The 2020-21 Budget:

California's Fiscal Outlook

See a list of this year's fiscal outlook material, including the core California's Fiscal Outlook report, on our fiscal outlook budget page.

LAO Contact

November 20, 2019

The 2020-21 Budget

California’s Fiscal Outlook

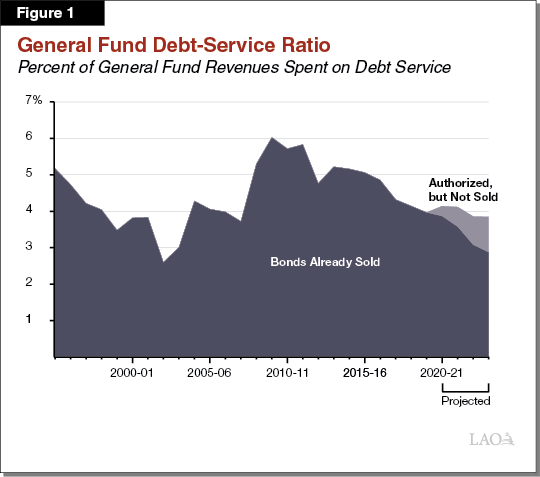

Debt Service on Infrastructure Bonds

Debt Service Ratio (DSR) Has Fluctuated Historically. The DSR—the ratio of annual General Fund spending on debt service costs to annual General Fund revenues and transfers—is often used as one measure of the state’s debt burden. As shown in Figure 1, the DSR has varied considerably in past decades between about 3 percent and 6 percent. In the late 2000s, the DSR grew to about 6 percent following the approval of several large bond measures, as well as a significant reduction in state revenues due to the recession. More recently, however, the DSR has declined to about 4 percent. This decline in the DSR occurred for a variety of reasons, including rebounding General Fund revenues, refinancing of existing debt due to low interest rates, and state policies shifting some state debt costs from the General Fund to special funds—such as in transportation.

DSR Expected to Fall Below 5 Percent. We estimate that the DSR will fall below 4 percent over the next several years. This is because we project that General Fund revenues will increase somewhat faster than debt service costs. We assume that the state gradually sells bonds that have been approved by voters or the Legislature. These bonds include most of the remaining unsold infrastructure bonds that voters approved in November 2018 for children’s hospitals and housing programs, as well as bonds approved in earlier years. In total, we estimate that the amount the state pays for debt service from the General Fund will grow from $5.7 billion in the current year to $6.4 billion in 2023‑24. Our projections do not include any additional debt service costs for new bonds that might be authorized by the voters or the Legislature during the forecast period, such as Proposition 13, a $15 billion general obligation bond for schools scheduled for the March 2020 election.