March 13, 2009

2009-10 Budget Analysis Series

The Fiscal Outlook Under the February Budget Package

Summary

Impressive Progress on Balancing 2009–10 Budget…

The budget package of $42 billion in solutions adopted by the Legislature and the Governor in February was an impressive step in addressing the state’s monumental budget shortfall. The package has a number of positive characteristics. By taking early action, the package allows solutions to be fully implemented by the start of 2009–10 so that full–year savings are generated. The budget uses both sides of the ledger—revenue increases and spending reductions—to attack the state’s dire fiscal situation. In addition, other than preserving the lottery borrowing proposal developed in 2008, the package resists adding significant amounts of new budgetary borrowing.

…But More Work to Be Done

Unfortunately, the state’s economic and revenue outlook continues to deteriorate. Even in the few weeks since the budget was signed, there have been a series of negative developments. Our updated revenue forecast projects that revenues will fall short of the assumptions in the budget package by $8 billion. Consequently, the Legislature and Governor will need to adopt billions of dollars in additional solutions in the coming months to bring the 2009–10 budget back into balance. Moreover, a number of the adopted solutions—revenue increases and spending reductions—are of a short–term duration. Thus, without corrective actions, the state’s huge operating shortfalls will reappear in future years—growing from $12.6 billion in 2010–11 to $26 billion in 2013–14.

Budget Counts on Nearly $6 Billion From the May Election

The budget package relies on the passage of three ballot measures to provide nearly $6 billion in 2009–10 solutions—$5 billion from the borrowing of future lottery profits (Proposition 1C), about $600 million by redirecting dedicated childhood development funds (Proposition 1D), and about $230 million by redirecting dedicated mental health funds (Proposition 1E). If these measures were to fail, the Legislature would need to quickly develop even more solutions before the start of the fiscal year as alternatives.

In future years, if all six measures on the special election ballot were to pass, the state’s finances would be affected in a number of ways. Propositions 1D and 1E would provide General Fund relief for a limited number of years. On the other hand, under our projections, Proposition 1B (education supplemental payments) and Proposition 1C would drive up General Fund costs by more than $1 billion annually by 2013–14. The fiscal effect of Proposition 1A, dealing with the Budget Stabilization Fund (BSF) “rainy day” reserve, is the most uncertain. While the measure would help balance future state budgets by extending recent tax increases for up to two years, it could also take billions of dollars “off the table” by requiring their deposit into the BSF. If the state is not always able to access these funds under Proposition 1A’s rules, the state’s budget shortfalls would grow even further in some years.

Closing the Additional Budget Gap

We recommend that the Legislature take a two–pronged approach in addressing the projected $8 billion drop in revenues:

- Optimize the Use of Federal Funds. With the drop in revenues, the minimum guarantee for K–14 education under Proposition 98 will also drop. This will allow the state to use billions of additional federal dollars to offset General Fund education costs currently budgeted. The Legislature should take advantage of this opportunity to lower General Fund spending to the minimum guarantee while preserving the level of support for these educational programs envisioned in the enacted budget package. While seeking to offset 2009–10 General Fund costs is the most immediate concern for the use of federal funds, the Legislature should also seek to preserve as many federal dollars as possible to help balance the budget in future years—as opposed to committing them now for augmentations.

- Continue Work on More Solutions. The Legislature should use the spring budget process to continue developing programmatic solutions. We provide a list of options from our recent publications to reduce spending and increase revenues (without additional rate increases).

Overview

The national recession and financial market credit crunch have dragged down California’s economy and state revenues. The 2009–10 Governor’s Budget projected that the state would end 2009–10 with a $40 billion deficit if no corrective actions were taken. In response, in February 2009, the Legislature and the Governor agreed to a $42 billion package of solutions (including the Governor’s vetoes of almost $1 billion). This package includes spending reductions, temporary tax increases, the use of federal stimulus funds, and borrowing from future lottery profits. Almost $6 billion of the package depends on voter approval at a May 19, 2009 special election.

Unfortunately, the state’s economic outlook since the release of the Governor’s budget has continued to deteriorate. Consequently, we project that the Legislature and the Governor will need to agree to billions of dollars in additional budgetary solutions to rebalance the 2009–10 budget. This report first highlights the major components of the $42 billion package, then lays out our office’s new long–term forecast of the state’s revenues and spending, and concludes with key considerations for the Legislature as it moves forward with its budget planning.

Closing a $40 Billion Shortfall

Major Solutions

Figure 1 summarizes the adopted $42 billion package which closed a $40 billion shortfall and built up a $2 billion reserve. The four main components of the budget package, described in more detail below, are:

- Spending Reductions. The package includes more than $15 billion in spending–related reductions. The largest reductions relate to K–12 schools, which experience both reductions to base program funding and the deferral of payments to future years. Reductions also include furloughing state workers, eliminating inflationary adjustments for many programs, and making other reductions in services.

- Tax Increases. The package includes about $12.5 billion in temporary tax increases. Most of these higher taxes are the result of increased rates for the sales and use tax (SUT), vehicle license fee (VLF), and personal income tax (PIT).

- Borrowing. The package counts on $5 billion from the borrowing of future lottery profits, which requires the passage of Proposition 1C at the May special election.

- Federal Funds. The package also assumes receipt of $8.5 billion in federal funds from the recent economic stimulus law to help balance the budget.

Figure 1

How the February 2009 Budget Package

Closes the $40 Billion Shortfall |

(In Millions) |

|

2008‑09 |

2009‑10 |

Two-Year

Total |

Tax Increases |

|

|

|

Increase sales tax by 1 cent |

$1,203 |

$4,553 |

$5,756 |

Increase vehicle license fee by 0.5 percent |

346 |

1,692 |

2,038 |

Increase personal income tax rates by 0.25 percentage point |

— |

3,658 |

3,658 |

Reduce dependent credit |

— |

1,440 |

1,440 |

Create new tax credits |

-15 |

-363 |

-378 |

Subtotals |

($1,534) |

($10,980) |

($12,514) |

Spending-Related Savings |

|

|

|

Reduce Proposition 98 spending |

$5,775 |

$2,647 |

$8,422 |

Reduce health and social services spending |

131 |

1,518 |

1,650 |

Furlough state workers and reduce other employee costs |

333 |

834 |

1,167 |

Reduce higher education spending |

132 |

756 |

888 |

Seek voter approval to redirect Propositions 10 and 63 monies |

— |

835 |

835 |

Redirect transportation funds |

254 |

407 |

661 |

Reduce Corrections and Rehabilitation (Governor’s veto) |

— |

400 |

400 |

Reduce other spending |

140 |

1,198 |

1,337 |

Subtotals |

($6,765) |

($8,594) |

($15,360) |

Borrowing |

|

|

|

Issue lottery bonds |

— |

$5,001 |

$5,001 |

Borrow from special funds |

$234 |

94 |

328 |

Subtotals |

($234) |

($5,095) |

($5,329) |

Federal Stimulus Funds |

$2,825 |

$5,701 |

$8,527 |

Total Solutions |

$11,358 |

$30,371 |

$41,730 |

Triggers

The budget package contains two “triggers” which modify the details of the plan if certain events happen.

Federal Funds Trigger. At the time the budget was adopted, the total amount of funds that the state would receive from the federal government as part of the economic stimulus package was not known. In particular, it was unclear what portion of those dollars received would be able to be used to offset General Fund costs. The budget package currently relies on $8.5 billion in federal economic stimulus funds to offset General Fund costs through 2009–10. If it is determined that more than $10 billion will be available, then $2.8 billion in spending reductions and tax increases included in the budget package would not go into effect.

Proposition 1A Trigger. The temporary tax increases adopted as part of the budget are scheduled to last about two years. If Proposition 1A (which makes changes to state budget practices) on the special election ballot passes, however, these tax increases would be extended for one to two years. Specifically, the SUT increase would be extended one year, and the VLF and PIT–related changes would be extended two years.

