Ballot Pages

A.G. File No. 2015-065

November 3, 2015

PDF Version

PDF VersionPursuant to Elections Code Section 9005, we have reviewed a proposed constitutional initiative concerning taxes (A.G. File No. 15-0065, Amendment No. 1). The proposal extends temporary personal income tax (income tax) rate increases on high-income taxpayers that were approved as part of Proposition 30 in 2012.

Background

California’s State Budget. California state taxes—primarily income taxes—are spent mainly from the state government’s General Fund. The General Fund is budgeted to spend about $115 billion during the current 2015-16 state fiscal year.

Proposition 30. Proposition 30 temporarily raised some state taxes.

- Sales Taxes. Proposition 30 increased the state sales tax rate by one-quarter cent from 2013 through 2016. In the current fiscal year, this increase is budgeted to generate $1.6 billion of revenue.

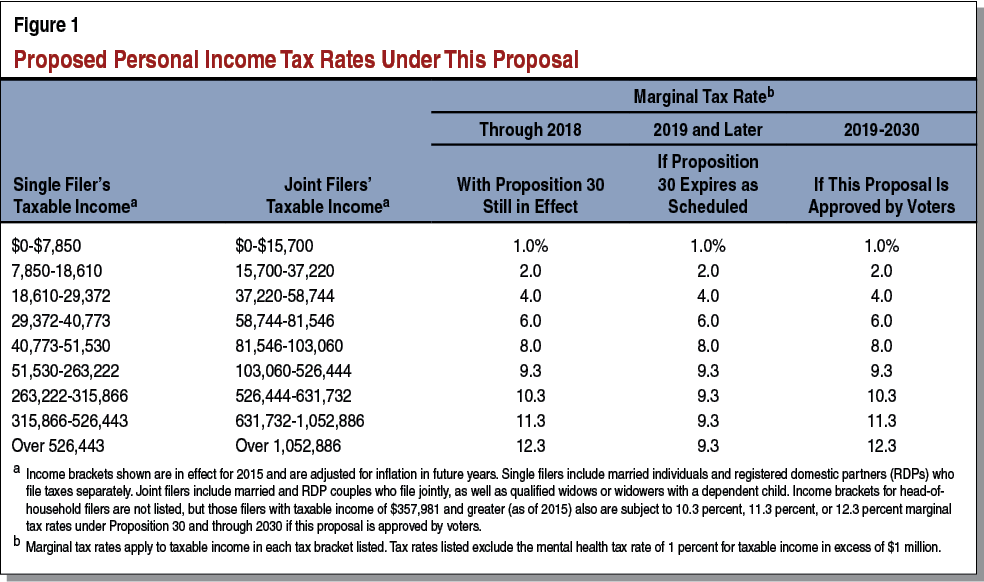

- Income Taxes. Proposition 30 also increased marginal income tax rates paid by roughly the 1 percent of tax filers in the state with the highest incomes. Depending on their taxable income levels, these filers pay an extra 1 percent, 2 percent, or 3 percent tax on part of their incomes. These increases are in effect from 2012 through 2018. In the current fiscal year, the Proposition 30 income tax increases are budgeted to generate $6.8 billion of revenue. (The actual total may be hundreds of millions of dollars or more above or below $6.8 billion.)

Proposition 98 and Other Programs. The largest category of state General Fund spending is for school districts and community colleges. Proposition 98, approved by voters in 1988 and modified in 1990, establishes a minimum funding level for schools and community colleges. This funding level tends to grow over time based on growth in the state’s economy, state tax revenue, and student attendance, among other factors. In the current fiscal year, the state budgeted $49 billion in General Fund Proposition 98 funding (over 40 percent of all General Fund revenues). In addition to this state funding, schools and community colleges will receive an estimated $19 billion from local property taxes.

The General Fund also pays for part of California’s health and human services programs, public universities, state prisons, statewide retirement systems for public employees, debt service on state infrastructure bonds, and other programs.

Recent Budgets and Proposition 2. High-income people pay a large share of California’s state taxes, and they receive a large portion of their taxable income from sources tied to the ups and downs of the stock market. California’s state budget has been volatile due mainly to large swings in income taxes paid by high-income people. These swings also have been linked to the ups and downs of the stock market.

