The state�s strong revenue performance-a $7.5�billion increase since January-presents an extraordinary opportunity for the Legislature. Key decisions are: (1) how much of the increase should be provided to K-14 education, (2) should increased school funding be allocated to new initiatives or to strengthen existing programs and pay off debts, and (3) which state debt should be prepaid?

We urge the Legislature to focus on regaining the state�s fiscal balance, particularly in light of the risks and uncertainties facing the state.

In the May Revision, the administration proposes to allocate nearly 40�percent of a $7.5�billion increase in revenues to K-14 schools, with the balance for the prepayment of budget debt; the build up of the reserve; and a combination one-time and ongoing augmentations to health, resources, corrections, and local governments. The budget also includes a proposed settlement to a lawsuit involving school funding resulting in added annual out-year obligations averaging over $400�million for seven years.

Our Bottom Line. The updated proposal has a number of positive features, including its reliance on cautious revenue assumptions and its emphasis on debt prepayments, one-time spending, and the build up of the reserve. Even with these positive features, however, the state will continue to face structural budget shortfalls in the subsequent years, at a time in which it will be facing a number of risks and budgetary pressures. For this reason, it will be important for the Legislature to consider the trade-offs involved in sharply rising ongoing commitments in education. Also, while we strongly support the administration�s emphasis on budgetary debt prepayment, more of an emphasis should be placed on debt prepayments and reserve build up that provide benefits to the General Fund in the next couple of years-when the projected shortfalls are the largest-rather than several years down the road.

In January, the Governor proposed a budget that provided significant new funds for K-12 and higher education, targeted increases in the judiciary and criminal justice programs, and more-or-less baseline increases in other state programs.

Based on much stronger-than-expected collections of personal income taxes in April, the May Revision projects an additional $7.5�billion in revenues in 2005-06 and 2006-07 combined. As shown in Figure�1, the May Revision allocates about $4.3�billion of these increased funds for additional program spending, $1.6�billion for the prepayment of budgetary debt, and $1.6�billion to increase the 2006-07 year-end reserve.

|

Figure 1 How May Revision

Allocates $7.5 Billion in |

|

|

(In Billions) |

|

|

|

|

|

New Resources |

|

|

Revenue increase relative to January: |

|

|

2005‑06 |

$4.8 |

|

2006‑07 |

2.7 |

|

Total, New Resources |

$7.5 |

|

New Uses |

|

|

Spending on Current Programs |

|

|

Proposition 98 |

$2.9 |

|

Health care: disaster preparedness |

0.4 |

|

Other health and social services |

0.1 |

|

Corrections: inmate population and health care |

0.5 |

|

Local government grants and reimbursements |

0.1 |

|

Flood control |

0.5 |

|

Other (net) |

-0.2 |

|

Subtotal |

($4.3) |

|

Prepayment of Budgetary Debt |

|

|

Deficit financing bonds |

$1.0 |

|

Special fund loans |

0.2 |

|

Proposition 98 settle-up payments |

0.2 |

|

Local flood control subventions |

0.1 |

|

Local mandates |

0.1 |

|

Subtotal |

($1.6) |

|

Increased Reserve |

$1.6 |

|

Total, New Uses |

$7.5 |

In terms of program spending increases, about two-thirds of the total is devoted to K-14 Proposition�98 education, where the Governor is proposing increases for a variety of one-time and ongoing purposes. The budget also includes new funds for health care disaster preparedness, additional corrections-related costs, local government grants and reimbursements, and flood control (including $500�million appropriated by AB 142 [Nu�ez], which was part of the infrastructure agreement reached in early May).

In terms of budgetary debt prepayment, the largest item is a $1�billion supplemental payment toward the roughly $10�billion in deficit-financing bonds currently outstanding. The prepayment would enable the state to pay off the bonds about one-half year earlier-by the middle of 2009-10 instead of at the end of that year-assuming that all future supplemental payments from the budget stabilization account were made through 2008-09. Other prepayments are proposed for Proposition�98 settle-up, special fund loans, local mandates, and local flood control subventions. (See accompanying box on page 6 for an update on budgetary borrowing.)

