Report in PDF

Report in PDFLAO Report

January 8, 2020FI$Cal IT Project Update—Special Project Report 8

- Background

- FI$Cal Project Status Leading up to SPR 8

- Analysis of SPR 8

- Project‑Related Workload Beyond SPR 8

- LAO Recommendations

Executive Summary

The Administration Has Been Developing an Integrated Financial Management System for the State Since 2005. For almost 15 years, the administration has been engaged in the design, development, and implementation of the Financial Information System for California (FI$Cal) project. This information technology (IT) project is being developed to replace the state’s aging and decentralized IT financial systems with a new system—FI$Cal—that integrates the state’s accounting, budgeting, cash management, and procurement processes. Over time, the cost, schedule, and scope of the project all have changed significantly. These changes have been documented in special project reports (SPRs). The FI$Cal project currently is operating under its eighth SPR.

The Administration Recently Made Significant Changes to the FI$Cal Project’s Schedule, Scope, and Cost. The eighth SPR approved by the administration delays the project deadline by one year (to July 2020). In addition, it removes some activities and functions from the project’s scope (to be finished later, after the project is deemed “complete”), while at the same time increasing project cost by $150 million. The administration has created a new arbitrary end date for the project, while proposing to continue additional work related to the project after its completion date. This muddles the determination as to when the project will actually be fully finished. We find the revised project schedule risky and the planned list of remaining activities and functions until project completion (as redefined) to fall short. As a consequence, the project—once “completed”—will not deliver what the Legislature expected when it authorized FI$Cal, and the Legislature will receive budget requests in future fiscal years to finish work that was originally within the project scope.

Changes Set Poor Precedent for Future IT Projects, and Impede and Complicate Legislative Oversight. Deeming a project complete as done under SPR 8 is inconsistent with current state IT policy. Specifically, SPR 8 ends the project before all planned functions of the FI$Cal system are implemented. This definition of project completion also is inconsistent with the agile approach—which relies on feedback from users to guide the future development of the system—completing the project before fully incorporating user feedback for some components. Legislative oversight—and that of other state entities tasked with oversight of IT projects—is complicated when project completion and measures of success are defined inconsistently across projects. In addition, current oversight processes are focused on the time up to a project’s completion, so a deemed completion prior to the actual completion of all planned activities and functions related to a project impedes oversight. Finally, legislative oversight is further limited when the administration submits budget requests for IT projects without first approving the latest project plan, as it did with SPR 8 for FI$Cal.

Recommendations to Enhance Legislative Oversight. Based on our findings related to SPR 8, we recommend the Legislature: (1) consider adopting statutory language defining IT project completion and success for the FI$Cal project; (2) consider adopting statutory language that continues current oversight practices into the operations and maintenance (post‑completion) stage of the FI$Cal project, should project completion continue to be defined as under SPR 8; and, (3) consider as a future practice adopting budget bill language that conditions the release of IT project funding (in the case of FI$Cal and IT projects more generally) on the California Department of Technology’s approval of the latest SPR and 30‑day notification being given to the Legislature that includes the total cost and schedule of the project from the project approval document.

Background

FI$Cal Project. The administration started the design, development, and implementation of the Financial Information System for California (FI$Cal) project in 2005 with the goal of replacing the state government’s aging and decentralized financial information technology (IT) systems with a new IT system—FI$Cal. FI$Cal will integrate the state’s accounting, budgeting, cash management, and procurement processes into a single system, eliminating the need for over 2,500 department‑specific applications. FI$Cal also will automate manual processes, improve tracking of statewide expenditures, provide greater transparency into the state’s financial data and management, and standardize state financial practices. With the exception of a small number of departments that are deferred or exempted from the project, the vast majority of state departments will manage their finances through FI$Cal. FI$Cal is one of the largest IT projects undertaken by the state—with a currently estimated cost of $1.1 billion total funds ($583 million General Fund). As shown in Figure 1, FI$Cal has significantly evolved since 2005 with, to date, eight major revised project plans (known as special project reports [SPRs]) that each significantly changed the project’s cost, schedule, and scope. (When it began in 2005, FI$Cal was a much smaller project estimated to be completed by 2011.) (For a more comprehensive history of the FI$Cal project, please see our March 10, 2016 report—The 2016‑17 Budget: Evaluating FI$Cal.)

Figure 1

Evolution of the FI$Cal Project Cost, Schedule, and Scope

|

Project Plan |

Total Estimated Project Cost (in Millions) |

Final Implementation Date |

Summary of Project Plan |

|

FSR |

$138 |

July 2011 |

The initial IT project was much more modest in scope than the current project. The Budget Information System, as the project was then known, was envisioned to better meet DOF’s budget development and administrative needs. |

|

SPR 1 |

$1,334 |

June 2015 |

The administration realized there was a need to modernize and replace the state’s entire financial management infrastructure. SPR 1 proposed increasing the scope of the project to include developing a single integrated financial information system for the state. The project would integrate the budgeting, accounting, cash management, and procurement functions of the state. Four partner agencies were identified—DOF, SCO, STO, and DGS—and the project was renamed FI$Cal. The SPR extended the schedule by four years and increased the cost by nearly $1.2 billion. |

|

SPR 2 |

$1,620 |

June 2017 |

SPR 2 analyzed advantages and disadvantages of various FI$Cal alternatives but proposed maintaining the project’s expanded scope to integrate the state’s financial management processes. The SPR extended the schedule by two years and increased the cost by nearly $300 million, relative to SPR 1. |

