In This Report

LAO Contact: Ann Hollingshead

February 24, 2016

The 2016-17 Budget

The Governor’s Proposition 2 Debt Proposal

Summary

Proposition 2 requires the state to pay down a minimum annual amount of state debts. In this publication, we analyze the administration’s proposal for meeting Proposition 2 debt payment requirements in 2016–17 and beyond. We find the administration’s proposal focuses on paying down debts that benefit schools and potentially benefit special fund fee payers. Specifically, the administration focuses on Proposition 98 settle up and repaying special fund loans. These debts also tend to carry relatively low interest rates.

We suggest an alternative approach for the Legislature to consider in meeting Proposition 2 debt requirements. Our approach focuses more on debts with high interest costs that the state is otherwise not addressing. Specifically, we suggest prioritizing two debts: (1) the state pension system for judges and (2) retiree health benefits for state and California State University (CSU) employees. Under our approach, the Legislature would continue to have an average of several hundred million dollars per year to pay down other Proposition 2 eligible debts. Compared to the Governor’s Proposition 2 debt plan, our alternative could save taxpayers billions of dollars more over the long run and begin to address more of the state’s retirement liabilities sooner.

Many other approaches are also reasonable, however. We suggest the Legislature hear from the pensions systems and others in considering its long–term plans for using Proposition 2 debt payment funds.

Background

In this section, we describe the constitutional requirements for minimum annual debt payments and the debts eligible for these payments under Proposition 2. We note that—as described in the box below—the annual state budget pays down billions of dollars of other liabilities outside of Proposition 2 requirements. In the appendix of a companion budget brief, The 2016–17 Budget: The Governor’s Reserve Proposal, we detail the administration’s calculation of Proposition 2 budget reserve and debt payment requirements.

Proposition 2 One Part of State’s Debt Approach

Other Liabilities Paid Outside of Proposition 2 Requirements. Beyond Proposition 2’s requirements, the annual budget pays down several billion dollars of liabilities each year. These include debt service on bonds, budgetary liabilities—such as K–14 mandate reimbursements—and pension unfunded liabilities. For example, in addition to $1.9 billion in Proposition 2 debt payments, the 2015–16 Budget Act allocated about $3 billion to the California Public Employees’ Retirement System to pay down the unfunded liability for state employee pension benefits. The 2015–16 budget plan also included $6.6 billion for debt service on general obligation bonds.

Proposition 2 Debt Payment Requirements

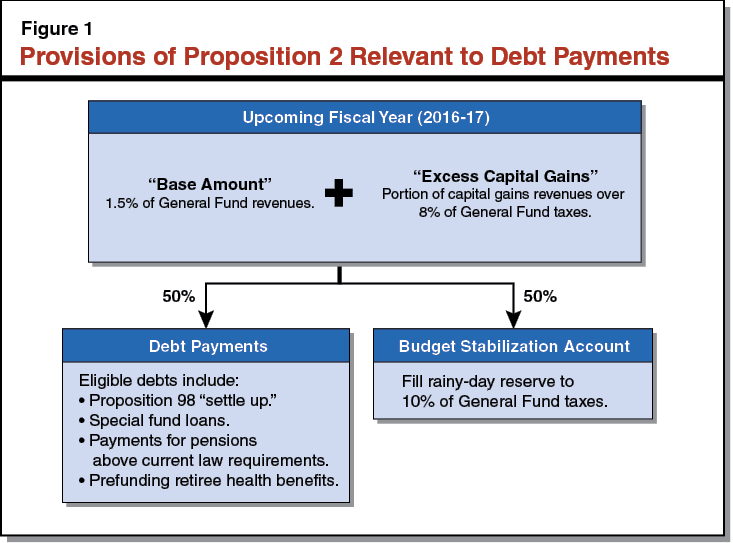

State Constitution Requires Minimum Debt Payments Each Year. Passed by voters in 2014, Proposition 2 amended the State Constitution to change budgeting practices concerning debt payments and budget reserves. Specifically, Proposition 2 requires the state to spend a minimum amount each year to pay down specified debts. These minimum payments are required through 2029–30. Thereafter, debt payments become optional, but amounts not spent on debt must be deposited into the rainy–day reserve.

