDP growth has affected our state. However, various industry and tax-related data suggest that California's economy clearly is participating in the national recovery. For example:

While these gains are encouraging, an important uncertainty concerning the durability of the current expansion—both at the national and state levels—is whether the recent improvements in spending and output will translate into more jobs in the months ahead. The jobs outlook is particularly clouded by the differing trends in employment data that the two main information sources are exhibiting, with the "household survey" showing growth but the "payroll survey" showing continued declines (see box on page 15). We examine California's job picture in more detail below, comparing its current performance to that of past recession/recovery periods and to the nation as a whole.

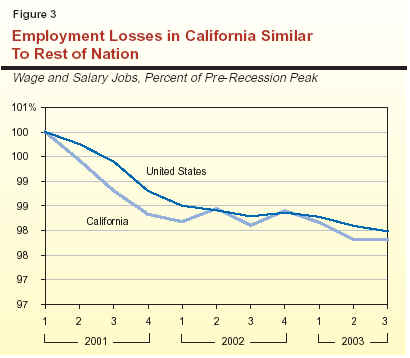

California Relative to the Nation. The job losses experienced in California since early 2001 (when the most recent recession began) are not out of line with the rest of the nation. As shown in Figure 3, the cumulative job loss over the past 30 months is about 2.2 percent in California, compared to 2 percent for the nation as a whole. Within California, the percentage reduction in the San Francisco Bay Area has been considerably greater than for the nation, but losses in Southern California and the Central Valley regions of the state have been proportionally less.

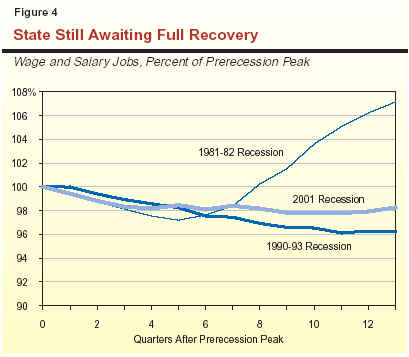

Current Performance Compared to Past

Recessions. As indicated in Figure 4, the

cumulative job losses associated with the 2001 recession

and its aftermath are roughly on a par with those

of the early 1980s' recession, but considerably

less severe than the early 1990s' downturn. In terms

of duration, however, job declines in the current period have been prolonged compared to the

1980s' experience. For example, the cumulative 2

percent decline in jobs during the 30 months following

the start of the 2001 recession compares

unfavorably to the 4 percent net gain in jobs that had

occurred 30 months after the beginning of the 1981 recession. In this regard, the current downturn

is more similar to the 1990s' recession.

Thus, while many indicators are pointing toward improved sales, production, and income

in the state, the lack of job growth thus far remains

a key concern regarding the durability of the expansion.

There are two surveys used to measure employment performance at the national and state

levels. The first is the household

survey, which is drawn each month from interviews with members of

a selected sample of households. The resulting data are then used to develop detailed estimates of

the employment and unemployment characteristics of individuals in the labor force. The second

source is the payroll survey, which is based on information collected from employers that file

withholding and unemployment insurance reports. These latter data are used primarily for estimates of

aggregate employment totals and job performance within various industry categories, and indeed are what

we are referring to in our discussion of current employment trends.

Historically, the above two employment series have usually moved in concert with one

another over economic cycles, although the household series has shown more month-to-month variation

due to its smaller sample size. As shown in Figure 5, however, the two series have significantly

diverged from one another in 2003, with the payroll survey showing year-to-year

declines averaging about

The payroll survey is traditionally considered to be a more reliable indicator of employment

trends due to its more extensive coverage and greater detail. However, at the present time, the

household survey seems to be more consistent with the more upbeat data on spending and production in

the economy. One of the possible explanations for the current difference between the two surveys'

results may be an increase in the use of contract

workers by employers that are reluctant to add to

their permanent workforce. These contract workers would show up in

the household survey as employed but may be excluded from

the industry survey, which is based on actual

company payrolls. While the contract jobs are more likely to be part time

and have less pay and fringe benefits than

traditional jobs, the growth in this sector provides

some positive evidence that businesses are taking

the first step toward renewed hiring.

So—What's the True Picture Regarding Employment Strength?

0.5 percent, and the household survey showing year-to-year

increases averaging about 1.2 percent. A similar discrepancy is evident at the national level.

Our updated forecast assumes that

U.S. economic growth will pick up somewhat and expand at a very healthy pace through 2004,

before settling into a somewhat more moderate

though sustainable pace in subsequent years. During

the next year, the economy is expected to benefit

from continued improvements in business investment and foreign trade, as well as ongoing expansion

in consumer spending. Overall, we forecast that growth in U.S. GDP will accelerate from 3

percent in 2003 to 4.2 percent in 2004, before

moderating some in subsequent years. The unemployment

rate is projected to slowly decline from the current

level of around 6.1 percent down to 5.6 percent by 2008.

What About Large Budget Deficits? Clearly,

the large U.S. budget deficits that federal

officials project for the future imply that the

borrowing needs of the federal government will be

substantial in the years ahead. At present, U.S.

government borrowing is being easily accommodated in

the credit markets, due to the large amount of

liquidity in the financial system and the fact that

businesses have large amounts of cash on hand to finance

new investments. However, the large federal budget deficits will likely put upward pressure on

interest rates once private demand for borrowing picks

up. This will push interest rates slowly upward

over the forecast period, and these higher rates

will eventually work to moderate economic performance in such areas as business

investment, consumer spending, and housing activity.