General Fund Condition

Figure 2 shows the state’s General Fund condition under the adopted budget package’s assumptions. Under these assumptions, the state would end the current year with a $3.4 billion deficit. In 2009–10, the state would spend $92.2 billion—$5.5 billion less than the $97.7 billion in expected revenues. This difference would allow the state to cover the 2008–09 ending deficit and build up a $2.1 billion reserve.

Figure 2

General Fund Condition

Under February Budget Package |

(In Millions) |

|

2008‑09 |

2009‑10 |

Prior-year fund balance |

$2,376 |

-$2,341 |

Revenues and transfers |

89,372 |

97,729 |

Total Resources Available |

$91,748 |

$95,388 |

Expenditures |

$94,089 |

$92,206 |

Ending Fund Balance |

-$2,341 |

$3,182 |

Encumbrances |

1,079 |

1,079 |

Reserve |

-$3,420 |

$2,103 |

Budget Stabilization Account |

— |

— |

Special Fund for Economic Uncertainties |

-$3,420 |

$2,103 |

Budget Process for 2009–10

The budget package includes 36 bills (see Figure 3), including revisions to the 2008–09 Budget Act and adoption of a new 2009–10 Budget Act. In other words, the state has already adopted its 2009–10 budget—more than four months before the start of the fiscal year. Such an early adoption is unprecedented and requires some adjustments to the normal budget process. For instance, the enacted 2009–10 budget used the Governor’s proposed budget as its base but deleted a number of the administration’s proposals “without prejudice.” These proposals were not considered in the accelerated adoption of the budget. Instead, it is the intent of the Legislature to consider the proposals as part of the normal legislative process. Among the key items for which the Legislature deferred action are:

- $744 million in lease–revenue bond funding for University of California (UC) and California State University (CSU) capital outlay projects.

- $290 million in lease–revenue bonds for CalFire capital projects (mainly fire stations).

- The Governor’s Emergency Response Initiative and a new surcharge on property insurance premiums statewide.

- $39 million (mainly bond funds) for various Delta–related projects and various changes for the State Water Project.

- $123 million in high–speed rail bond expenditures.

- Reorganization proposals, such as the decentralization of Cal Grant financial aid and expansion of the Office of the Chief Information Officer.

- $36 million for increased correctional officer overtime.

In addition, the budget package authorizes the administration to delay the release of the May Revision until after the special election.

Figure 3

2009‑10 Budget and Budget-Related Legislation |

Bill Number |

Chapter |

Author |

Subject |

SB 1xxx |

1 |

Ducheny |

2009‑10 Budget Act |

SB 2xxx |

2 |

Ducheny |

Changes to 2008‑09 Budget Act |

SB 4xxx |

12 |

Ducheny |

Education |

SB 6xxx |

13 |

Ducheny |

Human services |

SB 7xxx |

14 |

Ducheny |

Transportation |

SB 8xxx |

4 |

Ducheny |

General government |

SB 10xxx |

15 |

Ducheny |

Proposition 1E |

SB 14xxx |

16 |

Ducheny |

Prison facilities |

SB 15xxx |

17 |

Calderon |

Tax credits and sales factor |

SB 19xxx |

7 |

Ducheny |

Elections |

SB 20xxx |

3 |

Maldonado |

State Controller |

SB 3xx |

1 |

Florez |

Farm equipment and air quality |

SB 4xx |

2 |

Cogdill |

Design-build and public private partnerships |

SB 7xx |

4 |

Corbett |

Residential foreclosures |

SB 9xx |

7 |

Padilla |

Prevailing wage |

SB 10xx |

8 |

Oropeza |

Vehicle license fee (VLF) and rental cars |

SB 11xx |

9 |

Steinberg |

Judicial employment benefits |

SB 12xx |

10 |

Steinberg |

Court facilities financing |

SB 15xx |

11 |

Ashburn |

New home purchase credit |

SB 16xx |

12 |

Ashburn |

Horse racing |

SB 6 |

1 |

Maldonado |

Open primaries statutory changes |

SCA 4 |

2 |

Maldonado |

Open primaries proposition |

SCA 8 |

3 |

Maldonado |

Proposition 1F |

AB 3xxx |

18 |

Evans |

VLF, income tax, and sales tax increases |

AB 5xxx |

20 |

Evans |

Health |

AB 11xxx |

6 |

Evans |

Special election |

AB 12xxx |

8 |

Evans |

State lottery |

AB 13xxx |

9 |

Evans |

Cash management |

AB 15xxx |

10 |

Krekorian |

Tax credits and sales factor |

AB 16xxx |

5 |

Evans |

Federal fund trigger |

AB 17xxx |

11 |

Evans |

Proposition 1D |

ACA 1xxx |

1 |

Niello |

Proposition 1A |

ACA 2xxx |

2 |

Bass |

Proposition 1B |

AB 5xx |

3 |

Gaines |

Alternative work week |

AB 7xx |

5 |

Lieu |

Residential foreclosures |

AB 8xx |

6 |

Nestande |

California Environmental Quality Act |

Programmatic Features of the Package

Below, we provide more details on the February budget package, including the spending reductions and tax increases.

Proposition 98 K–14 Education

The February budget package includes major changes in Proposition 98 funding for 2008–09 and 2009–10. Figure 4 summarizes changes for K–12 education, the California Community Colleges, and other Proposition 98–supported agencies (including state special schools and the Division of Juvenile Facilities).

Figure 4

Proposition 98 Funding |

(In Millions) |

|

2008-09 |

|

2009-10 |

|

September

Budget Act |

Revised |

Change |

|

Enacteda |

Change From 2008-09 Revised |

K-12 education |

$51,620 |

$44,660 |

-$6,960 |

|

$48,315 |

$3,654 |

California Community Colleges |

6,359 |

5,972 |

-387 |

|

6,482 |

510 |

Other agencies |

106 |

106 |

— |

|

107 |

1 |

Totals |

$58,086 |

$50,738 |

-$7,347 |

|

$54,904 |

$4,165 |

General Fund |

$41,943 |

$35,036 |

-$6,907 |

|

$39,461 |

$4,426 |

Local property tax revenue |

16,143 |

15,703 |

-440 |

|

15,442 |

-260 |

K-12 funding per average daily attendance |

$8,719 |

$7,543b |

-$1,176 |

|

$8,185 |

$642 |

|

a Amounts do not include Proposition 98 backfill of lottery funds. |

b Reflects amount of per-pupil Proposition 98 funding. Adjusting for fund-source swaps and deferrals, programmatic per-pupil funding is $8,332. |

Budget Package Makes Considerable Reductions to 2008–09 Proposition 98 Spending…Continued deterioration of the state’s revenues has led to a decline in the Proposition 98 funding requirement (known as the minimum guarantee), allowing the state to reduce spending for K–14 education in the current year. The budget package spends at the revised estimate of the minimum guarantee—$50.7 billion, which is $7.3 billion less than the original 2008–09 Budget Act spending level (enacted in September 2008). As shown in Figure 4, the bulk of this midyear reduction ($7 billion) is borne by K–12 education.

…But Relies Heavily on Deferrals and Funding Swaps. Of the $7.3 billion reduction in current–year Proposition 98 spending, $2.4 billion represents a cut to K–14 programs (see Figure 5

below). The largest reductions, all affecting K–12 schools, are split between revenue limits and categorical programs—$944 million each. To achieve these savings, roughly 50 K–12 categorical programs are reduced by 15 percent. The remaining $5 billion in Proposition 98 adjustments (also shown in Figure 5) represent deferrals and funding swaps rather than ongoing reductions to K–14 programs. Specifically, the budget package defers $3.2 billion in K–14 payments to July 2009. Under this approach, schools and colleges continue to incur costs in the current fiscal year, but state payments will not be made until the next fiscal year. The budget also retires the state’s existing prior–year Proposition 98 settle–up obligations ($1.1 billion) and uses special funds to directly support the Home–to–School Transportation program ($619 million). Both of these changes provide K–12 schools with the same level of program funding but reduce 2008–09 Proposition 98 spending to the minimum guarantee.