Minimum Debt Payments Set by Proposition 2 Formula. Figure 1 illustrates the steps in determining the amount of required debt payments under Proposition 2. First, the state must set aside 1.5 percent of General Fund revenues (we refer to this as the “base amount”). Second, the state must set aside a portion of capital gains revenues that exceed a specified threshold (we refer to this as “excess capital gains”). The state combines these two amounts and then allocates half of the total to pay down eligible debts and the other half to increase the level of the rainy–day reserve.

Some Proposition 2 Rules Do Not Apply to Debt Payments. While Proposition 2 requires the state to “true up” reserve deposits, debt payment requirements are not revised in this way. In addition, unlike reserve requirements, which the Governor and Legislature may reduce during a budget emergency, the state may not reduce the constitutionally required debt payments for any reason.

Administration’s Estimates for Debt Payments. The administration estimates that required debt payments will total $1.6 billion in 2016–17. These requirements are based on the administration’s January 2016 estimates for 2016–17 General Fund revenues and tax proceeds, personal income taxes derived from capital gains, and the share of excess capital gains that the Constitution requires that the state spend on education. The estimates of these amounts—and therefore of required debt payments—will change when the administration releases its revised budget plan in May 2016.

Debts Eligible for Proposition 2 Funds

As shown in Figure 2, there are four types of debts eligible for payments under Proposition 2. These include two types of budgetary liabilities—certain amounts the state owes schools and amounts the state’s General Fund owes other state funds—and unfunded liabilities for pensions and retiree health benefits. Proposition 2 also made eligible reimbursements for pre–2004 mandate claims from cities, counties, and special districts, but the 2014–15 budget paid off these outstanding claims. We describe each of the remaining eligible liabilities in greater detail below.

Figure 2

Liabilities Potentially Eligible for Proposition 2 Debt Payment Funds

(In Billions)

|

Amount |

|

|

Budgetary Liabilities |

|

|

Special fund loans to the General Funda |

$4.0 |

|

Proposition 98 settle up |

1.2 |

|

Unfunded Retirement Liabilities—Pensions |

|

|

School and community college employeesb |

81.5 |

|

State and CSU employees |

43.3 |

|

UC employees |

12.1 |

|

Judges |

3.4 |

|

CalPERS quarterly payment deferral |

0.6 |

|

Unfunded Retirement Liabilities—Retiree Health |

|

|

State and CSU employees |

74.1 |

|

UC employees |

17.3 |

|

aAmount listed differs from administration’s display for two reasons. First, we list certain transportation loans that the administration lists separately ($879 million). Second, we list transportation loans from weight fees that the administration does not include in its list of eligible debts ($1.4 billion). bReflects total unfunded liabilities for school and community college employees administered by CalSTRS ($72.7 billion) and CalPERS ($8.8 billion). CalSTRS total includes amounts assigned to the state ($14.9 billion) and districts ($57.6 billion), and the amount unassigned ($0.2 billion). |

|

Special Fund Loans. As one of many actions the state took in the 2000s to address its budget problems, the state loaned amounts to the General Fund from other state accounts known as special funds. Any such loans outstanding as of January 1, 2014 are debts eligible for payment under Proposition 2. As noted in Figure 2, our display of special fund loans differs somewhat from the administration’s display. In particular, we include loans from a fund receiving transportation weight fees that—upon repayment—will be used for transportation bond debt service.

Proposition 98 “Settle Up.” Proposition 98 establishes a constitutional minimum funding guarantee for schools and community colleges. Settle up occurs when the minimum guarantee turns out to be larger than the amount that was initially included in the budget. Settle up existing as of July 1, 2014 is eligible to be paid from Proposition 2. The 2015–16 budget included $256 million for settle up, leaving $1.2 billion outstanding.