We forecast that California's economy will

grow in line with the national economy over the

next several years, reflecting the positive effects

of improving business investment and foreign trade on our manufacturing and high-tech

service industries. After falling for most of 2003, we

expect that wage and salary employment will stabilize

late in the year and grow modestly in 2004 and thereafter. On an average annual basis, we

forecast that jobs will fall by 0.4 percent in 2003

before expanding by 1.3 percent in 2004 and 2.6

percent in 2005.

Reflecting the improvement in jobs, wages, and business earnings, we project that personal

income will accelerate from 4.2 percent this year to 5.9 percent in 2004 and 6.3 percent in 2005.

Finally, we forecast that taxable sales will accelerate

from 2.4 percent this year to 5.9 percent in 2004 and 6.3 percent in 2005. These projected strong

taxable sales gains are in part reflective of the

expected improvement in the roughly one-third of

taxable sales that are related to business spending.

We expect that housing construction will remain near current levels through the

forecast period. While this is well above the rates

achieved over the past decade, our projected pace

of residential building construction remains below what many economists consider the

amount needed to fully accommodate the state's

ever-expanding population. The shortfall between

the available supply and demand for housing, which is partly related to the limited availability

of developable land in key areas of the state,

will continue to put upward pressure on home

prices in future years.

We see two primary risks to the

near-term economic outlook. These involve:

Lack of Job Growth. While our forecast

assumes that the recent growth in business spending

and output will translate into added jobs in the

U.S. and California economies, we have yet to see

firm evidence that this is occurring. On the one

hand, the fact that businesses have been able to

increase output and sales without adding to the

workforce suggests that productivity gains in the economy

are even better than anticipated. This, by itself,

has positive implications for the long-term

achievable growth in output, income, and wealth in the

nation and state. However, persistent softness on the

job front poses a significant near-term risk, in that

the lack of job creation may undermine consumer confidence and spending, and in turn undercut

the economic expansion. The lack of job growth is

an especially significant risk in California,

where concerns about business costs could translate

into more out-of-state outsourcing and less

expansion in the state than would normally be

expected during a growth period.

Potential Home Price Bubble. A second key

risk to California's outlook involves the pattern

of extraordinary increases in home prices.

Following four years of uninterrupted increases, the

median home price statewide is now over $400,000,

with many major metropolitan areas being above $500,000. The key question this raises is

whether the state faces a home price "bubble" that

will deflate or even burst in the near future.

Many economists and real estate analysts currently believe that the price jumps being experienced

are not due primarily to speculative excesses.

Rather, they attribute them as largely reflective of

limited housing supply in many regional markets

and ongoing growth in the state's population.

However, there is no doubt that the recent price

increases make the housing market more vulnerable

to adverse economic developments than otherwise, such as a significant upturn in interest rates.

To the extent that the increased household wealth associated with home price increases has been

a positive factor underlying consumer spending during the past two years, a sharp reversal in

home prices could have a significant negative effect

in the future.

California's population currently totals

slightly over 36 million. During the six-year forecast

period covered in this report, the state's population

is projected to grow annually by about 1.3

percent, or close to half a million persons yearly. (This

is roughly equivalent to a city the size of Long Beach.) Thus, California will add

roughly 2.9 million people over the forecast interval

and reach almost 39 million by 2009.

The population growth rate we are projecting is somewhat slower than that experienced in

the latter part of the 1990s, when growth was

averaging about 1.6 percent. This reflects both

the dampening effects of the slower economy of

recent years on in-migration, plus a continuing downward trend in birth rates.

California's population growth can be

broken down into two major

components—natural increase (the excess of births over deaths) and

net in-migration (persons moving into

California from other states and countries, minus

those leaving California for out-of-state

destinations). On average, these two components have

tended to contribute about equally over time to the

state's population growth. However, their relative

shares can vary significantly from one year to the

next depending largely on the strength of the net

in-migration component—by far the most

volatile element.

Natural Increase. We project that the

natural-increase component will average about

275,000 new Californians annually over the forecast

period. This amount is slightly less than in the late

1990s and early 2000s, when it averaged about

295,000. This softening reflects the ongoing decline in

birth rates being experienced by all ethnic

groups. Despite these declining birth rates, however,

the natural-increase component still will grow

slightly during the latter half of the forecast period.

This is due to significant growth in the female population of child-bearing age groups in

faster-growing segments of the population,

including Hispanic and Asian women.

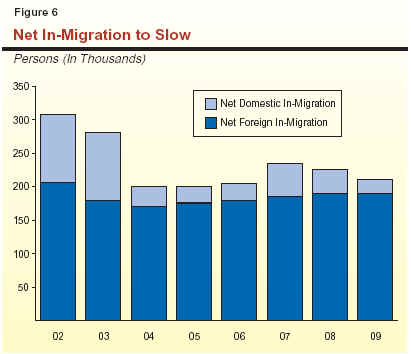

Net In-Migration. We project that net

in-migration will average nearly 215,000 annually over the next six years. This is weaker than

during the latter half of the 1990s and early 2000s

when annual net in-migration averaged about

260,000. It also is considerably less than the

projected natural-increase component. As shown in

Figure 6 (see next page), this reflects a projected drop

in domestic net in-migration that we believe

will follow California's period of economic

softness. In contrast, foreign net in-migration—which

has been relatively stable over the past decade and

has proved to be less sensitive to the

economy—is projected to remain relatively flat.

