In This Report

LAO CONTACTS

Overall State Budget Condition

(Including Reserves)

Education

Health and Human Services

Corrections, Transportation,

and Environment

(Including Infrastructure)

January 11, 2016

The 2016-17 Budget:

Overview of the Governor's Budget

Executive Summary

This publication is our office’s initial response to the 2016–17 Governor’s Budget proposal, which was presented to the Legislature on January 7, 2016.

Significant Increases in Revenues and School Funding. The administration’s revenue estimates for 2015–16 and 2016–17 are billions of dollars higher than they were in last year’s budget act. Higher revenues generate significant increases in Proposition 98 funding—$4.3 billion over the 2014–15 through 2016–17 period. After satisfying Proposition 98 and Proposition 2 requirements and funding adjustments to existing programs, the Governor’s plan allocates about $7 billion in discretionary General Fund resources.

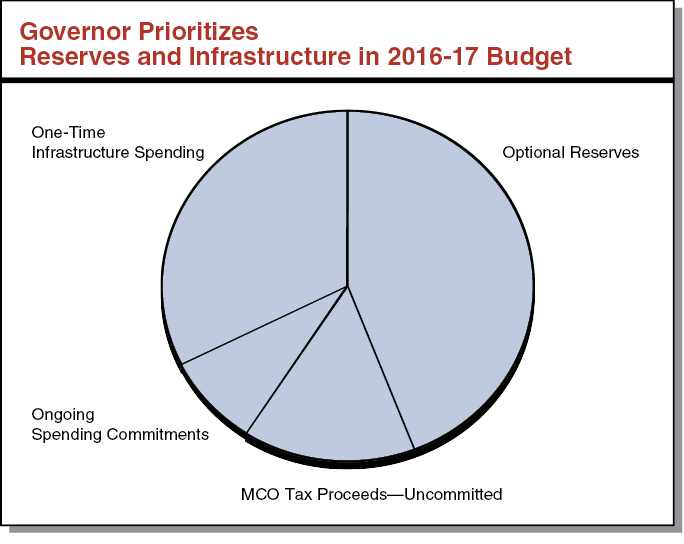

Governor’s Budget Prioritizes Reserves and Infrastructure. As shown in the figure below, in allocating discretionary resources for the 2016–17 budget, the Governor prioritizes reserves. Specifically, he proposes increasing total reserves to more than $10 billion. He allocates most other discretionary resources to one–time infrastructure spending. Outside the General Fund, the Governor plans to: (1) spend $3.1 billion cap–and–trade auction revenues, (2) provide additional revenues for transportation, and (3) extend the managed care organization (MCO) tax.

Plan for Next Economic Downturn. California has enjoyed remarkable economic growth over the past year. That said, the state may be reaching the peak of this long expansion. In crafting this year’s budget, the Legislature will choose a mix of reserves, one–time spending, and ongoing budget commitments based on its priorities. We encourage the Legislature to begin this process with a robust target for reserves for the end of 2016–17 and concentrate spending on one–time purposes. This would still leave some funds available for targeted ongoing commitments—particularly if the Legislature passes an extension of the MCO tax. Such a measured approach would better position the state for any near–term economic downturn.

Overview

On January 7, 2016 the Governor presented his 2016–17 budget proposal to the Legislature. As shown in Figure 1, the budget package proposes spending $168 billion in 2016–17, an increase of 2 percent over revised levels for 2015–16.

Figure 1

Governor’s Budget Expenditures

(Dollars in Millions)

|

Fund Type |

2014–15 Revised |

2015–16 Revised |

2016–17 Proposed |

Change From 2015–16 |

|

|

Amount |

Percent |

||||

|

General Funda |

$112,974 |

$116,064 |

$122,609 |

$6,544 |

5.6% |

|

Special funds |

41,702 |

47,636 |

45,032 |

–2,604 |

–5.5 |

|

Budget Totals |

$154,676 |

$163,700 |

$167,641 |

$3,941 |

2.4% |

|

Selected bond funds |

$5,145 |

$7,847 |

$3,086 |

–$4,761 |

–60.7% |

|

Federal funds |

90,049 |

99,761 |

91,899 |

–7,861 |

–7.9 |

|

a Includes Education Protection Account created by Proposition 30 (2012). |

|||||

Budget Position Continues to Improve. Figure 2 displays the administration’s summary data for the General Fund, the state’s main operating account. As shown in the figure, the General Fund is on steady footing. The administration’s revised revenue estimates for 2015–16 and 2016–17 are up by billions of dollars compared to last year’s budget act, similar to our office’s most recent projections for 2015–16 and 2016–17. (For more information about these revenue estimates, please see our January 7 comment on the LAO Economy and Taxes blog.) After satisfying constitutional requirements for higher reserves and spending on education, the Governor proposes significant extra reserve deposits. He then uses the remaining money for new spending commitments, primarily one–time infrastructure spending.

Figure 2

Administration’s General Fund Summary

(In Millions)

|

2014–15 Revised |

2015–16 Revised |

2016–17 Proposed |

|

|

General Funda Condition |

|||

|

Prior–year fund balance |

$5,356 |

$3,699 |

$5,172 |

|

Revenues and transfers |

111,318 |

117,537 |

120,633 |

|

Expenditures |

112,974 |

116,064 |

122,609 |

|

Ending fund balance |

$3,699 |

$5,172 |

$3,196 |

|

Encumbrances |

966 |

966 |

966 |

|

SFEU balance |

2,733 |

4,206 |

2,230 |

|

Reserve Balances at the End of the Fiscal Year |

|||

|

SFEU balance |

$2,733 |

$4,206 |

$2,230 |

|

BSA balance |

1,606 |

4,455 |

8,011 |

|

Total Reserves |

$4,339 |

$8,661 |

$10,241 |

|

Revenues and Transfersa |

|||

|

Personal income taxes |

$76,079 |

$81,354 |

$83,841 |

|

Sales and use taxes |

23,709 |

25,246 |

25,942 |

|

Corporation taxes |

9,007 |

10,304 |

10,956 |

|

Other revenues |

4,503 |

4,562 |

4,340 |

|

Subtotal, Revenues |

($113,298) |

($121,466) |

($125,078) |

|

Transfers to BSA |

–$1,606 |

–$2,849 |

–$3,556 |

|

Other transfers (net) |

–374 |

–1,080 |

–889 |

|

Totals |

$111,318 |

$117,537 |

$120,633 |

|

Spendinga |

|||

|

Proposition 98 (General Fund) |

$49,554 |

$49,992 |

$50,972 |

|

Non–Proposition 98 |

63,420 |

66,072 |

71,637 |

|

Totals |

$112,974 |

$116,064 |

$122,609 |

|

a Includes Education Protection Account created by Proposition 30 (2012). SFEU = Special Fund for Economic Uncertainties and BSA = Budget Stabilization Account. |

|||

Major Features of the Governor’s Budget

Figure 3 summarizes the major features of the Governor’s budget.

