LAO Contact

For other reports on COVID‑19,

see our COVID‑19 Issues page.

Correction 1/19/21: Legend on Figure 3 corrected to match data.

January 19, 2021

How Has COVID‑19 Affected Renters and Homeowners?

Summary

In this report, we look at how coronavirus disease 2019 (COVID‑19) has affected renters and homeowners and how state and federal policies have helped to stabilize household finances for both groups. We find that the unprecedented actions of the state and federal governments to boost incomes and provide rental and mortgage relief have helped many households who otherwise would have faced an eviction or foreclosure avoid these destabilizing events.

Despite these actions, many households continue to struggle financially due to the effects of COVID‑19. In particular, low‑wage workers were in a precarious financial position before the pandemic, and tend to work in industries that were most affected by the pandemic. These workers are likely to rent, rather than own, their home. As a result, there has been significant interest in how the pandemic has affected renters, especially how much rental debt has accumulated in California due to COVID‑19. To help answer this question, we collaborated with researchers from the Federal Reserve Bank of Philadelphia to update their recent national assessment of rental debt to more accurately reflect economic conditions and policies in California. In this report, we present the findings of our collaboration.

Our revised analysis estimates that California renters owe $400 million in unpaid rent, down from $1.7 billion estimated for California in the nationwide analysis, as of December 2020. Our analysis does not estimate the amount of underlying rental debt that existed prior to March 2020 due to the state’s longstanding housing affordability challenges, nor do we forecast how state and federal policy changes would affect the accumulation of rental debt in the future.

Introduction

With the emergence of COVID‑19, the state economy abruptly ground to a halt in the spring of 2020. While the state economy has experienced a modest rebound since that time, the pandemic continues to disrupt the lives of all Californians in small and large ways, from changing how we interact in our communities to the way we work. However, for many, including the 1.4 million Californians who remain out of work, the effects of COVID‑19 have been more dire. In this report, we look at how the pandemic has affected renters and homeowners and how state and federal policies have helped to stabilize household finances for both groups, preventing many households from experiencing rental evictions and mortgage delinquencies. We also provide an updated estimate of the total unpaid rental debt in California—taking into account state and federal steps to stabilize household finances—that has accumulated due to COVID‑19.

This report does not address the state’s underlying housing affordability challenges. Addressing California’s housing crisis is one of the most difficult challenges facing the state’s policy makers. Millions of Californians struggled to find housing that was affordable before the pandemic. The crisis is a long time in the making, the culmination of decades of shortfalls in housing construction. Just as the housing affordability crisis has taken decades to develop, it will take years or decades to correct. We hope that by shedding light on how COVID‑19 has added to the financial stress of renters, we can inform policy solutions to help renters through this crisis. In particular, the state and local governments will soon have to determine how to allocate recently authorized federal funding for emergency rental assistance. Beyond this crisis, continued work will be necessary to address the state’s underlying housing affordability challenges.

Looking Back at 2020:

Homeowners and Renters During COVID‑19

The Economic Consequences of COVID‑19 Have Been Widespread... In a matter of weeks, 2.6 million Californians and 22 million people nationally lost work due to the onset of the pandemic. Many observers, including our office, feared that a large number of these households would fall behind on rent or mortgage payments, leading to evictions and foreclosures.