2009–10 Budget Continues, Deepens K–12 Program Cuts. Proposition 98 funding increases by $4.2 billion from the revised 2008–09 level to the enacted 2009–10 level. As shown in Figure 5, however, the budget includes $4.6 billion to backfill for the one–time 2008–09 solutions. To accommodate this backfill, as well as fund $253 million in new growth and baseline adjustments, the 2009–10 budget package sustains the current–year programmatic cuts and makes $702 million in additional reductions to K–12 and child care programs. As in the current year, the bulk of the cuts are made through revenue limit reductions and across–the–board cuts to categorical programs ($268 million for each category). Compared to the original 2008–09 Budget Act, the cumulative 2009–10 reduction for the roughly 50 targeted categorical programs is 20 percent. The school district revenue limit deficit factor through 2009–10 (including foregone inflationary adjustments) is 13.1 percent. The budget also captures savings by eliminating the High Priority Schools Grant Program ($114 million) and making changes to child care provider reimbursement rates and family fees ($53 million).

Figure 5

February Proposition 98 Package |

(In Millions) |

|

|

September 2008‑09 Budget Act Spending |

$58,086 |

Programmatic Reductions |

|

Reduce base K-12 revenue limits |

-$944 |

Reduce most categorical programs across the board |

-944 |

Rescind K-14 cost-of-living adjustment |

-287 |

Other |

-210a |

Subtotal |

(-$2,384) |

2008‑09 Programmatic Spending Level |

$55,701 |

Other Adjustments in Proposition 98 Spending |

|

Defer certain K-14 payments |

-$3,244b |

Retire settle-up obligation |

-1,101 |

Use special funds for Home-to-School Transportation |

-619 |

Subtotal |

(-$4,963) |

2008‑09 Revised Proposition 98 Spending Level |

$50,738 |

Growth and baseline adjustments |

$253c |

Backfill 2008‑09 One-Time Solutions |

|

2008‑09 deferrals |

$3,244 |

Settle-up |

1,101 |

Home-to-School Transportation |

214 |

Other |

56 |

Subtotal |

($4,614) |

Other Budget Reductions |

|

Further reduce most categorical programs |

-$268 |

Further reduce K-12 revenue limits |

-268 |

Eliminate High Priority Schools program |

-114 |

Modify child care fee and rate policies |

-53 |

Subtotal |

(-$702) |

2009‑10 Proposition 98 Spending Level |

$54,904d |

Special funds for Home-to-School Transportation |

$408 |

2009‑10 Programmatic Spending Level |

$55,312 |

|

a Includes $160 million technical reduction to current-year funds expected to go unused. |

b Of these deferrals, $2.3 billion is from K-12 principal apportionment programs, $570 million is from K-3 class size reduction, and $340 million is from community college apportionments. |

c Adjustments include $185 million for 3 percent growth at California Community Colleges, $19 million for 1.2 percent growth in child care

programs, and savings of $111 million from an expected decline of 0.3 percent in K-12 average daily attendance. Total also includes $162 million in other baseline adjustments. |

d Excludes lottery backfill. With lottery backfill ($1.062 billion), Proposition 98 spending would be $55.966 billion. |

Budget Package Makes Significant Changes to Rules Governing Categorical Program Funds. In addition to the program reductions noted above, the budget package dramatically loosens restrictions on how school districts may use the bulk of their categorical program funds. While funding will continue to be distributed in the same manner as in previous years, districts will have full discretion to use this funding how they choose, beginning in the current year and continuing through 2012–13. For example, they may transfer funding originally intended for counselors and instead use it to purchase textbooks or transfer funding originally intended for professional development and use it to increase teacher salaries. This flexibility provision applies to about 40 (of the roughly 60) existing K–12 categorical programs and over one–third of K–12 categorical funding.

Other Spending Solutions

Outside of Proposition 98, the budget package generates $7 billion in spending–related savings by suspending cost–of–living adjustments (COLAs), using alternative funding sources outside of the General Fund, deferring some costs, and making targeted programmatic reductions.

No COLAs

Current estimates are that inflation growth will be minimal in 2009–10 (or perhaps even negative by some measures). The budget suspends COLAs that would otherwise be due to various programs. In total, these suspensions reduce General Fund costs by about $1.2 billion, as shown in Figure 6.

Figure 6

Budget Package Suspends Many Cost-of-Living Adjustments (COLAs)a |

(In Millions) |

Program |

COLA |

2008-09 and 2009-10

Savings |

SSI/SSP |

Pass-through of federal January 2009 |

$567 |

SSI/SSP |

June 2010 |

27 |

UC and CSU |

Inflation (per Governor's compact) |

299 |

State operations |

Operational expenses |

136 |

CalWORKs |

July 2009 |

79 |

Trial courts |

State Appropriations Limit adjustment |

33 |

Medi-Cal county administration |

July 2009 |

25 |

Total |

|

$1,166 |

|

a The budget also suspends COLAs for K-14 education programs within the Proposition 98 adjustments. |

Fund Shifts and Deferred Spending

Fund Shifts. The budget package uses about $1 billion in fund shifts to help balance the budget. The two largest such shifts—using Proposition 10 ($608 million) and Proposition 63 ($227 million) funds to benefit the General Fund—require voter approval and will appear on the special election ballot.

Deferred Spending. The budget also defers about $500 million in costs for expenses that the state will face in future years. For instance, the package redirects $200 million in tribal revenues to the General Fund that otherwise would have helped pay off prior transportation loans. The budget also defers $91 million in mandate reimbursements to local governments.

Program Spending Reductions

The budget package makes more than $4 billion in program spending reductions (outside of Proposition 98). As discussed later in this report, some of these reductions would be affected by the federal trigger.

Unspecified Corrections Reductions. The budget implements an unallocated 10 percent reduction ($180 million) to the Receiver’s medical services budget. In addition, the Governor vetoed $400 million from the California Department of Corrections and Rehabilitation (CDCR) budget. At this time, it is unknown how savings of this amount will be achieved.

Health Reductions. The budget eliminates certain optional Medi–Cal benefits, such as dental services, and reduces reimbursements to public hospitals—for combined General Fund savings of about $184 million in 2009–10. The budget also assumes $160 million in savings through regional center provider rate reductions and other measures that are being developed by the Department of Developmental Services in conjunction with stakeholders and other parties.

Social Services Reductions. The agreement reduces state In–Home Supportive Services (IHSS) participation in provider wages (currently $11.50 per hour) to $9.50. This results in savings of $74 million in 2009–10. (The budget agreement also eliminates state assistance with Medi–Cal co–payments for certain new IHSS recipients, for a savings of $4 million.) In the California Work Opportunity and Responsibility to Kids (CalWORKs) program and the Supplemental Security Income/State Supplementary Program (SSI/SSP), the package reduces grants (in addition to not providing COLAs). Specifically, the agreement reduces CalWORKs grants by 4 percent, resulting in annual saving of $147 million. The agreement reduces SSI/SSP grants by 2.3 percent, resulting in savings of $268 million.

Transportation. In order to avoid a funding shortfall in the Public Transportation Account, the budget package reduces current–year funding and suspends budget–year funding (through 2012–13) of the State Transit Assistance program. These actions achieve $460 million in General Fund savings in 2008–09 and 2009–10 combined.

