Total state funding for general government is proposed to increase by almost 4 percent in the budget year. This increase is the net amount from a number of factors, including both one–time costs and savings in 2007–08, various budget savings proposals for

2008‑09, and some rising expenditures. The “General Government” section of the budget contains a number of programs and departments with a wide range of responsibilities and functions. For instance, these programs and departments provide financial assistance to local governments, regulate businesses, provide services to state agencies, enforce fair employment practices, and collect revenue to fund state operations. The 2008‑09 Governor’s Budget proposes $8.4 billion in state expenditures (combined General Fund and special funds) for these functions. The proposed budget–year funding is $295 million (3.6 percent) more than proposed 2007–08 expenditures.

There are three major program areas within general government:

- State administrative functions, which include a broad range of state departments.

- Tax relief and local government payments.

State employee compensation and retirement, which includes increased salary and benefit costs for current and former employees.

We describe these program areas below, and Figure 1 shows the proposed 2007–08 and 2008‑09 expenditures by program area.

|

|

|

Figure 1

General Government Spending by Program Area |

|

(Dollars in Millions) |

|

Program |

Proposed

2007‑08 |

Proposed

2008‑09 |

Difference |

|

Amount |

Percent |

|

State administration |

$3,972 |

$4,061 |

$90 |

2.3% |

|

Tax relief/local governments |

1,010 |

1,114 |

104 |

10.3 |

|

State employee

compensation/retirementa |

3,153 |

3,254 |

101 |

3.2 |

|

Totals |

$8,135 |

$8,430 |

$295 |

3.6% |

|

|

|

a Costs not reflected in

departments' budgets, such as payments for retirees’ health premiums. |

|

Detail may not total

due to rounding. |

|

|

Within general government, there are about 50 departments and agencies that serve a wide range of functions. Departments provide services to the public, regulate businesses, collect tax revenues, and serve other state entities.

Government Services. A number of departments provide government services to the public. These services include housing assistance, coordination of emergency responses, and assistance to veterans. In most cases, the Governor’s budget proposes to reduce these services as part of the administration’s across–the–board reductions. After accounting for some increasing costs, there is a slight decrease in funding for these departments compared to the amounts received in 2007–08.

Regulatory Activities. Many departments are responsible for providing regulatory oversight of various consumer and business activities. These agencies promote business development while regulating various aspects of licensee, business, and employment practices. The groups regulated range from individuals licensed to practice specified occupations to large corporations licensed to conduct business in the state. Most of these departments are funded from special funds that receive revenues from regulatory and license fees.

Tax Collection. The Franchise Tax Board (FTB) and the Board of Equalization (BOE) are the state’s two major revenue collection agencies. The FTB is responsible primarily for collection and administration of the state’s personal income tax and the corporation tax. In addition, it assists in the collection of various types of nontax delinquencies, including child support payments and vehicle–related assessments. The BOE is responsible primarily for administration and collection of the sales and use tax, as well as excise taxes on fuel, cigarettes, and alcoholic beverages. The budget proposes total funding of $875 million ($796 million General Fund) for these two agencies in 2008‑09, up $45 million (5 percent) from the current year. This increase is due principally to proposed augmentations to increase tax enforcement and collection activities. These augmentations are expected to increase General Fund revenues by about $150 million in 2008‑09.

Services to Other Departments. Some state departments exist primarily to provide support for other departments. For instance, the Department of General Services assists state departments on purchasing and real estate decisions. The Department of Finance acts as the state’s fiscal oversight agency. The administration proposes $40 million for additional development costs of the $1.6 billion Financial Information System for California (FI$Cal), a computer project intended to modernize the state’s budgeting and accounting systems. This proposal is reflected in a new budget item, Item 8880. The administration proposes to finance most of the project’s costs.

The state provides tax relief—both as subventions to local governments and as direct payments to eligible taxpayers—through a number of different programs. The major programs in this area are homeowners’ property tax relief, various tax assistance programs for senior citizens, and open space property tax subventions. The state also reimburses local governments for state–mandated costs. The Governor’s budget proposes to increase payments in this area from $1 billion to $1.1 billion. This reflects an increase in mandate payments due to the state’s prepayment of 2007–08 costs to retire its mandate backlog. Partially offsetting this increase are budgetary savings proposals to (1) delay $75 million in 2008‑09 mandate payments and (2) reduce most tax relief programs by 10 percent.