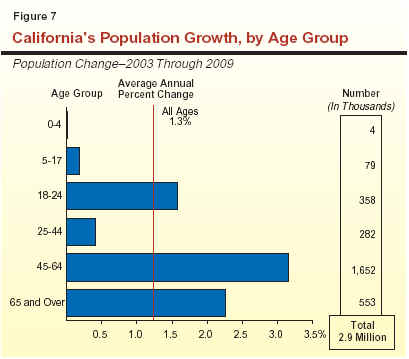

Figure 7 (see next page) shows our population growth projections by broad age categories, including both numerical and percentage growth.

Ranks of Baby Boomers to Dramatically

Swell. The 45-to-64 age group (largely the

"baby boomers") continues to be by far the fastest growing

segment of the population. Over 1.7 million new people

are expected to move into this age category over the next

six years. At the other extreme, slow growth is anticipated

for preschoolers and the K-12 school-age population.

This reflects several factors. One is the movement of children

of the "baby boom" generation beyond the upper-end of

the 5-to-17 age group. Other factors include the slower

rate of net in-migration, and the decline in birth rates in

recent years that has reduced the number of children

moving into the preschool and school-age categories.

These various age-group demographic projections

can have significant implications for the state's revenue

and expenditure outlook. For example, strong growth of

the 45-64 age group generally benefits tax revenues since

this is the age category that routinely earns the

highest wages and salaries. Likewise, the growth in the young

adult population affects college enrollments, while that for

the 0-to-4 and 5-to-17 age groups drives K-12

enrollment growth.

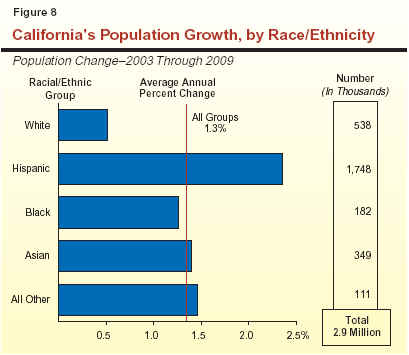

In addition to age, projected population growth will also differ markedly along other dimensions. For example:

The revenues that finance California's state General Fund budget come from a wide variety of sources, including taxes, fees, licenses, interest earnings, loans, and transfers. Over 90 percent of the total, however, is attributable to the state's three major taxes—the personal income tax (PIT), the sales and use tax (SUT), and the corporation tax (CT). In this chapter, we summarize our updated revenue projections and provide detail behind our key revenue-related assumptions.

In welcome contrast to our updates for the past two years when the key revenue-related development involved downward revisions, we are forecasting a significant improvement in the state's revenue picture compared to what was anticipated when the 2003-04 budget was adopted. Figure 1 presents our updated revenue projections.

|

Figure 1 The LAO�s General Fund

Revenue Forecast |

|||||||

|

(Dollars in Millions) |

|||||||

|

Revenue Source |

2002-03 |

2003-04 |

2004-05 |

2005-06 |

2006-07 |

2007-08 |

2008-09 |

|

Personal

income tax |

$32,442 |

$35,580 |

$38,270 |

$40,920 |

$43,840 |

$46,860 |

$50,090 |

|

Sales

and use tax |

22,330 |

23,540 |

24,850 |

26,410 |

28,030 |

29,680 |

31,370 |

|

Corporation

tax |

6,700 |

7,265 |

7,400 |

8,120 |

8,710 |

9,230 |

9,760 |

|

Other

revenues and transfers |

9,380 |

7,780 |

4,448 |

3,146 |

4,750 |

4,974 |

4,830 |

|

Total Revenues and

Transfers |

$70,852 |

$74,165 |

$74,968 |

$78,596 |

$85,330 |

$90,744 |

$96,050 |

|

Percentage

change |

-2.0% |

4.7% |

1.1% |

4.8% |

8.6% |

6.3% |

5.8% |

2003-04 Revenues. We project that

revenues will total $74.2 billion in 2003-04, a 4.7

percent increase from 2002-03. Our current estimate is

up $813 million from the 2003-04 budget forecast, reflecting the following partially offsetting factors:

2004-05

Revenues. We forecast that General Fund revenues will be $75 billion in 2004-05,

an increase of 1.1 percent from the current year.

Our updated estimate is $1.5 billion above the

2003-04 budget forecast. This reflects a $2.3 billion

increase in projected collections from the state's major

taxes, partly offset by a downward revision (from

$680 million to $200 million) in the amount of

receipts from new or renegotiated tribal gaming

compacts, along with some other downward adjustments.

Although the revenue growth rate for the budget year is only modest, the "underlying"

growth rate is considerably higher—over 6

percent—and thus more consistent with the economy's

projected moderate expansion. This discrepancy

between total versus underlying revenue growth reflects

the $3 billion in one-time funds included in the

2003-04 budget's revenue base. This is related to

the second tobacco bond ($2.2 billion) and loans

from special funds ($835 million). In addition, CT

receipts will be pulled down in 2004-05 due to the

conclusion of the two-year suspension of net operating

loss (NOL) deductions that has been in effect for

income years 2002 and 2003 (discussed further below).

The increase in our revenue forecast relative to the 2003-04 budget estimate reflects both the improving state economy and the stronger-than-expected cash performance during the past several months. Regarding the latter factor, total tax receipts during the first four months of 2003-04 are up by roughly $500 million, reflecting significantly higher PIT monies and more-modest gains in SUT and CT collections.