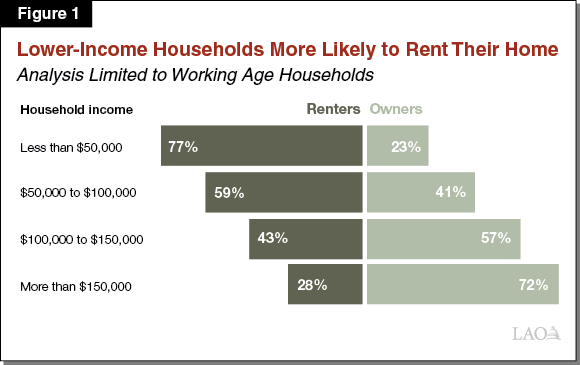

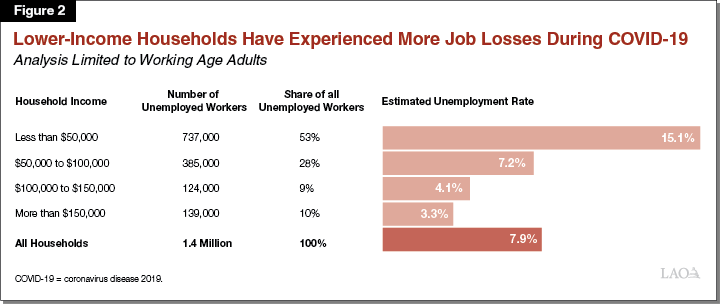

…But Renters Have Been Disproportionately Affected. Even before the pandemic, the high cost of housing in California placed renter households in a precarious position, particularly the 1.5 million low‑income households who paid at least half of their income toward housing. A pandemic‑induced job loss adds further financial stress to these households. Due to the composition of the industries and occupations most affected by public health restrictions and declining economic activity, renter households have faced higher rates of job loss during the pandemic. This is because job losses have been concentrated among lower‑wage workers who are much more likely to rent than higher‑wage workers. As shown in Figure 1, nearly 80 percent of households with less than $50,000 in annual earnings rent, whereas only 28 percent of households with more than $150,000 in annual earnings rent. As shown in Figure 2, more than half of workers who have lost their jobs are members of lower‑income households (less than $50,000 in annual earnings). The estimated unemployment rate for workers in lower‑income households (15 percent) is five times higher than the estimated unemployment rate for workers in higher‑income households (3 percent).

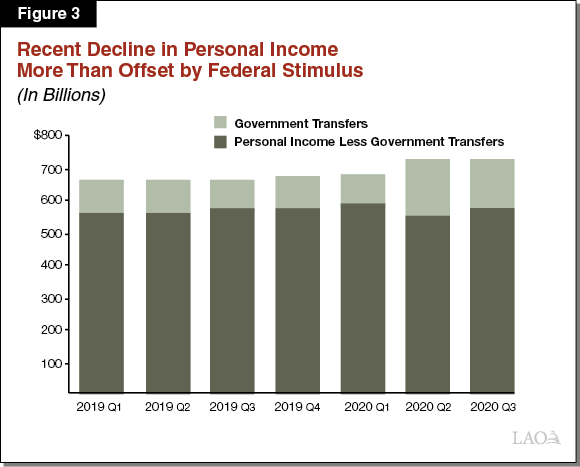

State Actions and Federal Stimulus Quickly Helped Stabilize Finances for Most Households… Very quickly after the pandemic declaration, the state and federal governments took unprecedented steps to boost households’ incomes and provide rent and mortgage relief to households affected by COVID‑19. In particular, several federal programs—such as expanded unemployment insurance (UI) benefits and stimulus checks—provided a significant boost to household incomes throughout 2020. For workers who experienced a job loss during 2020, enhanced UI benefits during the spring and summer backfilled lost income by up to $1,050 per week. During the COVID‑19 pandemic, the state has regularly distributed $5 billion per week in UI benefits ($100 million per week is typical during normal economic conditions). To date, the state has distributed more than $115 billion in UI benefits to unemployed workers. As Figure 3 shows, because of increased federal stimulus and UI benefit payments, the total income of California households was almost 10 percent higher in the second and third quarters of 2020 than those same quarters in 2019. (Of course, many households earned less during this period but, on average, household incomes increased throughout the state due to federal stimulus programs.)

…As a Result, Many Households Have Been Able to Avoid Evictions and Delinquencies. Due to the unprecedented steps to boost incomes and provide rental and mortgage relief, many households who otherwise would have faced an eviction (or fallen behind on their rent) or foreclosure (or fallen behind on the mortgage) have been able to avoid these destabilizing events. Despite these steps, some households—especially households headed by undocumented adults, who are ineligible for most federal stimulus programs, and those who have not received UI benefits due to processing delays—undoubtedly continue to struggle financially due to the effects of COVID‑19. Below, we provide further details on how COVID‑19 has affected renters and homeowners.

How Has COVID‑19 Affected Renters and Rental Debt?

