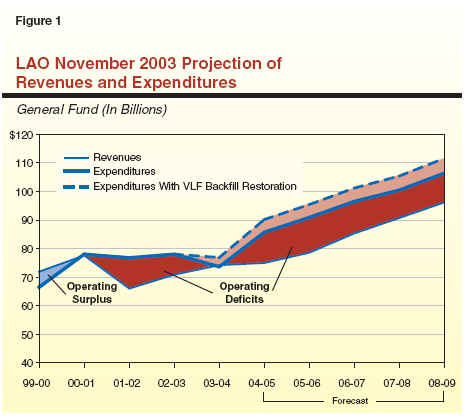

The basic challenge confronting lawmakers in crafting a 2004-05 budget was finding a way to once again close a large budget shortfall, which had plagued the state since 2001-02 when expenditures exceeded revenues due to a revenue plunge. At the beginning of the 2004-05 budget cycle—and subsequent to the new Governor's decision to roll back the statutorily triggered vehicle license fee (VLF) increase—we estimated the budget gap to be roughly $15 billion in 2004-05 and beyond, absent corrective actions (see Figure 1 next page). While in subsequent months there were numerous changes to the underlying revenue and expenditure estimates on which this gap estimate was based, the final budget dealt with a 2004-05 shortfall of approximately that same magnitude.

In this chapter, we (1) discuss the factors behind the 2004-05 shortfall, (2) highlight the major budget solutions included in the 2004-05 budget package, and (3) provide initial comments on how the actions taken in the 2004-05 budget will affect the outlook for 2005-06 and beyond.

2003-04 Budget. One year earlier in the 2003-04 budget, the Governor

and Legislature had temporarily closed a major cumulative budget

shortfall—estimated to be over $30 billion—primarily through substantial

borrowing, an assumed triggered increase in the VLF, and program savings.

While the plan had a projected reserve of over $2 billion for 2003-04, its

heavy reliance on borrowing and other one-time solutions meant that the

structural operating shortfall (revenues minus expenditures) was destined

to return in 2004-05. At the time of the budget's passage, our office

estimated the operating shortfall would be over $10 billion per year even

if all of the 2003-04 budget's assumptions held and revenues grew at a

moderate pace.

A key element of the 2003-04 budget was the authorization of a deficit financing bond. The proceeds of this bond were to be used to eliminate the 2002-03 year-end deficit, which at the time was estimated to be $10.7 billion. (In subsequent months, the estimate of the 2002-03 deficit declined, and the maximum amount of bonds authorized to be sold correspondingly fell to $8.6 billion.) Repayment of the bond was tied to one-half cent of the sales tax, and would have cost the General Fund about $2.4 billion annually for about five years beginning in 2004-05.

Post 2003-04 Budget Developments. Following the adoption of the 2003-04 budget, the projected 2004-05 budget shortfall expanded, mainly as the result of two factors:

Although these factors were partly offset by an improving revenue picture, the cumulative shortfall facing policymakers in 2004-05 had climbed to about $17 billion by the time the new budget was introduced in January 2004. This gap consisted of a roughly $2 billion year-end shortfall in the 2003-04 budget and a $15 billion ongoing operating shortfall in 2004-05. Further improvements in the revenue picture between late 2003 and mid-2004 narrowed the gap some. However, the final 2004-05 budget still had to deal with a projected shortfall of roughly $15 billion.

The budget signed by the Governor on July 31, 2004 contained about $16.1 billion in combined two-year solutions. These solutions enabled the state to eliminate the budget shortfall projected for 2004-05 and build up a modest year-end reserve of $768 million. As shown in Figure 2, these solutions can be divided into six categories—namely, (1) program savings, (2) the use of Proposition 57 bonds, (3) other loans and borrowing, (4) fund shifts, (5) increased revenues and transfers, and (6) diversions of local property taxes.

|

Figure 2 Allocation of

2004‑05 Budget Solutions |

|||

|

(In Billions) |

|||

|

|

2003‑04 |

2004‑05 |

Two-Year

Total |

|

Program savings |

$0.4 |

$3.4 |

$3.8 |

|

Proposition 57 bond: |

|

|

|

|

Larger

proceeds |

0.7 |

2.0 |

2.7 |

|

Reduced

debt service |

|

1.2 |

1.2 |

|

Other loans and borrowing |

1.6 |

1.9 |

3.5 |

|

Fund shifts |

0.1 |

1.7 |

1.8 |

|

Increased revenues, transfers |

0.2 |

1.6 |

1.8 |

|

Diversion of property taxes |

� |

1.3 |

1.3 |

|

Totals |

$3.0 |

$13.1 |

$16.1 |

Program Savings. The budget includes about $3.8 billion in program savings. Over half the total is related to a reduction in K-14 education spending related to the suspension of Proposition 98. Other savings include three-month delays in cost-of-living adjustments for California Work Opportunity and Responsibility to Kids and Supplemental Security Income/ State Supplementary Payment grants, reductions in institutional support for the University of California (UC) and California State University (CSU), and unallocated reductions in state operations spending.

Proposition 57 Bond. In December 2003, the Governor and Legislature placed on the March 2004 ballot two measures—namely, Proposition 57, which authorized up to $15 billion in deficit financing bonds, and Proposition 58, which put in the State Constitution an annual budget reserve requirement, an expanded balanced budget requirement, and a prohibition against deficit borrowing in the future. The Proposition 57 bond proceeds were proposed to be used in place of the deficit bond that had been authorized in the 2003-04 budget, and which was being challenged in court. Following voter approval of Propositions 57 and 58, the state sold $11.3 billion in deficit bonds to help with the budget, leaving approximately $3.5 billion in additional bonds available for 2005-06 and subsequent years. Relative to the previously authorized bonds, the Proposition 57 bonds benefited the General Fund in the following two ways:

Other Loans and Borrowing. This category accounts for $3.5 billion in solutions. It includes $929 million related to the use of proceeds from the sale of a pension obligation bond to offset payments to the Public Employees' Retirement System. It also includes a "settle-up loan" of over $1.2 billion related to 2003-04 and prior-year obligations to Proposition 98 education, and a Proposition 42 loan of $1.2 billion from transportation funds.

Fund Shifts. This category totals $1.8 billion, and includes numerous

funding redirections and fee increases. It includes $366 million related to

increased higher education fees, which are used to offset General

Fund support for UC, CSU, and California Community Colleges. It also

in

cludes $450 million related to a new law change requiring that

75 percent of court-related punitive damage awards be allocated the state. The

budget assumes that these funds will be used to offset General Fund costs

for state programs. Finally, this category includes $216 million related to

a federal waiver allowing federal financial participation of the state's

current state-only In-Home Supportive Services cases.

Increased Revenues and Transfers. This category includes $1.8 billion in total solutions. It includes targeted tax increases related to a two-year suspension of the teachers' tax credit ($210 million) and a two-year rule change related to the use tax on out-of-state purchases of certain large items such as yachts and airplanes ($26 million). It also includes $333 million from a two-month tax amnesty program beginning in the spring of 2005. The budget also includes various transfers from state transportation funds to the General Fund.

Diversion of Local Property Taxes. The budget includes a $1.3 billion annual diversion of local property tax revenues for the benefit of the General Fund in 2004-05 and 2005-06. This diversion is part of a broader agreement that places limits on future state diversions of certain local taxes and "swaps" VLF backfill payments and property taxes.

The final budget includes agreements with K-12 education and local governments. We discuss the detail of these agreements in Chapter 4. However, one element these agreements have in common is a fiscal trade-off. Each entity concedes something in 2004-05—a smaller funding increase in the case of education and a diversion of property taxes in the case of local governments—in return for funding restorations and other commitments in future years.