Pension Unfunded Liabilities. Payments toward unfunded liabilities of “state–level pension plans” are eligible to meet Proposition 2 debt payment requirements. In Figure 2, we have listed unfunded liabilities of pension benefits related to state and CSU employees, judges, school and community college employees, and University of California (UC) employees. Our display of debts eligible for Proposition 2 differs from that of the administration primarily because we list pension unfunded liabilities related to school and community college “classified” employees, such as food service workers. Proposition 2 requires payments for retirement liabilities to be in excess of the amounts scheduled under law. In other words, the spirit of the measure is to accelerate payments for retirement liabilities, not to replace planned or expected payments.

Payments to Prefund Retiree Health Benefits. The state and the UC generally pay for retiree health benefits when employees retire rather than during those employees’ working careers. This process shifts the cost of these benefits to future taxpayers. Proposition 2 permits the state to use its debt payment funds to prefund these benefits. Prefunding involves investing contributions and using the resulting investment returns to partially fund future costs. Prefunding these benefits costs taxpayers much less over the long term than the state’s and UC’s current “pay–as–you–go” approach.

Framework for Prioritizing Eligible Debts

In this section, we lay out a framework to help the Legislature prioritize the debts eligible for Proposition 2 funds. We suggest three factors for consideration related to each eligible debt: (1) whether or not the state is already addressing it, (2) its interest rate, and (3) the group or entities who benefit from its repayment.

No Plan in Place to Address Some Eligible Debts

The State Is Already Addressing Some Eligible Debts. The state is already addressing most of its key liabilities. In other words, the state has plans in place to address most of the liabilities shown in Figure 2. For example, recent actions taken by the California Public Employees’ Retirement System (CalPERS) board aim to increase the likelihood that unfunded liabilities for its key pension programs will be retired over about 30 years. Similarly, the 2014–15 budget package included a plan that aims to fully fund CalSTRS by the mid–2040s.

The State Is Not Yet Addressing Retiree Health. On the other hand, there are other debts eligible for Proposition 2 funds that, at least in part, are not being addressed and merit further legislative attention. Of these, the largest is the state’s retiree health benefit program. As of June 30, 2015 the state’s unfunded liability for retiree health benefits was estimated to be $74.1 billion. While the administration has begun efforts to prefund these liabilities through the collective bargaining process, the necessary bargaining agreements are not yet in place to address the vast majority of this unfunded liability. The nearby box describes the Governor’s approach for addressing this unfunded liability in more detail.

Governor’s Retiree Health Proposal

Approach Relies on Collective Bargaining Process. The state does not put money aside to fund future retiree health costs, but rather pays these costs as they are incurred on a pay–as–you–go basis. The Governor has proposed one approach to address retiree health liabilities through the collective bargaining process. Specifically, the administration’s proposal aims to (1) establish a prefunding plan through collective bargaining and (2) reduce state costs going forward through benefit scope changes for future employees. As such, the administration’s proposal hinges on the state’s success in using the collective bargaining process to establish a major new prefunding revenue stream from state employees. For more information on the Governor’s approach for prefunding retiree health benefits, see our March 2015 report, The 2015–16 Budget: Health Benefits for Retired State Employees.

The State Is Also Not Yet Addressing Some Judges’ Pensions. Another significant eligible liability that does not have a funding plan is the state’s pension program for judges elected or appointed before November 9, 1994. This pension program is known as Judges’ Retirement System I (JRS I). The state essentially pays JRS I benefits on a pay–as–you–go basis because the state has less than 2 percent of the assets needed for pension benefits earned by these judges to date. By contrast, the state has 72 percent of the assets needed for pension benefits earned by state and CSU employees.

Other Liabilities. There are some other debts eligible for Proposition 2 debt payment funds that do not have a funding plan in place. First, like the state, the UC does not yet have a prefunding plan in place to address its retiree health liabilities. Likewise, budgetary debts such as special fund loans and Proposition 98 settle up are generally not paid off under any preset schedule, meaning the Legislature must choose when to repay these debts.

Eligible Debts Have Different Interest Rates

Prioritizing High–Interest Debt Maximizes Savings for Taxpayers. The Proposition 2 eligible debts vary widely in terms of their interest rates. (While retirement liabilities do not explicitly accrue interest like loans or bonds, for simplicity we refer to retirement liability growth rates as “interest.”) In Figure 3 we make some rough estimates of the interest rates of various eligible debts over time. The figure shows that retirement liabilities grow much faster than budgetary liabilities. Prioritizing high–interest debts in the short run would result in more savings than prioritizing their low interest counterparts. These savings would accrue to taxpayers in the future, either in the form of lower taxes or more public services.