Budgetary Debt and the May RevisionTo help address major budgetary shortfalls in the 2001-02 through 2004-05 period, the state engaged in a substantial amount of budgetary borrowing. In the January budget, the Governor proposed to prepay $1.6�billion of these debts in 2006-07, leaving roughly $20�billion of outstanding budgetary debt at the close of the budget year. This consisted of $15�billion owed to private markets, and about $5�billion to local governments, schools, and special funds (mostly transportation). As the accompanying figure shows, scheduled repayments on that debt were projected to rise from $3.7�billion in 2006-07 to a peak of $5.4�billion in 2008-09, before falling to just over $4�billion in 2009-10, and further to below $1�billion in 2010-11. These payments include both the amortization of certain debt (such as deficit-financing bonds, local mandates, and settle-up payments to schools) and lump sum payments for other debt (such as loans to transportation and other special funds).

The May Revision proposes a number of changes that would have impacts on both the total amount of borrowing outstanding and the annual payments associated with the debt. Borrowing Outstanding. Despite proposed prepayments of an additional $1�billion in deficit-financing bonds and $600�million in other debt, the state would end 2006-07 with about $21.6�billion in budgetary debt outstanding. This is because the May Revision includes a proposed settlement to a court case involving Proposition�98 school funding. Under this agreement, the state would provide an additional $2.9�billion in school funding over a seven-year period. Annual Debt-Service Payments. The May Revision spreads out budgetary debt repayments in a number of areas. It assumes refinancing of roughly $1.4�billion in remaining Proposition�42 loans over ten years (consistent with the passage of SCA 7 [Torlakson] to be considered by voters in the November election) and it pays off the new school settlement obligation with annual payments averaging over $400�million for a seven-year period. On the other hand, its prepayment of deficit-financing bonds will enable the state to pay off the bonds by the middle of 2009-10, or about one-half year earlier than assumed in January. The figure shows that annual costs are somewhat less in the May Revision during 2007-08 through 2009-10, but more in 2010-11. Total payments are between $3.3�billion and $4.6�billion annually over the 2007-08 through 2009-10 period-amounts which are greater than the operating deficits projected for the period. |

Figure�2 shows the administration�s estimate of the General Fund budget condition in 2005-06 and 2006-07 after taking into account the May Revision budget proposals. It shows that the current year is expected to begin with a prior-year fund balance of $9.5�billion. Revenues and expenditures roughly balance in 2005-06, enabling the year to close with an ending balance of $9.4�billion, and a reserve of $8.8�billion. In 2006-07, General Fund revenues total $94.3�billion, or $6.7�billion less than the $101�billion in expenditures proposed for the year. This leaves a year-end fund balance of $2.7�billion and a reserve of $2.2�billion. It should be noted that the large operating shortfall in 2006-07 is partly a reflection of the administration�s proposals to prepay over $3�billion in budgetary debt owed in future years.

|

Figure 2 Governor�s Budget General Fund Condition |

||

|

(In Millions) |

||

|

|

2005‑06 |

2006‑07 |

|

Prior-year fund balance |

$9,507 |

$9,368 |

|

Revenues and transfers |

92,450 |

94,338 |

|

Total resources available |

$101,957 |

$103,706 |

|

Expenditures |

92,589 |

100,985 |

|

Ending fund balance |

$9,368 |

$2,721 |

|

Encumbrances |

521 |

521 |

|

Reserve |

$8,847 |

$2,200 |

|

Budget Stabilization Account |

— |

472 |

|

Reserve for Economic Uncertainties |

8,847 |

1,728 |

Recent Developments. At the time the 2006-07 Governor�s Budget was released in January, the U.S. and California economies had experienced a year of solid economic growth, although there were signs of softness in the fourth quarter of 2005. The administration�s budget forecast, as well as our February projections, assumed that the softness would be temporary, and that the U.S. and California economies would experience moderate growth in 2006 and 2007.