Exact Amount of Unpaid Rent as a Result of COVID‑19 Pandemic Unknown. There has been significant interest in how the pandemic has affected renters, in particular, how much rental debt has accumulated in California due to COVID‑19. Although the exact amount of unpaid rent in the state is unknown, researchers have attempted to estimate this amount to shed light on how the pandemic has affected renter households and thereby help inform any policy response.

Initial National Analysis by Federal Reserve Bank of Philadelphia Estimated California Renters Owe $1.7 Billion in Unpaid Rent. In October 2020, researchers at the Federal Reserve Bank of Philadelphia published a national analysis of rental debt due to COVID‑19. The results of their analysis were published in their report, Household Renter Debt During COVID‑19. The national model tracks households over the course of the pandemic, adjusting monthly household income downward for job losses and upward for federal stimulus and UI benefits. Based on how these households’ incomes change during the course of the pandemic, some households are estimated to have insufficient income to pay monthly rent and other nonhousing costs. Each month, rent debt accumulates for these households. The analysis found that about 5 percent of California renters (240,000 households) had accumulated unpaid rent due to COVID‑19. For households with rental debt, the average amount of unpaid rent was $7,000. In total, the report found that California renters likely would accrue a total of $1.7 billion in unpaid rent due to COVID‑19 through December 2020.

LAO Collaborated With Federal Reserve Bank of Philadelphia to Develop California‑Specific Estimate of Rental Debt. The Federal Reserve Bank of Philadelphia’s analysis calculates renter debt nationwide, meaning that several underlying assumptions are applied to renters in all states. This is a reasonable approach when developing a complicated model that aims to identify the scope of rental debt nationally, as was the goal of the Federal Reserve Bank of Philadelphia. Naturally, this approach means that some assumptions may not reflect the experience of a particular state. Mindful of this, our office collaborated with researchers at the Federal Reserve Bank of Philadelphia to adjust key assumptions about (1) renter nonhousing costs, (2) renter savings rates, and (3) statewide UI benefit amounts in their model to more accurately reflect economic conditions and policies in California. Specifically, our office revised estimates for monthly nonhousing costs upward to reflect California’s high cost of living and revised savings downward to reflect that many low‑income renters faced financial insecurity even before the pandemic. Next, we revised the model’s assumption that half of eligible unemployed workers receive UI benefits to match state UI benefit administrative records that show that a much higher share of workers have received UI benefits during the pandemic. The researchers at the Federal Reserve Bank of Philadelphia then updated their analysis of rental debt in California using our assumptions for these key inputs. (The Appendix provides additional information about this methodology.)

Updated Analysis Estimates That California Renters Owe $400 Million in Unpaid Rent. Our first two adjustments—revising nonhousing costs up and savings down—had the effect of increasing the estimate of total rental debt from $1.7 billion to $2.2 billion. These adjustments were more than offset, however, by our office’s revised estimate for UI benefits, which have represented a major income boost during the pandemic. Revising the UI participation rate upward to match state records had the effect of reducing total unpaid renter debt due to COVID‑19 from $2.2 billion to $400 million as of December 2020. Overall, the updated analysis estimated that about 2 percent of California renters (90,000 households) had unpaid rent. For households with rental debt, the average amount of unpaid rent was $4,500.