|

SPR 3 |

Unspecified |

Unspecified |

SPR 3 established the use of a multistage procurement approach. The multistage procurement strategy would assist the project in eliciting more qualified system integrators and more responsive proposals for building the FI$Cal system. The total cost and schedule for the project was left unspecified. At the conclusion of the procurement, when the software application and vendor would be selected, the project would submit SPR 4. |

|

SPR 4 |

$617 |

July 2016 |

SPR 4 updated the project cost and schedule based on the contract with the selected vendor. The total project cost for the FI$Cal system was estimated at about $620 million, about $1 billion less than estimated in SPR 2. The cost reduction is attributed to (1) updated estimates and (2) the move to a more phased implementation approach that resulted in lower overall project costs through reduced risk to the vendor and lower state staffing costs. The system would be completely implemented in July 2016. |

|

SPR 5 |

$673 |

July 2017 |

SPR 5 made various changes to the project’s implementation approach to reflect lessons learned over the two years since the vendor was selected and the development of the system began. The SPR resulted in a 12‑month schedule extension and increased the total project cost by $56 million, relative to SPR 4. |

|

SPR 6 |

$910 |

July 2019 |

SPR 6 made various changes to the project’s implementation approach to reflect lessons learned since SPR 5. SPR 6 resulted in a 24‑month schedule extension and increased the total project cost by $237 million, relative to SPR 5. |

|

SPR 7 |

$918 |

July 2019 |

SPR 7 made various changes to the project’s implementation approach, the largest of which was an alternative approach to implementing SCO and STO’s accounting and cash management functions in FI$Cal called the “Integrated Solution.” SPR 7 did not extend the schedule for project completion, and only increased the total project cost by $8 million. |

|

SPR 8 |

$1,063 |

July 2020 |

SPR 8 introduces a new definition of project completion for FI$Cal—the minimum viable product (MVP) for the Integrated Solution—that removes a number of planned activities and system functions from the project scope, while adding additional hours to complete what project scope remains to achieve the MVP. SPR 8 extends the schedule for project completion by one year and increases the total project cost by $145 million. |

|

FSR = Feasibility Study Report; IT = information technology; DOF = Department of Finance; SPR = Special Project Report; SCO = State Controller’s Office; STO = State Treasurer’s Office; and DGS = Department of General Services. |

|||

Four Control Agencies Manage Project. The FI$Cal project is managed by a partnership of four control agencies—the Department of Finance (DOF), the Department of General Services, the State Controller’s Office (SCO), and the State Treasurer’s Office (STO). Each of the partner agencies has unique constitutional and/or statutory responsibilities for state processes that FI$Cal will integrate—that is, accounting, budgeting, cash management, and procurement. State law mandates that these agencies collaborate in the design, development, and implementation of FI$Cal. A project governance plan also guides the relationships between the partners.

Department of FI$Cal Operates and Maintains the System. In 2016, state law established a Department of FI$Cal to maintain and operate the IT system and support its users. The department will assume full responsibility for the system once the project is complete. The department’s operating budget in 2019‑20 (which includes some project costs) is approximately $113 million total funds ($69 million General Fund) and includes 244 permanent positions.

CDT Approves and Oversees IT Projects, Including FI$Cal. The California Department of Technology (CDT) is responsible for reviewing and approving IT project proposals submitted by state departments. Once CDT approves a department’s proposal (and it becomes a “project”), CDT’s role is to provide project oversight. (Once an IT project is complete, it becomes an operating IT “system” and is maintained by the department operating it.) Specifically, CDT provides an independent review of the project to determine if it will achieve its scope on time and within budget. As part of this review, CDT routinely reports to departments on areas of concern it identifies with the project, shares lessons learned from other projects with departments, and recommends to them ways to reduce project risk and resolve known issues.

Over time, however, a project may change its scope or deviate from the schedule and/or cost approved by CDT. Any significant changes to a project are documented and justified in SPRs. Departments develop a revised project plan and submit it to CDT (as an SPR) for its review and approval. Once CDT approves a department’s SPR, the SPR constitutes a new agreement between CDT and the department on the project’s cost, schedule, and scope. In some cases, projects change considerably from their initial plan and several SPRs are required over the life of the project. CDT (or one of its predecessors) has performed these project approval and oversight functions throughout the life of the FI$Cal project.

FI$Cal Project Status Leading up to SPR 8

Project Successfully Implemented Budgeting and Procurement Processes. In 2015, the FI$Cal project integrated the state’s procurement processes into the FI$Cal system, launching Cal eProcure. According to the project, FI$Cal supports the entire procurement lifecycle electronically. Also in 2015, DOF prepared the Governor’s proposed budget for the first time using the FI$Cal system and, in 2016, used the system to provide the final details of the 2016‑17 enacted budget. The project also piloted its financial transparency website—Open FI$Cal—in 2018 and, in 2019, added to the website nonconfidential expenditure data from state departments using the system.

Project Added Large Number of State Departments to FI$Cal. There are 152 departments now using the FI$Cal system, including 64 departments that the FI$Cal project added to the system in July 2018. (In general, a department is “added” to the FI$Cal system when their information is available and their staff are ready to use the system for their accounting, budgeting, cash management, and procurement processes.) The number of departments using the system represents a significant percentage of all state government departments, including the majority of state expenditures.