As we noted in our February Perspectives and Issues outlook, these forecasts were subject to significant downside risks from both (1) a steeper-than-expected decline in California�s real estate markets and (2) a sharper-than-expected rise in energy prices.

Economic developments since our previous forecasts have been somewhat mixed.

May Revision Forecast. Taking into account these positive and negative developments, the administration�s updated forecast is generally similar to its January projection. It assumes that inflation-adjusted U.S. gross domestic product growth will slow from 3.5�percent in 2005 to 3.3�percent in 2006 and 3�percent in 2007. This compares to the January budget estimates of 3.6�percent, 3.2�percent, and 3 percent for the same three years. The May Revision assumes that California personal income will increase by 6.2�percent in 2006 and 5.8�percent in 2007, up slightly from the January projected growth rates of 5.8�percent and 5.5�percent.

Recent Developments. Current-year revenue collections have dramatically exceeded the January budget projection. Total receipts through early May are up by nearly $4.5�billion relative to the January forecast, with over three-fourths of the gain related to much stronger-than- expected personal income tax final payments filed in April. The extraordinary growth in these payments (which were up by over 40�percent between April 2005 and April 2006) appears to be related to higher-than-expected levels of capital gains from large stock-related transactions and real estate sales, as well as strong business earnings. However, there is only limited information at this time on the mix of these factors, as well as the extent to which they are due to one-time developments.

May Revision Forecast. The administration�s updated forecast assumes that total revenues will be $92.5�billion in 2005-06 (a 12�percent increase from 2004-05) and $94.3�billion in 2006-07 (a 2�percent increase from the current year). The current-year total is up $4.8�billion from the January budget estimate, primarily reflecting a $3.9�billion gain in personal income taxes and a $700�million increase in corporate taxes. The budget-year increase since January is $2.7�billion after adjusting for policy-related changes. The administration�s forecast assumes that roughly one-half of the current year increase in personal income taxes relative to January is related to one-time sources, such as nonrecurring capital gains.

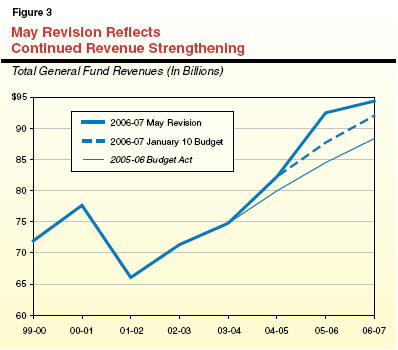

Upward Revisions Over the Past Year. As shown in Figure�3, the current-year and budget-year increases reflect a continuation of an upward trend to revenue projections. Over the past year, total projected revenues estimated for 2004-05 through 2006-07 have increased a combined total of almost $17�billion.

The May Revision�s economic and revenue forecasts are generally reasonable in view of recent developments and uncertainties about how much of the extraordinary growth in final payments in April is due to one-time versus ongoing factors. We believe that there is upside revenue potential in 2006-07, mainly related to continued strong growth in business earnings thus far in 2006. However, given the uncertainties facing the economy over the next year related to oil prices and real estate, as well as the lack of information about the one-time versus ongoing nature of the April final payments, the cautious approach taken by the administration is prudent.

Figure�4 provides information on the programmatic features of the May Revision. Given the large proportion of additional spending committed to education, we focus below on the administration�s Proposition�98 proposals. That discussion is followed by a review of the May Revision�s transportation proposal.

|

Figure 4 Key Programmatic Features of May Revision |

|

K-14 Education |

|

|

|

|

Health and Social Services |

|

|

|

|

Corrections |

|

|

Local Government |

|

|

|

|

Resources |

|

|

|

Transportation |

|

|

Figure�5 displays the May Revision changes in Proposition�98 funding compared to the January budget. The Governor proposes an additional $2.1�billion in the current year to meet the required increase in the Proposition�98 minimum guarantee-an additional $1.8�billion for K-12 and an additional $245�million for community colleges. The higher minimum guarantee results from the rapid increase in General Fund revenues in the current year. For the budget year, the Governor provides an additional $793�million for K-14 education. For the budget year, almost all of the increase goes to K-12 education.