Figure 3

Rough Estimates of Interest Rates for Eligible Debts

|

Interest Rate |

|

|

Budgetary Liabilities |

|

|

Special fund loans to the General Funda |

0.9% |

|

Proposition 98 settle up |

0.0 |

|

Unfunded Retirement Liabilities—Pensionsb |

|

|

State and CSU employees |

7.5 |

|

School and community college employeesb |

7.5 |

|

UC employees |

7.3 |

|

Judges |

4.3 |

|

Unfunded Retirement Liabilities—Retiree Healthb |

|

|

State and CSU employees |

4.3 |

|

UC employees |

4.5 |

|

a Rate shown is growth in interest costs if all loans are repaid in 2017–18 rather than 2016–17. bOver the long run, retirement programs grow at a rate similar to the assumed rate of return on investments, holding other factors constant. |

|

Retirement Liabilities Have High Interest Rates. Left unaddressed, over the long run, retirement liabilities tend to grow at a rate similar to their assumption for investment returns. This is because when public employers delay action on unfunded retirement liabilities, employers lose another year of assumed investment returns, an amount which compounds over time. As such, retirement liabilities present significant long–term risks to the state budget.

Other Eligible Debts Have Low Interest Rates. Budgetary liabilities either accrue no interest or grow at comparatively low interest rates. For example, when the state repays special fund loans, the General Fund incurs interest on the loan. That interest is calculated based on the earnings rate of the state’s short–term savings account on the day that the loan was made. Interest rates were low when the state made many of these loans. As a result, interest owed on these loans is generally low. Similarly, the state does not pay interest on Proposition 98 settle up.

Different Groups Benefit From Addressing the Various Eligible Debts

The Legislature may want to consider how paying down Proposition 2 eligible debts would benefit certain groups—including taxpayers, schools, the UC, and special fund fee payers. Paying down all of the eligible debts would result in some benefits to at least one of these groups, but repaying some of these debts could have more benefits to some groups than others. As such, evaluating the distribution of these benefits among the various groups is also a consideration when prioritizing the repayment of the Proposition 2 eligible debts.

Paying Down Unfunded Liabilities Benefits Taxpayers. As we noted earlier, paying off higher–cost debts sooner results in future benefits for taxpayers, either in the form of lower taxes or more public services. For example, making additional contributions to retirement systems in the short run would reduce long–term costs of these programs. These savings would result in more money available in the long run for other state programs or for tax reductions. In the case of retirement benefits for state and CSU employees and judges, paying down unfunded liabilities reduces long–term state General Fund costs.

Paying Down Proposition 98 Settle Up and School Employee Unfunded Liabilities Benefits Schools. Paying down Proposition 98 settle–up obligations would result in one–time revenue for school and community college districts. This action would increase near–term budgetary flexibility for districts. Similarly, using Proposition 2 debt payment funds to address unfunded liabilities for school and community college employees could result in longer–term ongoing savings for districts. Addressing these retirement liabilities could also reduce future pressure on the state General Fund to provide additional support to schools and community colleges.

Paying Down UC Pensions and Retiree Health Benefits UC. Paying down UC’s unfunded liability for pensions and retiree health benefits would reduce UC’s long–term costs of providing these benefits. As with schools, this action would also increase budgetary flexibility for UC, possibly resulting in more funding for UC programs or lower tuition for future UC students. Using Proposition 2 debt payment funds to address UC’s retirement liabilities could also reduce pressure on the state’s General Fund to support UC operations in the future.

Paying Down Special Fund Loans May Benefit Special Fund Fee Payers. Repaying special fund loans increases the balance available in those funds. In some cases, those balances could be used to increase services or reduce fees. If this occurred, it would benefit the individuals and businesses that pay fees into and receive services financed by these funds.