Project Working to Implement Accounting and Cash Management Processes Through Integrated Solution. SPR 7 (the most recent revised project plan prior to the one being discussed in this report) established a new approach to implementing SCO accounting and cash management processes (and STO cash management processes) in FI$Cal—the “Integrated Solution.” The Integrated Solution is an interim solution to the implementation of these particular functions in FI$Cal that is meant to provide FI$Cal, SCO, and STO additional time to develop and test the functions before they are fully implemented as planned. Under the Integrated Solution, SCO will run the FI$Cal system and its existing legacy accounting system in tandem. The Integrated Solution will develop interfaces between both systems so that data are entered only once (in either system), but then both systems share the data. This way, each system can perform the accounting and cash management functions for the state. SCO’s legacy system, however, will continue to serve as the state’s official accounting record, even though FI$Cal will have access to all of the necessary data and functionality to produce reports such as the state’s Comprehensive Annual Financial Report (CAFR). (The CAFR is the state’s year‑end financial statement for creditors and other stakeholders.) Ultimately, the intention is to decommission the legacy systems once the Integrated Solution is no longer needed for the SCO/STO processes. (For a more detailed description of the Integrated Solution, please see our March 2, 2018 report—The 2018‑19 Budget: Evaluating FI$Cal.)

Analysis of SPR 8

Overview

Recent Challenges Triggered New SPR. The project operated under its seventh SPR, which was approved by CDT in February 2018, until August 2019. A number of challenges caused the project to deviate from its schedule and trigger the need for a revised project plan approved by CDT—SPR 8. We describe these challenges in more detail later in the analysis. Below, we provide a high‑level summary of how SPR 8 changes the FI$Cal project’s schedule, scope, and cost.

Schedule Change—Project Establishes Another Arbitrary End Date for Completion. According to traditional state IT policy, an IT project is completed when all planned system functions are implemented. Instead, SPR 8 establishes July 2020 as the project’s end date—one year later than the project’s end date of July 2019 in SPR 7. The project would end on this date even though some planned system functions will not be implemented, some departments will not be using the system, and some legacy financial IT systems will not be decommissioned. As a consequence, the project will not deliver what the Legislature expected when it authorized FI$Cal, and the Legislature will receive budget requests in future fiscal years to complete unfinished work that was originally within the project scope. Why the administration is defining the end date of the project in this way, when its common practice has been to move the end date further out if needed to get all of the planned activities done, is unclear.

Scope Change—Project Now to Be Considered “Complete” With Fewer Planned Activities and System Functions. SPR 8 defines project completion as the implementation of a “minimum viable product” (MVP) for the Integrated Solution. Projects using the agile approach to IT project development—that is, an incremental and iterative approach to the implementation of a new system, instead of a traditional approach that implements all components of the system all at once—commonly use the term MVP. The MVP refers to the version of a product with just enough features for the product’s users to determine (1) whether to continue development of the product and, if so, (2) to provide the project with feedback on the product to incorporate into future versions. According to the project, applying the concept of the MVP to the Integrated Solution will—once implemented—result in a product that will allow FI$Cal to capture the information SCO needs to generate financial reports, validate balances, and ensure FI$Cal data align with SCO legacy system data. To define project completion in this way, the project removes a number of planned activities and system functions from the project scope while adding additional hours to complete what project scope remains to achieve the MVP.

Cost Change—the Cost of the Project Increases, but Project Cost Does Not Reflect Total Costs. The project cost increases from $918 million total funds ($493 million General Fund) in SPR 7 to $1.063 billion total funds ($583 million General Fund) in SPR 8, an increase of $145 million total funds ($90 million General Fund). Figure 2 provides the revised total project cost in SPR 8 broken down by fiscal year.

Figure 2

SPR 8—FI$Cal Project Cost

(In Millions)

|

Fiscal Year(s) |

General Fund |

Total Funds |

|

2005‑06 through 2015‑16 |

$220 |

$476 |

|

2016‑17 |

97 |

114 |

|

2017‑18 |

88 |

132 |

|

2018‑19 (estimated) |

54 |

108 |

|

2019‑20 (estimated) |

67 |

132 |

|

2020‑21 (projected)a |

57 |

101 |

|

Totals |

$583 |

$1,063 |

|

aReflecting traditional IT project budgeting practice, the projected 2020‑21 project costs include operations and maintenance costs for the first year following project completion (now scheduled for July 2020). SPR = special project report; FI$Cal = Financial Information System for California; and IT = information technology. |

||

The project cost as stated in SPR 8, however, does not reflect total costs associated with the project—an issue we also raised in our analysis of SPR 7. The project cost, for example, does not include $25.6 million total funds ($15.1 million General Fund) for SCO to support the development and implementation of the Integrated Solution. The project cost also does not include funding for departments to change their business processes and hire staff to use FI$Cal. Lastly, the project does not include the addition of deferred (and possibly exempt) departments to the FI$Cal system or the completion of project‑related activities and functions that will not be implemented by the project end date (which we will discuss later in the analysis).

Below, we go into greater detail about the FI$Cal project’s challenges that triggered the need for SPR 8. We provide our analysis of the main changes made by SPR 8 in response to these challenges and identify issues raised by them. Specifically, we discuss SPR 8’s response to delays in the implementation of the Integrated Solution, including an associated change in the determination of when the FI$Cal project is considered complete. Finally, we discuss SPR 8’s stated recognition of a need for additional support for departments already using FI$Cal.