Higher Education. The budget contains $232 million in unallocated reductions to the universities’ base budgets. The package, however, does not direct the use of about $300 million in new fee revenues that would be generated by the universities and available to offset programmatic effects of the reductions.

Employee Compensation. For many of the state’s bargaining units, the budget assumes the continued implementation of the Governor’s two–day per month furlough program. For units represented by Service Employees International Union Local 1000, the budget reflects savings similar to those that would be generated under recent agreements reached between the union and the administration—less than one–half of the savings per employee compared to the other units. (Approval of these agreements is pending before the Legislature.) In total, the budget package assumes $1.2 billion in savings in 2008–09 and 2009–10 combined.

Tax Changes

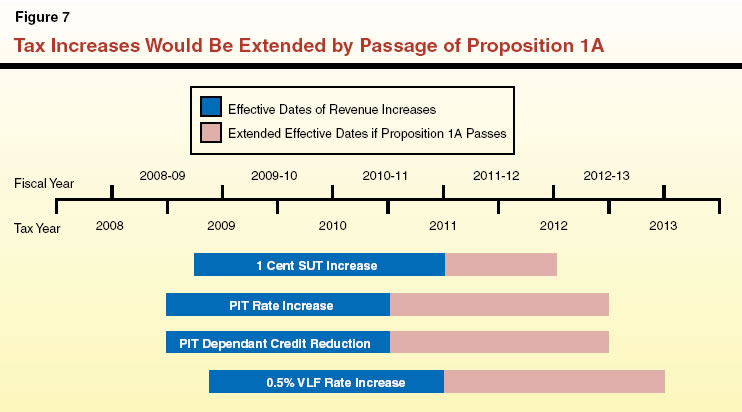

The budget package assumes an additional $12.5 billion in revenues over two fiscal years ($1.5 billion in 2008–09 and $11 billion in 2009–10) as a result of eight major changes to the state tax system. Four of the new provisions temporarily increase state taxes. The other new provisions reduce state taxes. These changes are described below, and their timing is summarized in Figure 7.

One Percent Sales Tax Increase. The budget package includes a one–cent increase in the state’s SUT. The increase will become effective April 1, 2009—raising the state rate to 6 percent and the average state and local rate to almost 9 percent. The duration of the tax depends on whether Proposition 1A passes. If the measure fails, the higher tax will lapse on July 1, 2011. If the measure passes, the tax increase will be extended for one year. The budget assumes $1.2 billion in additional sales tax revenues in 2008–09 and $4.6 billion in 2009–10.

PIT Rate Increase. A 0.25 percentage point increase in the PIT rate is the second major tax increase. The change increases each of the seven PIT tax rates by one–quarter of 1 percent. For example, the top PIT rate in 2008 for most taxpayers was 9.3 percent. With this increase, the top rate will now be 9.55 percent. Similarly, the lowest rate will increase from 1 percent to 1.25 percent. This change is subject to both budget triggers. If the federal funds trigger is reached, this PIT rate increase would be cut in half (resulting in a 0.125 percentage point rate increase to each marginal rate). If Proposition 1A gains voter approval, the PIT increase will end after tax year 2012. Otherwise, it will end after tax year 2010. The 0.25 increase is assumed to bring in $3.6 billion in additional revenues in 2009–10.

VLF Increase. The Legislature increased the VLF from 0.65 percent to 1.15 percent as part of the budget package. The VLF is essentially a personal property tax on cars and trucks. This change will become effective in May 2009 and is subject to the Proposition 1A trigger. If Proposition 1A passes, the higher tax rate sunsets on July 1, 2013. If it fails, the rate returns to the 0.65 percent level two years earlier on July 1, 2011. The budget assumes this increase will raise revenues by $346 million in 2008–09 and $1.7 billion in 2009–10. Revenues generated from about one–third of the increase (0.15 percent) would be dedicated to local government public safety grants (replacing General Fund spending).

Reduction in the Dependent Credit. The final tax increase is a reduction in the PIT dependent credit. The budget package reduces the dependent credit ($309 in 2008) to the same as the personal credit ($99 in 2008). This change is also subject to the Proposition 1A trigger—the credit would revert to the higher amount after tax year 2012 if the measure passes. If it fails, the higher credit will be reestablished after tax year 2010. The budget assumes the reduction in the dependent credit will increase revenues by $1.4 billion in 2009–10.

Tax Reductions Included in the 2009–10 Budget Package. The Legislature also enacted several measures that will reduce taxes for California taxpayers. Three of these measures temporarily reduce taxes during the next several years:

- Film Credit. A new tax credit for the film industry provides a tax credit for up to 25 percent of qualified expenditures of certain movies or television shows that are filmed in California. The credit is limited to $500 million in personal or corporate tax credits beginning in 2011–12 and ending in 2013–14.

- Hiring Credit. The budget package establishes a new employment credit in 2009 and 2010 for companies that increase net employment. They may receive a $3,000 credit for each additional employee. The credit is limited to $400 million over its life, and the budget assumes $345 million in lost revenues from this credit in 2008–09 and 2009–10 combined.

- New Home Purchase Credit. The budget package creates a credit for purchase of new homes equal to the lesser of $10,000 or 5 percent of the home’s purchase price, spread evenly over each of the next three tax years. The credit only applies to primary residences purchased between March 1, 2009 and March 1, 2010, and taxpayers will forfeit the entire amount of the credit if they do not occupy the home for at least two years. This credit is limited to a total of $100 million, and the budget assumes $33 million in lost revenues in 2009–10.

Finally, the Legislature enacted legislation that permanently gives multistate or multinational corporations another option for determining the proportion of profits that is subject to California’s corporate tax. Currently, companies must use a three–part formula that includes the proportion of total company sales, workforce, and property that are attributable to its California operations. The new legislation allows companies the option to use only sales to determine income attributable to California. This “single factor” option becomes effective for the 2011 tax year, and therefore, has no impact on revenues in 2008–09 or 2009–10. This change, however, is expected to reduce state revenues by hundreds of millions—or perhaps billions—of dollars annually beginning in 2011–12.

Budgetary Borrowing

The budget package relies on $5 billion in 2009–10 borrowing from future lottery profits. This borrowing will be allowed only if the state’s voters approve Proposition 1C at the special election. Lottery borrowing would involve selling bonds to investors, who would be paid back over 20 to 30 years. While the budget assumes that the state would borrow $5 billion, the proposition and related statutes do not limit the Legislature in the amount that could be borrowed in 2009–10 or future years. In addition, the budget borrows $328 million from various state special funds. The General Fund would generally need to repay these dollars over the next few years.

Federal Funds Trigger

As noted above, the budget package assumes $8.5 billion in General Fund solutions due to the receipt of federal economic stimulus funds. (This amount includes $510 million that the Governor vetoed from UC and CSU’s budgets in anticipation of using federal education dollars to backfill the reductions.) The budget package contains a trigger that would eliminate some cuts and a tax increase if the Director of Finance and State Treasurer determine that the state could receive at least $10 billion in federal offsets to General Fund spending by June 30, 2010. This determination must be made by April 1, 2009. Figure 8 shows the $948 million in spending reductions and a $1.8 billion tax increase (one–half of the PIT rate increase) contained within the budget package that would be reversed if the state reached this $10 billion amount in federal offsets. We discuss the receipt of federal funds in more detail in our recent publication, Federal Economic Stimulus Package: Fiscal Effect on California.