|

Figure 5 May Revision Changes in Proposition 98 Funding |

||

|

(In Millions) |

||

|

|

2005‑06 |

2006‑07 |

|

Total Proposition 98a |

|

|

|

January budget |

$49,986 |

$54,318 |

|

May Revision |

52,045 |

55,111 |

|

Changes |

$2,059 |

$793 |

|

K-12 |

|

|

|

January budget |

$44,637 |

$48,366 |

|

May Revision |

46,451 |

49,111 |

|

Changes |

$1,814 |

$745 |

|

Community Colleges |

|

|

|

January budget |

$5,242 |

$5,848 |

|

May Revision |

5,488 |

5,886 |

|

Changes |

$245 |

$38 |

|

|

||

|

a Includes Proposition 98 funding spent by other agencies including the Department of Corrections and Rehabilitation and state special schools. |

||

Figure�6 compares the proposed 2006-07 Proposition�98 funding level to the 2005-06 Budget Act, which generally represents the funding level that schools have for their current-year operations. Total Proposition�98 funding would increase by 10.3�percent over the 2005-06 Budget Act level (10�percent for K-12 and 12.8�percent for community colleges). The figure also shows that K-12 Proposition�98 spending per pupil increases significantly. When the 2005-06 Budget Act was adopted, we estimated per pupil spending at $7,402. The Governor is now proposing $8,291 per pupil for 2006-07, an increase of $889 per pupil or 12�percent.

|

Figure 6 Year-to-Year Changes in Proposition 98 Funding |

||||

|

(Dollars in Millions) |

||||

|

|

2005‑06 |

2006‑07 |

Change |

|

|

Amount |

Percent |

|||

|

K-12 |

$44,644 |

$49,111 |

$4,467 |

10.0% |

|

Community colleges |

5,217 |

5,886 |

669 |

12.8 |

|

Other |

107 |

114 |

7 |

6.5 |

|

Totals |

$49,968 |

$55,111 |

$5,143 |

10.3% |

|

General Fund |

$36,591 |

$41,295 |

$4,704 |

12.9% |

|

Local property tax |

13,377 |

13,817 |

440 |

3.2 |

|

K-12 attendance |

6,031,404 |

5,957,368 |

-74,036 |

-1.2 |

|

K-12 per pupil spending |

$7,402 |

$8,291 |

$889 |

12.0 |

Governor Proposes Agreement With Education Community Related to 2004-05 Suspension. Chapter�213, Statutes of 2004 (SB 1101, Committee on Budget and Fiscal Review), suspended Proposition�98 for 2004-05, and established a target funding level for K-14 education that was $2�billion lower than the amount called for by the guarantee. We refer to this spending level-$2�billion below the minimum guarantee-as the Chapter�213 target. Over the course of 2004-05, an improving economy resulted in the state receiving significantly more revenues than were projected when the 2004-05 Budget Act was enacted. This increase in revenues would have resulted in a substantial increase in the K-14 minimum guarantee had the state not suspended Proposition�98. As a result, the spending level needed to meet the Chapter�213 target increased above the funding level provided in 2004-05. This funding gap became an issue of contention between the state and the education community. Because the 2005-06 Proposition�98 minimum guarantee is calculated based on the funding level for 2004-05, the 2005-06 funding level is below the Chapter�213 target as well. For 2006-07, the Governor�s January budget proposed K-14 spending to return the funding level to the Chapter�213 target, but did not provide one-time settle-up funds for 2004-05 or 2005-06. The education community sued the state, claiming that the state �owed� schools the additional funding in 2004-05 required to meet the Chapter�213 target.