Responds to Delays in the Implementation of Integrated Solution

FI$Cal Project Implemented Some of the Integrated Solution in Late 2018. In SPR 7, the FI$Cal project planned the implementation of the Integrated Solution as the completion of six milestones. (Only five of the six milestones—Milestones 1 through 5—were within the project scope defined by SPR 7, with Milestone 6 scheduled to be completed after project completion.) Figure 3 provides a description of each of the Integrated Solution milestones.

Figure 3

Integrated Solution Milestones

|

Milestone |

Description |

|

1 |

Implement some functions STO needs to use the FI$Cal system. Implement security features for the Integrated Solution. |

|

2 |

Implement remaining functions STO needs to use the FI$Cal system. |

|

3 |

Implement some functions for Integrated Solution that allow the FI$Cal and SCO legacy systems to share some data. |

|

4 |

Implement remaining functions for Integrated Solution that allow the FI$Cal and SCO legacy systems to share and reconcile all data. |

|

5 |

Implement functions SCO needs for statewide financial reporting, including the state’s CAFR. |

|

6 |

Complete remaining activities and functions in FI$Cal system, including decommissioning the SCO legacy system and making FI$Cal the state’s book of record. |

|

STO = State Treasurer’s Office; FI$Cal = Financial Information System for California; SCO = State Controller’s Office; and CAFR = Comprehensive Annual Financial Report. |

|

The FI$Cal project implemented Milestones 1 and 2 in October 2018, and some of Milestone 3 in December 2018. The project could not implement the remaining milestones by the project end date in SPR 7 of July 2019.

Project Needed More Time to Stabilize and Support Milestones 2 and 3. One reason the project could not implement the remaining milestones by July 2019 was that the project needed to stabilize and support milestones that were already implemented to some degree—Milestones 2 and 3. (The term “stabilize” here means the project addresses any major performance or technical issues with the milestones and any other functions that have already been implemented.) After Milestones 2 and 3 were partially/fully implemented in late 2018, the project and its partners encountered a number of technical issues with the milestones and identified additional enhancements they would need for the Integrated Solution to work. As a result, the project needed more than six months to stabilize and support Milestone 2, and the project continues to stabilize and support some of Milestone 3 nearly a year after implementation.

SPR 8 Reschedules Implementation of Remaining Milestones Within Project Scope Through July 2020. The project expects to implement the remainder of Milestone 3, all of Milestone 4, and most of Milestone 5 by July 2020. The project will implement some functions within each of the milestones on a monthly basis. However, the majority of the functions will be implemented near or on July 2020. The schedule assumes that each function is stable soon after implementation, which will allow other functions to be implemented on schedule. Any functions implemented on July 2020 are assumed to be stable at some point soon after the project ends.

SPR 8 Provides More Resources for Stabilization and Support of Remaining Milestones. In response to the number of technical issues encountered with Milestones 2 and 3, the project adds dedicated resources to stabilize and support the remaining milestones after implementation. The schedule also assumes longer time frames to stabilize and support the remaining milestones that range from 6 to 24 months.

LAO Findings

New Schedule for Remaining Milestones Is Risky. In SPR 7, the project assumed it would be able to implement the remaining milestones by July 2019. A number of technical issues and additional enhancements that were needed to make the Integrated Solution work caused the project to deviate from its schedule. While SPR 8 does extend the project schedule one year and anticipates more time will be needed to stabilize and support the remaining milestones, we find the project schedule to be risky for several reasons:

- Some of the remaining milestones are more complex to implement than milestones already implemented. Any technical issues with these milestones could take longer to address, and any rush to implement them could lead to errors in the system.

- Some functions in the remaining milestones must be stable for other later functions to be implemented. The project needed more time than initially anticipated to stabilize Milestones 2 and 3. Given the complexity of the remaining milestones, there is a risk (as discussed in more detail in the paragraph below) the project will again need more time.

- Some functions in the remaining milestones must be implemented at the start of a fiscal year for SCO to collect data in both systems to prepare (as an example) the state’s CAFR. Any delay in the implementation of these functions might delay the preparation of the state’s CAFR using FI$Cal by (at least) one year.

Longer Time Frames to Stabilize and Support Remaining Milestones Likely Still Too Short. The FI$Cal project anticipates needing six months to stabilize and support Milestones 3 and 4, and 12 months to stabilize and support some of Milestone 5. Despite these time frames being longer than those estimated in SPR 7, they are likely still too short. The project needed longer than six months to stabilize and support Milestone 2, and continues to stabilize and support some of Milestone 3 nearly a year after implementation. If the project needs additional time to stabilize and support some of the milestones it implements, the project might not be able to implement other milestones that are dependent on the already implemented milestones being stable.

Stabilization and Support of Remaining Milestones Occurs After Project End Date. The stabilization and support time frames for some of Milestones 3 and 4 and all of Milestone 5 are scheduled after the project end date. The project schedule, therefore, suggests that the project could end before the Integrated Solution is stable. The project attempts to mitigate this risk by deploying some functions and testing their stability before their scheduled implementation date, and by requiring SCO to accept the MVP for the Integrated Solution before the project can end. The project, however, could still “implement” functions that are not stable (even after additional time to deploy and test), and SCO could still accept the MVP without knowing whether or not the Integrated Solution is stable (or reject the MVP without a clear path forward). To ensure that what the project delivers is stable, the stabilization and support time frames for the remaining milestones should remain within the project schedule.

