2012

Other Budget Issues

| Last Updated: | 5/24/2012 |

| Budget Issue: | Retirement costs |

| Program: | UC and CSU |

| Finding or Recommendation: | Recommend rejecting Governor's May proposals to not adjust UC and CSU's budgets for certain pension and retiree health and dental benefits costs. Recommend modifying proposed $52 million augmentation for UC to reflect its actual pension costs. Recommend approving technical change to separately track funding for CSU retiree health care costs. |

Further Detail

May Revision Makes Notable Modifications to January Retirement Proposals

The Governor's May Revision contains several modifications to his January proposals regarding the University of California (UC) and the California State University’s (CSU's) retirement costs.

January Proposal. The Governor’s January budget proposed to cease adjusting CSU’s base budget in the future to reflect changes in its retirement costs—including those for pensions and retiree health and dental benefits. For UC, the Governor similarly proposed to forgo any future adjustments for retirement costs. For 2012-13, however, the Governor proposed a $90 million base augmentation for UC which the administration suggested “could” be used for retirement contributions. Yet, the administration emphasized that this funding was not being proposed specifically to fund UC’s pension costs. (For more detail on the January proposal, please see the "Retirement Costs" section of The 2012-13 Budget: Analysis of the Governor's Higher Education Proposal.)

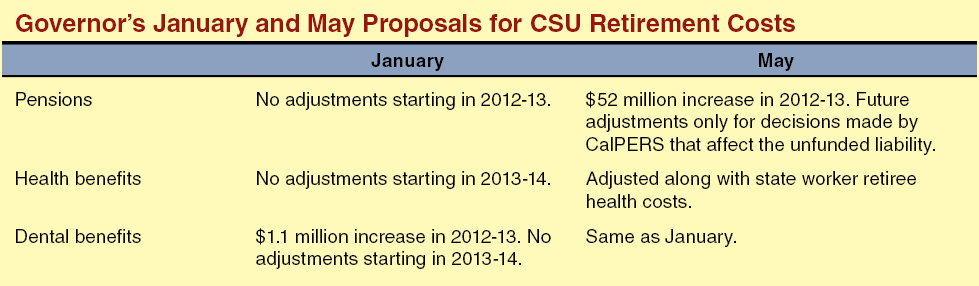

Modifications to CSU Retirement Proposal. In his May Revision, the Governor now proposes to provide CSU with the usual budget adjustment in 2012-13 for changes in its pension costs. (The administration estimates in its May Revision that this adjustment will equal $52 million.) Starting in 2013-14, however, CSU would only receive budget adjustments resulting from changes made by the California Public Employees Retirement System (CalPERS) that affect the pension plan's unfunded liability. This means that CSU would only be responsible for changes in pension costs related to changes in its total employee compensation. For example, if CSU were to increase its total payroll costs, then it would be responsible for the incremental increase in its employer pension contribution to CalPERS. In another departure from his January proposal, the Governor now proposes to provide the usual budget adjustments going forward for CSU’s retiree health care costs since these costs are determined by CalPERS. (In a related technical maneuver, the administration proposes to track state funding for these costs separately from the retiree health care costs for other state workers.) For retiree dental costs, the Governor retains his original January proposal to cease out-year budget adjustments since these benefits are managed by CSU and not CalPERS. The figure below summarizes the Governor’s January and May Revise proposals for CSU’s retirement costs.

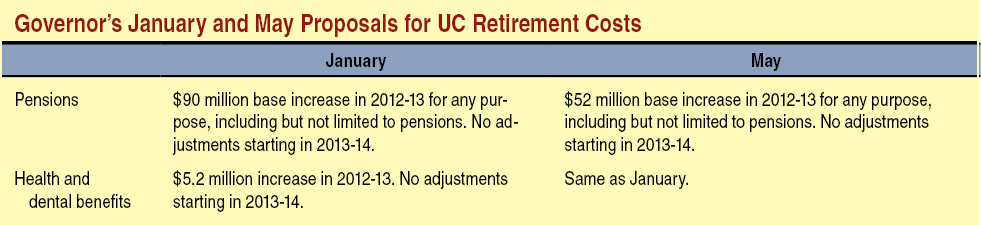

Modifications to UC Retirement Proposal. The May Revision proposes only one modification to the administration’s January plan for UC’s retirement costs. Specifically, the Governor reduces the proposed $90 million base augmentation to $52 million. The administration indicates that it is providing the reduced amount since it matches the administration’s estimate of CSU’s pension cost increase in 2012-13. The administration retains its January proposals to provide UC with no further budget adjustments for retiree health and dental costs beginning in 2012-13. The figure below summarizes the Governor’s January and May Revise proposals for UC’s retirement costs.

Revised Approach Makes Improvements but Still Has Problems

Addresses Concerns About Universities’ Lack of Control Over Certain Costs . . . The administration’s May proposal addresses some of our earlier concerns from January. For example, the administration now proposes to provide budget adjustments for CSU’s retiree health care costs and a portion of its pension costs that are determined by CalPERS. These changes address our concern that CSU did not have total control over these particular costs. Under the January proposal, CSU would have had to either redirect resources from elsewhere or raise new revenue (most likely through tuition increases) should these costs increase due to actions taken by CalPERS. Conversely, the state would not have been able to capture any savings should these costs have decreased. The May Revision corrects those shortcomings.

. . . But Changes to Workload Budgeting System Still Problematic. We are still concerned, however, that the proposal shifts budgetary responsibility to the universities for what have traditionally been considered workload budget adjustments. The state has traditionally provided these adjustments since it expects the universities to deliver (absent any policy changes) the same programs and services each year even if certain costs increase. (Likewise, the state has traditionally captured savings when these costs decrease.) Under the Governor’s May Revision, the universities would be responsible for changes in these costs. The Governor’s rationale for changing this longstanding workload budgeting system is tied to his January proposal for a “multiyear funding agreement” with the universities that would provide each segment with annual increases to their base funding to manage workload cost pressures. Thus, instead of the state making adjustments for many different costs, the state would instead simply increase their budget appropriations by a fixed percentage. The segments would be expected to manage their costs with that funding. The administration, however, has not yet presented to the Legislature its plan for the funding agreement. (According to the administration, it is still in negotiations with the universities on this plan.) This means that action on changing the workload budgeting system (as proposed in the May Revision) is premature.

Revised Amount Proposed for UC’s Pension Costs Still Arbitrary. In addition, we find that the Governor’s May Revision proposal for a $52 million increase for UC is just as arbitrary as the $90 million increase he had proposed in January. We continue to encourage the Legislature to link any state funding for UC’s pension costs to actual costs. In January, we were provided with information from UC that indicated that its additional costs for pensions in 2012-13 for state General Fund and tuition-funded employees would be about $78 million. (Specifically, $36 million is related to the General Fund and $41.5 million related to tuition.)

LAO Recommendations

We credit the administration for trying to devise a new way to budget for the universities that would give them an incentive to reduce costs, as well as for their spring revisions that improve the proposal’s workability. However, we still find that the proposal inappropriately decouples funding from actual costs. Accordingly, we recommend that the Legislature reject the proposed changes to the state’s longstanding workload budgeting methodology. In addition, we recommend that the Legislature only provide UC with an augmentation for its pension costs that is based on actual cost data provided by the university. (We have no issue with the proposed technical accounting change to track CSU’s state funding for retiree health care costs and recommend that the Legislature adopt this one part of the Governor’s proposal.)