The 2004-05 budget includes significant ongoing savings and it makes some progress toward resolving the state's ongoing structural budget shortfall. Nevertheless, like the two prior budgets, the current spending plan (1) contains a significant number of one-time or limited-term solutions and (2) obligates additional spending in future years. As shown in Figure 3 (see next page), major one-time savings include: the use of $2 billion in Proposition 57 bonds to support 2004-05 General Fund program spending, $929 million due to the sale of a pension obligation bond, the deferral of $1.2 billion in Proposition 42 transportation spending, and the postponement of local government mandate payments ($200 million) bringing the total of deferred reimbursements to $1.5 billion. In addition, the savings related to the $1.3 billion diversion of local property taxes and the suspension of the teachers' tax credit will expire after two years. Figure 3 also shows that deferred out-year costs associated with actions taken in 2004-05 and prior-year budgets include: Proposition 98 settle-up payments, Proposition 42 loan repayments, and repayment of the VLF "gap" loan from local governments. (The 2004-05 budget does include early repayment of a $1.4 billion loan from the Traffic Congestion Relief Fund, mostly financed by a tribal gaming bond.)

The combination of these factors suggests that state will continue to

face out-year budget shortfalls, absent corrective action. Based on the

May Revision budget plan, we had previously estimated these out-year

shortfalls to be in the range of $6 billion in 2005-06 and $8 billion in

2006-07. The final actions on the budget—which raised ongoing spending

commitments relative to the May Revision in several areas—will likely add

to these out-year projected shortfalls. While the remaining

Proposition 57 bond authority (about $3.5 billion) is available to offset some of

these shortfalls, it appears that substantial additional actions will be needed

to bring future budgets into balance. We will be updating our projections

of out-year budget shortfalls to reflect both the final budget actions and

current economic and revenue developments in our annual publication

entitled California's Fiscal Outlook, scheduled to be released in November 2004.

|

Figure 3 Key Factors Contributing

to Future Operating Shortfalls |

|

|

|

Limited-Term Solutions in 2004‑05 Budget |

|

Deficit bonds ($2 billion) |

|

Pension bond ($929 million) |

|

Proposition 42 loan ($1.2 billion) |

|

Diversion of local property taxes ($1.3 billion annually for

two years) |

|

Suspension of teachers� tax credit (about $200 million

annually for two years) |

|

Postponement of local mandate payments (about $200 million) |

|

Deferred Out-Year Costs |

|

Proposition 98 settle-up payments (about $150 million

annually beginning in 2006‑07) |

|

Proposition 42 loan repayments ($1.2 billion in

2007‑08, $1 billion in 2008‑09) |

|

VLF �gap� loan repayment ($1.3 billion in 2006‑07) |

The state spending plan for 2004-05 includes total expenditures from all funds of $105.4 billion. As indicated in Figure 1, this total includes budgetary spending of $102.4 billion, reflecting $78.7 billion from the General Fund and $23.7 billion from special funds. In addition, spending from selected bond funds totals $3 billion. These bond-fund expenditures reflect the use of bond proceeds on capital outlay projects in 2004-05. The General Fund costs of these outlays, however, involve the associated ongoing principal and interest payments that must be made until the bonds are retired; thus, for budgetary scoring purposes, these costs show up as General Fund debt-service expenditures.

As Figure 1 shows, total state spending falls by a net of $1.9 billion (1.8 percent) between 2003-04 and 2004-05. This consists of a $1 billion (1.3 percent) increase for the General Fund, a $4.3 billion (22 percent) increase in special funds, but a $7.3 billion decline in spending from bond funds.

|

Figure 1 The 2004-05 |

|||||

|

(Dollars in Millions) |

|||||

|

Fund Type |

Actual |

Estimated |

Enacted |

Change

From |

|

|

Amount |

Percent |

||||

|

General Fund |

$77,482 |

$77,633 |

$78,681 |

$1,047 |

1.3% |

|

Special funds |

18,282 |

19,431 |

23,701 |

4,270 |

22.0 |

|

Budget Totals |

$95,764 |

$97,065 |

$102,382 |

$5,317 |

5.5% |

|

Selected bond funds |

$11,015 |

10,249 |

2,995 |

-7,253 |

-70.8 |

|

Totals |

$106,779 |

$107,313 |

$105,377 |

-$1,936 |

-1.8% |

All three components of spending are affected by special factors. As discussed below, the General Fund spending totals are affected by borrowing, accounting changes, and other deferrals taken to balance the budgets in 2003-04 and 2004-05. The major special funds increase includes new spending associated with the repayment of deficit bonds approved by the voters in March 2004. Finally, over half of the decline in bond fund spending in 2004-05 is related to how education bond expenditures are recorded for budgetary purposes. Specifically, K-12 education bonds are shown as expenditures from bond funds when they are allocated to projects by the State Allocation Board. The 2002-03 and 2003-04 spending totals include allocation of most of the bonds approved by voters in the November 2002 election. However, the 2004-05 expenditure totals do not yet include the allocation of bonds approved in the 2004 election.

Figure 2 summarizes the estimated General Fund condition for 2003-04 and 2004-05 that results from the adopted spending plan.

|

Figure 2 The 2004‑05 Budget

Package |

|||

|

(Dollars in Millions) |

|||

|

|

2003‑04 |

2004‑05 |

Percent |

|

Prior-year fund balance |

$4,178 |

$3,127 |

|

|

Revenues and transfers |

74,570 |

77,251 |

3.6% |

|

Deficit Financing Bond |

2,012 |

� |

|

|

Total

resources available |

$80,760 |

$80,378 |

|

|

Expenditures |

$75,621 |

$80,693 |

6.7% |

|

Deficit Recovery Fund transfer |

2,012 |

-2,012 |

|

|

Total

expenditures |

$77,633 |

$78,681 |

|

|

Ending fund balance |

$3,127 |

$1,697 |

|

|

Encumbrances |

929 |

929 |

|

|

Reserve |

$2,198 |

$768 |

|

|

Proposition 98 |

� |

($302) |

|

|

Non-Proposition 98 |

� |

($466) |

|

2003-04. The budget assumes a prior-year balance of $4.2 billion, revenues and deficit bond proceeds totaling $76.5 billion, expenditures of $77.6 billion, and a year-end balance of $3.1 billion. After setting aside $929 million for encumbrances, 2003-04 ends with a positive reserve of $2.2 billion. The 2003-04 General Fund condition reflects the sale of $11.3 billion in Proposition 57 deficit bonds. About $9.3 billion of the proceeds were used to eliminate the 2002-03 deficit and to build up a reserve. The remaining $2 billion is reflected for accounting purposes as both revenues and expenditures in 2003-04—as the bond proceeds are first placed into the General Fund but then are subsequently transferred back out of the General Fund to a special fund.

2004-05. The budget assumes 2004-05 revenues of $77.3 billion, expenditures of $78.7 billion, and an ending balance of $1.7 billion. After setting aside $929 million for encumbrances, the budget reflects a reserve of $768 million. Of the reserve total, $302 million is designated for Proposition 98 purposes, and the remaining $466 million is available for any General Fund purpose.

As indicated in Figure 3, the 1.3 percent increase in 2004-05 General Fund spending is the net result of sharp increases in some programs and sharp decreases in others. In many areas of the budget, spending totals have been affected by special factors in either or both 2003-04 and 2004-05. For example:

|

Figure 3 The 2004‑05 Budget

Package |

|||||

|

(Dollars in Millions) |

|||||

|

|

Actual |

Estimated |

Enacted |

Change

From 2003‑04 |

|

|

Amount |

Percent |

||||

|

K-12 Education |

$27,112 |

$29,177 |

$32,468 |

$3,291 |

11.3% |

|

Higher Education |

|

|

|

|

|

|

CCC |

2,738 |

2,281 |

3,050 |

769 |

33.7 |

|

UC |

3,176 |

2,908 |

2,721 |

-187 |

-6.4 |

|

CSU |

2,698 |

2,630 |

2,448 |

-182 |

-6.9 |

|

Other |

874 |

985 |

1,098 |

113 |

11.5 |

|

Health |

14,254 |

14,012 |

16,320 |

2,308 |

16.5 |

|

Social Services |

8,806 |

8,957 |

9,147 |

190 |

2.1 |

|

Criminal Justice |

7,855 |

7,399 |

8,455 |

1,056 |

14.3 |

|

Vehicle License Fee subventions |

3,797 |

2,689 |

� |

-2,689 |

� |

|

Deficit Recovery Fund transfer |

� |

2,012 |

-2,012 |

� |

� |

|

All other |

6,172 |

4,583 |

4,986 |

403 |

8.8 |

|

Totals |

$77,482 |

$77,634 |

$78,681 |

$1,047 |

1.3% |

After adjusting for these and related special factors, underlying spending on state programs is estimated to grow at about 3 percent between 2003-04 and 2004-05.