Revises Definition of Project Completion: MVP for Integrated Solution

SPR 8 Introduces MVP for Integrated Solution. As noted above, SPR 8 uses a new term to define the completion of the FI$Cal project—the MVP for the Integrated Solution. SPR 8 defines the MVP for the Integrated Solution as a product that allows FI$Cal to capture the information SCO needs to generate financial reports, validate balances, and ensure FI$Cal data align with SCO legacy system data. In using the MVP to define project completion, the project removes a number of planned activities and system features from the project scope, while assuming at the same time it will take longer to complete what project scope remains.

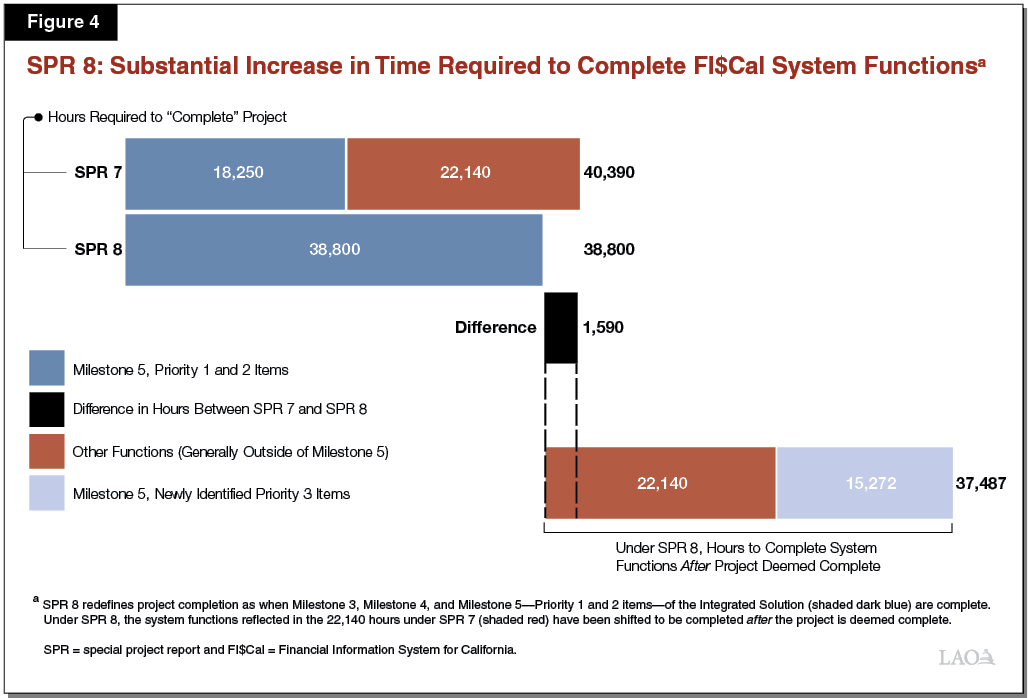

MVP Adds Additional Hours to Complete Most of Remaining Project Scope. In defining the project scope in SPR 7, the project estimated the number of hours it would need to complete the Integrated Solution. (As shown in Figure 4, for example, SPR 7 assumed the project would need 18,250 hours for Milestone 5 functions and 22,140 hours for some other functions that were previously in other milestones in order to complete the Integrated Solution.) As the project implemented some of the milestones of the Integrated Solution (and more fully planned others), the project learned that it would need more time both to complete the existing functions of the Integrated Solution and the new functions it did not anticipate in SPR 7. In SPR 8, the project recalculates the number of hours it would take to complete the MVP for the Integrated Solution. While the MVP includes the majority of the project scope from SPR 7 (removing some scope, which we discuss below), it assumes that more than double the number of hours—from 18,250 hours in SPR 7 to 38,800 hours in SPR 8, as shown in Figure 4—will be needed to complete what remains.

MVP Removes Some of the Project Scope to Accommodate Additional Hours. SPR 8 removes a number of functions from the project scope that, although critical to the completion of the FI$Cal system, are not needed to complete the MVP for the Integrated Solution. In other words, the project moves these functions to be completed after the project (as redefined in SPR 8) is considered done. The project calculated the number of hours it would need to complete these functions—that is, 22,140 hours as shown in Figure 4—and it is roughly equivalent to the additional hours the project will need to complete the MVP for the Integrated Solution. Figure 4 shows the net change in the estimated number of hours for the remaining project scope (as redefined by SPR 8)—that is, a net decrease of 1,590 hours. However, this small net decrease in hours to complete the project (with a narrower scope) is overwhelmed by the resulting increase under SPR 8 in the estimated number of hours for functions completed after the project is deemed complete—that is, an additional 37,487 hours (22,140 hours for other functions moved out of the project scope to be completed later and an additional 15,272 hours newly identified for Milestone 5 functions the project considers to be outside of the project scope).