Figure 8

Solutions Included in the 2009‑10 Budget if the Federal Trigger Is Not Reached |

(In Millions) |

|

2009‑10 |

Expenditure Reductions |

|

Judicial Branch: One-time unallocated reduction to the trial courts |

$100.0 |

Judicial Branch: Eliminate100 new judgeships |

71.4 |

Medi-Cal: Eliminate certain optional benefits and cut public hospital reimbursement rates by 10 percent |

183.6 |

CalWORKs: Reduce grants by 4 percent |

146.9 |

SSI/SSP: Reduce grants by 2.3 percent |

267.8 |

IHSS: Cap state participation at $9.50 per hour and share-of-cost proposal |

78.0 |

Higher Education: Unallocated reduction |

100.0 |

Subtotal |

($947.7) |

Revenue Increase |

|

Personal Income Tax: Increase rates by 0.125 percentage point |

$1,829.0 |

Total Solutions |

$2,776.7 |

Use of the Ballot

The budget package includes six propositions that will appear on the May special election ballot:

- Proposition 1A makes changes to the state’s budgeting practices and requires the state to set aside more funds in a rainy day reserve fund under certain conditions.

- Proposition 1B provides $9.3 billion in supplemental payments to education in lieu of existing 2007–08 and 2008–09 Proposition 98 maintenance factor obligations that otherwise would be created. Its provisions would go into effect only if Proposition 1A also passes.

- Proposition 1C authorizes the borrowing of future lottery profits.

- Proposition 1D allows the redirection of Proposition 10 dollars for child development programs to benefit the General Fund through 2013–14.

- Proposition 1E allows the redirection of Proposition 63 mental health dollars to benefit the General Fund through 2010–11. Specifically, the Proposition 63 funds would be redirected to the Early and Periodic Screening and Diagnosis Treatment program in place of General Fund support.

- Proposition 1F would limit state elected officials from receiving pay raises in certain cases when the state ends the year with a budget deficit.

We discuss the effect of these measures, if approved, on the state budget over the next few years later in this report. In addition, the budget package includes a ballot measure that would create an open primary system for future elections. This measure will appear on the June 2010 statewide ballot.

Cash Management

Cash Deferrals. In addition to the education deferrals discussed above (which cross fiscal years), the Governor’s budget included numerous deferrals of payments (within a state fiscal year) to schools, local governments, and other entities in order to help the state manage its ongoing cash flow problems. The budget package enacts a series of deferrals that were based on these original proposals, but shortened the length of many of them. Figure 9 summarizes the cash deferrals included in the enacted package.

Figure 9

Additional Payment Deferrals

Contained in the February Budget Package |

2008-09 and 2009-10 |

|

K-14 Education |

Defer $2.7 billion of payments to schools from July and August 2009 to October 2009. |

Transportation |

Defer transfers of $300 million of gas tax revenues to counties and cities for local street and road

projects from February through April 2009 until May 2009. |

Medi-Cal |

Defer $874 million of various Medi-Cal payments from March 2009 to April 2009. |

Payments to Counties |

Defer $714 billion of various social services payments to counties from July and August 2009 until

September 2009. |

Defer $92 million of mental health cash advances to counties from July 2009 to September 2009. |

Developmental Services |

Defer $400 million of payments for regional centers from July and August 2009 to September 2009. |

Payments to Health Plans for State Retiree Health Benefits |

Defer $194 million of payments for state retiree health benefits from February and March 2009 to April 2009. |

Mandates |

Defer $142 million of local mandate reimbursements from August 2009 to October 2009. |

Federal Government |

Defer $517 million of payments to the federal government related to Supplemental Security Income/State Supplementary Program from February and March 2009 to April 2009. |

Revenue Anticipation Warrants (RAWs). In January, the Governor proposed to use $4.7 billion in RAW borrowing as a budget balancing tool. The enacted budget does not rely on RAWs to close the $40 billion shortfall. However, it is possible that the state will still issue RAWs in the coming months in their traditional role as a cash flow tool.

Economic Stimulus

In addition to some of the tax reduction measures discussed earlier, the package includes several statutory measures intended to improve economic conditions and speed up construction of certain projects. For instance, the package creates a 90–day moratorium on home foreclosures in certain cases. The package also provides exemptions from the California Environmental Quality Act for some projects. The use of design–build and public private partnerships for the construction of state and local government projects is expanded. The package also includes statutory changes to expedite the construction of new state prisons.

Implications of the Package on the State’s Budget Crisis

We have updated our economic and revenue forecast based on data and information made available since the Governor’s budget was released. In addition, we have updated our forecast of spending over the next five years based on the decisions made in the February package. Below, we discuss the implications of these new projections and the May special election on the state’s fiscal outlook.

Impressive Progress on Balancing the 2009–10 Budget

The Legislature and Governor’s February budget agreement was an impressive effort to tackle a monumental $40 billion shortfall. Among its positive attributes:

- Early Action. By taking action in February on the 2009–10 budget, the package captures billions of dollars in savings in the current year. In addition, the early enactment allows solutions to be implemented now so that full–year savings can be generated in 2009–10.

- Balanced Approach. The budget uses both sides of the ledger—revenue increases and spending reductions—to attack the state’s fiscal woes.

- Minimal New Borrowing. The 2008–09 budget enacted in September 2008 already had laid the groundwork for the $5 billion in borrowing from future lottery profits. Other than the addition of a few hundred million dollars in special fund borrowing, the February package resisted a major expansion of the state’s budgetary borrowing (such as the Governor’s RAW proposal).

Risks Within the Package. Despite the impressive progress that the package makes in bringing the state’s finances back into balance, it is not without its risks. The two largest risks of not achieving the intended solutions are:

- Ballot. The package relies on the state’s voters providing authority for nearly $6 billion in 2009–10 solutions. If the measures related to the lottery, Proposition 10, and Proposition 63 are defeated, the state will need to quickly develop alternatives.

- Corrections Savings. As described above, the budget relies on almost $600 million in unspecified CDCR savings from reducing the Receiver’s budget and the Governor’s veto. In both cases, no programmatic changes were made to accompany the reductions. Consequently, achieving these savings will require additional actions by the Legislature and the administration.

Economic and Revenue Outlook

Below, we discuss our updated economic and revenue forecast.

Economic Forecast

National Recession. The outlook for the national economy remains grim. Virtually all indicators of economic activity are negative. The revised gross domestic product (GDP) in the fourth quarter of 2008 fell more than 6 percent. Large–scale layoffs have continued in 2009. Foreign trade has slowed markedly, weakening the strongest sector of the national economy over the past year. The federal government continues to grapple with the near collapse of the nation’s financial and credit markets.

California’s Economy. The economic situation in California is similar. Consumer spending continues a downward trend. Car sales in the fourth quarter of 2008 were almost 40 percent below levels reached a year earlier. Unemployment rates have risen unusually quick, increasing from 8 percent in October 2008 to 10.1 percent in January 2009. Housing prices continue to decline, but sales have increased—providing a glimmer of hope that the housing market might begin to stabilize in the coming months.

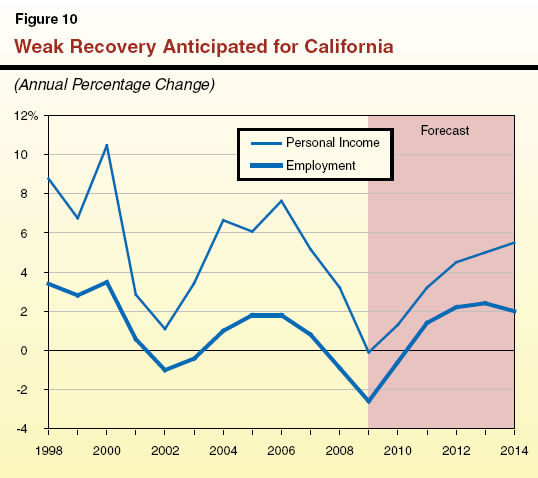

Delayed Recovery— Slow Long–Term Growth. Our current economic forecast projects a recovery beginning in the first quarter of 2010. Over the next five years, however, our forecast projects relatively slow growth compared to past recoveries. In our view, weakness in the finance, housing, and export markets are likely to keep the national economy from expanding at rates that typically occur after a recession. While our forecast is similar to the economic outlook shared by many economists, some see recovery taking even more time.