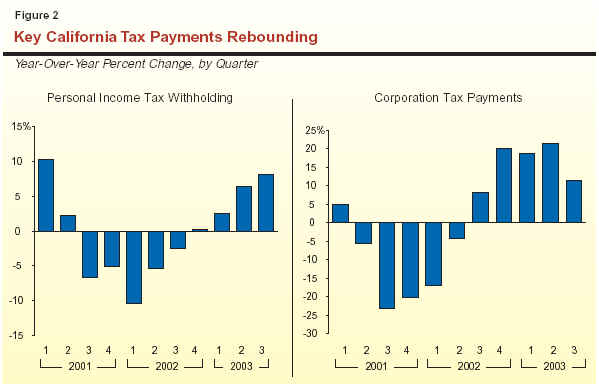

Of special significance is the strength in key payments that are tied to current economic activity. As shown in Figure 2, PIT withholding payments have steadily improved over the course of 2003, and were up a healthy 8 percent from the prior year in the third quarter. This reflected growth in wages, bonuses, and a revival in stock-option income. Similarly, CT payments jumped beginning in the fourth quarter of 2002 and have remained strong throughout 2003. While some of this strength in the CT relates to the suspension of NOL deductions noted above, a significant portion also appears to simply reflect stronger underlying business profits.

These higher tax payments suggest that, although the economic expansion has thus far

failed to produce significant job growth, the increases

in sales and output in the economy are producing meaningful growth in both personal and

corporate income in California.

The revenue totals shown in Figure 1 reflect not only basic economic developments, but also numerous revenue-related policy actions taken in conjunction with the 2002-03 and 2003-04 budgets. Key examples include:

As shown in Figure 3, the above one-time or limited-term factors can have major impacts on the General Fund revenue totals for individual years. For example, they increased the revenue totals by $7 billion in 2002-03 and nearly $4 billion in 2003-04, but will reduce revenues by varying amounts in subsequent years. The significant revenue decline shown for 2005-06 relates to the scheduled repayment of the TCRF loan.

We currently forecast that PIT receipts will

increase from $32.4 billion in 2002-03, to $35.6

billion in 2003-04, and $38.3 billion in 2004-05.

Over the longer term, we project that receipts from

this source will grow at an average annual rate of

about 7 percent between 2004-05 and 2008-09,

reaching $50.1 billion by the end of the forecast

period. Compared to the 2003-04 budget forecast, our

current estimate is up $2 billion in 2003-04 and

$2.2 billion in 2004-05.

Our upward PIT revision from the

2003-04 budget forecast is primarily related to the

recent strength in cash payments and evidence of an

improving economy and stock market.

Cash Receipts Up. Cash receipts from the

PIT during the first four months of 2003-04 are

running about 4 percent ahead of the budget estimates,

reflecting strength from a variety of payment sources,

including withholding and quarterly estimated payments. It

appears that the stronger economy is having a positive effect

on wages, bonuses, business income, and stock

market-related receipts.

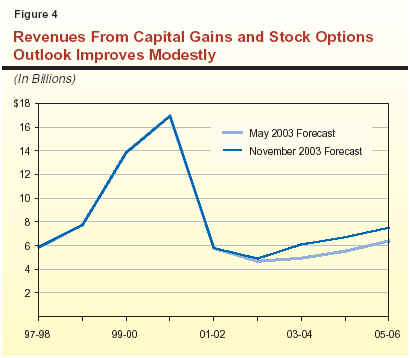

With regard to the latter factor, Figure 4 provides

some perspective on the impact of capital gains and stock

options on General Fund revenues in recent history and through

the forecast period. It shows that revenues from these

sources accounted for as much as $17 billion in PIT receipts at

the peak of the market in 2000-01, but then plunged to $6 billion in 2001-02 and

to less than $5 billion in 2002-03.

Capital Gains and Stock

Options—Strengthening but Still Down.

The figure also shows that for the 2003-04 budget forecast made last May, we

assumed that revenues from these sources would increase moderately beginning in 2003-04, but

remain well below their previous peak through the five-year forecast period. Reflecting the recent

positive stock market and revenue-related developments, we have raised our associated revenue

estimates by roughly $1.2 billion per year in our

updated forecast. Even with this improvement, however, our projected amount of revenues from

these sources still remains less than half of the

2000-01 peak through the forecast period.

We estimate that SUT receipts will total $23.5 billion in 2003-04, a 5.2 percent increase

from the prior year. We project that these receipts

will grow further to $24.9 billion in 2004-05, an

increase of 5.6 percent from the current year. Our

updated estimates for 2003-04 and 2004-05 are similar

to those in the 2003-04 budget, reflecting

slightly stronger estimates of "real" sales growth, but

slightly less growth in commodity prices than we

had assumed previously. Over the longer term, we

forecast that SUT receipts will increase at an

average annual rate of about 6 percent per year

between 2004-05 and 2008-09, reaching

$31.4 billion by the end of the forecast period.

The main determinant of SUT receipts is

taxable sales, about two-thirds of which is related

to retail spending by consumers, and about

one-third of which is related to business-to-business

transactions. The past weakness in business

spending on both new facilities and equipment has had

a major adverse impact on taxable sales during

the previous two years. In 2002, for example,

taxable spending fell by 0.9 percent, reflecting a sizable

drop in business-related transactions partially offset

by a small gain in retail spending.

Taxable Sales Growth to Pick Up. Our

forecast for 2003 assumes that an improvement in

business spending will occur in the second half of the

year, and that this half-year effect will boost overall

sales by a modest 2.8 percent for the year as a

whole. Thereafter, the continuation of this healthier

business spending on a full-year basis should

produce the 5.9 percent increase that we forecast for

calendar year 2004, and similar gains in subsequent years.