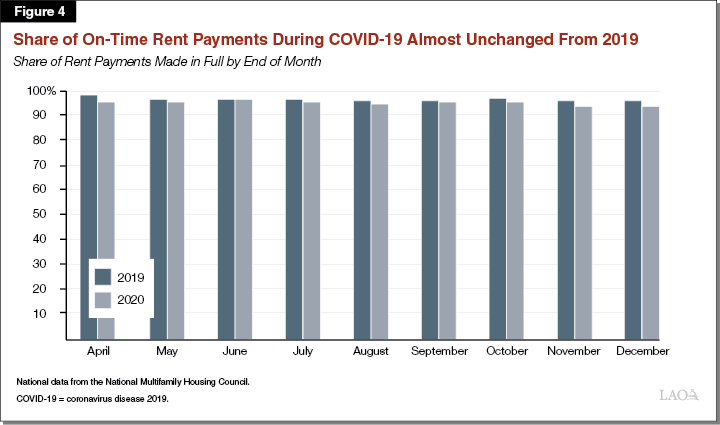

Lower Estimate of Unpaid Rent in California Appears Consistent With Data on On‑Time Rent Payments. The updated estimate that California renter households owe $400 million in unpaid rent due to COVID‑19 may appear low given the widespread economic consequences of the pandemic. However, recent data on rent payment timeliness suggest that the unprecedented federal actions to boost incomes have helped many renter households cover their rent. According to a nationwide survey conducted by the National Multifamily Housing Council, shown in Figure 4, the share of rent payments that were on time during COVID‑19 has been only slightly lower than the share made on time during the same month in 2019.

Updated Estimate of Pandemic‑Related Renter Debt Reflects Small Fraction of California Rent Payments… Households who cannot make their rent payments clearly face difficult choices. In the aggregate, however, the model’s estimate of unpaid rent—$400 million due to COVID‑19—represents a very small fraction of overall rent payments in the state, which likely total more than $100 billion annually.

…But Only Accounts for COVID‑Related Rental Debt. It is important to keep in mind that renters already faced sizeable affordability challenges prior to the pandemic. For instance, prior to the pandemic, our office estimated the state would need to provide roughly $10 billion per year in renter assistance to ensure no low‑income renter paid more than 50 percent of their monthly income in rent (a threshold often used to distinguish those who are severely rent burdened). The initial, as well as the revised, model only estimates rental debt attributed to COVID‑19. To reiterate, the model does not estimate the amount of underlying rental debt that existed prior to March 2020, nor does the model forecast how state and federal policy changes (specifically the expiration of state and federal relief efforts) would affect the accumulation of rental debt in the future.

State and Federal Policy Changes Affecting Renters

Eviction Protections. In an effort to avert a worsening of the state’s housing crisis due to the financial hardships experienced by Californians because of COVID‑19, the Governor, Judicial Council, and Legislature have adopted various policies related to housing and homelessness since the start of the pandemic. (While the federal government issued national eviction protections, the state‑based actions generally provided a higher level of protection for renters from eviction.) Most significant have been the eviction protections for renters provided by the Tenant, Homeowner, and Small Landlord Relief and Stabilization Act of 2020 (Chapter 37 of 2020 [AB 3088, Chiu]). Under the legislation, no tenant can be evicted before February 1, 2021 because of rent owed due to a COVID‑19‑related hardship experienced between March 4, 2020 and August 31, 2020, if the tenant provides a declaration of hardship. (Executive orders from the Governor and Judicial Council rules offered renters eviction protections during this period.) The law also specifies that for a COVID‑19‑related hardship that occurs later—between September 1, 2020 and January 31, 2021—tenants must pay at least 25 percent of their rent due to avoid eviction. Tenants are still responsible for paying unpaid rents to landlords, but those unpaid amounts cannot be the basis for an eviction. These protections are set to expire on January 31, 2021. The 2021‑22 Governor’s Budget identifies his desire to continue some type of eviction protection past January 31, 2021, however, the budget does not provide details about an extension of the eviction moratorium.

Recently Authorized Federal Funding For Emergency Rental Assistance. In late December 2020, the federal government authorized $25 billion for emergency rental assistance. California is estimated to receive $2.6 billion of that funding. Local governments with populations over 200,000 are eligible to receive a direct allocation from the federal government to provide rental assistance. Current estimates indicate the state government will receive $1.4 billion, while local governments will receive $1.2 billion. Federal requirements provide some limitation on the use of this funding, including that eligible households must have experienced financial hardship due to COVID‑19, be at risk of homelessness or housing instability, and have a household income at or below 80 percent of the area median. Eligible households can use these resources to address past‑due rent and utility payments, as well as future rental payments. While federal requirements provide parameters for the use of these funds, the state and local governments have important decisions to make about how they will administer this funding to assist renters that have accumulated rental debt because of the pandemic.