Figure 10 summarizes our revised forecast for two key economic variables for California—growth in personal income and employment. We project that:

- Personal income growth will remain stagnant in 2009. Growth resumes in 2010 but at a very sluggish pace. Stronger growth is projected beginning in 2011, but at rates under 6 percent (levels typically experienced after a recession) for the next five years.

- Employment will fall in 2009 and 2010. Beginning in 2011, employment is projected to be subdued and increase by about 2 percent a year.

Revenue Projections

The weakening economic outlook has taken its toll on projections of state revenues. In the few weeks since the Governor signed the budget package, the following negative developments have occurred:

- The state’s unemployment rate rose from 8.7 percent in December to 10.1 percent in January. The national unemployment rate rose from 7.6 percent to 8.1 percent in February.

- The federal government reported that GDP for the fourth quarter of 2008 fell at a 6.2 percent annual rate, worse than the previous estimate of a 3.8 percent drop.

- Receipts for the state’s big three taxes (PIT, SUT, and corporate income tax) were collectively $815 million below the forecast for February.

- The stock market has continued to slide.

2009–10 Revenues Down Significantly. Our current forecast projects a similar level of General Fund revenues in 2008–09 as the enacted budget package. In 2009–10, however, our forecast is nearly $8 billion lower—reflecting the recent negative news and the expectation of a likely delay in the state’s recovery. Our forecast projects a year–over–year increase of only about $530 million. This small increase masks a significant drop in revenues which is offset by the additional $10 billion in new revenues that result from recently enacted tax increases. Figure 11 compares our forecast to the one assumed with the budget package (based on the Governor’s budget estimates).

Figure 11

Estimated Revenues: Comparison

Between Budget Package and LAO |

(In Millions) |

|

2008-09 |

2009-10 |

Budget package |

$89,372 |

$97,729 |

LAO |

89,358 |

89,892 |

Difference |

-$14 |

-$7,837 |

Longer–Term Outlook. After falling significantly in the current and budget years, our baseline revenue projections (that is, excluding the effects of the enacted tax changes) grow modestly in 2010–11 and 2011–12. As a result, our baseline revenue forecast for 2013–14 is more than $5 billion lower than our prior forecast in November—reflecting the generally weak long–term growth of the economy expected over the next five years.

Budget Will Need Work to Get Back Into Balance

Outlook for 2009–10

Spending Outlook. On the spending side of our forecast, we have some estimating differences with those included within the February package. On net, however, our projections of spending for 2008–09 and 2009–10 are similar to those of the enacted budget. For the purposes of our forecast, we assumed that the federal funds trigger level would not be reached. Consequently, our forecast includes the savings from the $948 million in spending reductions (and the $1.8 billion in additional revenues).

Shortfall of $6 Billion if No Further Action. The nearly $8 billion drop in 2009–10 revenues discussed above is the single most significant factor in our revised projections in the near term. As a result of this revenue drop, we project that the state would end the 2009–10 fiscal year with a $6 billion deficit if no further corrective actions are taken (that is, the $8 billion revenue drop less the assumed $2 billion reserve). Whereas under the budget’s assumptions, the state has a $5.5 billion operating surplus, the state would have nearly a $2.5 billion operating shortfall under our forecast.

Long–Term Outlook Remains Grim

Factors Limit Progress on Closing Future Shortfalls. There are a number of factors that would limit the state’s progress in closing future shortfalls. For example, many of the solutions contained within the budget package are onetime or short term in nature. Among the key factors:

- Employee compensation savings would generally end after 2009–10.

- No additional borrowing of lottery profits is assumed after the initial $5 billion.

- Federal funds available to offset General Fund costs will drop significantly after 2009–10.

In addition, the state’s recovery from the recession is expected to be relatively slow and modest—reducing the opportunity to grow out of the state’s chronic operating shortfalls. Finally, the tax package is of a limited duration. Even if Proposition 1A is approved, the tax increases would begin to phase out after three years. Moreover, the single sales factor change affecting corporations described above would significantly reduce state revenues beginning in 2010–11.

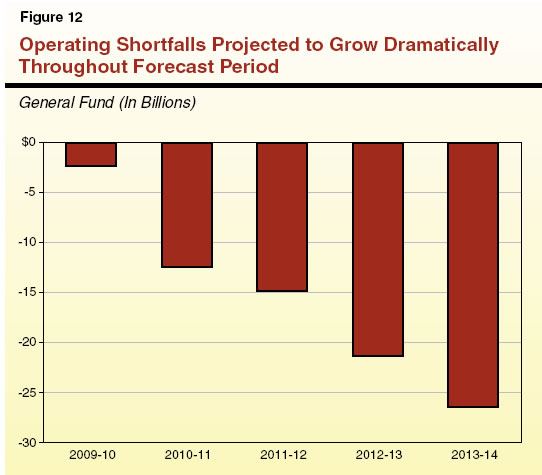

Shortfalls of at Least $12 Billion Beginning in 2010–11. Under our updated estimates of the policies contained within the budget package (including passage of the ballot measures), we project that the state would face huge operating shortfalls from 2010–11 through 2013–14. Specifically, in 2010–11, we project that the state would face a shortfall of $12.6 billion. As shown in Figure 12, that shortfall would grow consistently in the following years—all the way to $26 billion by 2013–14. Given these budgetary pressures, the state could experience recurring cash flow pressures in the coming months and years. This would particularly be the case if credit markets remain strained and restrict the state’s access to borrowing for cash flow purposes.

Effect of the Special Election On the Budget Outlook

The six measures that will appear on the May special election ballot have major implications for the state’s budget outlook in 2009–10 and in future years. In the materials that we prepared for the state voter information guide on the election, we provided our initial assessment of these measures’ fiscal effects. Below, we discuss their effect relative to our new five–year forecast. The fiscal effects of some of the measures—particularly Proposition 1A and Proposition 1B—are sensitive to changes in the state’s fiscal position. Their fiscal effect, therefore, could change significantly over time. Figure 13 summarizes the effects of all six measures through 2013–14 under our forecast.

Figure 13

Summary of Budget-Related Propositions Under LAO March Forecasta |

|

|

Effect on State General Fund Budgets |

Proposition |

Topic |

2009‑10 |

Through 2013-14 |

1A |

"Rainy day" reserve

fund |

Not significant |

Higher tax revenues of $15 billion through 2012‑13. Transfers to reserve assumed to be accessed by the General Fund. |

1B |

Supplemental payments for education |

None |

Higher annual costs of about $800 million by 2013-14. |

1C |

State Lottery |

$5 billion in benefit from borrowing from future

lottery profits |

Net increased costs of about $400 million

annually. |

1D |

Early childhood development program funds |

Up to $608 million in

savings |

$268 million annually in savings from 2010‑11 through 2013‑14. |

1E |

Mental health program funds |

About $230 million in

savings |

About $230 million in savings in 2010‑11. |

1F |

State elected officials' salary increases |

Potential minor reduction in costs |

Potential minor reduction in costs in some years. |

|

a In some cases, amounts differ from those included in voter information guide for the special election. Those estimates were based on earlier forecasts. |

Proposition 1A. Proposition 1A’s fiscal effect over the next few years is the most uncertain of the six measures. Its specific effect would depend in large part on the decisions that the Legislature makes in balancing the large projected shortfalls in subsequent budgets. For instance, Proposition 1A restricts the withdrawal of funds from the Budget Stabilization Fund (BSF) in years when available revenues exceed the prior–year’s spending grown for inflation and population. Consequently, the level of spending approved in one year will affect Proposition 1A’s mechanics for the next year.