Governor’s Proposal for Debt Payments

Proposition 2

Figure 4 shows the administration’s debt proposal for 2016–17 under Proposition 2.

Figure 4

Administration’s Proposition 2 Debt Proposal for 2016–17

(In Millions)

|

Proposed Debt Payment |

|

|

Special fund loans to the General Funda |

$1,128 |

|

Proposition 98 settle up |

257 |

|

University of California pensions |

171 |

|

Total |

$1,556 |

|

a Includes $64 million in interest on these loans. Also includes $173 million in repayments to Transportation Congestion Relief Fund, which the administration displays separately. |

|

Administration’s Proposition 2 Debt Proposal Focuses on Special Fund Loan Repayments. The administration’s proposal for debt payments under Proposition 2 focuses on special fund loan repayments. Specifically, in 2016–17, it uses $1.1 billion of the required $1.6 billion to repay special fund loans. As shown in Figure 5, the largest of these repayments are $308 million for the Unemployment Compensation Disability Fund, $173 million for the Transportation Congestion Relief Fund, and $112 million for the Off–Highway Vehicle Trust Fund. The total debt repayments also include $64 million in interest on special fund loans.

Figure 5

Proposed Special Fund Loan Repayments

(In Millions)

|

Fund Name |

Amount |

|

Unemployment Compensation Disability Fund |

$308 |

|

Transportation Congestion Relief Fund |

173 |

|

Off–Highway Vehicle Trust Fund |

112 |

|

Greenhouse Gas Reduction Fund |

100 |

|

School Land Bank Fund |

59 |

|

Harbors and Watercraft Revolving Fund |

51 |

|

Hospital Building Fund |

50 |

|

Oil Spill Response Trust Fund |

40 |

|

Housing Rehabilitation Loan Fund |

35 |

|

Accountancy Fund |

21 |

|

State Corporations Fund |

19 |

|

Tax Credit Allocation Fee Account |

13 |

|

State Board of Barbering and Cosmetology Fund |

11 |

|

Vehicle Inspection Repair Fund |

10 |

|

Enhanced Fleet Modernization Subaccount |

10 |

|

Other special fund loansa |

52 |

|

Subtotals, Proposed Repayments (Principal) |

($1,064) |

|

Interest on loans projected for repayment |

$64 |

|

Total Proposed Special Fund Repayments |

$1,128 |

|

a Includes 17 other special fund loan repayments, each under $10 million. |

|

Administration Also Proposes Paying Proposition 98 Settle Up. The Governor’s proposal for Proposition 2 debt payments includes funds for paying down Proposition 98 settle up. The proposed $257 million payment would reduce the total settle up owed to schools and community colleges to about $1 billion. These payments would be in addition to estimated growth in the minimum funding guarantee for schools and community colleges.

Administration Includes Debt Payments for UC Retirement Liabilities. The administration proposes payments of $171 million for unfunded liabilities related to UC employee pension benefits. The funds would represent the second year of a three–year agreement that requires the UC Regents to limit the amount of future employee salaries that may count toward UC employees’ pension benefits. Like the amounts included in the 2015–16 budget, these funds would only be released to UC after the UC Regents have made this change. The UC Regents have not yet taken this action. While the 2015–16 Budget Act did not set a deadline for this action, the administration has indicated it expects UC to make this change no later than June 30, 2016.

LAO Comments

Governor’s Proposal

Administration Generally Pays Down Low–Interest Debt in 2016–17. By using most of Proposition 2 required debt payments for special fund loans and Proposition 98 settle up, the administration’s debt proposal prioritizes low–interest debts in 2016–17. Two of these items, repayment of the Transportation Congestion Relief Fund loan and Proposition 98 settle up, carry no interest at all. Other special fund loans carry interest at a much lower rate than retirement liabilities.