Going Forward

Could Rental Debt Increase Going Forward? Despite our revised analysis and recently authorized federal funding for emergency rental assistance, the actual amount of accrued rental debt is unknown. On the one hand, renter relief during COVID‑19 and recently enacted federal income assistance should help many rental households avoid accruing additional rental debt going forward. Furthermore, although many renters remain out of work, the state economy has rebounded since April 2020, regaining more than 1 million out of the 2.6 million jobs that were lost in March and April 2020. As a result, many renters who were out of work earlier in the pandemic may now be working again and able to stabilize their household finances. On the other hand, 1.4 million workers remain unemployed and recent surges in the pandemic have resulted in a new round of tightened public health orders, which could have financial ramifications on renters and lead to further accrual of rental debt. Moreover, the expiration of the eviction protections offered by AB 3088 at the end of January creates significant uncertainty for renters going forward. Until the pandemic is behind us and jobs can fully return, some renters may continue to accrue rental debt and face a risk of homelessness or housing instability.

How Has COVID‑19 Affected Homeowners?

Relative to renters, homeowners tend to be higher income and hold greater savings and other assets, positioning them better to weather financial disruptions. Because of homeowners’ generally stronger financial position and federal policy response to the pandemic, homeowners have fared relatively well during the pandemic compared to the concerns many observers held during the first months of the pandemic. Throughout 2020, mortgage delinquencies remained very low, in part because—as discussed earlier—job losses have been less severe in jobs typically held by homeowners and federal stimulus programs have stabilized household budgets. Additionally, for homeowners specifically, delinquencies have remained low due to a new federal relief program that allowed many homeowners to defer their mortgage payments for up to 12 months. Going forward, while delinquencies likely will increase somewhat during the spring and summer of 2021 as forbearance periods begin expiring, we anticipate that many borrowers will be able to continue making their mortgage payments after their forbearance period ends.

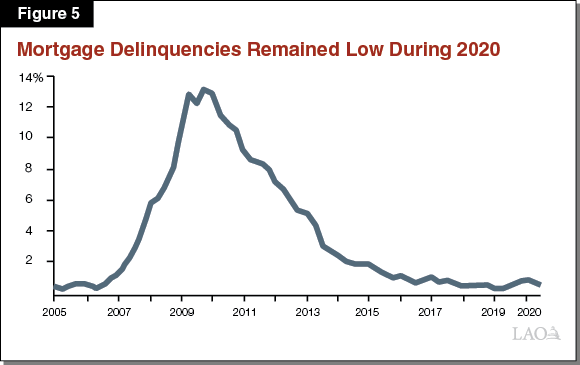

Mortgage Delinquency Remained Low in 2020. Credit report data compiled by the Federal Reserve and included in Figure 5 shows that mortgage delinquencies among California homeowners remained low in 2020. Specifically, 5 in every 1,000 California homeowners were more than 90‑days late on their mortgage during the third quarter of 2020. This level is about even with the average level of delinquency from 2017 to 2019, and significantly lower than the level during the last recession.

Why Have Delinquencies Remained Low? As discussed earlier, federal actions to boost household incomes, as well as low unemployment among higher‑income workers (who are most likely to be homeowners), have helped most homeowners weather the downturn. For homeowners who nevertheless were unable to make their payments, a federal forbearance program provided the option to defer mortgage payments to the end of their loan term.

Forbearance Programs Allowed Homeowners to Defer Payments to End of Loan. The federal Coronavirus Aid, Relief, and Economic Security (CARES) Act provides up to 12 months of loan forbearance for borrowers who have been affected by COVID‑19. Mortgage payments are not made during forbearance. Borrowers have several options for repaying mortgage payments not made during forbearance, including repaying them as regular monthly payments at the end of the borrower’s loan term. A survey by the national Mortgage Bankers Association estimates that about 5 percent of all loans currently are in forbearance. According to the survey, 80 percent of these borrowers requested forbearance during the first months of the pandemic.

Could Delinquencies Increase Going Forward? The federal 12‑month forbearance guarantee will lapse this spring for borrowers who requested assistance during the first months of the pandemic. However, not all borrowers who requested forbearance will enter delinquency. For several reasons, many forbearance borrowers likely will be able to continue their mortgage payments after forbearance.