- Base Transfer. We have assumed that the Governor suspends the base transfer into the BSF in each year (as has been the case in recent years). While Proposition 1A makes this suspension more difficult than under current law, we have assumed—given the state’s budget shortfalls—that the state would meet the criteria for such suspensions. Under the provisions of Proposition 1A, however, one–half of the transfers could not be suspended (as the funds would go to the supplemental education payments required under Proposition 1B).

- Ten–Year Revenue Trend. In addition, transfers would be made to the BSF based on amounts over the ten–year revenue trend. These transfers could not be suspended. Our best estimates based on our current revenue forecast is that this provision could become a factor in transferring funds to the BSF beginning in 2012–13. In particular, in 2013–14, the provision could require the transfer of billions of dollars to the BSF. As noted above, whether these funds could be transferred back to the General Fund to help balance the budget would depend on several factors. Our estimates assume that the full amounts could be transferred back to the General Fund in the same year that they are made. In contrast, if the provisions of Proposition 1A restricted the use of any funds in a particular year, that year’s shortfall would be larger than under our projections.

- Extension of Tax Increases. If Proposition 1A passes, the rate increases adopted for the sales tax, VLF, and PIT would be extended by one to two years. These tax extensions would add a total of about $15 billion in revenues over our forecast period—with more than $10 billion of this amount in 2011–12.

Proposition 1B. Proposition 1B would eliminate any maintenance factor created in 2007–08 and 2008–09 under Proposition 98 and replace them with $9.3 billion in supplemental payments to be made beginning in 2011–12. Our forecast includes the first $4.4 billion of these payments by 2013–14. As described in our voter guide analysis, the fiscal effect of Proposition 1B depends in part upon one’s baseline—how one reads the current provisions of Proposition 98. In our forecast and under our interpretation of current constitutional language, Proposition 1B (in conjunction with the passage of Proposition 1A) would result in K–14 education spending in 2013–14 that is about $800 million higher than would otherwise be the case.

Proposition 1C. Our forecast assumes that the state successfully sells $5 billion in lottery bonds in 2009–10. In subsequent years, however, the debt–service payments on these bonds would cost the state about $400 million annually.

Proposition 1D. By allowing the redirection of Proposition 10 funds, Proposition 1D would result in General Fund savings of about $600 million in 2009–10 and $268 million annually through 2013–14.

Proposition 1E. By allowing the redirection of Proposition 63 funds, Proposition 1E would generate a reduction in General Fund costs of about $230 million in each of 2009–10 and 2010–11.

Proposition 1F. If elected official salaries end up being lower under Proposition 1F than under current law, the state would generate minor savings.

Closing the Additional Budget Gap

In approving the budget in February, the Legislature and the Governor closed a huge budget gap. Unfortunately, the state’s revenues continue to fall. As a first step to closing the additional gap that we identify, we recommend that the Legislature ensure that the state is maximizing the use of available federal funds. It will also need to use the spring to develop additional savings proposals.

Optimize Use of Federal Funds

As we laid out in our report on the federal economic stimulus funds (see page FED–14), the state’s flexibility to use federal education dollars increases as the state’s Proposition 98 minimum guarantee falls. Under our current projections, the minimum guarantee in 2009–10 will fall $3.6 billion below the level in the enacted budget. The state could reduce state spending by roughly this amount (spending must remain above the state’s 2005–06 level of spending) by swapping out currently budgeted General Fund dollars for federal funds. While the specific amounts will depend on revised estimates developed in May, we recommend that the Legislature take this general approach for the Proposition 98 budget. This will generate roughly $3 billion in new budgetary solutions (the enacted budget had already counted on $510 million of offset) while preserving education programs at the level envisioned in the February package (as opposed to requiring additional reductions). By far, we believe this is the most significant step that the Legislature can take to optimize its use of federal funds in the context of this year’s state budget. Some others are discussed in our recent report on the federal economic stimulus package. As the state learns more about federal guidelines and requirements, there will likely be additional opportunities for General Fund savings in other program areas.

While seeking to offset 2009–10 General Fund costs is the most immediate concern, the large budget shortfalls on the horizon require a strategic multiyear approach regarding the expenditure of the federal funds. The Legislature should seek to preserve as many federal dollars as possible to help balance the budget in future years—as opposed to committing them now for augmentations.

Continuing Work on More Solutions

The February budget package contained some of the most significant program reductions (particularly those tied to the federal funds trigger) that the state has implemented in recent years. Unfortunately, the further deterioration of the revenue outlook and the massive shortfalls on the horizon signal that the state’s work is not done in this area. In January and early February, our office released a series of recommendations in our 2009–10 Budget Analysis Series. A number of these recommendations (or similar proposals) were contained within the enacted budget package. We believe the remaining recommendations would be a good starting point for the Legislature to begin developing additional solutions. Our General Fund recommendations which remain viable are summarized in the Appendix and discussed below. In some cases, these recommendations will not generate immediate savings. Given the huge future shortfalls that we project over the next few years, the Legislature should actively pursue broad–based programmatic changes even if they take several years to generate any savings.

Proposition 98. In January, we laid out a series of options in case the minimum guarantee dropped further than initially anticipated. Adopting any of these options could allow the state to preserve more federal economic stimulus funds to help balance future budgets. In particular, our recommendation to begin raising community college fees makes even more sense than a few months ago. Recent changes to federal tax credits means that higher community college fees would allow the state to tap hundreds of millions of new federal dollars without a significant financial effect on students. In addition, undertaking reform of education mandates would reduce long–term liabilities and streamline state requirements.

Other Spending Programs. Many other recommendations that we made over the past few months to reduce spending remain viable. Some of the larger dollar savings would come from making further changes to health and social services programs and implementing a package of prison and parole changes.

Tax Gap and Tax Expenditures. The significant tax increases that the Legislature adopted in February make our office extremely reluctant to recommend that the state raise any more tax rates. Yet, the opportunity still exists to make targeted changes in tax expenditures. In addition, the Legislature can implement a number of administrative changes at the state’s tax agencies that would generate additional revenues.

Conclusion

The state’s declining revenue outlook means that the Legislature’s work on the 2009–10 budget is not yet done. By using the spring budget process to ensure that the state maximizes its use of federal funds for budgetary relief and to develop new programmatic solutions, the Legislature will be in the best possible position to pass amendments to the enacted 2009–10 budget to bring it back into balance.

Appendix

2009-10 Budget Analysis Series: Summary of LAO Recommendationsa |

|

(In Millions) |

|

Page |

Department/Program |

Recommendation |

Savings |

|

CJ-24 |

Corrections and

Rehabilitation |

Adopt alternative package of correctional population reduction proposals (savings level assumed implementation by March 1, 2009). |

$400 |

|

CJ-27 |

Judicial Branch |

Implement electronic court reporting. |

13 |

|

CJ-27 |

Judicial Branch |

Utilize competitive bidding for court security. |

20 |

|

CJ-28 |

Justice |

Require state and local agencies to pay for laboratory services. |

— |

|

CJ-29 |

Corrections and

Rehabilitation |

Use existing available funds from AB 900 to support certain capital outlay projects. |

16 |

|

CJ-30 |

Corrections and

Rehabilitation |

Reject proposal to increase funding for correctional officer overtime. |

—b |

|

CJ-35 |

Corrections and

Rehabilitation |

Increase federal Workforce Investment Act funding for parolee employment programs. (Additional savings possible using newly available federal stimulus funding.) |

7 |

|

CJ-37 |

Justice |

Reject proposal to fund additional positions in Correctional Writs and Appeals section. |

—b |

|

ED-14 |

K-14 Education |

Achieve savings based on updated revenue forecast while adhering to parameters of the federal Fiscal Stabilization Fund. |

3,466 |

|

ED-27

ED-31 |

K-14 Education |

Consolidate 42 K-12 programs into three block grants. Consolidate eight California Community Colleges (CCC) programs into two block grants. |

