![]()

The Governor signed the 2002-03 Budget Act on September 5, 2002, a record 67 days into the new fiscal year. In enacting the $99 billion budget, the Legislature was faced with the unprecedented and formidable task of addressing a $23.6 billion shortfall. It did this through adopting a variety of program savings, borrowings and loans, transfers, deferrals, and revenue augmentations. The budget also includes a modest year-end General Fund reserve of $1 billion. In terms of the budget's growth, both current-dollar and real per capita spending in 2002-03 are down modestly from their prior-year levels.

In this chapter, we first discuss the factors underlying the major fiscal challenge facing the Governor and Legislature as they approached the 2002-03 budget, and then describe the key actions taken to address the shortfall. In subsequent chapters, we provide additional details about the adopted budget package, including its main features, its development, and its revenue and expenditure detail.

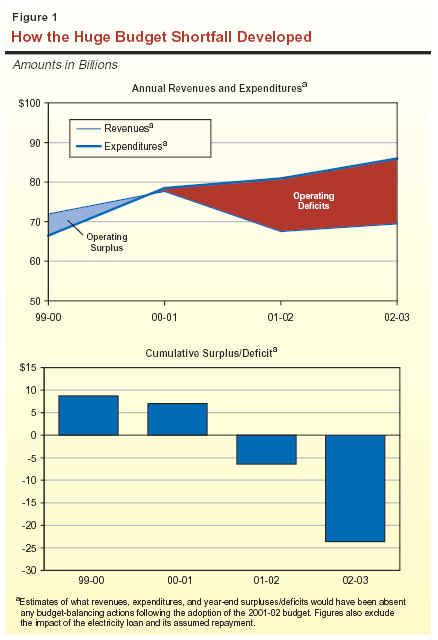

The $23.6 billion budget gap facing the Governor and Legislature in 2002-03 reflected the cumulative impact of an unprecedented decline in General Fund revenues in 2001-02 and 2002-03, along with projected continued growth in General Fund expenditures during the two years. The budgetary impact of these trends is depicted in Figure 1 (see page 2), which shows what revenues and expenditures would have been in 2000-01 through 2002-03 had there been no budget-balancing actions taken following the 2001-02 budget's enactment. (These figures have also been adjusted to exclude the $6.2 billion electricity loans in 2000-01 and their assumed repayments in 2001-02.) The figure shows that:

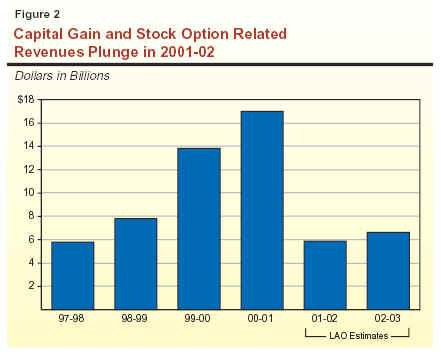

As indicated above, the large revenue decline was the main factor behind the budget shortfall. This decline was the largest in any single year since the Great Depression. While the national and state economic downturns beginning in 2001 played a significant role, the main factor behind the revenue plunge was the sharp drop in stock market-related revenues. As shown in Figure 2, we estimate that total personal income tax receipts related to stock options and capital gains fell from $17 billion in 2000-01 to roughly $6 billion in both 2001-02 and 2002-03. Even with an assumed sustained recovery in overall economic activity in 2002, the loss of stock market-related revenues reduced the ongoing amount of annual state revenues by well over $10 billion relative to pre-2001-02 levels.

As indicated above, based on the provisions and assumptions incorporated in the 2002-03 budget package, all of the $23.6 billion budget gap would be eliminated by the close of the budget year. Figure 3 shows the various budget-related solutions that were adopted (based on the administration's methodology for categorizing the savings). These include:

|

Figure 3 |

|||

|

(In Billions) |

|||

|

Estimated

Funding Gap |

2001‑02 |

2002‑03 |

Total |

|

Program cost savings |

$1.8a |

$5.6 |

$7.5 |

|

Increased borrowing |

0.2 |

5.4 |

5.6 |

|

Inter-fund loans, funding shifts, and transfers |

1.4b |

3.5 |

4.8 |

|

Revenue increases |

— |

2.9 |

2.9 |

|

Deferral of certain education disbursements |

1.0c |

0.7 |

1.7c |

|

Assumed increased federal funds |

0.1 |

1.0 |

1.1 |

|

Total Actions |

$4.6 |

$19.0 |

$23.6 |

|

a

Includes $0.2 billion in 2000‑02 savings |

|||

|

b

Includes $0.3 billion in 2000‑01 funding shifts. |

|||

|

c

Represents funds deferred in Chapter 101, Statutes of 2002

(AB 3011, Committee on Budget). Does not include $77 million in

school performance award payments deferred in the 2002‑03

Budget Act. |

|||

|

Detail may not total due to rounding. |

|||

Although the above actions addressed the budget problem for 2002-03, they did not eliminate the multibillion dollar underlying imbalance that currently exists between General Fund revenues and expenditures. This is because most of the adopted budget solutions are either one-time or limited-term in nature. In fact, some of the actions--such as the special fund loans, borrowing, and net operating loss suspension--will result in additional budgetary obligations in later years. Because of the relatively limited amount of ongoing savings incorporated in the 2002-03 budget package, the state will continue to face large multibillion shortfalls in 2003-04 and beyond, absent corrective actions.