Figure 3

Major Features of the Governor’s Proposed Budget

|

Revenues |

|

|

Reserves |

|

|

|

|

Infrastructure |

|

|

|

|

|

Education |

|

|

|

|

|

|

Health and Human Services |

|

|

|

|

Other |

|

|

|

|

|

aAmount by which the Special Fund for Economic Uncertainties grows relative to 2015–16 Budget Act. LCFF = Local Control Funding Formula; MCO = managed care organization; DDS = Department of Developmental Services; IHSS = In–Home Supportive Services; and SSI/SSP = Supplemental Security Income/State Supplementary Payment. |

Reserves Total Over $10 Billion. The Governor proposes contributions to both state budget reserves: the Special Fund for Economic Uncertainties (SFEU), the state’s discretionary reserve, and the Budget Stabilization Account (BSA), the state’s constitutional rainy day fund. The budget increases the balance of the SFEU by $1.1 billion over the level assumed in the 2015–16 Budget Act. Pursuant to Proposition 2 (2014), the budget makes a constitutionally required deposit of $2.6 billion to the BSA for 2015–16 and 2016–17 combined. (We note that, by May, the Proposition 2 revised “true–up” deposit for 2015–16 could increase by hundreds of millions or more for various reasons.) In addition, the Governor proposes that the Legislature approve an optional deposit of $2 billion to the BSA. Under the Governor’s plan, by the end of 2016–17 reserves would total $10.2 billion, consisting of $2.2 billion in the SFEU and $8 billion in the BSA. This total does not include over $1 billion in proposed, but unallocated, revenues from the tax on managed care organizations (MCOs), which the Legislature could use to benefit the General Fund.

Budget Also Focuses on Infrastructure. In addition to building reserves, the Governor’s budget commits spending to infrastructure using both General Fund and special fund sources. This includes funding for maintenance, repair, and construction of state office buildings, the state highway system, local roads, university campuses, and county jails.

Other Significant Proposals on Education, Health, and the Environment. The Governor also makes other proposals. He uses most of the constitutionally required increase in Proposition 98 spending to continue implementing the state’s formula for funding school districts. The Governor also has a revised proposal to restructure the tax on MCOs while cutting other taxes on affected health plans. The Governor uses a small portion of the revenues from this tax for the In–Home Supportive Services program. He also proposes a plan to spend cap–and–trade auction revenues.

LAO Comments

Governor’s Emphasis on Reserves Is Appropriate. After meeting constitutional requirements on education spending and debt payments, the Governor proposes using a large portion of the remaining funds to grow the state’s budget reserves. We believe this general approach is prudent as a large budget reserve is the key to weathering the next recession with minimal disruption to public programs.

Focus on Infrastructure Makes Sense, but Specific Proposals Raise Several Issues. Much of the state’s infrastructure is aging and needs to be renovated, adapted, or improved to meet current and future needs. As such, we think the Governor’s focus on infrastructure makes sense. However, the Governor’s specific proposals raise several issues that merit legislative consideration. For example, the Legislature will want to consider the appropriateness of the proposed funding sources, ensure such funding is allocated to the highest priority and most cost–effective infrastructure needs, and allow for sufficient legislative oversight.

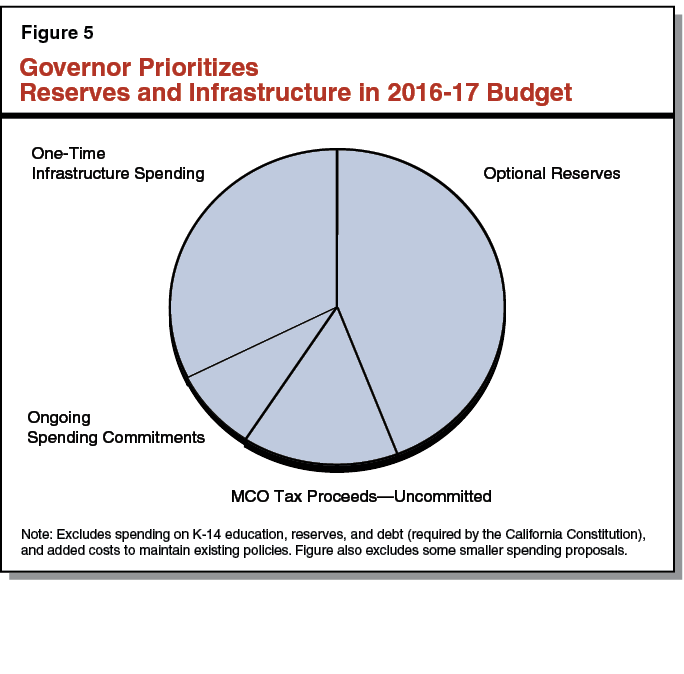

Governor Allocates About $7 Billion in Discretionary Resources. In assembling this budget, the Governor was faced with decisions about how to allocate roughly $7 billion of discretionary General Fund resources. (“Discretionary,” in this context, excludes billions of dollars controlled by constitutional funding requirements, such as Proposition 98 and Proposition 2, and added costs to maintain existing policies.) As shown in Figures 4 and 5, the Governor prioritizes reserves and one–time spending. Specifically, he uses a significant portion of the discretionary resources to increase total reserves to over $10 billion. This doubles the size of budget reserves. He proposes allocating most remaining discretionary funds to one–time infrastructure spending. Finally, he proposes ongoing budget commitments of around $600 million.

