April 4, 2018

The 2018-19 Budget

California's New Tax Departments

- Introduction

- Tax Administration and Appeals Prior to the New Laws

- Tax Administration and Appeals Under the New Laws

- 2018‑19 Budget Proposals

- Office of Tax Appeals in 2018‑19

Summary

New Laws Reorganized State Tax Agencies. In 2017, the Legislature passed two laws that made major changes to tax administration and appeals in California. Prior to these laws, the Board of Equalization (BOE) had administrative and appeals responsibilities for many taxes and fees. The laws created two new departments—the California Department of Tax and Fee Administration (CDTFA) and the Office of Tax Appeals (OTA)—and transferred most of BOE’s duties to these departments.

Governor Proposes $714 Million for These Tax Agencies in 2018‑19. The administration’s 2018‑19 budget proposal includes $30 million for BOE, $664 million for CDTFA, and $20 million for OTA. The Department of Finance has been reviewing some key components of these budgets and will report its findings to the Legislature this spring.

Administration Has Begun Establishing OTA. The new laws created OTA, transferring most of BOE’s tax appeal duties to the new office. This year, the executive branch has begun executing these new laws and establishing the new department. So far, OTA has determined its organizational structure; proposed an initial budget and size; established its physical locations in Sacramento, Fresno, and Los Angeles; and begun hearing tax appeal cases.

Introduction

In 2017, the Legislature passed two laws—AB 102 and AB 131—that made major changes to tax administration and appeals in California. The laws created two new departments—the California Department of Tax and Fee Administration (CDTFA) and the Office of Tax Appeals (OTA)—and transferred most of the Board of Equalization’s (BOE) duties to these departments. In this report, we summarize these changes and provide an update on OTA.

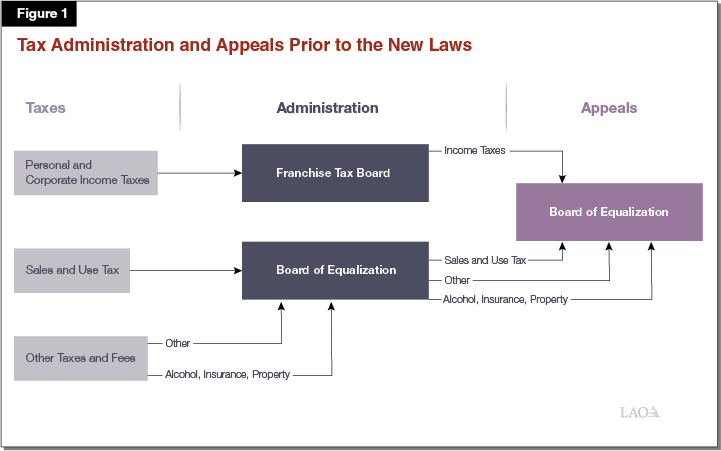

Tax Administration and Appeals Prior to the New Laws

State Tax System. The state collects revenue from a variety of taxes and fees. Most state revenue comes from three major sources—the personal income tax, the sales and use tax, and the corporation tax. The state also collects revenues from a variety of other taxes, including taxes on alcohol and on insurance. County governments in California administer the property tax, collecting the funds and distributing them to other local governments.

Tax Administration

BOE Administered Many Taxes and Fees. Prior to the new laws, BOE’s primary responsibility was to administer the sales and use tax (see Figure 1 below). It also administered dozens of smaller tax and fee programs, including some programs related to property taxes. BOE is headed by a five‑member board, with four members elected directly by district, and the fifth—the State Controller—elected on a statewide basis.

Franchise Tax Board (FTB) Administers Personal Income Tax and Corporation Tax. FTB administers personal income and corporate taxes and is headed by a three‑member board: the State Controller, the Director of Finance, and the chair of the BOE. In 2016‑17, FTB had a budget of $758 million and 6,167 full‑time equivalent (FTE) employees.

Tax Appeals

Taxpayers Can Appeal Decisions. When taxpayers disagree with the state about the taxes they owe, they can appeal. In the initial steps of the appeal process, taxpayers interact with the same agency that administered the disputed tax. If these initial steps do not resolve the disagreements, taxpayers can have their appeals heard by a quasi‑judicial body.

BOE Heard Tax Appeals. Prior to the new laws, BOE was the quasi‑judicial body that heard appeals for state tax programs. The five‑member board presided over appeals hearings and ruled on appeals by a majority vote of the board. Taxpayers who disagreed with the board’s decisions could have their appeals heard in the trial courts. Tax administration agencies, however, could not appeal the board’s decisions.

Concerns About BOE

Longstanding Concerns. BOE’s structure combines specific features of the legislative, executive, and judicial branches of government. BOE is like the legislative branch in the sense that geographically distinct districts elect the board members. However, BOE must carry out activities prescribed by the Legislature—a feature typically associated with the executive branch. At the same time, the board must resolve disputes over the application of laws—a judicial function. Due to the conflicts inherent in this structure, our office and others long expressed concerns about BOE’s ability to operate effectively. For example, our analysis of the 1949‑50 Budget Bill noted inconsistencies in tax administration among board members’ districts.