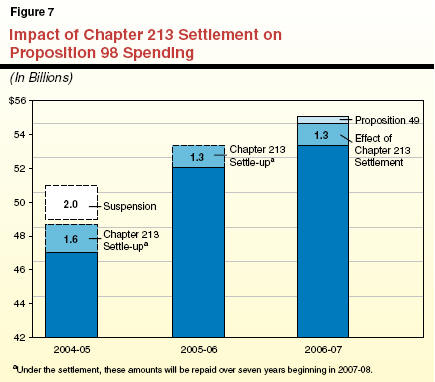

The Governor�s May Revision proposes to settle this disagreement with the education community. Specifically, the Governor proposes to restore the K-14 funding level to the Chapter�213 target for the budget year, and settle up to the Chapter�213 target for 2004-05 and 2005-06. Figure�7 shows the impact of the Chapter�213 target on Proposition�98 spending for 2004-05 through 2006-07, as adjusted for the Governor�s new revenue, attendance, and other assumptions that determine Proposition�98 funding. Specifically, the Governor proposes to pay off $2.9�billion in one-time settle-up payments ($1.6�billion from 2004-05 and $1.3�billion from 2005-06) over seven years beginning in 2007-08. (These funds would be on top of the Proposition�98 minimum guarantee obligations for those specific years, and will be counted as appropriations for 2004-05 and 2005-06 for Proposition�98 purposes.) The budget-year impact of the Chapter�213 settlement is around $1.3�billion.

Prepayment of Prior-Year Proposition�98 Obligations. In addition to these settle-up funds for 2004-05 and 2005-06, the state continues to owe $1.4�billion to meet the Proposition�98 minimum guarantee for fiscal years 1995-96 through 2003-04. Existing law requires these obligations to be settled in annual $150�million payments starting in 2006-07. The January budget includes the 2006-07 payment, and the May Revision proposes to make the 2007-08 $150�million payment a year early. These funds would be used to fund unpaid mandate costs from prior years. This would leave a total of $1.1�billion of these settle-up obligations outstanding at the close of the budget year.

Lower Attendance Frees up Funding. Attendance has decreased substantially for both K-12 schools and community colleges. For K-12, the administration estimates that attendance is 37,000 less in 2005-06 and 66,000 less in 2006-07 than projected in January. A large portion of the savings from lower attendance is automatically redirected to the costs of declining enrollment provisions. The remainder is redirected to new programs discussed in detail below. For community colleges, the administration estimates that the community colleges will fall about 60�percent short (or 20,000 full-time equivalent students) of their 2005-06 growth target, and thus about $85�million of their 2005-06 enrollment growth funding will revert to the Proposition�98 Reversion Account. The May Revision would rebench community college base enrollment funding downward by $85�million to reflect this enrollment shortfall. The administration continues to propose 3�percent growth, but now off this lower base.

The Governor�s proposal for K-14 education presents the Legislature a rare opportunity to address critical issues in K-12 education and community colleges. With the increases proposed in the May Revision, the administration would commit more than $10�billion in new ongoing and one-time funds for education. These funds are the result of the natural increase in the Proposition�98 minimum guarantee, spending to settle up past year minimum guarantees, and the settlement of the dispute about the 2004-05 suspension.

Higher ongoing funding accounts for $5.1�billion, about one-half of the increase. The budget proposes $2.6�billion in one-time funds, including $2.1�billion resulting from a higher Proposition�98 minimum guarantee for 2005-06. In addition, the budget provides $556�million to settle up Proposition�98 obligations for past years (pre-2004-05), and spend funds that have accumulated in the Proposition�98 Reversion Account. The May Revision also proposes to commit the state to appropriating $2.9�billion in Chapter�213 related settlement funds that would be programmed now, but spent in 2007-08 through 2013-14.