In this section, we highlight the major developments in the evolution of the 2004-05 budget, beginning with the Governor's November 2003 proposals and ending in late July 2004, when the budget was signed into law.

After taking office in November 2003, the new Governor called a special session to place a deficit bond issue and a revised spending limit before the voters in March 2004. After several weeks of negotiations, the administration's initial cap proposal was replaced with a measure that (1) restricted future deficit borrowing, (2) required that budgets passed by the Legislature and signed by the Governor be balanced, and (3) required that, beginning in 2006-07, a portion of annual revenues be set aside into a budget stabilization account. In mid-December, the Legislature passed the deficit-bond proposal and the revised companion measure, which were subsequently placed before the voters as Proposition 57 and Proposition 58, respectively. (These measures were subsequently passed by the voters at the March 2004 election.)

The administration also proposed a variety of mid-year budget reductions in health, social services, and other state programs in late November. No action was taken on these measures, however, and many of the mid-year reductions were subsequently incorporated into the Governor's January budget proposal.

In January 2004, the Governor proposed a 2004-05 General Fund budget that addressed a shortfall estimated to be about $17 billion. As indicated in Figure 4 and discussed below, it proposed widespread spending reductions, borrowing, a diversion of local property taxes for the benefit of the state, and various funding shifts and transfers from transportation funds.

|

Figure 4 Key Elements of January

Budget Proposal for 2004-05 |

|

|

|

�

Program Savings From Throughout Budget |

|

� Significant

reductions in education, health, social services, and |

|

�

Many reductions were ongoing in nature |

|

�

Local Property Tax Diversion |

|

�

$12.3 Billion in Proposition 57 Bond Proceeds |

|

�

Other Borrowing, Fund Shifts, Transfers, and Loans |

|

�

Pension bond |

|

�

Redirection of transportation funds |

Program Savings. The plan contained about $7 billion in program savings from most areas of the budget. These included:

Proposition 57 Bonds. The budget also assumed $12.3 billion in proceeds from Proposition 57 bonds, which were proposed to be used in place of the $10.7 billion of statutory bonds that had been authorized in the 2003-04 budget. These previously authorized bonds were facing legal challenges at the time.

Other Proposals. The budget's other proposals included: (1) an ongoing $1.3 billion shift of local property taxes from local governments to the benefit of the state; (2) a shift of about $685 million in transportation funds to the General Fund; and (3) a deferral of $1 billion in "settle-up" obligations to Proposition 98 attributable to 2003-04 and prior years. It also proposed significant CalWORKs reforms involving stricter work requirements and greater sanctions, and significant K-12 spending reforms relating to categorical funding.

The May Revision reflected an over-$3 billion increase in available total resources, which it proposed to use to (1) scale back many of the budget reductions proposed in health and transportation, and (2) lower the amount of Proposition 57 bonds used in the 2004-05 budget.

Improved Revenue Picture. The revenue picture improved by about $3.3 billion between January and mid-May, when the Governor released his revised spending plan for 2004-05. The improvement was related to (1) approximately $1.3 billion from stronger-than-expected revenues from an abusive tax shelter amnesty program (2) another $1 billion from an accounting change resulting in accruals of additional revenues, and (3) a $1.3 billion increase in the revenue outlook for the 2003-04 and 2004-05 fiscal years combined.

Spending Restorations. As indicated in Figure 5, the Governor used the additional projected revenue proceeds to partially restore reductions that had been proposed in the areas of health, social services, transportation, and education spending and reduced reliance on deficit bonds. Specifically, the administration:

|

Figure 5 May Revision: Key Changes

From January Proposal |

|

|

|

�

Spending Restorations in Health and Social Services |

|

� Eliminated

proposals for provider rate cuts and enrollment caps |

|

� Restored

funding for IHSS residual program, sought federal waiver |

|

�

New Proposals |

|

� Employee

compensation reductions |

|

� Punitive

damage award payments to state |

|

� Dedication

of tribal gaming bond proceeds to transportation loan |

|

�

New Agreements |

|

� Local

government, including limit on property tax diversion to two |

|

� UC and

CSU compacts |

In other areas, the administration eliminated proposals to transfer transportation funds to the General Fund and modified the proposal to suspend Proposition 42 payments. Under the revised plan, the Proposition 42 suspension was replaced by a "loan" from transportation funds. In effect, the amount owed to transportation, along with interest, was proposed to be deferred until 2007-08.

The budget also replaced the $400 million unallocated reduction in corrections primarily with a proposed reduction in employment compensation through renegotiation of existing collective bargaining agreements with correctional officers and other state employees. The administration proposed a law change requiring that 75 percent of court-ordered punitive damage awards be directed to the state's General Fund. Finally, the administration stated its intent that proceeds from bonds related to prospective tribal gaming agreements would be used to repay the loans from the Traffic Congestion Relief Fund (TCRF).

New Agreements. The May Revision embodied the Governor's agreement reached in the spring with local governments, and a compact with University of California (UC) and California State University (CSU). Under the local government agreement, the ongoing $1.3 billion annual property tax shift proposed in January was limited to two years. The agreement also included a complex swap of VLF "backfill" revenues for school district property taxes. In addition, the Legislature was asked to place before the statewide voters in November a constitutional amendment. This amendment would restrict the state's authority to: (1) reduce noneducation local government taxes, except for the $1.3 billion shift of property taxes from these agencies for the benefit of the state budget in 2004-05 and 2005-06 and (2) impose mandates without providing annual reimbursements.

Under the compact with higher education, UC and CSU would receive future funding increases for base support and enrollment increases. The compact also calls for annual increases in student fees, which would be retained by the segments. Finally, it commits the segments to provide annual reports on a variety of activities and outcomes.

Following the May Revision, the Conference Committee met to reconcile the budget differences of the two houses. Following conference actions and approximately six weeks of negotiations between the Governor and legislative leadership, an agreement was reached in late July. The budget was passed by the Assembly on July 28 and the Senate on July 29. After using his line-item veto authority to delete about $116 million ($80 million General Fund) in spending, the budget was signed by the Governor on July 31, 2004.

Comparison to the May Revision. As indicated in Figure 6, the final

budget package includes several key provisions from the Governor's

May

|

Figure 6 Final Budget: Comparison

to May Revision for 2004‑05 |

|

|

|

�

Key Similarities |

|

� K-12

education funding |

|

� Higher

education fee increases |

|

� Local

government agreement, including property tax diversion |

|

� Transportation funding |

|

� Proposition 57

bond amounts and pension bonds |

|

� Punitive

damage award payments to state |

|

�

Key Differences |

|

� Targeted

restorations for higher education |

|

� CalWorks

and SSI/SSP COLAs delayed instead of suspended |

|

� CalWorks

grant reduction rejected |

|

� Most

employee compensation funding restored |

|

� Teachers�

tax credit suspended |

Revision. It provides for a two-year $1.3 billion diversion of

property taxes and incorporates most of the Governor's earlier agreement

with local governments. It includes a roughly $2 billion reduction in

Proposition 98 funding relative to the minimum guarantee, and significant

fee increases in higher education. It contains the May Revision proposals

related to court-ordered punitive damage awards and pension

obligation bonds, and it assumes the sale of $11.3 billion in Proposition 57 bonds.

It also assumes that proceeds from tribal gaming related bond sales will

be used to repay a loan from the TCRF.

At the same time, the final budget differs from the Governor's May Revision proposal in several important ways. For example:

Background. Article XIII B of the State Constitution places limits on the appropriation of taxes for the state and each of its local entities. Certain appropriations, however, such as for capital outlay and subventions to local governments, are specifically exempted from the state's limit. As modified by Proposition 111 in 1990, Article XIII B requires that any revenues in excess of the limit that are received over a two-year period be split evenly between taxpayer rebates and increased school spending.