One-Time Gain From Suspended

Transfer. Our sales tax estimate for the current year also

reflects a one-time gain of $87 million related to the

one-time suspension of the annual transfer of

certain sales tax revenues from gasoline sales out of

the General Fund and into a special transportation fund.

We estimate that CT receipts will increase from $6.7 billion in 2002-03, to $7.3 billion in 2003-04, and $7.4 billion in 2004-05. Over the longer term, we forecast that collections from the CT will increase at an average annual rate of slightly over 7 percent between 2004-05 and 2008-09, reaching $9.8 billion by the final year of the forecast period. These updated estimates are up from the 2003-04 budget forecast by $230 million in 2003-04 and $245 million in 2004-05.

The main factor underlying CT receipts is

the California taxable corporate profits of firms

doing business in California. We currently estimate

that these profits will jump 16 percent in 2003 and 12.5 percent in 2004. This reflects the combined effect of large increases in sales and output and

declining unit labor costs—the latter due to

significant productivity gains across all major

industry sectors. We project that profit growth in

subsequent years will settle into a more moderate and

sustainable pace, increasing at about 6 percent per year.

NOL Deductions to Return. The CT receipts

are also being affected by two special factors. The

first is legislation passed in conjunction with the 2002-03 budget that suspended NOL carryforward allowances for 2002 and 2003. These allowances

are reinstated in 2004, with the percentage of losses

that can be deducted against future earnings

increasing from 65 percent to 100 percent effective

beginning in 2005. This provision raised revenues

by $600 million in 2003-04, but will reduce

collections by $325 million in 2004-05 and slightly

higher amounts annually thereafter.

MIC to Disappear. The second special factor

is the expiration of the manufacturers' investment credit (MIC) beginning in 2004. The statute

creating the MIC in 1994 included a provision

stating that the MIC would expire following any year

after 2000 in which the cumulative growth in

manufacturing employment (excluding aerospace)

from 1994 was less than 100,000 jobs.

Manufacturing jobs fell below the specified threshold level in

2003, triggering the expiration of the MIC effective

January 1, 2004. The elimination of this credit

will boost CT revenues by $40 million in 2003-04, $195 million in 2004-05, and up to $450 million

In this chapter, we discuss our General Fund expenditure estimates for 2002-03 and 2003-04, and our projections for 2004-05 through 2008-09, both in total and by key program area. We first look at general budgetary trends during the forecast period, and then discuss in more detail our expenditure projections for individual major program areas.

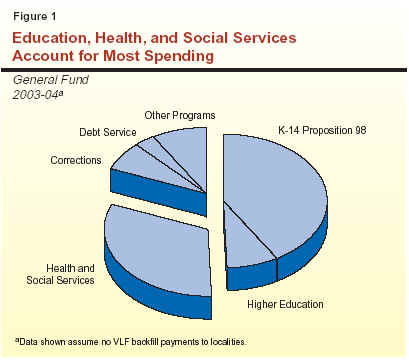

Figure 1 shows how General Fund spending is distributed among major program areas in 2003-04. It indicates that education programs account for nearly one-half of total spending, with 41 percent attributable to K-14 education and another 8 percent for the University of California (UC) and California State University (CSU). Nearly one-third of the total is for health and social services, and about 7 percent is for corrections. The remainder is for debt service, various local subventions, pension payments, and other purposes.

Figure 2 (see next page) shows our forecast for major General Fund spending categories. The impacts of a vehicle license fee (VLF) rate rollback are included at the bottom of the figure. We forecast that General Fund expenditures will jump from $73.7 billion in 2003-04 to $85.7 billion in 2004-05, an increase of 16.4 percent. This large jump is related to two main factors: (1) the expiration of one-time expenditure savings included in the 2003-04 budget, and (2) large increases in expenditures for the repayment of the deficit financing bond assumed to be issued in 2004-05.