LAO Findings

New Definition of Project Completion Inconsistent With Agile Approach; Legislative Oversight Is Compromised. Agile projects use the term MVP to refer to a version of a product—often the first version, with a minimum number of functions users need to determine whether to continue development of a product and, if so, to decide how it can be improved. The FI$Cal project, however, uses MVP to define the completion of the Integrated Solution and the project. To allow a project to end this way is inconsistent with state IT policy in general, as it ends the project before all planned functions of the FI$Cal system are implemented. The inconsistency of SPR 8’s definition of project completion with the agile approach is also problematic—under SPR 8, the FI$Cal project will be considered complete before taking advantage of all of the feedback from users to guide the future development of the system. This sets a poor precedent for future IT projects that use the agile approach. The oversight authority of the Legislature—and other state entities with oversight of IT projects—is compromised when key terms such as project completion and measures of success are defined inconsistently across projects. Such inconsistency makes it confusing for oversight agencies and more difficult for them to track projects.

Recent Changes Since Approval of SPR 8 Raise Questions About MVP. Since CDT’s approval of SPR 8 at the end of August, the FI$Cal project has moved at least four additional functions out of project scope to be completed later (after the project is deemed complete) and identified more functions it will need to complete the MVP. (These changes are not reflected in Figure 4, and would have an uncertain net effect on the number of hours.) These changes in project scope suggest the project might not know whether the MVP is, in fact, the “minimum” set of functions or is “viable.” Not only will some of the key functions in the remaining milestones be stabilized and supported after the project end date (as we previously discussed), but also the Integrated Solution will start capturing (and validating) most of the information that SCO needs after the project end date. If the milestones are not stable or the Integrated Solution does not capture (and also validate between the FI$Cal system and SCO legacy system) the information SCO needs, the Integrated Solution might not be viable. A MVP that might not include the minimum number of functions or might not be viable means that its users might not be able to make an informed decision and provide feedback regarding its continued development consistent with the agile approach.

SPR 8 Adds Additional Hours Without a Complete Plan. To create the MVP in SPR 8, the project moved an estimated 22,000 hours of work for critical system functions from the previously defined project scope to be completed after the project is deemed complete. These system functions join a list of other activities and functions to be completed in the future as part of Milestone 6, including the addition of deferred (and possibly exempt) departments to the FI$Cal system and the decommissioning of legacy financial IT systems. SPR 8 does not include a plan for Milestone 6 or, more generally, an operations and maintenance (O&M) plan, and does not include any of the costs associated with Milestone 6 in the total project cost for FI$Cal. (An O&M plan is a document submitted by a project to CDT for approval with detailed information about the activities that will be completed after the project ends, including the estimated cost of each activity, the estimated date of completion, and any risks or consequences to the system from delayed completion or a failure to complete each activity. Generally, the cost of activities included in an O&M plan are not included in a project’s total cost.) What plan SPR 8 does offer for certain O&M activities includes an estimated 15,000 hours of work for new functions—Milestone 5, Priority 3 items—that it did not anticipate in SPR 7 and that it adds to the list of activities and functions to be completed after the project ends (including the 22,000 hours of work moved from the previously defined project scope). These 15,000 hours may therefore be viewed as additional hours being added to the overall number of hours connected with the project (before and after deemed completion). The project expects to implement Milestone 5, Priority 3 items by June 2021—after the project end date. More work added for after the project ends without a complete plan compromises the Legislature’s oversight of the FI$Cal system, as discussed below.

Activities and Functions to Be Completed After the Project Ends Not Subject to Same Level of Legislative Oversight as FI$Cal Project. Current oversight practices for a highly critical IT project such as FI$Cal will not continue after July 2020 (the revised project end date) without an O&M plan or other authority—such as statutory language—that continues those practices into the O&M phase of the project. (Current oversight includes at least monthly meetings with the project and stakeholders—including the Legislature—to review oversight reports on the project.) An O&M plan can include measures such as specific oversight practices to ensure all remaining activities are completed successfully. The importance and volume of activities and functions to be completed after the project ends suggests continued oversight of this stage, and more generally of the FI$Cal system, is warranted.

Provides Additional Support for Departments Already Using FI$Cal

SPR 8 Anticipates Additional Support Will Be Necessary for Departments Using FI$Cal. A significant number of departments with large budgets now use the FI$Cal system. SPR 8 anticipates that most of the departments will need additional support from the project and the Department of FI$Cal as the project implements the Integrated Solution and as departments close their month‑ and (fiscal) year‑end financial statements. Implementation of the Integrated Solution will require some departments to change their business processes to accommodate the new functions implemented in the FI$Cal system. Other departments will need to learn how to close month‑ and year‑end financial statements in the system, and might ask for help when they have difficulty entering, processing, and/or reconciling their data. Nearly all departments will need additional training of new and existing staff on how to use the system.

Legislature Approved Additional Funding in 2019‑20 Budget Act for Department of FI$Cal. To provide additional support to departments (and implement the Integrated Solution), FI$Cal requested—and the Legislature approved—$64.1 million total funds ($39.1 million General Fund) over three fiscal years. With this funding, the Department of FI$Cal will provide additional user training (including on closing month‑ and year‑end financial statements in FI$Cal) and department support (including, for example, on changing their business processes and identifying potential enhancements to the system). The FI$Cal project also will use some of this funding to stabilize and support the remaining milestones of the Integrated Solution. The Legislature approved these resources in June as part of the 2019‑20 Budget Act, more than two months before CDT approved the new project plan for FI$Cal in August.

