January 4, 2010

Pursuant to Elections

Code Section 9005, we have reviewed the proposed constitutional initiative

relating to state and local approval requirements for taxes, fees, and penalties

(A.G. File No. 09‑0089).

Background

Taxes

State Taxes.

The State Constitution

requires a two-thirds vote of each house of the Legislature for measures that

result in increases in revenues from imposing new state taxes or changing

existing state taxes. This has been interpreted to allow measures that do not

result in a net increase in state taxes to be adopted by majority vote. For

example, a measure that results in higher taxes for some taxpayers but an equal

(or larger) reduction in taxes levied on other taxpayers would not result in an

aggregate increase in taxes. Under current practice, this type of measure could

be passed by a majority vote.

Local Taxes. Local governments may impose or increase taxes (other than ad

valorem property taxes) subject to the approval of their local voters. If the

local government proposes to use the tax proceeds for general purposes (a

"general tax"), the tax requires approval by a majority of local voters. If the

tax proceeds are earmarked for a specific purpose (a "special tax"), the voter

approval threshold is two-thirds. In some cases, local governments place

nonbinding "companion measures" on the same ballot with proposed general tax

increases. These advisory measures express voter intent regarding the

expenditure of funds raised by the general tax.

Fees, Assessments, Fines, and Other Charges

Current law generally gives state and local

governments significant discretion in establishing fees, assessments, fines,

penalties, and other charges. Governments may impose these charges for many

reasons, including to offset their costs to provide specific services and

benefits ("user fees"), regulate a particular activity ("regulatory fees"),

penalize certain behaviors ("fines" and "penalties"), and finance property or

business improvements ("assessments").

In some cases—such as many user fees, admission fees, and

assessments—the charge is closely linked to the cost of providing a particular

service to an individual

beneficiary. In other cases—particularly regulatory fees (including

environmental mitigation)—the charge may be based on the costs of government

oversight of a group or industry, or on the social costs associated with

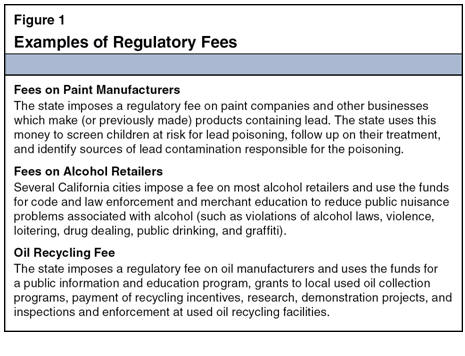

particular activities. Figure 1 provides some examples of fees imposed for broad

regulatory purposes.

Imposing Fees, Assessments, and Charges. By

a majority vote, the Legislature may impose fees, assessments, and charges—or

delegate this responsibility to state administrative agencies. State charges may

not exceed government's related costs. (State charges in excess of costs are

considered "taxes" and are subject to the Constitution's voter approval

requirements for taxes.) With three exceptions, local governments generally have

similar authority to impose fees, assessments, and charges. Specifically, state

law requires local governments to obtain the approval of business owners before

imposing assessments to finance improvements in business districts. In addition,

the Constitution requires local governments to receive approval from property

owners or voters before imposing (1) property owner assessments or (2) fees as

an incident of property ownership ("property-related fees"), other than fees for

water, sewer, and refuse collection services.

State and Local Requirements Regarding Fines and

Penalties. State and local governments have significant discretion to

set fines and penalties for violations of state laws and local ordinances and to

discourage certain behavior. The Constitution generally does not restrict how

state and local governments spend the funds raised from fines and penalties.

State and local governments may impose most fines and penalties with a majority

vote of the governing body. The Constitution does not limit state or local

governments' authority to impose fines administratively (that is, outside of an

adjudicatory or quasi-adjudicatory proceeding).

Proposal

This measure amends the Constitution to constrain state

and local government authority to impose taxes and fees.