State's Position Relative to Its Limit. As a result of the previous sharp decline in revenues, the level of state spending is now well below the spending limit. Specifically, based on the revenue and expenditure estimates incorporated in the 2004-05 budget, state appropriations were $13.7 billion below the limit in 2003-04 and are expected to be $10.6 billion below the limit in 2004-05.

In addition to the 2004-05 Budget Act, the budget package includes a

number of related measures enacted to implement and carry out the

budget's provisions. Figure 7 lists these bills.

|

Figure 7 2004-05 Budget-Related

Legislation |

|||

|

Bill Number |

Chapter |

Author |

Subject |

|

SB 1096 |

211 |

Budget Committee |

Local government�vehicle license fee |

|

SB 1097 |

225 |

Budget Committee |

Technology, Trade, and Commerce technical

corrections |

|

SB 1098 |

212 |

Budget Committee |

Transportation financing |

|

SB 1099 |

210 |

Budget Committee |

Transportation�Proposition 42 suspension |

|

SB 1100 |

226 |

Budget Committee |

Taxation |

|

SB 1101 |

213 |

Budget Committee |

Education finance�Proposition 98 suspension |

|

SB 1102 |

227 |

Budget Committee |

General government |

|

SB 1103 |

228 |

Budget Committee |

Health |

|

SB 1104 |

229 |

Budget Committee |

Social services |

|

SB 1105 |

214 |

Budget Committee |

Public employee retirement |

|

SB 1106 |

215 |

Budget Committee |

Pension obligation bonds |

|

SB 1107 |

230 |

Budget Committee |

Resources |

|

SB 1108 |

216 |

Budget Committee |

Education finance |

|

SB 1110 |

217 |

Budget Committee |

State employees: state bargaining unit 6 |

|

SB 1111 |

218 |

Budget Committee |

Veterans Affairs |

|

SB 1112 |

219 |

Budget Committee |

State fire protection fee repeal |

|

SB 1119 |

209 |

Budget Committee |

Ballot measures |

|

SB 1120 |

220 |

Budget Committee |

Deficiency bill: 2003-04 budget |

|

SB 1448 |

233 |

Alpert |

Pupil assessment |

|

SB 1809 |

221 |

Dunn |

Labor Code revisions |

|

AB 1554 |

263 |

Keene |

School finance�emergency apportionments and

lease financing |

|

SCA 4 |

133a |

Torlakson |

Local government constitutional amendment |

|

|

|||

|

a

Resolution chapter number. |

|||

The 2004-05 Budget Act resulted in a number of tax-related changes, although no broad-based tax increases were enacted. The increased revenues from these changes include $333 million from a broad tax amnesty, $210 million from the suspension of the teachers' tax credit, and $26 million from a change in the application of the use tax on certain out-of-state purchases. Another major factor that affects the state's revenue position for 2004-05 is the reinstatement of net operating loss (NOL) carryover deductions.

The adopted budget enacts a tax amnesty program that applies to major General Fund taxes—the personal income tax, corporation tax, and sales and use tax. The amnesty program will occur during the period February 1, 2005 through March 31, 2005, and apply to tax years prior to 2003. The program would allow those taxpayers with unreported or underreported tax liabilities to avoid penalties and fees on overdue amounts if they pay such taxes in full or enter into an installment agreement for the payment of them. The amnesty also prevents the Franchise Tax Board (FTB) and the Board of Equalization (BOE) from taking criminal action against program participants. Following the conclusion of the program, penalties for various types of taxpayer noncompliance will be increased. As shown in Figure 1, the amnesty program is expected to result in $333 million of additional revenues. (This will be recognized as an increase in the beginning 2003-04 General Fund balance.)

|

Figure 1 2004-05 Budget |

|

|

(In Millions) |

|

|

|

General

Fund Revenue Gain |

|

Tax Amnesty |

|

|

Personal income tax |

$195 |

|

Corporation tax |

65 |

|

Sales and use tax |

73 |

|

Subtotal |

($333) |

|

Tax Expenditure Programs |

|

|

Teachers� tax credit suspension |

$210 |

|

Modified use tax application |

26 |

|

Natural Heritage Tax Credit suspension |

11 |

|

Subtotal |

($247) |

|

Total |

$580 |

Teachers' Tax Credit Suspended

Under the budget agreement, the teachers' tax credit will be suspended for tax years 2004 and 2005. The teachers' tax credit was established as part of the 2000-01 budget and provides to credentialed teachers in public and private K-12 schools a credit against their income taxes ranging from $250 (for those with at least four years but fewer than six years of experience) to $1,500 (for those with 20 or more years of experience). The teachers' tax credit was also suspended for the 2002 tax year. The two-year suspension is estimated to result in additional revenues of $210 million in 2004-05 and $180 million in 2005-06.

Use Tax on Out-of-State Purchases Modified

The budget agreement also changes the application of the use tax on

certain out-of-state purchases. Generally, out-of-state purchases made by

a California resident and intended for use in California are subject to a

use tax (equivalent to the sales tax). However, some major items—such

as vessels, vehicles, and aircraft—purchased out of state and kept there

for a certain minimum period of time are not considered to be "intended

for use in California," and thus are not subject to the use tax. Budget

language extends from the current 90 days to 12 months the period that

such purchases would need to remain out of state in order to qualify for

this use tax exemption. This statutory change would be effective for two

years. The estimated General Fund revenue gain from this is $26 million in

2004-05 (partial-year effect) and $35 million in 2005-06.

Natural Heritage Tax Credit Suspended

The Natural Heritage Tax Credit is a program available to income

taxpayers and is equal to 55 percent of the market value of certain

qualified

property approved by the Wildlife Conservation Board that is

contributed to the state, a local government, or a nonprofit organization

approved by a local government. The 2004-05 budget calls for the

suspension of this credit through June 2005 for a 2004-05 revenue gain of

$11 million.

As shown in Figure 1, the 2004-05 revenue gain from the above changes is $580 million.

In addition to the amnesty program, the Legislature also adopted some additional administrative measures. Specifically:

The use of NOL carryover deductions was suspended for tax years 2002 and 2003 as a component of the 2002-03 budget. This deduction will be reinstated and will be available for tax years beginning in 2004. In addition, as part of that year's budget, the NOL carryover percentage, which was formerly 65 percent, has been increased to 100 percent (also effective for the 2004 tax year). The reinstatement of this tax program will result in decreased General Fund revenues in the mid hundreds of millions of dollars.

The budget package includes $47 billion in Proposition 98 spending in

2004-05 for K-14 education. This represents an increase of $788 million, or

1.7 percent, from the revised 2003-04 spending level. Figure 1 summarizes

the budget package for K-12 schools, community colleges, and other

affected agencies. Because of upward revisions in the Proposition 98 minimum

funding guarantee in 2003-04, however, this change does not reflect the

actual increase in new resources available to K-14 in 2004-05. Thus, the

package reflects an increase of $1.3 billion or 2.8 percent from the

2003-04 Budget Act appropriation level. The budget package also includes an

additional $765 million in one-time Proposition 98 funds, including $439 million

in 2003-04 settle-up funds and $326 million of prior-year funds from

the Proposition 98 Reversion Account.

|

Figure 1 Proposition 98 Budget

Summary |

|||

|

2003‑04 and 2004‑05 |

|||

|

|

2003-04

Budget Package |

|

|

|

As

Enacted |

Revised |

2004-05 |

|

|

K-12 Proposition 98 |

|

|

|

|

General Fund |

$27.6 |

$28.0 |

$30.9 |

|

Local property taxes |

13.6 |

13.7 |

11.2a |

|

Subtotals,

K-12 |

($41.3) |

($41.7) |

($42.1) |

|

Average Daily Attendance ( |

5,990,495 |

5,950,626 |

6,006,898 |

|

Amount per |

$6,887 |

$7,009 |

$7,007 |

|

California Community Colleges |

|

|

|

|

General Fund |

$2.2 |

$2.3 |

$3.0 |

|

Local property taxes |

2.1 |

2.1 |

1.8a |

|

Subtotals,

Community Colleges |

($4.4) |

($4.4) |

($4.8) |

|

Other Agencies |

$0.1 |

$0.1 |

$0.1 |

|

Totals,

Proposition 98 |

$45.7 |

$46.2 |

$47.0 |

|

General Fund |

$30.0 |

$30.4 |

$34.0 |

|

Local property taxes |

15.7 |

15.8 |

13.0 |

|

|

|||

|

a

Property taxes decline due to changes in the allocation of tax

proceeds among local government agencies. See text for further details. |

|||

The 2004-05 spending level is $2.3 billion below the 2004-05 Proposition 98 minimum guarantee, for two reasons. First, Chapter 213, Statutes of 2004 (SB 1101, Committee on Budget and Fiscal Review), suspends the minimum guarantee for 2004-05 and requires the state to provide $2 billion less than the minimum guarantee. Second, the budget creates a $302 million Proposition 98 General Fund reserve—that is, the appropriation level is $302 million less than required by Proposition 98. The reserve reflects an increase in General Fund revenues compared to the Governor's May Revision estimates.