LAO Findings

Several Departments Missed Deadlines for Year‑End Financial Statements. As part of its 2019‑20 budget request to the Legislature, FI$Cal set a goal of providing enough support—that is, additional staff, training, and other resources—to every department using FI$Cal to close their year‑end financial statements in the system no later than the October following the end of a fiscal year in June. Recent data from FI$Cal show the project did not meet its goal for the 2018‑19 fiscal year by a significant margin—only 77 out of 152 (or 51 percent) departments using FI$Cal closed their financial statements by October. The 77 departments that closed their financial statements on time also represent only a small fraction of the total departmental budgets in FI$Cal—$35 billion out of $295 billion (or 12 percent). As shown in Figure 5, as of November 2019, a number of large departments, such as the Department of Education and the Employment Development Department, have yet to submit their 2018‑19 year‑end financial statements.

Figure 5

Several Large Departments Using FI$Cal Have Yet to

Submit Their 2018‑19 Year‑End Financial Statementsa

(In Billions)

|

Department |

2018‑19 Budget |

|

California Department of Education |

$81.6 |

|

Employment Development Department |

14.9 |

|

California Community Colleges Chancellor’s Office |

10.0 |

|

Department of Developmental Services |

7.4 |

|

Judicial Council of California |

5.2 |

|

aAs of November 2019. FI$Cal = Financial Information System for California. |

|

Uncertain How Large Departments With Late/Estimated Year‑End Financial Statements Will Impact State’s 2019‑20 CAFR. Given the significant number of departments with year‑end financial statements outstanding—and their impact on the amount of total departmental budgets closed in FI$Cal—what impact the submission of late or estimated year‑end financial statements for these departments will have on the state’s 2019‑20 CAFR is uncertain. In its most recent report on the FI$Cal project, the California State Auditor mentions the possibility that it could issue a modified opinion of the CAFR—that is, a finding that the financial statements referred to in the CAFR might not be presented completely and accurately. The Auditor noted that a modified opinion could, for example, lead a bond‑rating agency to downgrade the state’s bond rating because the agency cannot rely on the state’s CAFR (and possibly other financial statements) for decision‑making.

Unclear How Additional Funding for Department of FI$Cal Complements Funding and Resources Requested by Other Departments Using FI$Cal. One of the reasons the Department of FI$Cal requested more funding in the 2019‑20 budget cycle was to provide departments with additional support. At least 13 departments, however, separately requested FI$Cal‑related resources during the 2019‑20 budget cycle. Whether the departments coordinated their requests with the Department of FI$Cal to, for example, ensure the requested resources were complementary and not duplicative is unclear. While these are costs associated with the FI$Cal project, SPR 8 does not include them in the total project cost.

Administration Limited Legislature’s Oversight by Submitting a Project Funding Request Before Approving an SPR. The administration submitted a budget request for the Department of FI$Cal and the FI$Cal project prior to the approval of SPR 8. Without an approved SPR, the Legislature did not have updated information about the cost, schedule, and scope of the project with which to consider the budget request. By not providing this information, the administration limited the Legislature’s oversight of the project, such as the Legislature not having a complete view of all of the significant changes to the FI$Cal project scope.

Project‑Related Workload Beyond SPR 8

In this section, we describe what work remains to be done after the project is complete (as redefined by SPR 8). Remaining workload after project completion includes the activities and functions removed from the project scope by SPR 8 (and others already moved to Milestone 6); the addition of deferred (and possibly exempt) departments to the FI$Cal system; and the continued support of departments already using FI$Cal to close their financial statements on time, decommission their legacy systems, and train their staff and update their business processes.

Activities and Functions to Be Completed After the Project Ends. The work to be completed for the FI$Cal project after it ends is large relative to other IT projects. In addition to the 22,000 hours of work for critical system functions moved from the project scope to be completed later and the 15,000 hours of work for new functions—Milestone 5, Priority 3 items—in SPR 8, the post‑project completion stage also includes the development of many other functions in the FI$Cal system. These include the transition from SCO’s legacy system to FI$Cal as the state’s book of record and the decommissioning of SCO’s legacy system. While the number of hours required to complete this stage is unknown currently, the project partners likely will work on completing these activities and functions through at least 2022. (SPR 8 anticipates SCO could consider a transition to FI$Cal as the state’s book of record as well as consider decommissioning its legacy system—thereby ending the Integrated Solution—in 2022.)

Deferred and Exempt Departments. According to FI$Cal, there are nine state entities that are deferred from the FI$Cal system (which means they will be added to the system at a later time), including some large departments such as the Department of Corrections and Rehabilitation and the Department of Transportation. Figure 6 provides a full list of the remaining departments that are deferred or exempt (which means they are not expected to be added to the system at this time) from the FI$Cal system.

Figure 6

Number of Large Departments Remain Deferred or

Are Exempt From Using FI$Cal

|

Deferred Departments |

|

Department of Corrections and Rehabilitation |

|

Department of Justice |

|

Department of Motor Vehicles |

|

Department of Technology |

|

Department of Transportation |

|

Department of Water Resources |

|

Prison Industry Authority |

|

State Lottery Commission |

|

State Teachers’ Retirement Systema |

|

Exempt Departments/Fund |

|

California Law Revision Commission |

|

California State Auditor |

|

California State University |

|

Department of Rehabilitation |

|

Legislative Counsel Bureau |

|

Legislature |

|

Public Employees’ Retirement System |

|

State Compensation Insurance Fund |

|

State Teachers’ Retirement Systemb |

|

University of California |

|

aAccounting only. bExcept accounting. FI$Cal = Financial Information System for California. |

A number of the deferred departments have existing contracts for IT systems that perform some or all of the functions of the FI$Cal system and, when those contracts expire, we understand that the administration will consider whether or not to add the departments to FI$Cal. If the administration does decide to add a department to FI$Cal, FI$Cal will determine how much it will cost to add the department and likely request those resources through the budget process.