State Employee Compensation. The costs for compensating about 350,000 state government and university employees under existing pay and benefit schedules are included in each department’s budget. The Governor’s budget assumes that employee salaries total $23 billion (all funds) in 2008‑09. Including employer benefit expenses (principally retirement and health benefit contributions) and payroll taxes, the total cost of compensating these employees is about $30 billion. The Governor also proposes $615 million ($362 million General Fund) in the budget item that covers the costs of anticipated and proposed pay and benefit increases across all departments. Most of the General Fund amount consists of the estimated costs to impose the administration’s contract offer on the correctional officers’ union. Under the administration’s plan, the $230 million included for this purpose assumes that the Legislature also approves proposals to reduce the state’s prison population, thereby reducing personnel costs. Also included in the budget item are initial estimates of costs to provide pay and benefit increases to California Highway Patrol officers (whose current labor agreement expires in 2010) and professional engineers. The engineers’ current labor agreement expires on July 2, 2008, but includes a final pay increase effective on the first day of the 2008‑09 fiscal year. The state’s 19 other labor agreements with employee bargaining units already have expired or will expire on June 30, 2008. In general, the Governor’s budget includes no funds to increase pay and benefits for members of these 19 units or their supervisors and managers. Accordingly, if the Legislature approves any new labor agreements, additional 2008‑09 costs will have to be paid from the reserve.

Retirement Programs. The state contributes to the retirement benefits of:

- State and California State University employees—through the California Public Employees’ Retirement System (CalPERS).

- School and community college district teachers and administrators—through the California State Teachers’ Retirement System (CalSTRS).

Judges and other small groups of employees.

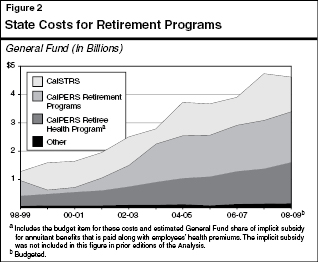

As shown in Figure 2, General Fund costs for these retirement programs (excluding payroll taxes for employees’ Social Security and Medicare benefits) spiked upward to $4.8 billion in the current year—an increase of 23 percent—due largely to a one–time, court–ordered payment to CalSTRS of $500 million described below. The Governor’s budget assumes that General Fund retirement costs total $4.6 billion in 2008‑09. As shown in Figure 2, the state’s contributions to CalPERS’ retirement programs increased sharply in the early part of this decade due largely to declines in the stock market, which affected the investment portfolios of CalPERS’ pension funds. These contributions have stabilized recently due to (1) large recent years’ gains in the CalPERS’ investment portfolio, (2) CalPERS’ implementation of a policy to stabilize employer contribution rates, and (3) the stable benefit levels for current or past employees. Since 2004, the most consistent driver of increased retirement contributions (not including the costs related to the CalSTRS lawsuit) has been the state’s retiree health program. The Governor’s budget assumes that 2008‑09 will be the eleventh consecutive year of double–digit percentage growth in retiree health expenses. This rapid growth is caused by (1) increases in health premium costs established by CalPERS and (2) growth in the number of state retirees. Because the state pays retiree health costs on a “pay–as–you–go” basis (unlike pensions), there are no investment returns generated to cover a portion of these expenses.

CalSTRS Proposals. The Governor’s budget includes several proposals concerning CalSTRS. The state lost a court case in 2007–08 concerning a one–time reduction of payments to CalSTRS four years ago, and the court required the state to pay an unbudgeted $500 million to the system during the current year (pursuant to a continuous appropriation). The administration proposes that the Legislature appropriate funds over a three–year period (beginning with an $80 million payment in 2008‑09) to comply with payment orders of the court related to interest and legal costs. In addition, the administration proposes changing the inflation protection component of CalSTRS benefits to reduce current–law expenditures by $80 million in 2008‑09.

Return to General Government Table of Contents, 2008-09 Budget AnalysisReturn to Full Table of Contents, 2008-09 Budget Analysis