Figure 4

Governor’s Key Choices in Allocating Discretionary General Fund Resources

(In Billions)

|

Amount |

|

|

Reserves |

|

|

Makes extra rainy day fund deposit |

$2.0 |

|

Grows discretionary reserve balance |

1.1 |

|

Subtotal |

($3.1) |

|

MCO Tax Proceeds—Uncommitteda |

$1.1 |

|

One–Time Spending |

|

|

Replaces and maintains state office buildings |

$1.5 |

|

Funds statewide deferred maintenance projects |

0.5 |

|

Provides grants for replacing and renovating county jails |

0.3 |

|

Subtotal |

($2.3) |

|

Ongoing Budget Commitments |

|

|

Sets aside funds for 2016 collective bargaining process |

$0.3 |

|

Augments funding for UC and CSU |

0.3 |

|

Makes augmentations for CDCR and courts |

0.1 |

|

Makes augmentations for SSI/SSP and DDS |

0.1 |

|

Subtotal |

($0.8) |

|

Total |

$7.3 |

|

a While the Governor places proceeds of this tax in a special fund, he chose not to use most of these to benefit the General Fund or augment other programs. As a result, we include the unallocated proceeds in this figure. Note: Excludes spending on K–14 education, reserves, and debt (required by the California Constitution), and added costs to maintain existing policies. Figure also excludes some smaller spending proposals. MCO = managed care organization; CDCR = California Department of Corrections and Rehabilitation; SSI/SSP = Supplemental Security Income/State Supplementary Payment; and DDS = Department of Developmental Services. |

|

Legislature Can Allocate These Funds Differently. The Governor has communicated his priorities for the budget: more reserves and new money for infrastructure. The California Constitution, however, entrusts the Legislature to craft the annual state budget. As such, the Legislature will now choose its preferred mix of reserves, one–time spending, and ongoing budget commitments. Figure 6 shows some key questions for the Legislature to consider in its deliberations on these matters. For example, when reviewing the Governor’s proposal to deposit an extra $2 billion in the BSA, the Legislature may want to consider whether it prefers to keep those reserves in a discretionary reserve over which it has more control. We discuss other budgetary issues for consideration later in this document, and we will identify others in our upcoming budget analysis publications.

Figure 6

Key Questions for Legislative Consideration in Crafting the 2016–17 Budget

|

Reserves |

|

|

|

|

|

One–Time Spending |

|

|

|

|

|

Ongoing Budget Commitments |

|

|

|

|

|

|

aThe sales tax rate temporarily declines in certain instances if reserve balances reach a particular level, pursuant to Sections 6051.4 and 6051.45 of the Revenue and Taxation Code. The quarter–cent sales tax reductions would amount to around $1.5 billion for each year that they are in effect. SFEU = Special Fund for Economic Uncertainties and BSA = Budget Stabilization Account. |

Plan for Next Economic Downturn. California has enjoyed remarkable economic growth over the past year. The state, however, may be reaching the peak of a long economic expansion. Planning for the next downturn—including setting aside budget reserves—is an important priority. As the Legislature considers the trade–offs among different budget priorities, we encourage it to begin with a robust target for budget reserves for the end of 2016–17 and concentrate spending on one–time purposes. This approach would still leave some funds available for targeted ongoing commitments—particularly if the Legislature passes an extension of the MCO tax. Such a measured approach would better position the state for any near–term economic downturn.

Proposition 98

Below, we highlight the major features of the Governor’s Proposition 98 package and offer our preliminary assessment of it.

Major Features of Governor’s Plan

Minimum Guarantees for 2014–15 and 2015–16 Revised Upward. As shown in Figure 7, the administration’s revised estimate of the 2014–15 minimum guarantee is $66.7 billion, an increase of $387 million compared with the budget plan adopted last June. This upward revision is due primarily to an increase in the amount of local property tax revenue received by schools and community colleges. (Because Test 1 is operative in 2014–15, increases in property tax revenue result in a higher overall Proposition 98 funding level rather than offsetting General Fund costs.) The administration’s revised estimate of the 2015–16 guarantee is $69.2 billion, an increase of $766 million compared with the June budget plan. This increase is due primarily to an increase in General Fund revenue, which requires the state to make a larger maintenance factor payment. Upon making this maintenance factor payment, the state will have paid off all maintenance factor created during the last recession, leaving no maintenance factor outstanding for the first time since 2005–06.

Figure 7

Tracking Changes in the Proposition 98 Minimum Guarantee

(In Millions)

|

2014–15 |

2015–16 |

||||||

|

June 2015 Estimate |

January 2016 Estimate |

Change |

June 2015 Estimate |

January 2016 Estimate |

Change |

||

|

Minimum Guarantee |

|||||||

|

General Fund |

$49,608 |

$49,554 |

–$54 |

$49,416 |

$49,992 |

$575 |

|

|

Local property tax |

16,695 |

17,136 |

441 |

18,993 |

19,183 |

191 |

|

|

Totals |

$66,303 |

$66,690 |

$387 |

$68,409 |

$69,175 |

$766 |

|

2016–17 Minimum Guarantee Increases Notably Over 2015–16 Budget Act Level. As shown in Figure 8, the Governor’s budget includes $71.6 billion in total Proposition 98 funding in 2016–17. This funding level is $3.2 billion above the 2015–16 Budget Act level and $2.4 billion over the revised 2015–16 level. Under the Governor’s budget, Test 3 is operative in 2016–17, with the higher guarantee primarily resulting from a 2.4 percent increase in per capita General Fund revenue and the higher prior–year level carrying forward. The administration estimates that the state creates $548 million in new maintenance factor in 2016–17.

Figure 8

Proposition 98 Funding by Segment and Source

(Dollars in Millions)

|

2014–15 Revised |

2015–16 Revised |

2016–17 Proposed |

Change From 2015–16 |

||

|

Amount |

Percent |

||||

|

K–12 Educationa |

|||||

|

General Fund |

$44,496 |

$44,536 |

$45,442 |

$906 |

2.0% |

|

Local property tax |

14,834 |

16,560 |

17,802 |

1,242 |

7.5 |

|

Subtotals |

($59,330) |

($61,096) |

($63,244) |

($2,148) |

(3.5%) |

|

California Community Collegesb |

|||||

|

General Fund |

$4,979 |

$5,373 |

$5,447 |

$74 |

1.4% |

|

Local property tax |

2,302 |

2,624 |

2,812 |

188 |

7.2 |

|

Subtotals |

($7,281) |

($7,997) |

($8,259) |

($262) |

(3.3%) |

|

Other Agenciesc |

$80 |

$82 |

$83 |

— |

0.3% |

|

Totals |

$66,690 |

$69,175 |

$71,585 |

$2,410 |

3.5% |

|

General Fund |

$49,554 |

$49,992 |

$50,972 |

$980 |

2.0% |

|

Local property tax |

17,136 |

19,183 |

20,613 |

1,430 |

7.5 |

|

aIncludes State Preschool in 2014–15 and 2015–16 and proposed early education block grant in 2016–17. bIncludes $500 million for adult education regional consortia in 2015–16 and 2016–17. cConsists entirely of General Fund. |