The 2004-05 budget also reflects significant changes in the funding sources for Proposition 98. General Fund support for Proposition 98 increases $3.6 billion, or almost 12 percent from the revised 2003-04 spending level. This large General Fund increase is caused primarily by an 18 percent ($2.8 billion) decrease in property tax revenues for schools resulting from noneducation budget decisions. Changes to property tax collections for K-14 education include:

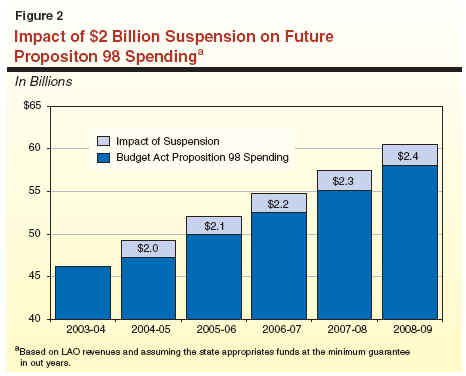

Long-Run Impact of the Budget Package on K-14 Spending. The budget package contains two provisions that will affect future Proposition 98 spending levels. Most importantly, the lower appropriations levels that result from suspending the Proposition 98 guarantee in 2004-05 likely will yield savings to the state in future budgets. Figure 2 shows our estimate of the annual savings to the state from the budget's Proposition 98 suspension (see shaded box). The figure shows that the $2 billion of savings in 2004-05 grows to $2.4 billion by 2008-09. This growth occurs because savings from the 2004-05 suspension increases at the same rate as the annual growth in the minimum guarantee. Annual savings from the suspension will continue until the Proposition 98 maintenance factor is fully paid off.

In addition to the multiyear savings from the Proposition 98

suspension, the budget package delays payment of $969 million in Proposition 98

settle-up obligation for 2002-03 and 2003-04. The delay effectively

transforms

this obligation into a loan from Proposition 98 to the General Fund.

A repayment plan for this loan also is part of the budget package.

Chapter 216, Statutes of 2004 (SB 1108, Committee on Budget and Fiscal

Review), requires the State Department of Education and the

Department of Finance to jointly determine by January 1, 2006, the amount

owed under the Proposition 98 minimum guarantee for fiscal years

1995-96 through 2003-04. Chapter 216 also appropriates $150 million from

the General Fund beginning in 2006-07 and continuing each year until

these prior-year obligations are satisfied. The annual appropriation will be

distributed based on enrollment (for K-12) or full-time equivalent

students (FTE) (for community colleges). Depending on the amount owed by

the state for these years, settle-up payments could continue through 2014-15.

Starting in 2001-02, the Legislature opted to defer significant

education program costs to the subsequent fiscal year rather than make

additional spending cuts. Figure 3 shows that the budget continues to defer

almost $3.5 billion in K-14 costs to the future. As discussed later, the budget

provides an additional $270 million to reduce the revenue limit deficit

factor. In addition, the budget uses $58 million in one-time 2003-04 settle-up

funds to pay outstanding education mandate costs. However, since the

budget does not fund the ongoing costs of education mandates (estimated to

be

about $250 million annually), cumulative deferrals remain at about

$3.5 billion in 2004-05.

|

Figure 3 Update on the K-14

Education Credit Card Balance |

||||

|

2001‑02 Through 2004‑05 |

||||

|

|

2001‑02 |

2002‑03 |

2003‑04 |

2004‑05 |

|

One-Time Costs |

|

|

|

|

|

Revenue limit and categorical deferrals |

$931 |

$2,158 |

$1,097 |

$1,083 |

|

Community college deferral |

116 |

� |

200 |

200 |

|

Cumulative mandate deferrals |

656 |

958 |

1,266 |

1,524 |

|

Ongoing Costs |

|

|

|

|

|

Revenue limit deficit factor |

� |

� |

$883 |

$643 |

|

Totals |

$1,703 |

$3,116 |

$3,446 |

$3,450 |

As shown in Figure 1, spending on 2004-05 K-12 Proposition 98 totals $42.1 billion, an increase of about $400 million (1 percent) from the revised 2003-04 spending level. As discussed above, however, because of upward revisions in the 2003-04 minimum guarantee, this comparison understates the actual increase in resources K-12 schools will receive in 2004-05. Comparing 2004-05 spending to the level included in the 2003-04 Budget Act shows K-12 spending increasing by $833 million (2 percent).

Growth in Proposition 98 spending also is distorted because numerous expenses have been deferred from one fiscal year to another from 2001-02 through 2004-05. These deferrals—which pay districts for program services that were provided in the previous year—make cross-year comparisons difficult. Figure 4 displays the impact of deferrals on per-pupil spending by moving deferred funds into the year in which the district expenditures occur. We refer to this deferral-adjusted funding level as "programmatic" funding because it provides a clearer picture of the actual level of funding and services available to schools and districts each year. Using this calculation, per-pupil spending increased by 2.5 percent ($173 per pupil) over the 2003-04 revised funding level. In contrast, funding actually declined by less than 1 percent ($2 per pupil) between 2003-04 and 2004-05.

|

Figure 4 K-12 Proposition 98

Spending Per Pupil |

||||

|

2001‑02 Through 2004‑05 |

||||

|

|

Actual |

Actual

2002‑03 |

Revised

2003‑04 |

Proposed

2004‑05 |

|

Budgeted Funding |

|

|

|

|

|

Dollar per ADAa |

$6,608 |

$6,597 |

$7,009 |

$7,007 |

|

Percent growth |

� |

-0.2% |

6.2% |

� |

|

|

|

|

|

|

|

Programmatic Fundingb |

|

|

|

|

|

Dollar per |

$6,788 |

$6,805 |

$6,831 |

$7,004 |

|

Percent growth |

� |

0.3% |

0.4% |

2.5% |

|

|

||||

|

a

Average Daily Attendance. |

||||

|

b

To adjust for the deferrals, we counted funds toward the fiscal

year in which school districts had |

||||

Figure 5 displays major K-12 funding changes from the 2003-04 Budget Act. The budget package provides about $2.3 billion in new K-12 expenditures. Funds for these proposals come from three main sources:

The budget uses the $2.3 billion in available funds to provide growth, COLAs, and other funding increases. Major spending changes include:

In addition to the increase in state funds, the budget includes major increases in federal funds. Specifically, the federal funding for special education increases by $140 million (most of which is used to provide for special education growth and COLA). Title I funding increases by $120 million (most of which was passed through to districts). In addition, the budget sets-aside $67 million in federal support for low-performing school districts pending legislation creating a school district accountability system.