— |

|

ED-36 |

K-14 Education |

Eliminate six of costliest K-12 mandates. Eliminate three of costliest CCC mandates. |

— |

|

ED-51 |

K-14 Education |

Create one state cash disbursement system that is aligned with district expenditures. |

— |

|

GG-8 |

Employee

Compensation |

Reject bargaining agreements that secure cost savings now in

exchange for substantial cost increases later. |

— |

|

GG-12 |

Tax agencies |

Adjust various administrative changes, additional penalties and interest charges for noncompliance, user fees, and conform selective provisions of state law to federal law (net increased revenues). |

81 |

|

GG-18 |

Franchise Tax Board (FTB) |

Postpone Enterprise Data to Revenue project, but (1) approve resources to process backlog and (2) direct FTB to use existing electronically filed tax return schedules to increase tax revenues. |

24 |

|

GG-23 |

Military |

Reject funding for new Tuition Assistance Program for California National Guard. |

—b |

|

GG-23 |

California Emergency

Management Agency |

Reject preliminary plans for construction of replacement facility for the Southern Region Emergency Operations Center. |

—b |

|

GG-24 |

Military |

Fund eight staff for mental health services with Proposition 63. |

—b |

|

GG-24 |

Secretary of State |

Recommend funding state's share of costs of 2009 special election. |

N/A |

|

GG-41 |

Gambling Control

Commission |

Reform Special Distribution Fund local grants to target scarce resources better and

protect the General Fund. |

— |

|

Page |

Department/Program |

Recommendation |

Savings |

HE-22 |

Health Care

Services (DHCS) |

Restructure skilled nursing home waiver agreement to include Medicare revenue. |

$26 |

HE-22 |

DHCS |

Create a more effective enforcement mechanism to collect overdue quality assurance fees from nursing homes. |

10 |

HE-24 |

DHCS |

Implement pilot program to evaluate the savings and service benefits of contracting with a broker for Medi-Cal nonemergency medical transportation. |

— |

HE-25 |

Public Health |

Adopt cost-cutting measures for AIDS Drug Assistance Program. |

— |

HE-26 |

Public Health |

Modify Proposition 99 accounts to increase flexibility. |

— |

HE-30 |

Developmental Services |

Clearly define "cost-effective" services. |

5 |

HE-32 |

Developmental

Services |

Implement regulations to govern regional center expenditures. |

— |

HE-34 |

Mental Health |

Adjust state hospital caseload. |

— |

HED-20 |

University of

California (UC) |

Reject targeted enrollment increase for nursing. |

—b |

HED-20 |

UC |

Reject targeted enrollment increase for PRIME. |

—b |

HED-20 |

California State

University |

Reject targeted enrollment increases for nursing. |

—b |

HED-20 |

Higher Education

Segments |

Provide enrollment guidance for next academic year. |

— |

HED-41 |

CSAC |

Decentralize California Student Aid Commission (CSAC) Cal Grant award process. |

— |

HED-44 |

CSAC |

Convert CSAC to department in executive branch. |

— |

HED-46 |

CPEC |

Reject consolidation of California Postsecondary Education Commission (CPEC) into executive branch. |

— |

RES-18 |

Conservation Corps |

Adopt Governor's proposal to eliminate Corps, but deny proposed grant program. |

22 |

RES-19 |

CalFire |

Enact new wildland fire protection fee. |

Unspecified |

RES-20 |

Fish and Game |

Increase regulatory fees. |

3 |

RES-21 |

State Water Board |

Increase regulatory fees, including expanding fee base. |

29 |

RES-22 |

Water Resources |

Increase watermaster fees. |

1 |

RES-22 |

OEHHA |

Fund regulatory support activities from fees. |

5 |

RES-24 |

CalFire |

Adopt various General Fund program reductions and expenditure deferrals. |

34 |

RES-43 |

Water Resources |

Reduce CALFED General Fund base budget. |

6 |

REV-25 |

PIT—Senior credit |

Eliminate the extra personal income tax (PIT) credit provided to those 65 and older. |

190 |

REV-25 |

PIT—Employer

contribution for

life insurance |

Eliminate the exclusion of life insurance benefits from taxable income. |

100 |

Page |

Department/Program |

Recommendation |

Savings |

|

REV-26 |

PIT—Employer-provided parking |

Eliminate the exclusion of subsidized parking benefits from taxable income. |

$100 |

|

REV-26 |

PIT—Small business stock exclusion |

Eliminate the exclusion from taxable income of profits on certain sales of small business stock. |

20 |

|

REV-26 |

PIT and Corporate—

"Like kind" exchanges |

Eliminate the exclusion from taxable income of profits from trading properties. |

350 |

|

REV-27 |

PIT and Corporate—Enterprise zone subsidies |

Cancel zones authorized in 2006 and phase out other zones as their designations expire. |

100 |

|

REV-27 |

Sales—Animal life, feed, and seeds |

Eliminate the exclusion for animal feed; seeds, plants, and fertilizers; drugs and

medicines administered to animals; and medicated feed and drinking water. |

465 |

|

REV-27 |

Sales—Industry-specific equipment |

Eliminate the exclusion for timber harvesting, farming, and post-production equipment for television and films. |

145 |

|

REV-28 |

Sales—Doctor and

veterinarian sales |

Eliminate the partial exclusion for glasses, contact lenses, drugs and medicines used by veterinarians, and other medical specialty items. |

80 |

|

REV-28 |

Sales—Other

exemptions |

Eliminate the exemption for diesel fuel, custom computer programs, and leasing of films and tapes. |

140 |

|

SS-16 |

Social Services |

Pay counties to move certain state-only Cash Assistance Program for Immigrants (CAPI) recipients to federally funded Supplemental Security Income/State Supplementary Program (SSI/SSP). |

17 |

|

SS-16 |

Social Services |

Eliminate SSP restaurant meals allowance. |

35 |

|

SS-16 |

Social Services |

Eliminate CAPI prospectively. |

20 |

|

SS-19 |

Social Services |

Reduce In-Home Supportive Services (IHSS) share of cost (SOC) buyouts by 50 percent. |

28 |

|

SS-19 |

Social Services |

Cap IHSS SOC buyouts at determined level. |

13 |

|

SS-20 |

Social Services |

Adjust tiered reduction in IHSS domestic care hours. |

36 |

|

SS-27 |

Social Services |

Conduct self-sufficiency reviews and impose community service work requirement for "safety net" parents for CalWORKs (LAO version). |

57 |

|

SS-29 |

Social Services |

Create new kinship guardianship program in order to draw down more federal funds. |

31 |

|

SS-31 |

Social Services |

Increase fees and gradually increase investigation efforts in community care licensing. |

4 |

|

SS-32 |

Social Services |

Suspend "hold harmless" budgeting methodology for child welfare services. |

10 |

|

SS-37 |

Child Support Services |

Create matching program for local child support agencies. |

4 |

|

SS-39 |

Social Services |

Adopt various reforms to the Adoptions Assistance Program. |

2 |

|

SS-40 |

Social Services |

Increase oversight and accountability in IHSS by reforming time card practices. |

— |

|

|

|

a Assumes that cuts and tax increase tied to federal trigger remain in effect. |

|

b "Without prejudice" issue. Savings from the recommendation already assumed in the budget package. |

|

|

Acknowledgments

This report was written by

Michael Cohen with assistance from the entire office. The Legislative Analyst's Office (LAO) is a nonpartisan

office which provides fiscal and policy information and advice to the Legislature.

|

LAO Publications

To request publications call (916) 445-4656. This report and others, as well as

an E-mail subscription service, are

available on the LAO's Internet site at www.lao.ca.gov. The LAO is located at 925

L Street, Suite 1000, Sacramento, CA 95814.

|

Return to LAO Home Page