|||||

Significant New Proposition 98 Spending. Under the Governor’s budget, the combined increases in the minimum guarantees for the three–year period result in $4.3 billion in additional Proposition 98 spending. In addition, the Governor proposes to make a $257 million settle–up payment related to meeting the 2009–10 guarantee. The Governor scores this amount as a Proposition 2 payment. After making this payment, the state would have $1 billion in outstanding settle–up. Under the Governor’s budget, K–12 Proposition 98 funding per pupil increases from a revised 2015–16 level of $10,237 to $10,605 in 2016–17, an increase of $368 (3.6 percent). Proposition 98 funding for community colleges increases from a revised 2015–16 level of $6,878 per full–time equivalent (FTE) student to $7,003 per FTE student in 2016–17, an increase of $125 (1.8 percent). Below, we highlight the Governor’s major Proposition 98 spending proposals.

Dedicates Most New Ongoing K–12 Proposition 98 Funding to Local Control Funding Formula (LCFF). The Governor’s budget proposes a $2.8 billion augmentation to LCFF, reflecting a 6 percent per–pupil increase over the 2015–16 LCFF level. The Governor estimates this increase will close 49 percent of the remaining gap to the LCFF target rates. Under the Governor’s proposal, the LCFF would be approximately 95 percent funded in 2016–17.

Restructures Preschool Programs. The Governor proposes to redirect $1.7 billion in Proposition 98 funds to create a new block grant intended to benefit low–income and at–risk preschoolers (four year olds and young five year olds). Specifically, the proposal would redirect all Proposition 98 funds from State Preschool ($878 million), Transitional Kindergarten ($726 million), and the State Preschool Quality Rating and Improvement System (QRIS) Grant ($50 million). The block grant would be given to local education agencies (LEAs) and potentially other entities that currently offer State Preschool. The Governor indicates the funds would be distributed based upon population and need, but the proposal also includes a hold harmless provision for LEAs and potentially other preschool providers. The Governor proposes developing the details of the new preschool program through a stakeholder process, with more details released at the May Revision. Key details to be addressed include eligibility criteria, curriculum requirements, funding rates, staffing requirements, child–to–staff ratios, and the possibility of non–LEA grant recipients. The Governor’s intent is that the block grant provide considerable local discretion.

Dedicates Substantial One–Time Funding to Paying Down Education Mandate Backlog. The Governor’s budget provides $1.4 billion to pay down the K–14 mandate backlog ($1.3 billion for K–12 and $76 million for community colleges). Although the Governor outlines several areas that the funding could support (including professional development and deferred maintenance), LEAs would be allowed to use the funds for any purpose. As in previous years, the funding would be distributed to school districts, county offices of education, charter schools, and community colleges on a per–student basis. The administration estimates about 60 percent of the amount allocated ($786 million) would reduce the backlog, with many LEAs receiving funding in excess of their existing claims. After making this payment, the administration estimates the state would have a remaining mandate backlog of $1.8 billion.

Creates New Workforce Program, Makes Another Permanent. The budget includes $200 million in new ongoing funding to implement recommendations of the Board of Governors Task Force on Workforce, Job Creation, and a Strong Economy. The new “Strong Workforce Program” would require community colleges to collaborate with education, business, labor, and civic groups to develop regional plans for career technical education (CTE). The regions would be based on existing planning boundaries for the federal Workforce Innovation and Opportunity Act. The budget also includes $48 million in ongoing funding to support the CTE Pathways Program. Over the last 11 years, this program has supported regional collaboration among schools, community colleges, and local businesses to improve career pathways and linkages. The state had scheduled to sunset the program at the end of 2014–15 but extended it in 2015–16 using one–time funding. The Governor proposes that future CTE Pathway funding align with the regional plans developed under the Strong Workforce Program, but the Pathway program would continue to have separate categorical requirements.

Initiates Five–Year Plan for Transitioning All Subsidized Child Care to Voucher System. In addition to his major Proposition 98 preschool restructuring proposal, the Governor has a major non–Proposition 98 child care restructuring proposal. Currently, the state offers child care through a mix of direct contracts with providers and vouchers that families can use for various child care arrangements. The Governor proposes trailer bill language that would require the California Department of Education (CDE) to develop a five–year plan for eliminating direct contracts and transitioning all subsidized child care to a voucher system.

LAO Comments

Administration’s Estimate of Local Property Tax Revenue Too Low. The administration estimates that local property tax revenue counting toward Proposition 98 will be $19.2 billion in 2015–16 and $20.6 billion in 2016–17. We think these estimates are about $1 billion too low across the two–year period. Of the $1 billion difference between the administration’s estimates and our estimates, roughly $700 million is related to the dissolution of redevelopment agencies. The administration’s lower estimate does not appear to reflect growth in the tax increment associated with former redevelopment agencies or the reduction in redevelopment–related debt. The remaining roughly $300 million difference is due to the administration having lower estimates of assessed property values. Whereas the administration estimates that assessed property values will grow by 5.6 percent in 2015–16 and 2016–17, we estimate growth rates of 6 percent in 2015–16 (based on the latest data submitted by county assessors) and at least 6 percent in 2016–17 (based on continuing growth in housing prices). If local property tax revenue comes in higher than the administration estimates, Proposition 98 General Fund costs will be correspondingly lower and available non–Proposition 98 General Fund will be higher.

Budget Plan Provides Modest Cushion Against Potential Downturn. Though we anticipate the state’s economic growth will continue in the near term, the minimum guarantee could decrease in 2017–18 or future years if stock market prices were to drop or growth in the economy and personal income were to decline. Such a scenario serves as a caution against the state committing all available Proposition 98 funding for ongoing purposes. The Governor’s budget dedicates $520 million of the funding within the 2016–17 minimum guarantee for one–time activities. This effectively reflects a cushion of less than 1 percent (0.7 percent). If the guarantee were to decline by more than this amount in 2017–18, the Legislature might have to reverse its progress toward LCFF implementation or make reductions to other ongoing programs. The Legislature could consider dedicating a larger share of 2016–17 funding for one–time activities to minimize the likelihood of such future reductions.