|

Figure 5 Major Adjustments to K-12

Proposition 98 Funding |

|

|

Changes From the 2003‑04 Budget Act |

|

|

Program |

Amount |

|

Growth |

$508.5 |

|

Cost-of-living adjustments |

979.9 |

|

Deficit factor |

270.0 |

|

Instructional materials |

188.0 |

|

Deferred maintenance |

173.0 |

|

Unemployment insurance |

120.1 |

|

Equalization |

109.9 |

|

Net reduction of deferral costsa

|

-1,048.3 |

|

Reversion Account funds used for ongoing programb |

-218.1 |

|

Special education federal fund offset |

-126.6 |

|

Other changes |

-123.4 |

|

Total Changes |

$833.0 |

|

|

|

|

a

In 2003‑04, the state used over $1 billion to pay off

categorical and revenue limit deferrals. These costs were one-time in

nature, and the funds can be used for ongoing purposes beginning in

2004‑05. The budget takes advantage of these freed-up one-time funds to

support other K-14 priorities. |

|

|

b

The state used $119.5 million of Proposition 98

reversion account funds to cover ongoing child care costs and $98.6 million

for the Targeted Instructional Improvement Grants. |

|

The education trailer bills and related legislation made the following major changes:

The 2004-05 budget provides a total of $8.9 billion in General Fund support for higher education. As shown in Figure 6, this is $361 million, or 4.2 percent, more than the amount provided in 2003-04. This net change results from the combined effect of a $769 million increase in General Fund support for the California Community Colleges (CCC) and a $408 million reduction for the University of California (UC), the California State University (CSU), Hastings College of the Law, and the California Student Aid Commission (CSAC).

|

Figure 6 General Fund

Appropriations for Higher Education |

||||

|

(Dollars in Millions) |

||||

|

|

|

|

Change |

|

|

2003‑04 |

2004‑05 |

Amount |

Percent |

|

|

|

$2,907.8 |

$2,721.0 |

-$186.8 |

-6.4% |

|

|

2,630.1 |

2,448.0 |

-182.1 |

-6.9 |

|

California Community Colleges |

2,281.2 |

3,050.2 |

769.0 |

33.7 |

|

Student Aid Commission |

672.8 |

636.8 |

-36.0 |

-5.4 |

|

|

2.0 |

2.0 |

� |

� |

|

|

11.1 |

8.1 |

-3.0 |

-26.7 |

|

Totals |

$8,505.0 |

$8,866.1 |

$361.1 |

4.2% |

Although the Legislature approved some of the Governor's proposals for reductions at UC and CSU, it also significantly modified a few of them (as described below). Further, although the May Revision referenced "compacts" whereby the Governor has committed to include various funding increases for the segments in future budget proposals (beginning in 2005-06), these commitments are not binding on the Legislature, and the 2004-05 budget makes no reference to them.

Student Fees. All three public higher education segments increased student fees for 2004-05. Figure 7 shows the change in student fees from 2003-04 to 2004-05. As the figure shows, UC and CSU increased resident undergraduate fees by 14 percent and CCC's resident fees increased by $8 per unit, or 44 percent. Graduate fee increases ranged from 20 percent for UC academic graduate students and CSU teacher education students to 37 percent for UC optometry and pharmacy students. (Nursing students at UC did not experience any systemwide fee increase.) The UC and CSU also increased nonresident tuition by about 20 percent. These higher fees will generate $358 million in additional revenue to backfill a General Fund reduction of the same amount. (About $15 million of this amount was in jeopardy at the time this report was being prepared, due to a superior court injunction preventing UC from imposing the fee increase on continuing professional school students.) Despite the Governor's proposal to enact a long-term fee policy, no such policy was adopted as part of this budget package. However, the Legislature subsequently passed a bill (AB 2710, Liu) directing UC and CSU to develop policies that would result in more predictable and moderate changes in student fees.

|

Figure 7 Student Fees |

||||

|

(Systemwide Tuition and Fees for Full-Time Students) |

||||

|

|

|

|

Change

From 2003‑04 |

|

|

2003‑04 |

2004‑05 |

Amount |

Percent |

|

|

|

|

|

|

|

|

Resident Fees |

|

|

|

|

|

Undergraduate

students |

$4,984 |

$5,684 |

$700 |

14% |

|

Graduate

students |

5,219 |

6,269 |

1,050 |

20 |

|

Professional

school studentsa |

|

|

|

|

|

Optometry |

$10,339 |

$14,139 |

$3,800 |

37% |

|

Pharmacy |

10,339 |

14,139 |

3,800 |

37 |

|

Dentistry |

13,524 |

18,024 |

4,500 |

33 |

|

Veterinary medicine |

12,029 |

16,029 |

4,000 |

33 |

|

Medicine |

14,013 |

18,513 |

4,500 |

32 |

|

Business administration |

14,824 |

19,324 |

4,500 |

30 |

|

Theater, film, and television |

8,649 |

11,249 |

2,600 |

30 |

|

Law |

15,313 |

19,113 |

3,800 |

25 |

|

Nursing |

8,389 |

8,389 |

� |

� |

|

Nonresident

Tuition and Fees |

|

|

|

|

|

Undergraduate

students |

$19,194 |

$22,640 |

$3,446 |

18% |

|

Graduate

students |

17,709 |

21,208 |

3,499 |

20 |

|

|

|

|

|

|

|

Resident Fees |

|

|

|

|

|

Undergraduate

students |

$2,046 |

$2,334 |

$288 |

14% |

|

Teacher

education students |

2,256 |

2,706 |

450 |

20 |

|

Graduate

students |

2,256 |

2,820 |

564 |

25 |

|

Nonresident

Tuition and Fees |

|

|

|

|

|

Undergraduate

students |

$10,506 |

$12,504 |

$1,998 |

19% |

|

Graduate

students |

10,716 |

12,990 |

2,274 |

21 |

|

California Community Colleges |

$540b |

$780c |

$240 |

44% |

|

|

||||

|

a

A preliminary injunction in August 2004 prevented UC at least

temporarily from imposing the |

||||

|

b

Reflects per unit fee of $18. |

||||

|

c

Reflects per unit fee of $26. |

||||

In addition, the budget assumes UC and CSU will begin to phase in surcharges on students who take "excess" units (those beyond 110 percent of the units required for a baccalaureate degree). These surcharges are supposed to eventually result in students being charged the full cost of instruction for excess units. For 2004-05, UC and CSU are expected to receive an additional $25 million in student fee revenue as a result of this new surcharge.

Allocated Reductions. The budget achieves $244 million in General Fund savings—$107.9 million at UC and $136.3 million at CSU—by reducing funding for research and academic support, increasing student-faculty ratios, and imposing other allocated reductions. The allocated reductions include those associated with the excess unit surcharge.

Enrollment. In adopting the 2004-05 budget, the Legislature rejected the Governor's proposal to redirect 7,000 eligible freshmen from UC and CSU to the community colleges. While it did not restore the associated $24.8 million reduction to UC's enrollment funding, the budget package anticipates that UC will accommodate all eligible students with existing funds. For CSU, the budget fully restores the Governor's associated reduction of $21.1 million, and further augments General Fund support by $12.2 million to fund an additional 2,155 FTE students. However, as explained in the shaded box, CSU will actually serve about 11,000 fewer students in 2004-05 than the previous year.

K-14 Outreach Programs. The budget maintains funding for UC and CSU's outreach programs at their 2003-04 levels. For UC, the budget provides the full $29.3 million in General Fund support. For CSU, the budget provides $7 million in General Fund support and assumes CSU will redirect funding from other programs to add another $45 million in outreach funding, thus matching total outreach funding at its 2003-04 level of $52 million. As discussed in the accompanying box, CSU plans to shift funds away from enrollment to support its outreach programs.

General Fund support for CCC increases by $769 million (or 34 percent) from 2003-04 to 2004-05. However, this overstates the increase in CCC's overall financial resources because some of the increase simply offsets reductions in local property tax revenue and some is earmarked to pay for costs incurred in 2003-04. Adjusting for these factors, and including new revenue from a student fee increase, reveals a year-to-year increase in available resources of $288 million, or 5.9 percent. Major augmentations are identified below.

Proposition 98 Funding. General Fund support and local property tax revenues used by local community college districts are counted as Proposition 98 appropriations. The CCC's total Proposition 98 funding increases by $412 million, or 9.4 percent. The 2004-05 budget provides CCC with 10.2 percent of total Proposition 98 appropriations.

Deferrals. The 2004-05 budget continues to defer $200 million in Proposition 98 spending into the next fiscal year. Because the 2004-05 budget also includes $200 million for spending that was deferred from the 2003-04 fiscal year, these two amounts cancel each other out and thus do not affect the overall appropriation level for 2004-05.