In response to budget deficits resulting from this volatility, the state took various actions, including budget cuts, tax increases, and other measures. As a result of these actions and the improving economy, the General Fund has not ended a fiscal year with a deficit since 2011-12. In November 2014, California voters approved Proposition 2. Proposition 2 creates a new set of rules to determine the amount of money the state has to deposit to a rainy day fund (the Budget Stabilization Account) when the economy and stock market are doing well. This fund is intended to reduce the need for budget cuts, tax increases, and other measures in the future when the economy or stock market weakens. Proposition 2 also requires speeding up payment of certain state debts. In addition to Propositions 2, 30, and 98, the State Constitution includes other rules affecting the state budget, such as the state spending limit that has been in place since passage of Proposition 4 in 1979.

Proposal

Extends Proposition 30 Income Tax Increases Through 2030. Under this measure, the Proposition 30 income tax rate increases on high-income Californians would not expire at the end of 2018, as scheduled under current law. As summarized in Figure 1, this measure would extend those income tax rate increases through 2030.

Does Not Extend Proposition 30 Sales Tax Increase. Under this measure, Proposition 30’s sales tax rate increase would not be extended. This sales tax rate increase would expire at the end of 2016.

Excludes Revenues From Proposition 2, as Specified. This measure increases state revenues beginning in 2019 and ending in 2030. Revenues raised by this measure would be excluded from the key requirements of Proposition 2. Spending from the revenues raised by this measure, however, would be subject to the state’s spending limit.

Fiscal Effects

Increased State Tax Revenues. Currently, the Proposition 30 income tax rate increases are scheduled to expire at the end of 2018. This measure would increase state income tax revenues by billions of dollars per year above current expectations for the years 2019 through 2030. (This would result in increased tax revenues for fiscal years 2018-19 through 2030-31.) The precise amount of this revenue in any given year would depend heavily on trends in the stock market and the economy. For example, if the stock market and economy were weak in 2019 (the first year of the proposed tax increase extension), this measure might generate around $5 billion of increased revenue. Conversely, if the stock market and economy were strong at that time, the measure might raise around $11 billion. Near the midpoint of this range—around $7.5 billion—is one reasonable expectation of the additional revenue that this measure would generate in 2019. Thereafter, through 2030, that amount will rise or fall each year depending on trends in the stock market and the economy.

Increased School and Community College Funding. Under current law, the expiration of Proposition 30 is expected to slow the growth of state tax revenues, thereby slowing the growth of school and community college funding. Under this measure, the amount of Proposition 98 funds provided to schools and community colleges each year probably would increase by a few billion dollars, compared to what these entities would receive if all of Proposition 30’s tax increases expired. The amount of increased school spending over the 2019-2030 period could vary significantly, depending on such factors as the Proposition 98 variables and the state of the economy during the period.

Remaining Funding Generally Available for Any Purpose. Because funding for schools and community colleges generally would increase by a portion of the increased state tax revenues, the remaining revenues raised by this proposal typically would result in more state General Fund money being available for any budget purpose. The use of that funding would depend on decisions by future Members of the Legislature and future Governors.

Interactions With Other Budget Rules. Currently, Proposition 2 requires a portion of the existing Proposition 30 taxes to be deposited in the rainy day fund or used to speed up state debt payments. This measure would exclude its proposed revenues—those generated by extending the Proposition 30 income tax rate increases after 2018 through 2030—from the key requirements of Proposition 2. This essentially means that the taxes on potentially large amounts of capital gains generated by the proposed extension of the Proposition 30 income tax increases (1) would not be required to be deposited to the rainy day fund and (2) would not be required to be spent on speeding up payment of state debts.

The Proposition 2 rules for reserve deposits and debt payments are linked in part to each year’s Proposition 98 budget calculations. Because this measure would affect Proposition 98 calculations, it could affect the amount of Proposition 2 reserve deposits and debt payments funded by General Fund revenues after 2018. The precise nature of these effects is difficult to predict. Similarly, the likelihood that the state exceeds its Proposition 4 spending limit in the future is difficult to predict. If, however, this were to occur between 2019 and 2030, part of this measure’s revenues would go to taxpayer rebates instead of being available for other state purposes.

Fiscal Summary. This measure would have the following major fiscal effects:

- Increased state revenues annually from 2019 through 2030—likely in the $5 billion to $11 billion range initially—with amounts varying based on stock market and economic trends.

- School and community college funding would increase, as would funding available for other state purposes.