Prioritizing LCFF Implementation Consistent With State’s Prior–Year Actions. The Governor’s plan to dedicate most additional ongoing K–12 funding to LCFF implementation is consistent with the Legislature’s approach over the past three years. By continuing to prioritize LCFF implementation in 2016–17, both the Governor and the Legislature would be fostering greater local control and flexibility while simultaneously making progress toward providing additional funding for disadvantaged students.

Recommend Legislature Adopt Governor’s Basic Preschool Restructuring Approach. We believe consolidating preschool funding and prioritizing funds for low–income children would be a major improvement over the state’s existing preschool policies. Consolidating existing funding streams into one funding stream that has uniform application would simplify and streamline the existing system while potentially allowing for greater consistency in service. Prioritizing funds for low–income children would ensure that the state’s available resources are directed to those most in need of the support, as low–income families are less likely than higher–income families to be able to afford preschool on their own. Moreover, one of the more consistent research findings is that preschool provides greater initial benefits to children from low–income than high–income families.

Ensure New Preschool Program Upholds Key Principles. In developing a new preschool program for low–income children, we recommend the Legislature keep certain key principles in mind. Of primary importance, we recommend the Legislature establish a clear objective for the new program. California’s existing preschool programs have tended to suffer from a lack of both clarity and unity of overarching objectives. Without clear objectives, the state would not be able to assess whether a new program is functioning as intended and producing desired public benefits. In building the new preschool program, we also recommend the Legislature build off the tenets of the LCFF by keeping funding linked to children and treating similar children similarly—meaning the state would provide the same or about the same amount of funding per low–income child regardless of district and expect the same or about the same type and quality of service. As with LCFF, having this type of transparency and equity does not have to come at the expense of flexibility. Preschool providers still could build their programs consistent with local interests and priorities (such as using different learning content or emphasizing different wraparound services). In building the new preschool program, we also recommend the Legislature minimize initial disruption to preschool providers while avoiding permanently locking in funding allocations that would undermine other key principles, including transparency, equity, and accountability.

Recommend Legislature Consider Most Appropriate Way of Retiring Existing Mandate Backlog. We believe the Governor’s basic mandate backlog approach of providing a per–student allocation to all LEAs is reasonable, as all LEAs were required to undertake specified mandated activities in previous years. A per–student approach, however, very likely will never eliminate the existing backlog entirely because the amount of remaining claims per student varies significantly across the state, with a few LEAs having much higher per–student claims than other LEAs. We estimate the state would need to provide more than $150 billion to eliminate the existing backlog using such an approach. We recommend the Legislature consider ways to eliminate the backlog entirely without necessarily rewarding a few LEAs that filed much higher claims than all other LEAs. One such approach would be to provide an amount equal to or in excess of the remaining backlog, distribute on a per–student basis, but make a condition of receipt that participating LEAs accept the funding in lieu of all outstanding claims.

Better Regional Alignment of Workforce Education a Laudable Goal but Governor’s Approach Further Fragments Already Fragmented System. By creating a new workforce education program and making permanent an otherwise expiring one, the Governor’s proposals would hinder the state’s goal of creating a more coherent and integrated workforce development system. In 2015–16, the state budgeted $6 billion for more than 30 workforce programs administered across nine state agencies. Of these amounts, $2.6 billion and nine programs were administered or co–administered by community colleges. To comply with the requirements of these existing workforce programs, community colleges already participate in numerous local and regional consortia of education, business, labor, and civic groups. Each of these programs also has unique service and accountability requirements. The new workforce program the Governor proposes would add another set of rules to the current mix. Continuing the otherwise expiring CTE Pathways program would retain a separate set of rules permanently. Rather than adding to the complexity and fragmentation of the state’s workforce system, we recommend the Legislature remain focused on the overarching vision of moving toward a more coherent and integrated system. The Legislature could work toward this end by further consolidating and streamlining existing workforce programs rather than creating new ones.

Recommend Legislature Adopt Child Care Restructuring Approach and Provide Guidance to CDE in Developing Transition Plan. Shifting all subsidized child care to a voucher system would have many benefits, including allowing more low–income, working families to have flexibility in finding helpful child care arrangements. We recommend that the Legislature adopt the Governor’s basic approach and provide guidance to CDE as it develops a transition plan. Specifically, we recommend that the Legislature task CDE with creating a plan that would provide one child care reimbursement rate structure, one set of minimum statewide standards, and one streamlined set of associated administrative processes.

Infrastructure

Governor’s Proposals

The Governor’s budget includes various proposals to improve public infrastructure, such as the state highway system, state office buildings, schools, local streets and roads, and county jail facilities. We describe each of these—and other— proposals below.

Transportation Funding Package ($3.6 Billion Special Funds). On the day the Governor signed the 2015–16 Budget Act, he called a special legislative session on transportation funding. As part of this special session, the Governor proposed last fall a package of proposals to increase funding for transportation programs. These proposals are generally reflected in the Governor’s proposed budget for 2016–17. Specifically, the Governor’s transportation funding package proposes to provide an estimated $3.6 billion annual increase for state and local transportation infrastructure programs. Revenue from the funding package would phase in during 2016–17 and 2017–18 and provide a permanent ongoing increase thereafter. The funding package includes primarily new tax revenues, but also redirects certain existing revenues. Specifically, the funding package includes:

- $2 billion annually from a new $65 vehicle registration tax.

- $1 billion annually from increases in gasoline and diesel excise tax rates, including indexing these rates for inflation.

- $500 million annually from cap–and–trade auction revenues.

- $100 million from efficiencies at the California Department of Transportation (Caltrans) resulting from various minor changes to streamline project delivery processes.

In addition, the budget assumes that $879 million in prior loans from transportation accounts are repaid over a four year period from 2016–17 through 2019–20.

The proposed budget allocates about half of the new transportation revenues to the state and half to local agencies to support various existing and new programs. Specifically, the Governor proposes to allocate about $1.5 billion to rehabilitate state highways, about $1.4 billion for local streets and roads, $400 million for transit, $200 million to improve trade corridors, and $120 million for state highway maintenance.