State Taxes

The measure specifies that any change in a state statute

that results in any taxpayer paying a higher state tax requires (1) a

two-thirds vote of the Legislature and (2) majority approval by the statewide

electorate. (This would include statutes that do not impose a net increase in

revenues but only reallocate tax burdens.) The measure provides a waiver of the

voter-approval requirement in cases of emergency as long as the tax expires by

the next statewide election in the year after the emergency.

Local Taxes and Fees

The measure broadens the definition of a local special

tax to include: (1) any tax that is the subject of a companion measure advising

that its funds would be used for specific purposes, and (2) a wide range of

charges that local governments currently may impose by a majority vote of their

governing boards. Specifically, the measure defines as a special tax all local

fees or charges except:

-

User charges to reimburse a local government for its

costs in providing a product or service requested by the fee payer, which

the fee payer reasonably could have declined.

-

Fines and penalties imposed "for a violation of a law

in an adjudicatory or quasi-adjudicatory proceeding."

-

Charges imposed as a condition of property development.

-

Property-related fees.

State Fees

The measure constrains the Legislature's authority to

impose state fees, assessments, and charges. Specifically, the measure:

-

Requires the Legislature to approve any new or

increased fee—other than user fees—by a two-thirds vote.

-

Prohibits the Legislature from imposing a tax, fee, or

assessment on real property or the sale or transfer of real property.

(Currently, the Legislature is already prohibited from imposing ad valorem

or sales taxes on real property.)

-

Prohibits

the Legislature from imposing a fine or penalty except those imposed "for a

violation of a law in an adjudicatory or quasi-adjudicatory proceeding."

Fiscal Effects

By subjecting state tax increases (except those for

emergencies) to voter approval, expanding the scope of what is considered a

local special tax, and limiting state and local government authority to impose

fees and other charges, the measure would make it more difficult for state and

local governments to enact a wide range of measures that generate revenues.

State Government

The measure makes three significant changes to state

finance. First, the measure requires state statutes that increase or reallocate

state taxes to be approved by two-thirds of the Legislature and a majority of

the state's voters. Under current law, no statewide vote is required, and some

of these measures can be passed by a majority vote of the Legislature. The

measure also requires state statutes that increase or impose many fees—other

than user fees—to be approved by a two-thirds vote of the Legislature, rather

than the current legislative majority. Finally, the measure prohibits the

Legislature from enacting certain revenue measures, such as assessments on real

property and new fines levied outside of an adjudicatory or quasi-adjudicatory

proceeding.

The overall revenue impact of these changes would depend

on future actions of the Legislature and voters. By making it more difficult to

pass measures which increase revenues, it is likely that state revenues would be

lower in the future than they would be otherwise. Given that state tax and fee

measures frequently total hundreds of millions or billions of dollars, the

higher approval thresholds in the measure could result in major decreases in

state revenues and spending.

Local Government

Under the measure, many local revenue measures—including

local regulatory fees, general taxes that are accompanied by provisions

specifying how its proceeds would be used, and some fines—would be considered

special taxes. As a result, instead of being approved by a majority of local

governing boards, these charges also would require approval by two-thirds of

local residents.

The overall revenue impact of this measure would depend

on future actions of the local governing bodies and voters. By making it more

difficult to pass these revenue increases, it is likely that some local

governments would have less revenues in the future than they would otherwise.

Given the amount of revenues derived from these local charges, the higher

approval threshold in this measure could result in major decreases in local

revenues and spending. In some cases, local governments receive revenues from

taxes controlled by the state. By making it more difficult for the Legislature

to pass measures that increase taxes, local governments may receive lower

revenues from these sources.

Summary

The measure would have the following impacts on state and

local governments:

-

Potentially

major decrease in state and local revenues and spending in the future,

depending upon actions of the Legislature, local governing bodies, and

voters.

Return to Propositions

Return to Legislative Analyst's Office Home Page