Departments Currently Using FI$Cal. FI$Cal will be involved in a number of one‑time and ongoing activities with the 152 departments that currently use the FI$Cal system, including helping departments close their month‑ and year‑end financial statements, decide whether to decommission their legacy financial IT systems, and participate in change management efforts to (as an example) train new and existing departmental staff on how to use the FI$Cal system.

- Financial Statements. FI$Cal was expected to change how departments close their month‑ and year‑end financial statements both by improving the process in the FI$Cal system itself (through additional system development), and by working directly with departments to make their business processes for closing these statements more efficient. Given the number of departments that were unable to close their 2018‑19 financial statements in FI$Cal, these efforts likely will continue over the next several years.

- Legacy Systems. An unknown number of departments that use the FI$Cal system also continue to use their legacy financial IT systems as well. Nearly all departments that were using the primary legacy financial IT system—the California State Accounting and Reporting System—now only have limited access to that system. However, several other legacy systems remain in use because, for example, the functions the departments need are not available in the FI$Cal system. Whether a state entity can require departments to decommission their legacy systems is unclear. These decisions likely will continue to involve FI$Cal, however.

- Change Management. FI$Cal continues to train department staff on how to use the FI$Cal system. As departments use the FI$Cal system, many of them consider changes in their business processes that can require additional resources or enhancements to the existing FI$Cal system. These efforts to change how a department operates in response to the implementation of a new IT system is called change management. FI$Cal likely will be more involved in change management efforts in the next several years because of the number and size of the departments that were recently added to the FI$Cal system and the number of functions (including the Integrated Solution) that remain to be implemented and could change how departments operate.

LAO Findings

Remaining Workload After Project Ends Critical to Project Success. SPR 8 moves the project end date to July 2020, at which time (if the MVP for the Integrated Solution is implemented) the administration will consider the project complete. It is clear that while the administration will consider the project complete, there are number of activities that continue beyond SPR 8 that are critical to the project’s success. The completion of activities and functions removed from the project scope by SPR 8 (and others already moved to Milestone 6), the addition of deferred (and possibly exempt) departments to the FI$Cal system, and the continued support of departments already using FI$Cal are all essential to FI$Cal becoming the state’s single system for accounting, budgeting, cash management, and procurement. These activities also come at a cost, the sum of which should be considered together with the approved total project cost for FI$Cal.

LAO Recommendations

Based on our findings related to SPR 8, we make the following recommendations related to FI$Cal.

Consider Statutory Language to Define Project Completion and Success. We recommend that the Legislature consider adopting statutory language that defines project completion and success for the FI$Cal project. Current statutory language defines the broad objectives of the FI$Cal system, but does not define what activities must be done for the FI$Cal project to be considered complete or successful. The project’s current definition of completion as the MVP for the Integrated Solution is inconsistent with the agile approach (meaning it is unclear whether the project will deliver system functions in a way that allows for feedback from users regarding their continued development), is an incomplete implementation of the Integrated Solution, and sets a poor precedent for future IT projects that use the agile approach. Project completion could, for example, be defined as FI$Cal becoming the state’s book of record with accounting and cash management processes fully implemented in the system. Measures of “success” could be, for example, the number and cost of the legacy financial IT systems that have been decommissioned as a result of the FI$Cal system and the number and cost of those legacy systems that remain.

Consider Statutory Language to Continue Legislative Oversight of Project Beyond Deemed Project End Date. We recommend the Legislature consider adopting statutory language that continues current oversight practices into the next phase of the project beyond its revised deemed end date of July 2020, given the large number of activities and functions that are expected to continue beyond this date. After July 2020, the current oversight practices for FI$Cal will not continue without an O&M plan or other authority that continues those practices. (Except for the State Auditor’s oversight role, most oversight activities with respect to FI$Cal have developed as a matter of practice and are not codified in statute.) These practices would include (but not be limited to) at least monthly meetings with FI$Cal and stakeholders and the continued involvement of independent project oversight and independent verification and validation consultants.

In Future, Consider Budget Bill Language to Condition Release of Project Funding on Approval of Latest SPR. We recommend the Legislature in the future consider adopting budget bill language that conditions the release of IT project funding (in the case of FI$Cal and IT projects more generally) on (1) CDT’s approval of the latest SPR and (2) 30‑day notification being given to the Legislature (Joint Legislative Budget Committee) that includes the total cost and schedule of the project from the project approval document. We see this as a way to structurally improve and protect the Legislature’s oversight authority. As discussed above, the administration limited the Legislature’s oversight of the project by submitting a 2019‑20 budget request for the Department of FI$Cal and the FI$Cal project without the latest SPR approved by CDT. Budget bill language provides the Legislature with another opportunity to review the budget request alongside the project plan to determine, for example, if the changes in the plan merit additional resources.