|

Figure 2 Projected General Fund

Spending for Major Programs |

||||||||||

|

(Dollars in Millions) |

||||||||||

|

|

Estimated |

|

Forecast |

Average

Annual Growth From |

||||||

|

2002‑03 |

2003‑04 |

2004‑05 |

2005‑06 |

2006‑07 |

2007‑08 |

2008‑09 |

||||

|

Education

programs |

|

|

|

|

|

|

|

|

|

|

|

K-14�Proposition 98 |

$29,189 |

$30,513 |

|

$34,135 |

$35,978 |

$37,672 |

$39,250 |

$40,781 |

4.5% |

|

|

CSU |

2,646 |

2,430 |

|

2,500 |

2,596 |

2,711 |

2,843 |

2,998 |

4.6 |

|

|

UC |

3,059 |

2,761 |

|

2,846 |

2,955 |

3,086 |

3,236 |

3,413 |

4.6 |

|

|

Health

and Social Services |

|

|

|

|

|

|

|

|

|

|

|

Medi-Cal benefits |

$9,967 |

$10,018 |

|

$11,784 |

$12,345 |

$13,156 |

$13,892 |

$14,503 |

5.3% |

|

|

CalWORKs |

2,077 |

2,082 |

|

2,402 |

2,573 |

2,636 |

2,701 |

2,801 |

3.9 |

|

|

SSI/SSP |

3,031 |

3,380 |

|

3,550 |

3,771 |

3,975 |

4,229 |

4,546 |

6.4 |

|

|

IHSS |

1,122 |

1,269 |

|

1,425 |

1,607 |

1,831 |

2,076 |

2,343 |

13.2 |

|

|

DDS |

1,866 |

2,102 |

|

2,398 |

2,568 |

2,800 |

3,064 |

3,361 |

8.8 |

|

|

Other major programs |

4,832 |

4,556 |

|

5,499 |

5,836 |

5,923 |

6,139 |

6,404 |

3.9 |

|

|

Department

of Correctionsa |

$4,948 |

$5,084 |

|

$5,188 |

$5,458 |

$5,789 |

$5,953 |

$6,112 |

4.2% |

|

|

VLF

subventions |

$3,786 |

� |

|

� |

� |

$834 |

� |

� |

� |

|

|

Debt

service |

$2,233 |

$2,484 |

|

$3,788 |

$4,087 |

$4,480 |

$4,855 |

$5,253 |

8.5% |

|

|

Other

programs/costs |

$9,276 |

$6,996 |

|

$10,016 |

$10,771 |

$10,957 |

$11,549 |

$12,947 |

6.6% |

|

|

Totals�no

VLF backfill |

$78,031 |

$73,675 |

|

$85,727 |

$90,941 |

$96,496 |

$100,514 |

$106,275 |

5.5% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Effect of

resumed VLF backfill: |

|

|

|

|

|

|

|

|

|

|

|

VLF subventions |

� |

$3,237b |

|

$4,224 |

$4,394 |

$4,581 |

$4,787 |

$5,024 |

4.4% |

|

|

CalWORKs VLF interaction |

� |

� |

|

223 |

127 |

129 |

130 |

133 |

-12.1 |

|

|

Totals�with

VLF backfill |

$78,031 |

$76,912 |

|

$90,175 |

$95,462 |

$101,206 |

$105,431 |

$111,433 |

5.4% |

|

|

|

||||||||||

|

a

Reflects employee compensation costs starting with forecast

period (2004-05). |

||||||||||

|

b

Assumes VLF rate reduction made retroactive to October 1, 2003.

The 2003-04 amount would be $1.8 billion if rate reduction were

effective on |

||||||||||

Expiration of One-Time Savings. Major

examples in this first category are:

Deficit Financing Bond Repayment. The spending totals for 2004-05 and beyond include roughly $2.4 billion in increased annual General Fund payments for Proposition 98. These payments are part of a multistage shift of sales and property taxes (the so-called "triple flip"), and are tied to repayment of the deficit financing bond (see box on page 32).

Key Education TermsWhat Is the Maintenance Factor?Over the long-run, the Proposition 98 minimum guarantee is determined by the growth in In either of these circumstances, the Constitution requires the state to restore in future years

the difference between the actual level of spending and the long-term Test 2 level of spending.

This difference is known as the maintenance factor. Generally, maintenance factor is restored

during Test 2 years (when the growth of General Fund revenues exceeds growth in personal income).

For instance, in 2001-02 when General Fund revenues fell by more than 17 percent (a Test 3 year),

the Legislature appropriated $3.9 billion less than would have been required if Test 2 were

operative. This created a $3.9 billion maintenance factor that must be restored in the future.

In 2002-03, the state was required to provide approximately $500 million to begin restoring

the maintenance factor. Based on our current forecast, the state will be required to restore

additional maintenance factor of $875 million in 2003-04 and around $600 million in 2004-05. Currently,

for each $1 increase in General Fund revenues, there is around a $.50 increase in the minimum

guarantee as more maintenance factor is required to be restored. What Is the Deficit Factor?Because school district revenue limit funding is continuously appropriated, the Legislature must amend statute if it wants to provide less than the full statutory COLA or enrollment funding, or wants to make additional reductions to revenue limit funding. Technically, the Legislature and Governor "deficit" (that is, reduce) the revenue limit funding by some factor or percentage. In the early 1990s the revenue limit deficit factor grew to 11 percent after several consecutive years of not providing school districts with a full statutory COLA. In 2000-01, the state provided an addition $1.8 billion in revenue limit funding to eliminate the deficit factor. In 2003-04, the state created a new deficit factor of 3.1 percent or $894 million—consisting of a base reduction of 1.2 percent and a foregone COLA (1.9 percent). This deficit factor would be fully restored in 2005-06 absent additional legislative action. The Triple FlipA key feature of the 2003-04 budget package was the method devised to finance the deficit financing bonds. The state enacted a three-step approach—commonly referred to as the triple flip—that provides a dedicated funding source for the deficit bonds:

The retirement of the bonds is dependent on revenues received by the state, but is expected to occur over roughly five years. The swap of sales taxes for property taxes ends after the deficit financing bonds are repaid.

|

The right-hand column of Figure 2 shows

the average annual growth rates from 2004-05

through 2008-09 that we are projecting. Overall

spending is projected to grow by an average of about

5.5 percent per year, reflecting divergent trends

among major state program areas. With regard to

specific individual program areas, the figure shows that:

State spending for K-14 education

(K-12 schools and community colleges) is governed

largely by Proposition 98, passed by the voters in

1988. Proposition 98 sets the minimum amount the

state must provide for California's public K-12

education system and the California Community Colleges (CCC). Proposition 98 is funded from

the state General Fund and local property taxes

and accounts for almost 80 percent of total support

for K-14 education. The remainder is from a

variety of sources including federal funds, lottery

revenue, and other local revenues.

California's public K-12 education system consists of more than 1,000 locally governed

school districts and county offices of education

serving about 6.2 million K-12 students. In addition,

these entities serve infants and preschool students

receiving child care and individuals in adult

education programs. The CCC provides instruction to

about 1.1 million full-time equivalent students at

108 colleges operated by 72 locally governed districts.