State Office Buildings ($1.5 Billion General Fund). The Governor’s budget proposes one–time funding of $1.5 billion from the General Fund to be deposited into a new State Office Infrastructure Fund (SOIF). Under the proposal, monies in this fund would be continuously appropriated for the replacement and renovation of various state office buildings in the Sacramento area. The Governor proposes spending $10.1 million from SOIF in 2016–17 to initiate the replacement or renovation of three state buildings: the Food and Agriculture Annex, the State Capitol Annex, and the Natural Resources Building. The SOIF could enable the administration to fund the renovation or replacement of some buildings up front on a “pay–as–you–go” basis, rather than financed by borrowing through the use of long–term bonds. We note, however, that the administration envisions constructing the new Natural Resources Building using a lease–to–purchase approach.

The Governor’s proposal follows the July 2015 release of a long–range planning study of office space in the Sacramento region that was required as part of the 2014–15 budget package. The study identified various deficiencies at 29 state–owned office buildings and ranked the Natural Resources Building, Personnel Building, and Paul Bonderson Building as those in most critical need of renovation or replacement. The study excluded several buildings not considered as typical office space, including the Food and Agriculture Annex and State Capitol Building and Annex.

UC Merced Campus Expansion ($1.1 Billion State and Nonstate Funds). Pursuant to Chapter 50 of 2013 (AB 94, Committee on Budget), the Department of Finance (DOF), rather than the Legislature, approves the University of California’s (UC’s) capital outlay requests. For 2016–17, Chapter 50 requires DOF to submit an initial list of approved projects to the Legislature by February 1, 2016 and a final list no earlier than April 1, 2016. On September 1, 2015, UC submitted a proposal to DOF to expand the Merced campus significantly. Specifically, the proposal seeks to grow enrollment on the campus from 6,200 to 10,000 students by 2020. The project would cost $1.1 billion and add 917,500 square feet of facility space to the campus (more than doubling existing space). The UC is requesting from DOF the authority to use its main General Fund appropriation to pay for debt service on about half the project’s total costs (with nonstate funds used for debt service on the remainder). The UC plans to enter into a public–private partnership to finance, design, build, operate, and maintain the project’s facilities.

Deferred Maintenance ($807 Million Various Funds). The Governor’s budget and the associated five–year infrastructure plan identify state infrastructure deferred maintenance needs of $77 billion, the large majority of which is related to the state’s transportation system and addressed by the transportation funding package discussed above. The budget proposes one–time spending totaling $807 million from various sources toward addressing these needs. Of the total, the Governor proposes $500 million in non–Proposition 98 General Fund support for various entities as shown in Figure 9. The proposal also includes $289 million from budget–year and prior–years’ Proposition 98 funds for the California Community Colleges. Under the proposal, this funding could be used to address deferred maintenance, instructional equipment, and water conservation projects. The remaining $18 million is from the Motor Vehicle Account for the deferred maintenance needs at the California Highway Patrol and Department of Motor Vehicles. (By comparison, the 2015–16 Budget Act included $120 million in one–time, non–Proposition 98 General Fund support for deferred maintenance and $148 million in Proposition 98 funds for deferred maintenance projects and certain other one–time purposes at the community colleges.)

Figure 9

Administration’s General Fund (Non–Proposition 98) Deferred Maintenance Proposal

(In Millions)

|

Department/Program |

Proposed Amount |

|

Water Resources |

$100.0 |

|

State Hospitals |

64.0 |

|

Judicial Branch |

60.0 |

|

Parks and Recreation |

60.0 |

|

Corrections and Rehabilitation |

55.0 |

|

California State University |

35.0 |

|

University of California |

35.0 |

|

Developmental Services |

18.0 |

|

Fish and Wildlife |

15.0 |

|

Military Department |

15.0 |

|

General Services |

12.0 |

|

Veterans Affairs |

8.0 |

|

Forestry and Fire Protection |

8.0 |

|

State Special Schools |

4.0 |

|

California Fairs |

4.0 |

|

Science Center |

3.0 |

|

Hastings College of the Law |

2.0 |

|

Emergency Services |

0.8 |

|

Conservation Corps |

0.7 |

|

Food and Agriculture |

0.3 |

|

San Joaquin River Conservancy |

0.2 |

|

Total |

$500.0 |

County Jail Construction ($250 Million General Fund). Since 2007, the state has approved three measures authorizing a total of $2.2 billion in lease–revenue bonds to fund the construction and modification of county jails. For example, the 2014–15 budget package authorized $500 million in lease–revenue bonds for jail construction. The Governor’s budget for 2016–17 proposes an additional $250 million from the General Fund for jail construction. According to the administration, the proposed funds would be awarded to counties that have either (1) not received any of the above $2.2 billion or (2) received less funding than they requested. Under the proposal, counties would be subject to a 10 percent match requirement, except that small counties (population of 200,000 or less) would be subject to a 5 percent match requirement.

School Facilities. The Governor continues to express interest in working with the Legislature to improve the state’s existing school facility program and revisit how the state and schools share facility costs. While emphasizing the need for a revamped program, the Governor notes that the proposed $9 billion school bond for the November 2016 ballot makes no changes to the existing school facility program. Despite raising various concerns with both the existing school facility program and the already eligible school bond measure, the Governor’s budget package contains no specific alternative.

LAO Comments

Much of the state’s infrastructure is aging and needs to be renovated, adapted, or improved to meet current and future needs. Thus, we think the Governor’s attention to infrastructure makes sense. However, the Governor’s specific proposals raise several issues that merit legislative consideration. Specifically, in reviewing the proposals the Legislature will want to consider (1) its priorities for funding infrastructure, (2) the appropriate sources of funding to address the identified infrastructure needs, (3) the appropriate financing approach to address the identified infrastructure needs, (4) the extent to which funding will be allocated to the highest priority and most cost–effective projects, (5) whether the proposals include adequate long–term plans for addressing infrastructure needs, and (6) whether the proposals allow for sufficient legislative oversight.

Assess Priorities for Funding Infrastructure. In reviewing the Governor’s infrastructure proposals, the Legislature will want to consider how it prioritizes infrastructure spending compared to other important state needs, as well as which types of infrastructure spending are of highest priority. As it considers these priorities, the Legislature will want to think about whether there are other ways to meet state infrastructure needs, such as by adopting strategies to reduce demands for infrastructure through policies that increase utilization, encourage less costly alternatives, or improve efficiency. Similarly, the Legislature will want to consider how recent policies have impacted the demand for certain infrastructure, such as the passage of Proposition 47 (2014), which reduced workload for county jails by reducing jail terms for certain offenders. Additionally, the Legislature will want to determine the extent to which the state should bear responsibility for costs related to local infrastructure. This will be a particularly important consideration with regard to any school facility funding changes.