To use these new funds most effectively, we recommend the Legislature take a broader perspective on the needs of the education system. In crafting our recommendations on K-14 spending proposals, we relied on the following four guidelines:

Given these criteria, the Governor�s proposal has several shortcomings. Much of the Governor�s proposal creates new initiatives (one-time and ongoing) instead of strengthening the base program. The proposal does retire a significant amount of debts, especially for state mandates, but leaves more than $1.5�billion on the education credit card. The Governor also proposes using the Chapter�213 settlement funds for ongoing purposes, although the funding would end after seven years.

Below, we briefly describe the major 2006-07 proposals for K-14 education and our recommendations. We begin with the ongoing Proposition�98 funds. Then, we turn to a review of the one-time funding, followed by a discussion of the settlement funding proposal.

Ongoing Funds. Figure�8 shows the major discretionary budget increases included in the Governor�s budget and May Revision. As the figure shows, the proposed budget includes more than $2�billion in discretionary program increases. (Not shown in this figure are nondiscretionary increases in inflation and K-12 growth, which total approximately $3.1�billion.)

|

Figure 8 K-14 Proposition 98 Ongoing Spending: New Initiatives |

||

|

(In Millions) |

||

|

|

Governor |

LAO

|

|

K-12 |

|

|

|

Revenue limit equalization |

$317.8 |

$200.0 |

|

Revenue limit deficit factor reduction |

308.6 |

308.6 |

|

Counselors |

200.0 |

100.0a |

|

Mandates |

133.4 |

133.4 |

|

Arts and music block grant |

166.0 |

— |

|

Teacher recruitment and retention |

100.0 |

— |

|

Physical education |

85.0 |

— |

|

Beginning teacher support |

65.0 |

— |

|

Preschool expansion |

50.0 |

50.0a |

|

CAHSEE supplemental assistance |

50.5 |

50.5a |

|

School meal increase |

37.8 |

37.8 |

|

Economic impact aid equalization and augmentation |

— |

415.0 |

|

Special education equalization |

— |

150.0 |

|

Special education mental health |

— |

30.0 |

|

Fully fund prorated programs |

— |

48.0 |

|

Other new programs |

74.5 |

65.3 |

|

Subtotals |

($1,588.6) |

($1,588.6) |

|

California Community Colleges |

|

|

|

Growth |

$151.3 |

$88.0 |

|

Equalization |

130.0 |

160.0 |

|

Career technical education |

50.0 |

22.0 |

|

Maintenance |

29.5 |

69.6 |

|

Matriculation |

24.0 |

30.0 |

|

Mandates |

4.0 |

20.0 |

|

Other |

40.4 |

39.6 |

|

Subtotals |

($429.2) |

($429.2) |

|

Totals |

$2,018.0 |

$2,018.0 |

|

|

||

|

a We recommend alternative implementation plans instead of the administration�s proposals for these programs. |

||

As shown in the figure, we recommend approval of many of the administration�s proposals (sometimes with important program modifications). We also suggest the Legislature consider several significant changes to the proposed spending plan. Most significantly, our alternative proposal would redirect $643�million to increase funding for the Economic Impact Aid (EIA) ($415�million) and special education ($150�million) programs. We believe existing funding allocations in these two programs do not sufficiently support the goals of the programs. In addition, our EIA proposal would provide ongoing funds for disadvantaged and English learner students in lieu of the administration�s proposal to use the settlement funds for low-performing schools (which would target limited-term funding for ongoing program activities).

One-Time Funds. Figure�9 displays the major proposals in both the Governor�s budget and May Revision for the use of one-time funds for K-12 education and community colleges. Similar to the Governor�s proposals for ongoing funds, a significant proportion of the $2.6�billion in one-time funds would be used to support a variety of new and expanded programs.

