- All Articles State Revenues

The 2024-25 Budget: Temporary Corporation Tax Increases May 17, 2024

The May Revision proposes to temporarily increase corporation tax revenues by limiting the use of business tax credits and net operating loss deductions. This post analyzes those proposals. We think the proposal to limit use of tax credits is worth serious consideration. On the other hand, the proposal to limit net operating loss deductions raises concerns. In response, we suggest the Legislature consider alternative ways to raise revenue should it wish to pursue revenue solutions.

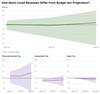

Updated "Big Three" Revenue Outlook May 2, 2024

Revenues Likely to Fall Below Governor’s Budget Assumptions. Our forecast continues to suggest there is significant downside risk to state revenues relative to the Governor’s Budget. Specifically, our forecast is $19 billion below the Governor’s Budget across the 2022-23 to 2024-25 budget window. That being said, there is still significant uncertainty about how much revenue the state ultimately will collect. It is entirely possible that revenues could end up $8 billion higher or lower than our estimate for 2023-24 and $20 billion higher or lower for 2024-25.

Evaluating Tax Policy Changes in the Governor's Budget February 22, 2024

The Governor’s budget includes several proposed tax policy changes. We recommend approving proposals to eliminate certain tax expenditures for fossil fuel companies and conform to federal law on tax deductions for open space and historical preservation. We also suggest, in light of the state’s fiscal situation, seriously considering the proposal to eliminate lenders’ ability to claim tax deductions or refunds for sales tax payments made with bad debt. Finally, we recommend rejecting the proposal to limit the use of net operating loss deductions.

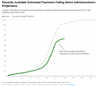

Recent Revenues Coming in Below Governor's Budget Projections January 22, 2024

In the first few weeks of January, real-time personal income tax (PIT) revenue collections are running $3 billion to $4 billion short of the January target for current year revenue projections included in the 2024-25 Governor's Budget.

How Does Tech Company Equity Pay Affect Income Tax Withholding? November 16, 2023

California's technology companies, including giants like Apple, Google, Nvidia, and Meta, are some of the most valuable companies in the world and support thousands of high-paying jobs in the state. Many employees at these companies receive equity pay, such as stock options, as part of their compensation. State income tax withholding on this equity pay has grown notably, reaching 6 percent in the last few years. The recent jump in these companies' stock prices, which affects withholding on equity pay, has bolstered otherwise weak income tax withholding during 2023.

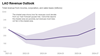

Updated 2022-23 "Big Three" Revenue Outlook March 15, 2023

Based on the most recent revenue and economic data, we currently estimate that collections from the state’s “big three” taxes—personal income, sales, and corporation taxes—are likely to fall below the Governor's Budget assumption of $200 billion in 2022-23.

October Tax Collections November 17, 2022

Although October colletions from the state's “big three” tax revenues—personal income, corporation, and sales taxes—came in far ahead of Budget Act assumptions, this is not indicative of better than expected revenue performance for 2022-23 overall. Instead, a closer look at the data shows that the recent trend of revenue weakness continued in October.

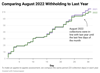

Income Tax Witholding Tracker: August 2022 September 1, 2022

August state income tax withholding was down $450 million (6.1 percent) compared to last year.

2021-22 “Big Three” Revenue Outlook Update: March 2022 March 28, 2022

Based on the most recent revenue and economic data, we currently project that there is a very good chance that collections from the state’s “big three” taxes will exceed the Governor's Budget assumption of $185 billion in 2021-22 by at least several billion dollars.

2021-22 “Big Three” Revenue Outlook Update: February 2022 February 17, 2022

Based on the most recent revenue and economic data, we currently project that there is a very good chance that collections from the state’s “big three” taxes will exceed the Governor's Budget assumption of $185 billion in 2021-22 by at least several billion dollars.

2021-22 “Big Three” Revenue Outlook Update: January 2022 January 21, 2022

Based on the most recent revenue and economic data, we currently project that there is a strong chance that collections from the state’s “big three” taxes will exceed the Governor's Budget assumption of $185 billion in 2021-22.

Income Tax Withholding Tracker: November 1 - November 30 November 30, 2021

California income tax withholding collections in November were up nearly a third over last November.

2022-23 Fiscal Outlook Revenue Estimates November 17, 2021

We discuss the revenue estimates in our recently released Fiscal Outlook.