Consider Appropriateness of Funding Sources. In addition, the Legislature will want to consider the appropriate sources of funding to address the identified infrastructure needs. For example, the Governor proposes a mix of permanent tax increases and one–time and ongoing uses of existing special fund and General Fund resources to fund the various infrastructure proposals. The Legislature may want to ensure that permanent funding sources (such as new tax revenues) are used to meet ongoing needs, whereas one–time funding sources are aligned with one–time needs (such as reducing backlogs of required maintenance work).

Weigh Trade–Offs of Proposed Financing Approaches. The Legislature will want to consider the appropriate financing approach for infrastructure projects—whether direct appropriations (pay–as–you–go), renting or leasing, or borrowing (typically through the issuance of bonds). For example, the proposed SOIF could enable the administration to fund some renovations and replacements of state office buildings on a pay–as–you–go basis rather than through bonds. It is reasonable to fund projects that provide services over many years, such as building replacements, through bonds that are repaid over time. While bonds are somewhat more expensive than direct appropriations, as the state must pay interest on them, the difference in costs is less significant in the current low–interest rate environment. Thus, the Legislature will have to weigh the benefits of spreading costs out over time (thus freeing up funding for other legislative priorities) against the modest extra cost of using bonds. Additionally, the Legislature will want to consider whether a public–private partnership is the preferred approach for undertaking the UC Merced project, given that the state has experienced some challenges with using public–private partnerships in the past.

Ensure Funding Allocated to Most Cost–Effective and Highest Priority Projects. The Legislature will also want to ensure that funding is allocated to the most cost–effective and highest priority projects. For example, the Governor’s deferred maintenance proposal does not include a specific list of proposed projects, which makes it difficult to evaluate whether the administration prioritized the distribution of deferred maintenance funds to the highest priorities. Additionally, funding highway maintenance is significantly more cost–effective than allowing highways to deteriorate such that major rehabilitation is needed. However, the Governor’s plan provides only a minor increase for highway maintenance. Moreover, we note that the Governor’s transportation proposals would create additional and more complex formulas for allocating funds among programs. The Legislature could consider simplifying the system of allocating transportation revenues to better ensure funding is allocated to the highest priorities. The Legislature also faces challenges in ensuring any new school facility funding goes to the most cost–effective and highest priority projects, as the Governor and many other groups believe the state’s existing allocation approach is seriously flawed.

Require Long–Term Planning. Long–term planning is required to ensure that infrastructure is well constructed and maintained. Accordingly, the Legislature will want to make sure that the administration has provided sufficient information on long–term plans to help ensure that the funds will be spent in the most effective manner. For instance, while allocating one–time funding for deferred maintenance is a step in the right direction, the Governor has not identified a long–term plan to address the overall backlog or the underlying causes of deferred maintenance. Additionally, the long–range planning study of Sacramento office space did not include a required funding and sequencing plan for the renovation or replacement of state office buildings over the next 25 years. Without such a plan, it can be difficult for the Legislature to adequately evaluate the Governor’s proposal for funding state office buildings.

Allow for Sufficient Legislative Oversight. For any new funding provided, the Legislature will want to have accountability measures in place to ensure that funds are spent in a manner that best meets the state’s needs. For example, we have recommended in the past that the Legislature establish project–level accountability for Caltrans projects by requiring the independent California Transportation Commission to oversee the cost, scope, and schedule of all state highway rehabilitation projects.

Additionally, we have recommended in the past that the Legislature evaluate projects through the typical state budget process. Some 2016–17 proposals circumvent routine legislative oversight. For example, by being continuously appropriated, the Legislature would not have an opportunity to evaluate SOIF projects through the typical state budget process. We strongly recommend the Legislature not take this approach to allocating SOIF funds as it would greatly reduce the Legislature’s ability to ensure that funds are allocated to the highest priority projects and are adequately overseen. Additionally, by requiring only DOF approval, the Legislature would not have an explicit opportunity to evaluate the UC Merced project, despite it being a major, complex, and costly campus expansion. The Legislature likely will want to consider what the appropriate process is for reviewing these types of projects, allocating associated funds, and maintaining adequate accountability. The Governor’s deferred maintenance proposal also limits legislative oversight by not identifying the specific projects that would be funded. Rather, the proposal is to notify the Legislature of projects after enactment of the budget. This process essentially limits the Legislature’s ability and time to ensure that the funded projects are aligned with its priorities.

Health and Human Services

MCO Tax

Proposes Revised MCO Tax. The state’s existing MCO tax leverages federal Medicaid funds that offset General Fund spending for Medi–Cal local assistance by over $1.1 billion in 2015–16. Under current law, this MCO tax expires on July 1, 2016. The federal government issued guidance that California’s MCO tax is likely incompatible with federal Medicaid requirements for health–care related taxes and California must make changes necessary to bring the tax structure into compliance by no later than the end of this legislative session. While the administration and the Legislature have considered different approaches to structuring a permissible MCO tax, to date no legislation has been enacted to authorize such a replacement tax. The Governor’s budget includes a revised MCO tax structured with the intent of complying with federal Medicaid requirements.

Governor’s Plan Structured to Meet Several Goals. The Governor’s proposed MCO tax plan is structured to meet three administration goals:

- Meet Federal Requirements. According to the administration, the proposed MCO tax is structured so as to meet federal requirements. However, the state would still need to seek formal federal approval of any restructured MCO tax the state ultimately adopts.

- Aid General Fund and Pay for Restored In–Home Supportive Services (IHSS) Hours. Under the Governor’s proposal, revenues from the restructured MCO tax would draw down sufficient federal funds to maintain the current $1.1 billion “offset” for Medi–Cal costs that otherwise would be paid from the General Fund. Pending legislative approval of a revised MCO tax, the Governor’s budget proposal holds most of the 2016–17 MCO tax revenues in a special fund reserve. Therefore, the expenditure authority would need to be granted to spend these revenues on Medi–Cal or other purposes if an MCO tax is approved. The restructured tax would also raise an additional $236 million in 2016–17. This amount would provide the nonfederal share of the Medicaid funding needed to continue the restoration of IHSS hours that were eliminated as a result of the previous 7 percent reduction in service hours. (The 2015–16 budget restored these IHSS hours on a one–time basis using General Fund resources.)