Major Augmentations. The Legislature approved major augmentations proposed by the Governor, including $80 million for progress in equalizing the per-student funding among CCC districts, $106 million for a 2.41 percent COLA for apportionments and some categorical programs, and $134 million for a statewide enrollment increase of 3 percent (about 33,300 FTE students). In addition, the Legislature added $27 million in enrollment funding to pay for some of the existing, unfunded enrollment at districts that have exceeded their enrollment caps.

The budget includes $808 million for CSAC. Of this amount, $759 million is for the Cal Grant programs. This is $104 million, or 16 percent, more than Cal Grant expenditures in 2003-04. Of total Cal Grant funding, $602 million is General Fund, $147 million is Student Loan Operating Fund (SLOF) monies, and $10 million is federal funds. As part of a short-term budget solution, SLOF monies are being used for the first time to support Cal Grant costs. Because of this shift of some costs to the SLOF, General Fund support actually declines from 2003-04 to 2004-05 by $42 million, or 7 percent.

The Cal Grant budget includes funding for 66,000 new high school entitlement awards, 3,000 new transfer entitlement awards, and, as specified in law, 22,500 new competitive awards. It also increases the Cal Grant award for UC and CSU students by 14 percent, sufficient to fully offset the undergraduate fee increase. The budget decreases the Cal Grant award for students attending private colleges and universities by 14 percent, from $9,708 to $8,322. In addition, the budget raises the Cal Grant income ceilings by the percent change in per capita personal income from 2003.

The 2004-05 budget package makes major changes to local government revenues and proposes a constitutional amendment to greatly restrict future state authority over local finance. Specifically, the package:

|

Proposition 65

and Proposition 1A |

|

Proposition 65

and Proposition 1A both amend the State Constitution to achieve

three similar objectives regarding state and local government finance.

Proposition 65 was sponsored by statewide local government

associations and qualified for the ballot through the initiative

process. Proposition 1A was placed on the ballot by the Legislature

(SCA 4, Torlakson). |

|

Both Measures Significantly Limit State Authority |

|

Effect

on |

|

�Proposition 65�s

restrictions apply retroactively, and thus would prevent a major part of

the 2004‑05 budget plan from taking effect (the two-year, $1.3 billion

annual property tax shift). This property tax shift could occur in the

future, if approved by the state�s voters. |

|

�Proposition 1A�s

restrictions apply to future state actions only, and would allow the

planned $1.3 billion property tax shift to occur. |

|

Effect

on |

|

�Proposition 65

allows the state, upon approval of the state�s voters, to modify major |

|

�Proposition 1A

prohibits such state changes, except for limited, short-term shifting of |

|

Both Measures Greatly Reduce State Authority to

Reallocate Tax Revenues |

|

Effect

on Revenue Allocation |

|

�Proposition 65

requires state voter approval before the state can reduce any individual

local government�s revenues from the property tax, uniform local sales

tax, or vehicle |

|

�Proposition 1A

prohibits the state from reducing any local government�s revenues from

the uniform local sales tax or optional sales tax, but maintains some

state authority to alter the allocation of property tax revenues, VLF

revenues, and other taxes with the consent of the local government.

Proposition 1A does not include a voter approval requirement. |

|

Types

of Local Governments Affected |

|

�Proposition 65�s

restrictions apply to cities, counties, special districts, and

redevelopment agencies. |

|

�Proposition 1A�s

restrictions do not apply to redevelopment agencies. |

|

Both Measures Restrict State Authority to Impose Mandates |

|

�Proposition 65

authorizes individual local governments, schools, and community college

districts to decide whether or not to comply with a state requirement if

the state does not fully reimburse local costs. |

|

�Proposition 1A

provisions do not include schools and community colleges. If the state

does not fund a mandate, the state must pass a law temporarily

eliminating every local government�s obligation to implement it. |

|

|

|

Figure 8 Major Provisions of the

Property Tax Shift |

|

|

|

The

budget package shifts $1.3 billion of property taxes from cities,

counties, special districts, and redevelopment agencies to K-14

districts in 2004‑05 and again in 2005‑06. This tax shift

reduces state General Fund education spending obligations by a

commensurate amount. Local shift amounts are as follows: |

|

Cities�$350 Million.

Each city�s shift is based on a statutory formula. In general,

the formula sets each city�s shift at an amount equal to at least 2 percent,

but not more than 4 percent, of city general purpose revenues. |

|

Counties�$350 Million.

Each county�s shift is specified in statute. In general, each

county�s shift reflects its proportionate share of 2003‑04

county vehicle license fee allocations. |

|

Special

Districts�$350 Million. Each special district�s shift

will be determined pursuant to a statutory formula. |

|

�

Nonenterprise

Districts. Fire, police, hospital, library, veterans�

memorial, and mosquito/vector control districts are exempt from the

shift. Other nonenterprise special districts contribute 10 percent

of their property tax revenues, or about $60 million. |

|

�

Enterprise

Districts. The shift from transit and certain public utility

enterprise districts is limited to 3 percent and 10 percent,

respectively, of their property tax revenues. All other enterprise

special districts contribute property taxes so that the total shift from

special districts reaches $350 million. No shift from an enterprise

district may exceed 10 percent of its total revenues. |

|

Redevelopment

Agencies�$250 Million. Similar to the 2003‑04

redevelopment property tax shift, the 2004‑05 budget plan: |

|

�

Requires each agency to make a payment to its |

|

�

Allows agencies to extend the life of their plans by up to

two years. |

|

The

amount of each agency�s payment reflects both its proportionate share

of: (1) gross tax increment and (2) net tax increment (which

accounts for amounts passed-through to other local agencies). If an

agency has insufficient funds to make its payment, it may borrow up to

half of the amount from its Low and Moderate Income Housing Fund or

request its host city or county to make the payment. If a redevelopment

agency (or its host city or county) fails to make the required property

tax contribution, the county auditor will transfer property taxes from

the host city or county to cover the payment. |

The 2004-05 Budget Act provides about $16.3 billion from the General Fund for health services programs, about a $2.3 billion or 16.5 percent increase compared to the revised prior-year level of spending as shown in Figure 9. This increase is primarily the result of one-time adjustments in the Medi-Cal Program that we discuss below. Several significant aspects of the budget package are summarized in Figure 10 and discussed below.

|

Figure 9 Health Services Programs |

||||

|

(Dollars in Millions) |

||||

|

|

|

|

Change |

|

|

2003-04 |

2004-05 |

Amount |

Percent |

|

|

Medi-Cal (local assistance only) |

$9,947 |

$11,916 |

$1,969 |

19.8% |

|

Department of Developmental Services |

1,975 |

2,231 |

256 |

13.0 |

|

Department of Mental Health |

895 |

943 |

48 |

5.4 |

|

Healthy Families Program (local assistance only) |

291 |

319 |

28 |

9.7 |

|

Department of Alcohol and Drug Programs |

233 |

237 |

4 |

1.7 |

|

All other health services |

671 |

674 |

3 |

0.4 |

|

Totals |

$14,012 |

$16,320 |

$2,308 |

16.5% |

Various Rate Changes. The budget plan adopts an administration proposal to achieve savings of $31 million by reducing by 10 percent the interim amount initially paid to certain hospitals that serve Medi-Cal patients. The budget also includes a modified version of an administration proposal that would achieve net state savings of $52 million through a reduction in Medi-Cal pharmacy reimbursements.

The budget provides that certain managed care plans, known as county organized health systems, would receive a 3 percent rate increase to improve their financial stability at a state cost of about $15 million.

The spending plan rejects an administration proposal to save

$28 million by modifying the reimbursement rates for certain clinics that serve

Medi-Cal patients.

Ten Percent Rate Reduction

Withdrawn. The budget plan does not include a proposed 10 percent rate cut in provider reimbursement rates

for Medi-Cal and various public health programs that would have been

in addition to the 5 percent reduction enacted as part of last year's budget

act. The administration withdrew the proposal, which was intended to save

the state about $620 million in 2003-04 and 2004-05, at the May Revision.