- Not All Homeowners in Forbearance Have Missed Mortgage Payments. The federal forbearance program is available to all borrowers, not only those who are unable to make their mortgage payments. Under federal law, borrowers do not need to prove or document their inability to meet their mortgage payment. As a result, some borrowers may have requested forbearance as a cautionary step and, after several months of relief, may be able to continue making payments. A survey from the Mortgage Bankers Association shows that about 30 percent of the 2 million U.S. homeowners who have exited forbearance since June continued to make their mortgage payments despite being in forbearance.

- Employment Has Improved. Some borrowers who currently are in forbearance have regained employment since the pandemic began and therefore are more likely to be able to continue their payments. Although the economic rebound had slowed in recent months, the labor market has nevertheless regained 1 million jobs since it hit bottom in April 2020.

- Home Equity Has Risen. Monetary policy and guidance set by the Federal Reserve in response to the pandemic helped to push down mortgage interest rates. As a result, home values have risen considerably since the start of the pandemic, creating additional wealth for most California homeowners. Data from Freddie Mac suggests that very few (less than 1 percent) of homeowners in forbearance have negative equity—that is, they owe more than their home is worth. Negative equity is a common risk factor of mortgages entering delinquency.

For the reasons stated above, while delinquencies likely will increase somewhat during the spring and summer of 2021, we anticipate that many forbearance borrowers will be able to continue making payments.

Acknowledgement

We would like to thank the Federal Reserve Bank of Philadelphia and their research staff for sharing their expertise and collaborating with our office on this work.

Appendix:

Additional Information about Rental Debt Model

Overview of Federal Reserve Bank of Philadelphia Model. The national model built by the Federal Reserve Bank of Philadelphia tracks households over the course of the pandemic, adjusting monthly household income downward for job losses and upward for federal stimulus and unemployment insurance (UI) benefits. Based on how these households’ incomes change during the course of the pandemic, some households are estimated to have insufficient income to pay both monthly rent and other nonhousing costs. When this occurs, the model assumes these households do not pay their full monthly rent. Each month, rental debt accumulates for these households. By December 2020, the initial analysis estimated that California renters would owe a total of $1.7 billion.

Updated California‑Specific Assumptions. Our office provided updated California‑specific information on renter nonhousing costs, renter savings rates, and statewide UI benefits. Specifically, our office revised estimates for monthly nonhousing costs upward from $8,000 per person, per year to $12,000 per person, per year to reflect a higher cost of living in California. We also revised available savings downward from the original model assumption that renter households had 5 percent of their annual income in available savings. As a conservative estimate, our revised assumption was that the average California renter household had no available savings to cover rent and other expenses in the event of a job loss. Together these adjustments increased unpaid renter debt in California relative to the initial findings in the Federal Reserve Bank of Philadelphia’s analysis. Specifically, these assumptions increase the estimate of total rental debt by about $500 million, from $1.7 billion to $2.2 billion. However, this increase is more than offset by our office’s revised estimate for UI benefits.

The Federal Reserve Bank of Philadelphia’s model is sensitive to assumptions about UI benefits because the federal enhancements greatly increased the average weekly benefit unemployed workers receive. The Federal Reserve Bank of Philadelphia’s national model assumes a UI take‑up rate of about 50 percent—that is, that about 50 percent of eligible unemployed workers receive UI benefits, including the federal enhancements. In our review, however, we uncovered a discrepancy between this key assumption and available state administrative data. Specifically, the model assumes that half of California’s 2.6 million unemployed workers (as of the peak in April) received UI benefits, for a total of about 1.3 million recipients. However, administrative data from the state’s Employment Development Department show that more than 4 million workers received UI benefits in April. Our review suggests an actual take‑up rate that is well above 100 percent. (The vast majority of this discrepancy is due to a difference between how unemployment is calculated in federal surveys and how UI eligibility is determined by the state, not fraudulent claims.)

In light of this discrepancy, we revised the UI benefit take‑up rate assumption from 50 percent to 100 percent. This revised assumption has the effect of reducing total unpaid renter debt. After adjusting the unemployment insurance take‑up rate assumption upward, the model’s estimate of total unpaid renter debt falls from $2.2 billion to $400 million as of December 2020.