|

Figure 9 K-14 Proposition 98 One-Time Spending |

||

|

(In Millions) |

||

|

|

Governor |

LAO Alternative |

|

K-12 |

|

|

|

Mandates |

$959 |

$959 |

|

Classroom supplies |

400 |

— |

|

Instructional materials |

250 |

250 |

|

Physical education equipment |

250 |

— |

|

Art and music equipment |

250 |

— |

|

Emergency repairs (Williams settlement) |

137 |

137 |

|

Library materials |

75 |

— |

|

Preschool revolving loan fund |

50 |

50 |

|

K-12 deferrals |

— |

718 |

|

Fiscal solvency block grant |

— |

300 |

|

Other |

138 |

96 |

|

Baseline adjustments |

-247 |

-247 |

|

Subtotals |

($2,263) |

($2,263) |

|

California Community Colleges (CCC) |

|

|

|

General purpose block grant |

$100 |

— |

|

Deferred maintenance/instructional materials |

100 |

— |

|

Mandates |

38 |

$100 |

|

CCC deferrals |

— |

200 |

|

Other |

25 |

— |

|

Subtotals |

($262) |

($300) |

|

K-12/CCC career technical equipment |

$90 |

$52 |

|

Totals |

$2,615 |

$2,615 |

|

|

||

Our approach would use one-time funds to repay more debt than in the administration�s plan. We think eliminating deferrals is a critical step in restoring the fiscal integrity of the state budget, and retiring much of the remaining education credit card. We recommend using $718�million to significantly reduce the amount of deferrals in K-12 education. Similarly, in the community colleges, we recommend the Legislature redirect funds to fully pay off past mandate claims and the $200�million deferral.

We also include $300�million for �fiscal solvency block grants,� which would provide a source of funding for districts to address a variety of fiscal problems including retiree health benefit liabilities. While these block grants are not large enough to completely resolve these local pressures, our proposal is intended to help districts begin addressing these fiscal challenges. This proposal of one-time funds is linked with our alternative plan for the use of the settlement funds.

Settlement Funds. As described above, the May Revision proposes to pay the difference between actual Proposition�98 appropriations in 2004-05 and 2005-06 and the target set by Chapter�213. This amount-$2.9�billion-would be paid over a seven-year period beginning in 2007-08. While a detailed plan for the use of these funds is not available, the Department of Finance indicates that the K-12 funds would support additional funds for low-decile schools for a variety of academic improvement activities. These could include class size reduction, teacher stipends, and other ongoing or one-time activities. For community colleges these funds are proposed for technical education programs, nursing programs, and improving the transfer rate to four-year colleges.

As we discussed above, we think the administration�s plan for low-decile schools would be more appropriately funded with ongoing Proposition�98 funds. Moreover, the funds could more effectively be allocated through the EIA program rather than distributed based on academic rankings. Under our plan, the settlement funds would, instead, be used to continue the fiscal solvency block grants. Beginning in 2007-08, the funding stream created by the settlement would support the block grants, which also would be broadened to include community colleges. In this way, districts and community colleges would receive a total of $3.2�billion that would be dedicated toward addressing liabilities for retiree health benefits.

The Governor�s May Revision proposes a major change in transportation funding relative to the January budget.

Current Law. Currently, a specified portion of the state gasoline sales tax revenues (known as the �spillover�) is required to be transferred to the Public Transportation Account (PTA). Spillover revenues are used to support both transit (rail and bus) capital improvement and operations, and to provide intercity rail services. For 2006-07, current law also requires that the first $200�million of spillover be retained in the General Fund and the next $125�million be used to fund seismic retrofit of state toll bridges. Any amount in excess of $325�million will go to the PTA.

Spillover Revenue Proposed for Debt Service of Transportation Bonds. Due to recent increases in gasoline prices, the May Revision projects substantial spillover revenue for 2006-07, about $670�million-roughly $350�million more than the January projection. In contrast to current law�s distribution, the May Revision proposes that starting in 2006-07, all projected spillover (other than $125�million for toll bridges) be used to pay debt service on existing and new transportation bonds.