Prior Rate Reductions. No longer assumes a 5 percent reduction in the rates paid to certain Medi-Cal providers had been enacted as part of the 2003-04 budget. However, the spending plan no longer assumes about $248 million in savings in 2003-04 and 2004-05 from rate reductions that have been blocked by still-pending litigation. In addition, the spending plan reverses the 5 percent reduction ($4.2 million) that was largely unaffected by the court case for the California Children's Services, the Genetically Handicapped Persons Program, the Child Health and Disability Prevention Program, the Breast and Cervical Cancer Early Detection Program, and the Multipurpose Senior Services Program.

|

Figure 10 Major Changes in General

Fund Spending |

|

|

2004-05 (Dollars in Millions) |

|

|

|

|

|

Medi-Cal |

|

|

Backfill one-time accounting and federal

cost-share savings |

$1,613 |

|

Assume no savings from 2003‑04 5 percent

provider rate reduction |

248 |

|

Increase county organized health system rates by

percent |

15 |

|

Delay checkwrites to providers |

-288 |

|

Reduce pharmaceutical reimbursements |

-52 |

|

Rescind adjustments for nursing home wages |

-46 |

|

Adjust caseload

for reconciliation of |

-33 |

|

Reduce interim rates paid to certain hospitals by

10 percent |

-31 |

|

Control costs for county administration of Medi-Cal

eligibility |

-10 |

|

Impose quality improvement fee for managed care

plans |

-9 |

|

Expand auditing of hospitals |

-3 |

|

Department of Developmental Services |

|

|

Augment community programs to facilitate closure

of Agnews |

$11 |

|

Recognize federal funds from recertification of

regional center |

-30 |

|

Make unallocated reduction in regional center

services and operations |

-18 |

|

Department of Mental Health (DMH) |

|

|

Adjust for EPSDTa

spending growth (DMH reimbursements) |

$135 |

|

Reduce Children's System of Care local assistance |

-20 |

|

Delay and reduce beds activated at |

-10 |

|

Public Health |

|

|

Reverse 5 percent provider rate reduction for

various programs |

$4 |

|

Suspend state contribution to CMSPb |

-20 |

|

|

|

|

a

Early and Periodic Screening, Diagnosis and Treatment Program. |

|

|

b

|

|

The budget act provides about $11.9 billion from the General Fund ($33 billion all funds) for local assistance provided under the Medi-Cal Program. This amounts to almost a $2 billion or 20 percent increase in General Fund support for Medi-Cal local assistance discussed in more detail below.

One-Time Adjustments. A General Fund backfill of two major one-time technical funding changes accounted for about $1.6 billion of the increase in spending. These are: (1) the inclusion in 2003-04 of a program accounting change ("accrual to cash") that reduced program costs on a one-time basis, and (2) the expiration in the budget year of a temporary increase in federal support for the program that required an increase in state support for Medi-Cal local assistance. Absent these technical changes, the year-over-year increase in Medi-Cal spending would be about $350 million, or 3.5 percent, in the spending plan signed by the Governor.

Checkwrite Delays. The single largest Medi-Cal savings in the spending plan are one-time savings due to delaying checkwrites by two weeks for reimbursements to providers. This means some payments to providers that would otherwise have occurred in 2004-05 will actually occur in 2005-06. This results in savings of about $288 million in 2004-05.

Medi-Cal Reform. The budget plan does not include staffing and funding sought by the administration to develop a federal waiver that would allow the Medi-Cal Program to be structured to achieve as much as $400 million a year in future state savings. The Legislature determined that any such resources should be provided as part of subsequent policy legislation (now anticipated to be introduced in January 2005) for this purpose.

Quality Improvement Fee. The Legislature approved with

modifications an administration proposal to levy a quality improvement fee on

certain managed care health plans. The fee, which would take effect in January

2005 subject to federal approval, would result in a net savings to the state

General

Fund of $9 million in 2004-05 that would grow to $53 million in 2005-06.

Antifraud and Other Activities. The budget plan adopts a series of proposals to combat fraud and overspending in the Medi-Cal Program, including the addition of 20 new auditor positions to examine the claims of hospitals serving Medi-Cal beneficiaries. The state savings from the additional audits are projected to be $3.1 million in 2004-05 and $8.8 million in 2005-06. A proposed change in state law to prevent middle-income persons from disposing of their assets to become eligible for Medi-Cal was not adopted as part of the budget.

Wage Adjustment Rate Program. The budget rescinds the Wage Adjustment Rate Program (WARP) that had been established (but never implemented) to use state funds to augment the wages of personnel working in nursing facilities. The General Fund savings in 2003-04 from rescinding WARP were $46 million. These savings will continue through 2004-05 and beyond.

Caseload Adjustment. The budget plan assumes that the state will achieve more than $33 million in savings in the budget year from a reduction in the Medi-Cal caseload that will result from a comparison of Medi-Cal eligibility records kept by the state and Los Angeles County. The Medi-Cal caseload is expected to decline by a monthly average of 58,000 persons as a result of this reconciliation of eligibility files.

County Administration of Eligibility. The budget reduces county allocations for administration of Medi-Cal eligibility by counties by $10 million in General Fund support to reflect cost-control efforts that are to be initiated in 2004-05.

The budget provides about $319 million from the General Fund

($872 million all funds) for local assistance under the Healthy Families

Program during 2004-05. This reflects a General Fund increase of about

$28 million or 9.7 percent for the program. Part of the growth in spending is due to

the projected continued increases in program caseload to about 774,000

children by June 2005. As noted, proposals to cap program enrollment and

to shift part of the program into a county block grant were not

adopted. The Legislature also rejected administration proposals for staff

resources and contract funding to restructure the program into two tiers that

would vary in their benefits and level of family premiums. However, the

budget plan increases premiums for higher-income families whose children

are participating in the program starting in 2005-06 to achieve annual

state

savings of about $5.4 million.

The administration withdrew—following legislative action to reject the proposals—two proposals offered in January to achieve savings of about $66 million in certain health programs (as well as social services programs) through the imposition of enrollment limits and the establishment of a county block grant. The block grant proposal would have affected the Healthy Families Program. The enrollment cap would have affected Healthy Families as well as the Medi-Cal Program, state hospitals, the AIDS Drug Assistance Program, California Children's Services, the Genetically Handicapped Persons Program, and the Breast and Cervical Cancer Treatment Program.

The budget provides more than $2.2 billion from the General Fund ($3.5 billion all funds) for services to individuals with developmental disabilities in developmental centers and regional centers. This amounts to an increase of about $256 million, or 13 percent, in General Fund support over the revised prior-year level of spending.

Community Programs. The 2004-05 budget includes a total of $1.8 billion from the General Fund ($2.8 billion all funds) for community services for the developmentally disabled, an increase in General Fund resources of about $236 million over the prior fiscal year. In enacting this budget plan, the Legislature rejected an administration proposal to save about $12 million by establishing statewide standards for the purchase of certain services. It strengthened the auditing of regional center vendors and imposed additional unallocated reductions of more than $18 million to regional center operations and services. The budget implements copayments for families of developmentally disabled children with incomes above 400 percent of the federal poverty level ($73,600 for a family of four). Finally, the budget recognizes about $30 million in additional federal funds, that will be used to offset General Fund costs, from the recertification of the South Central Los Angeles Regional Center for the Home and Community-Based Waiver program.

Developmental Centers. The budget provides about $390 million from

the General Fund for operations of the developmental centers and related

activities (about $715 million all funds). This

represents about a $19 million increase above the revised level of General Fund support provided to

the centers in 2003-04. Part of the spending increase is due to an

$11 million augmentation to assist in the closure of Agnews Developmental

Center.

Specifically, the Legislature rejected a proposal to make improvements

at Sonoma Developmental Center to accommodate residents moved out

of Agnews and instead redirected the funds to expand community

programs for the same purpose.

The budget provides about $943 million from the General Fund ($2.6 billion all funds) for mental health services provided in state hospitals and in various community programs by the Department of Mental Health. This amounts to about a $48 million, or 5.4 percent, increase in General Fund support overall over the 2003-04 level of spending.