- Limit Financial Impact of the Tax on MCOs. While exact details are not yet available, the administration indicates its plan would cut other taxes paid by some MCOs—specifically, their corporation and insurance taxes that are paid to the state General Fund. The administration reports that its plan would reduce corporate and insurance taxes by about $370 million per year. After these tax cuts are taken into account, the administration estimates the MCO industry overall would receive a $90 million net benefit annually. (We understand that some individual plans may receive a net benefit under the plan, while others may be worse off financially.)

Possible Effects on Other Budget Items. Under the Governor’s proposal, revenues from the MCO tax are not currently proposed to be spent in the Department of Developmental Services (DDS) budget in 2016–17. The Governor’s budget summary indicates “additional targeted spending proposals” in DDS would likely be funded from a revised MCO tax. The budget summary also indicates the administration may seek to end the state’s Coordinated Care Initiative for persons eligible for both Medi–Cal and Medicare if a revised MCO tax is not approved.

Issues for Legislative Consideration. Given the need to seek federal approval, the administration has indicated it seeks swift approval of a revised MCO tax. Below, we suggest several issues for legislative consideration in reviewing the Governor’s proposal:

- Distributional Impact on MCOs. While the administration considers that its proposal would result in a net benefit to the MCO industry overall, the net financial effects for individual plans would vary. Some plans would face a net fiscal liability while other plans would benefit. The market impacts of the uneven distribution of tax liability across plans should be considered to assess whether there may be unintended negative consequences for the industry and consumers.

- Required Federal Approval Is Not Certain. In addition to obtaining authority from the Legislature to enact the proposed MCO tax, the state must also seek approval from the federal government. The structure of the proposed MCO tax would require the state to formally request the federal government to waive certain federal requirements for health care–related taxes in seeking federal approval for the MCO tax. While the administration is of the view the proposed MCO tax is permitted under federal Medicaid rules, federal approval is not certain. Accordingly, if the Legislature passes a revised MCO tax, it should consider contingency budget plans in the event that the federal government rejects the state’s plan.

- General Fund Revenues and School Funding. The Governor’s proposal would cut taxes that MCOs pay to the state’s General Fund. Reductions in General Fund tax revenues result in lower Proposition 98 school funding requirements in most years. Accordingly, the Governor’s plan could reduce school funding requirements in some future years—perhaps by a couple hundred million dollars, based on the administration’s estimates of General Fund revenue loss. The administration’s budget estimates do not consider these effects. In addition, the administration’s estimates do not consider the possible effects of recent appellate court and Franchise Tax Board determinations related to certain health plans’ tax obligations. Most notably, a September 2015 state appellate court decision (Myers v. State Board of Equalization) found that certain managed care plans could potentially be regarded as insurers, which would subject them to the state’s insurance tax. If the Governor’s MCO tax plan relieves those plans of their future obligations to pay insurance taxes, the resulting General Fund revenue loss—and the related reduction in school funding requirements—may be larger than discussed above.

Developmental Services

The 2016–17 budget provides for several new spending proposals in the DDS. These major budget proposals are primarily to support community services and their development, as described below. The budget also includes a proposal for additional headquarters staff resources to improve DDS’ fiscal oversight of services provided to persons with developmental disabilities.

Budget Assumes a New Rate for Certain Residential Facilities. The Governor’s budget proposes $46 million ($26 million General Fund) to allow for the development and implementation of a new rate for certain residential facilities serving four or fewer individuals. These facilities are currently funded through a rate methodology—known as the Alternative Residential Model (ARM) rate—which has not been updated in many years. This rate methodology was established based on the assumption that each home would support six residents. Therefore, the current individual rate–per–consumer paid to facilities assumes that overhead and staffing costs is spread across six placements, even though Regional Centers (RCs) are increasingly using facilities with fewer placements, which is generally consistent with federal policy direction. The new rate would be based on a four–bed model. Because many individuals residing in DDS–funded residential homes are in ARM–rate facilities, we think the Governor’s proposal merits consideration. However, the Governor’s budget does not include any other proposed rate adjustments or reforms for any other community service provider rates, which continue to be of significant interest to the Legislature and part of ongoing stakeholder and legislative discussions.

Funding to Begin Compliance Efforts With New Federal Regulations. The Governor’s budget provides $17.1 million ($12.2 million General Fund) to support compliance by March 2019 with new federal requirements related to Medicaid–funded community–based services. California receives about $1.7 billion in federal funds annually for these services in the DDS budget. The new federal rules require that services are provided in settings that are integrated with the larger community. The proposed funding would support 21 Program Evaluator positions within the RCs to evaluate and monitor compliance and would provide resources to providers for service modifications and staffing needs to meet compliance. Noncompliance with these regulations could put federal funding at risk. While the Governor’s proposal shows the administration’s commitment to bringing California into compliance, it is unclear how this proposal would be implemented and the extent to which the funding levels provided for service changes move the state toward full compliance with the federal regulations.

Additional Service Development Funds Support Developmental Center Closures. In May 2015, the administration announced plans to initiate closure of the state’s remaining developmental centers, with some exceptions. The 2015–16 spending plan reflects the Legislature’s approval of the Governor’s intent in concept. On October 1, 2015, DDS submitted to the Legislature a plan to close Sonoma Developmental Center and in November 2015 announced intent to submit similar closure plans for Fairview Developmental Center and the general treatment area at Porterville Developmental Center. The Governor’s budget includes $78.8 million ($73.9 million General Fund) in one–time resources for service development targeted for individuals transitioning from these centers. The state is at risk of losing additional federal funding related to these developmental centers due to violations generally related to clients’ health, safety, and rights. The state was able to reach a settlement agreement with the federal government that would continue funding if certain terms are met, which include a commitment to transition individuals out of Sonoma Developmental Center. The state is in similar negotiations related to the other developmental centers proposed for closure.

Budget Includes Funds to Support Improvements in RC Caseload Ratios. Current reports to DDS indicate that all RCs were out of compliance with one or more caseload–ratio requirements for the past two years. The Governor’s budget includes $17 million ($13 million General Fund) to support an estimated 200 additional RC service coordinator positions. Caseload reports show RCs have had a longstanding noncompliance in meeting caseload–ratio requirements. We note that the Governor’s proposal does not appear to provide adequate funding to bring RCs into full compliance with these ratios, and to the extent that RCs are out of compliance with federal caseload ratios, some federal funding could be at risk.