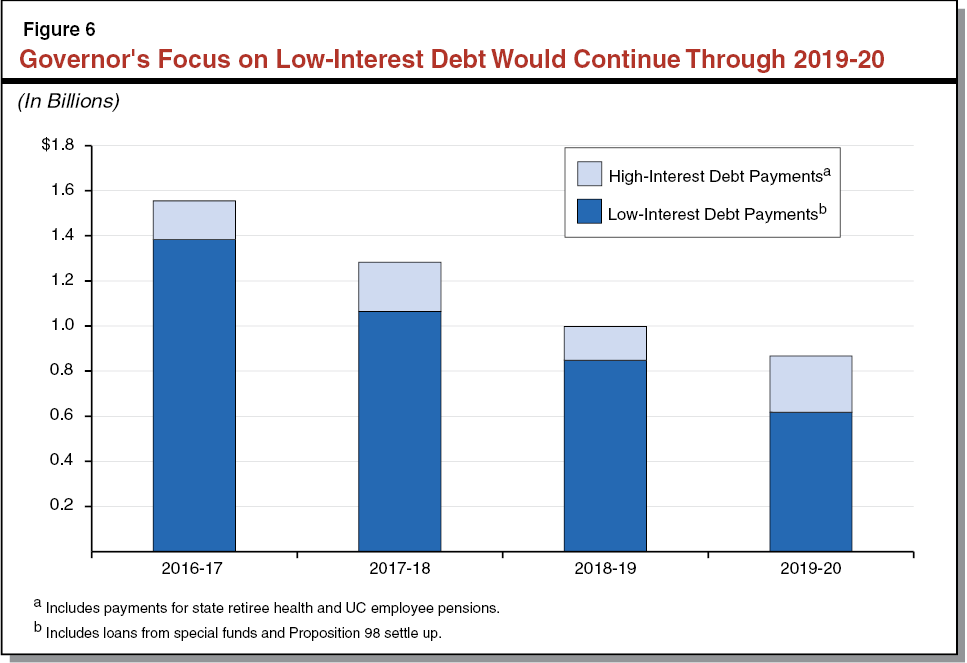

Focus on Low–Interest Debt Would Continue Through 2019–20. Figure 6 displays Proposition 2 debt payments under the administration’s multiyear budget forecast, categorized by interest costs. Over the next four fiscal years, the administration would continue to focus on low–interest debts, principally special fund loans and Proposition 98 settle up. Over the period, 83 percent of Proposition 2 debt payments would be directed to low–interest debt.

Schools Benefit From Governor’s Proposal. After a few years of large funding increases under Proposition 98, the Governor’s budget provides schools and community colleges a more modest increase in 2016–17. Proposition 98 settle up is provided on top of the minimum guarantee. As a result, the administration’s Proposition 2 proposal would provide a small benefit to schools and community colleges above their base increases in funding.

Special Fund Fee Payers Potentially Benefit From Governor’s Proposal. Repaying special fund loans could benefit special fund fee payers if increases in their balances were used to increase services or reduce fees. (The repayment of a loan provides a key opportunity for the Legislature to address how to deal with large fund balances.) However, it is not clear that these benefits would materialize. Specifically, while proposing repayment of special fund loans in recent years, the Governor and other administration officials have suggested that the state could borrow from these funds again when the state General Fund faces a shortfall. We suggest the Legislature ask the administration whether it plans to borrow from these funds again in the future rather than using the repayments to benefit fee payers.

Alternative Approach

Below, we outline an alternative approach that could produce more savings over the long run than the administration’s proposal.

Shift Attention Toward Unaddressed, High–Interest Liabilities. As we have noted, the state is already addressing some Proposition 2 eligible debts, while others merit further legislative attention. Meanwhile, the various Proposition 2 eligible debts carry different interest rates—and therefore different future costs. Proposition 2 presents an opportunity for the state to shift its attention toward the more costly of these liabilities. Addressing these types of liabilities could potentially result in billions of dollars more in long–term savings than the Governor’s multiyear Proposition 2 plan. As such, we suggest the Legislature consider placing a higher priority on unaddressed, high–interest liabilities.

Prioritize Funds for JRS I in Near Term. One unaddressed, high–interest liability that the Legislature may want to consider addressing in the short term is JRS I. Over the next few years, the Legislature could use Proposition 2 funds to eliminate the relatively small unfunded liability for JRS I. The long–term savings would be substantial. Based on information presented in the most recent JRS I actuarial valuation, a five–year plan to address the JRS I unfunded liability would cost $4 billion. Compared to the nearly $6 billion expected cost of the current pay–as–you–go approach, implementing this plan would save the state about $2 billion in the future. By year six of this plan, our alternative would likely free up about $200 million per year, which would be available for other legislative priorities.