Figure 3 displays our projections of the Proposition 98 minimum guarantee—as well as its General Fund and local property tax funding components—throughout the forecast period. We would also note that our budget totals reflect an updated figure for 2002-03 Proposition 98 spending which is $100 million higher than assumed at the passage of the 2003-04 budget package.

|

Figure 3 The LAO Proposition 98

Forecast |

|||||||

|

2003-04 Through 2008-09 |

|||||||

|

|

2003-04 |

2004-05a |

2005-06 |

2006-07 |

2007-08 |

2008-09 |

|

|

Budget

Act |

Revised |

||||||

|

Proposition 98 |

|

|

|

|

|

|

|

|

General

Fund |

$30.0 |

$30.5 |

$34.1 |

$36.0 |

$37.7 |

$39.2 |

$40.8 |

|

Local

property tax |

15.7 |

16.1 |

14.9 |

16.0 |

17.3 |

18.5 |

19.7 |

|

Totals |

$45.7 |

$46.6 |

$49.0 |

$52.0 |

$54.9 |

$57.8 |

$60.5 |

|

|

|||||||

|

a

Funding components reflect a $2.45 billion reduction in property

tax revenues�and commensurate increase in General Fund support�due

to the triple flip budget solution, which has an ongoing effect

throughout the forecast period. |

|||||||

Forecast for the Current Year. The

2003-04 Budget Act appropriates $45.7 billion in

Proposition 98 spending. We now forecast a minimum

guarantee of $46.6 billion for 2003-04, around

$875 million higher than the current appropriation level.

The increase in the minimum guarantee is mainly

due to our estimate of $2.2 billion in higher

General Fund tax revenues in 2003-04, but is also

affected by changes in school attendance and

population estimates. Because the 2003-04 appropriation

level has not changed, we forecast that the

Proposition 98 minimum guarantee is now underappropriated by $875 million. Based on

the legislative intent language in Chapter 228,

Statutes of 2003 (AB 1756, Budget Committee) to spend

at the minimum guarantee in 2003-04 and 2004-05, our fiscal forecast assumes that the Legislature

appropriates an additional $875 million in

2003-04. We forecast that local property tax revenues

will be $345 million higher than assumed in the

2003-04 Budget Act. Thus, the state would be required

to provide an additional $530 million from the

General Fund to meet the minimum guarantee. This additional funding would reduce the

outstanding "maintenance factor" to just under $2.5 billion

(see discussion in box on page 32).

Forecast for the Budget Year. For 2004-05,

we estimate the Proposition 98 minimum

guarantee will total $49 billion. This is $2.4 billion

(5.1 percent) more than in 2003-04. During 2004-05, K-14 local property tax revenue will decrease by a net of $1.2 billion because of (1) a

$2.45 billion transfer of K-14 local property taxes to cities

and counties to backfill foregone sales tax revenue

as part of the triple flip (also discussed in box on

page 32) and (2) $1.2 billion in increased local

property tax revenues because of increased assessed

property values. Thus, General Fund costs of

meeting the Proposition 98 minimum guarantee will

grow by $3.6 billion between the current 2003-04

level and 2004-05 (an 11.9 percent increase).

Out-Years' Forecast. For the remainder of

the forecast period, we estimate that growth in

total Proposition 98 spending will average

$2.9 billion annually (5.4 percent). Strong property tax

growth averaging $1.2 billion annually (7.4 percent)

helps reduce the impact on the General Fund.

General Fund support for Proposition 98 will grow

around $1.7 billion annually (4.5 percent).

Key Forecast Factors. General Fund

expenditures for Proposition 98 depend on a variety of

factors—including K-12 average daily

attendance (ADA), per capita personal income, per capita

General Fund revenues, and local property taxes.

Figure 4 summarizes our assumptions for these

factors and the K-12 COLA rate.

Figure 4 The LAO Proposition 98

Forecast Factors 2003-04 2004-05 2005-06 2006-07 2007-08 2008-09 Proposition 98 �Test� 2 2 2 2 2 2 Annual Percentage Change K-12

average daily attendance 1.1% 1.0% 0.9% 0.5% 0.3% -0.1% Per

capita personal income 2.3 2.8 4.1 5.0 4.6 4.5 Per

capita General Fund 5.5 4.5 5.5 5.2 4.9 4.9 State

population 1.5 1.3 1.3 1.3 1.4 1.3 Local

property taxes 8.8 7.6a 7.9 7.7 7.2 6.7 K-12

COLA 1.9 2.2 2.5 2.8 2.8 2.8 a

Growth rate in 2004-05 reflects the underlying growth in school

district and community college property tax revenues. This rate does not

account for changes in revenues resulting from the triple flip.

For our forecast:

The state's actions to address the 2002-03 and 2003-04 budget problems in K-14 education relied heavily on (1) one-time solutions, (2) borrowing from the future by deferring appropriations to future years to support current costs, and (3) a large limited-term reduction in general purpose funding for K-12. The growth in Proposition 98 funding over the forecast period would allow the state to (1) address the fiscal obligations created by the recent budget solutions, (2) provide growth and COLA, and (3) allocate roughly an additional $1 billion in growth annually throughout the forecast period for program expansions or restorations. In this section, we provide information on the statutory cost pressures for K-14 education over the forecast period. Specifically, these fiscal obligations include:

Because of the strong growth in

Proposition 98 over the forecast period, the Legislature could

fund all of the cost pressures described above, and

still allocate roughly $1 billion annually throughout

the forecast period for program restorations or

expansions. The Legislature's choices in allocating

this additional funding will affect the "split" of

Proposition 98 resources between K-12 schools and

CCC. The CCC's share of Proposition 98 resources

has ranged between 9 percent and 11 percent.