Spillover Revenue Fluctuates Significantly; Unstable Source of Funding. In any given year, the amount of spillover revenue depends greatly on the price of gasoline as well as the sales of all other goods in the state. Everything else being constant, a large and sustained increase in the price of gasoline would significantly increase the amount of spillover revenue. Conversely, in times of stable gasoline prices, an expanding economy with growing sales of all other goods would result in little or no spillover revenue. As a result of these factors, spillover revenue has been a highly unstable source of funding for public transportation, with amounts fluctuating greatly from year to year. In 13 out of the last 30 years, no spillover revenue was generated. In the other years, spillover revenue fluctuated from a low of less than $2�million to a high of about $380�million in the current year.

May Revision Proposal Would Reduce General Fund Expenditures Substantially. . . Currently, the state pays about $350�million annually from the General Fund for debt service of three transportation bonds (Propositions 108, 116, and 192). If approved by voters in November 2006, about $20�billion in additional general obligation bonds will be authorized for transportation purposes, including $4�billion for public transit. The average debt-service payment for the new bonds would be about $1.4�billion a year.

Assuming continued high gasoline prices, the May Revision projects that over the next ten years, spillover revenues would total about $4�billion. If these revenues materialize as projected, the May Revision proposal to use these revenues for debt service would lower General Fund expenditures on debt service by several hundreds of millions of dollars a year.

. . .While Public Transit Funding Would Be Correspondingly Less. Redirecting any spillover would result in less funding for public transit by a corresponding amount, with one-half of the redirected amount coming from transit operating assistance, and the other one-half from intercity rail service and transit capital improvements. The impact is offset to the extent that the new transportation bond, if approved by voters, would provide $4�billion for capital improvements (but not operations) of mainly bus and rail transit.

In our analysis of the out-year implications of the January budget proposal, we indicated that, despite an $11�billion improvement in the revenue outlook between June 2005 and February 2006, the state would continue to face out-year operating shortfalls (that is, annual expenditures in excess of annual revenues) in the range of $4�billion to $5�billion. These estimates did not include the impacts of potential budget risks or pressures, including lawsuits, retiree health benefit liabilities, federal actions, and steeper-than-expected slowdowns in the economy.

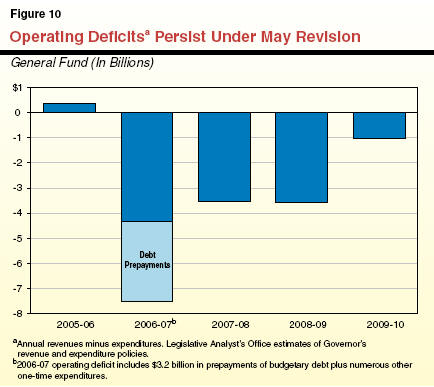

The revenue outlook has improved another $7.5�billion since the Governor�s January estimate ($5.2�billion relative to our February estimates), yet the May Revision plan would still leave the state with significant out-year budget shortfalls. As shown in Figure�10, the state would face operating shortfalls of roughly $3.5�billion in both 2007-08 and 2008-09, before dropping to around $1�billion in 2009-10 (as deficit-financing bond debt service payments drop off). The updated estimates are subject to the same risks and pressures as our February projections, in that they assume continued economic and revenue growth, and do not include potential added costs associated with lawsuits and other factors.

The May Revision raises a number of policy issues for the Legislature. Among these are:

The state�s strong revenue performance is welcome news and presents an extraordinary opportunity. We urge the Legislature to keep its focus on regaining long-term fiscal balance, particularly in view of the magnitude of risks and budgetary pressures facing the State of California.

|

Acknowledgments This report was prepared by Brad Williams with contributions from by Rob Manwaring, Paul Warren, Dana Curry, and many others in the office. The Legislative Analyst's Office (LAO) is a nonpartisan office which provides fiscal and policy information and advice to the Legislature. |

LAO Publications To request publications call (916) 445-4656. This report and others, as well as an E-mail subscription service, are available on the LAO's Internet site at www.lao.ca.gov. The LAO is located at 925 L Street, Suite 1000, Sacramento, CA 95814. |