Alongside JRS I, Address Debts That Benefit Special Fund Fee Payers, Schools, and UC. A five–year plan to address JRS I would cost about $800 million per year, leaving an average of several hundred million dollars per year in Proposition 2 debt payment funds. Over this period, the Legislature could use these funds to pay down any other eligible debt, including special fund loans, Proposition 98 settle up, and UC retirement liabilities. Paying down these debts could benefit special fund fee payers, schools and community colleges, and UC.

Prioritize Funds for Retiree Health in the Long Term. After retiring the JRS I unfunded liability, the Legislature could use Proposition 2 funds as part of a retiree health prefunding plan. Over the long run, investment returns would pay for a greater share of the cost of providing future retiree health benefits, substantially reducing the long–term costs of providing these benefits. Reducing and eventually eliminating unfunded liabilities for retiree health benefits could save taxpayers billions of dollars over the long term. Under our approach, the state would prefund retiree health liabilities using Proposition 2 and other funds without requiring the employee match sought by the Governor. As we describe below, our alternative could save more money than the Governor’s approach.

Our Alternative May Save More Than the Governor’s Approach. The Governor’s approach for prefunding retiree health benefits would produce long–term savings. Those savings, however, would likely be partially offset by increases in pay granted to employees in exchange for employees sharing in costs of prefunding the benefits. Compared to the Governor’s approach, our alternative that does not require an employee match may allow the state to address this problem at a lower cost. This approach may also preserve the state’s ability to change these benefits in the future. For more information on the Governor’s approach for prefunding retiree health benefits, see our March 2015 report, The 2015–16 Budget: Health Benefits for Retired State Employees.

Develop a Long–Term Plan. The approach we have outlined above is one of many possible approaches. We suggest the Legislature collaborate with the administration, state pension systems—including CalPERS, CalSTRS, and the UC Regents—and others to develop a long–term plan for Proposition 2 debt payment funds. Experts from these groups can present their case for how the state may best use Proposition 2 funds, informing the Legislature’s own priorities.

Conclusion

Long–Term Plan Needed. Proposition 2 requires the state to make minimum debt payments each year for 14 more years, resulting in roughly $15 billion to $20 billion (in today’s dollars) for paying down state debts. To maximize this opportunity, we advise the Legislature to develop a long–term plan for Proposition 2 debt payment funds. For example, as we outline here, one way to seize this opportunity would be to address unfunded liabilities for retiree health benefits for state and CSU employees and judges’ pensions. Together, these liabilities represent two of the few remaining liabilities for which the state does not have a plan in place.

LAO Approach Results in More Savings to Taxpayers. In this brief, we have outlined an approach that uses Proposition 2 debt payment funds to address two of the last remaining unaddressed, high–interest liabilities. Specifically, our alternative would address the JRS I unfunded liability over five years while leaving several hundred million dollars per year for paying down other eligible debts that could benefit special fund fee payers, schools and community colleges, and UC. In the longer term, we suggest using Proposition 2 as a part of a retiree health prefunding plan that does not require the employee match sought by the Governor. Compared to the Governor’s multiyear Proposition 2 debt plan, our alternative could save billions of dollars more over the long term while still maintaining some benefit for the groups mentioned above.

Many Approaches Are Reasonable. As we have noted, our approach is one of many possible approaches. Other approaches may save more for taxpayers or place more emphasis on benefits for certain groups. For example, some may point out that paying more toward the CalPERS unfunded liability would save the state more, in the long run, than our approach would. Others may want the state to focus less on debt payments that benefit the state General Fund and more on debt payments that benefit schools and UC. For example, using Proposition 2 funds to address UC’s retirement liabilities could, over the long run, result in more funding for UC programs, lower tuition, and reduce pressure on the state General Fund to support UC operations. These are all trade–offs the Legislature would want to consider as it develops a long–term plan.