Recent Concerns. In recent years, various audits, evaluations, hearings, and other inquiries have indicated a variety of problems with BOE’s operations, including actions that were not consistent with legislative directives. For example, an evaluation by the Department of Finance found that board members routinely supplemented their personal staff by redirecting BOE employees who were supposed to be performing other tasks, such as audits.

BOE Established in State Constitution . . . The State Constitution sets up BOE’s basic structure, including its elected officers. The Constitution also establishes BOE’s authority over assessment and collection of the alcoholic beverage tax, assessment of the insurance tax, and several aspects of property taxes.

. . . But Most Duties Were Statutory. Prior to the new laws, state statute assigned most of BOE’s roles, including the largest one—administering the sales and use tax. State statute also gave BOE the authority to hear appeals of state taxes and fees.

Tax Administration and Appeals Under the New Laws

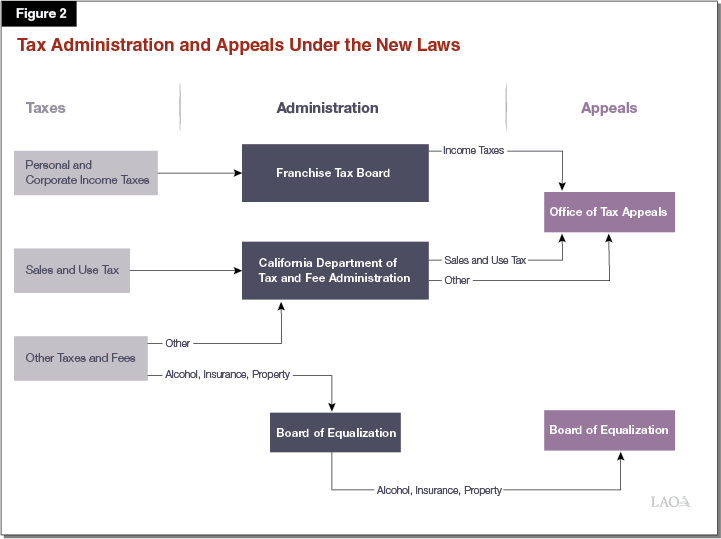

Laws Transferred BOE’s Statutory Duties to New Departments. In June 2017, the Legislature passed and the Governor signed AB 102. This law created two new departments—CDTFA and OTA—and transferred all of BOE’s statutorily assigned duties to these new departments. The law did not amend the State Constitution, so BOE maintained its constitutional authority over taxes on alcoholic beverages, insurance, and property (see Figure 2). The law did not make any changes to FTB. In September 2017, the Governor signed AB 131, which further clarified some of the changes made by AB 102.

Tax Administration

CDTFA. Under the new laws, CDTFA administers most of the tax and fee programs formerly administered by BOE. Accordingly, the new laws transferred most of BOE’s budget, staff, facilities, and other resources to CDTFA. CDTFA is a department within the Government Operations (GovOps) Agency. The head of the department is a director appointed by the Governor and confirmed by the Senate.

Tax Appeals

OTA. The new laws also created OTA, transferring most of BOE’s tax appeal duties to the new office. OTA is now responsible for hearing tax appeal cases formerly assigned by statute to BOE, including personal income, franchise, and sales tax appeals. Unlike CDTFA, OTA is not part of a state agency. Like CDTFA, however, the head of the department is a director appointed by the Governor and confirmed by the Senate. OTA’s director reports directly to the Governor.

New Laws Funded OTA in 2017‑18. The new laws appropriated $5 million in 2017‑18 to establish OTA. The new laws also gave the administration the authority to augment this appropriation using a transfer of funds from BOE’s budget to OTA’s budget with notification to the Legislature. The administration notified the Legislature it was making such a transfer of $2.2 million in February, bringing OTA’s total budget for 2017‑18 to more than $7 million.

New Laws Directed OTA to Hear Appeals in Three Offices. The new laws directed OTA to hear cases in tax appeals panels, each consisting of three administrative law judges (ALJs). These panels are to hear cases in three locations: Sacramento, Fresno, and Los Angeles. The laws also directed OTA to issue a written opinion for each case decided by the panels within 100 days. Similar to the process that existed with BOE, the laws allowed taxpayers to appeal decisions made by OTA to the trial courts.

2018‑19 Budget Proposals

The administration proposes $714 million in total funds in 2018‑19 to support 4,554 FTE employees at the three tax agencies reorganized in the 2017‑18 budget. As a single entity, in 2016‑17, BOE had a budget of $617 million and 4,716 FTE employees.

BOE

Administration Proposes $30 Million and 204 FTE Employees for BOE in 2018‑19. The administration proposes $30 million in General Fund spending and 204 FTE for BOE in 2018‑19. This proposal amounts to five percent of BOE’s 2016‑17 budget.

Report on Board Members’ Staff. The 2017‑18 Budget Act directed the Department of Finance to report to the Joint Legislative Budget Committee by April 1, 2018 regarding the ongoing staffing needs of the board members. Our office will comment on this report in upcoming budget hearings.