The Proposition 98 levels in our forecast suggest

that the Legislature will have considerable discretion

in how to allocate K-14 funding beyond growth, COLA, and other obligations.

Proposition 49. Approved by voters in

2002, Proposition 49 requires that the state

appropriate additional funding for after school programs

beginning in 2004-05 if certain conditions are

met. Specifically, the state must appropriate up to

an additional $430 million for after school

programs if total state spending reaches a specified

threshold. Based on our revenue forecast, the state

would not be required under Proposition 49 to

augment after school programs over the forecast period.

In addition to community colleges, the

state's public higher education system includes UC

and CSU. The UC consists of eight general

campuses, one health sciences campus, numerous special

research facilities, and a soon-to-open tenth

campus in Merced. The UC awards bachelor's, master's,

and doctoral degrees, as well as various

professional degrees. The UC has primary jurisdiction

over public university research. The CSU consists of

23 campuses and several off-campus centers. The

CSU grants bachelor's and master's degrees and may award doctoral degrees under specified

circumstances.

The Spending Forecast. We estimate that

General Fund spending for UC and CSU (excluding funding for capital outlay and debt service)

will increase from $5.2 billion in 2003-04 to $5.3

billion in 2004-05. This is an increase of $154

million, or 3 percent. It primarily reflects the

restoration of one-time reductions that were made in

the 2003-04 budget. By 2008-09, we estimate that

that spending for UC and CSU will increase to $6.4

billion, reflecting average annual increases of

almost 5 percent starting in 2005-06.

Key Forecast Factors. Consistent with the

Legislature's expressed intent, our forecast assumes

no funding for enrollment growth, new salary

increases, or discretionary price adjustments in

2004-05. We assume that the segments will begin

receiving additional funds for COLAs and

enrollment growth starting in 2005-06. Over the forecast

period, inflation is projected to average about

2.8 percent annually.

With regard to enrollment growth, our forecasts are based primarily on population growth

among 18 to 24 year olds. This population is

currently growing at a relatively low rate, although we

project that this rate will increase to about 2.6 percent

by the end of the forecast period. While we assume that there will be no funding for enrollment

growth in 2004-05, we have assumed that the demand

created by population growth in 2004-05 would be accommodated in subsequent fiscal years.

Our estimates assume that college participation rates will remain relatively constant throughout

the forecast period. This is for three reasons. First,

we note that college participation rates are already

at historic highs. Second, recent and anticipated

fee increases could dampen the potential for

further increases in participation rates. Finally, recent

reductions in funding for UC and CSU outreach programs could further reduce the likelihood that

participation rates would increase significantly

during the forecast period.

Cal Grant Costs Likely to Increase

Substantially. We estimate that spending for financial aid

programs administered by the Student Aid Commission will increase from

$683 million in 2003-04 to approximately $1.1 billion in

2008-09. The bulk of the expected increase is attributable to the

Cal Grant Entitlement programs. Effective beginning in

2001-02, these programs guarantee financial aid to recent

high school graduates and community college transfer

students under 24 years of age. Because these programs are still

relatively new, future growth in their participation rates remains

uncertain. However, our projections assume that student

participation in the entitlement programs will continue to

grow somewhat faster than student enrollment.

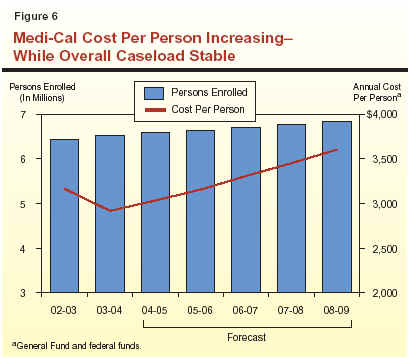

The Medi-Cal Program (the federal

Medicaid Program in California) provides health care

services to recipients of CalWORKs or SSI/SSP

grants, and other low-income persons who meet the

program's eligibility criteria (primarily families

with children and the elderly, blind, or disabled).

The state and federal governments share most of

the program costs on a roughly equal basis.

The Spending Forecast. We estimate that

General Fund spending for Medi-Cal local

assistance (including benefits, county administration of

eligibility, and other costs) will reach $10.7 billion

in the current year, about a $170 million increase

over the amount appropriated in the 2003-04

Budget Act. We project that, barring other actions by the

Legislature and Governor, General Fund support would grow to $12.6 billion in 2004-05, a

17 percent increase from current-year expenditures.

This is largely due to the one-time effect of the

accounting shift of the program from an accrual to

cash basis as well as the phase-out of a temporary

increase in the federal share of support for the

Medicaid Program. By the end of the forecast

period in 2008-09, we estimate that General Fund

spending for Medi-Cal will reach $15.5 billion, an

average annual increase of 7.8 percent over the

projection period.

Key Forecast Factors. Several factors play a

significant role in our forecast:

The Healthy Families Program (HFP)

implements the federal State Children's Health

Insurance Program, enacted in 1997. Funding generally is

on a two-to-one federal/state matching basis. The

program offers health insurance to eligible children

in families with incomes below 250 percent of the

federal poverty level. Families pay a relatively

low monthly premium and are offered coverage

similar to that available to state employees.

The Spending Forecast. We estimate that

overall General Fund spending for HFP will be $290 million in 2003-04. We further estimate

that overall General Fund spending for the program

will increase about 5.5 percent in 2004-05 to

about $306 million, and that by 2008-09 the program