Some Programs Administered by CDTFA. Under a memorandum of understanding, CDTFA administers the alcoholic beverage tax and the insurance tax on behalf of BOE. These programs—listed under CDTFA’s budget—account for nearly $4 million and 21 FTE employees.

CDTFA

Administration Proposes $664 Million and 4,270 FTE Employees for CDTFA in 2018‑19. The administration proposes $664 million ($354 million General Fund) in funding and 4,270 FTE employees for CDTFA. This proposal includes $70 million for an ongoing large‑scale information technology (IT) project.

Administration Conducting Mission‑Based Review. The Department of Finance is currently conducting a mission‑based review of CDTFA’s administration of the sales and use tax. Such reviews examine state programs in greater depth than the standard budget process. The goal of these reviews is to align programs’ activities and use of resources as closely as possible with their core missions. At this time, it is unclear whether the sales and use tax review will lead to any proposals—such as new statutes or changes in CDTFA’s budget—that would require formal legislative action. Even if such action is not required, the review presents an opportunity for legislative oversight of the new department.

OTA

Administration Proposes $20 Million and 80 FTE Employees for OTA in 2018‑19. The administration proposes $20 million in General Fund spending for OTA in 2018‑19. The budget includes nearly $12 million to support the salaries and benefits of 80 FTE employees and around $8 million for operating expenses and equipment. About $2 million of these funds are dedicated for one‑time purposes, such as purchasing furniture and making office modifications.

Office of Tax Appeals in 2018‑19

In this section, we provide updates for the Legislature on how the administration is interpreting the law as it establishes and begins operations in OTA.

Organization and Staffing

OTA Organized Into Five Divisions. OTA plans to organize its 80 staff members into five divisions. They are:

- Executive. This division, which includes the director and chief counsel, leads and directs OTA.

- Hearing. This division includes the ALJs—the personnel most directly involved in carrying out the department’s core mission of hearing tax appeals.

- Foundation. This division consists primarily of tax counsels, who will primarily provide case research for the hearings.

- Case Management. This division provides other support functions for the hearings, including setting the hearing calendar for tax appeals.

- Administrative. This division provides fiscal oversight and performs personnel management, IT, and business service functions.

OTA Has Hired 20 ALJs, Including Two Presiding ALJs. OTA has hired 20 ALJs, including two presiding ALJs. These ALJs will form a number of “fluid” panels so that the same three individuals do not always hear cases together. The presiding ALJs will perform both management and review functions for other ALJs (and occasionally will hear cases by sitting on the panels). The review functions will include reading cases for consistency across decisions and clarity. Through this review process, OTA aims to ensure consistency in decisions across panels.

Panels Will Issue Written Opinions. The panels of ALJs will issue a written opinion on each case within 100 days of hearing that case. In order to issue an opinion, at least two of the three panel members must concur in the holding of the opinion. Both taxpayers and the state are permitted to submit a petition for a rehearing in the event of an irregularity, accident, new evidence, or if the party can demonstrate there was insufficient evidence to justify the decision. Under law, taxpayers, but not the state, may also appeal decisions made by OTA to the trial courts.

OTA Plans to Hear Cases in Three Offices, But Have Permanent Staff in Two. As required by law, OTA will hear cases in three locations in the state: Sacramento, Fresno, and Los Angeles. The Sacramento office will serve as OTA’s headquarters, where the executive division staff, 12 ALJs, and 1 presiding ALJ (among other staff) will work. The remaining staff, including six ALJs and one presiding ALJ will be located in Los Angeles. The Fresno office will have a venue for panels to hear cases, but right now, OTA does not plan to have any staff permanently located in this office. For cases to take place in Fresno, ALJs (and occasionally other staff) from the other offices will travel to Fresno.

Executive Team Will Not Be Directly Involved in Hearings. Under law, the director of OTA is prohibited from directing, overseeing, supervising, or otherwise being involved in the decision‑making process of the tax appeals panels. OTA has indicated that the hearing division will maintain this independence. However, the management structure of OTA will nonetheless intertwine the executive and hearing divisions. For example, the presiding ALJs will report to the chief counsel and the director. OTA also states that the chief counsel will read the written opinions of the panels and review them for consistency and clarity, but will not be involved in the decision‑making process. The director will only read cases after they are published.

Workload

OTA Began Hearing Cases in January 2018. The new laws directed OTA to begin hearing cases on January 1, 2018 and prohibited BOE from conducting appeals or taking an action with respect to appeals after that date. OTA held its first hearings in Sacramento on January 22 and 23 and in Los Angeles on March 28. OTA plans to begin hearing cases at its Fresno office in the early fall of 2018.

OTA Faces an Active Backlog of Cases. OTA believes it will receive a total backlog of approximately 2,200 cases from BOE, although about 1,200 of the cases received so far are active (meaning OTA is able to take action on the case). This active backlog represents about a year of typical case workload. OTA has indicated it intends to prioritize working down the backlog of active cases.

OTA Currently Has 28 Vacancies. OTA has 28 vacancies and is actively recruiting or interviewing for 22 of those vacant positions. These vacancies are concentrated in the Los Angeles office.