October 17, 2019

The 2019‑20 Budget: California Spending Plan

Debt and Liabilities

Introduction

Three Primary Types of Debts and Liabilities. California’s debts and liabilities fit into three broad categories:

- Retirement Liabilities. As discussed below, California has unfunded liabilities associated with pension benefits for judges and state employees, retiree health benefits, and the state’s share of pension benefits for the state’s teachers and school administrators.

- Budgetary Borrowing. For the purposes of this post, these are the debts the state has incurred in the past to address its budget problems. These include loans from other state funds to the General Fund and outstanding obligations to other entities, like cities, counties, and school and community college districts.

- Bond Debt. These liabilities include the principal and interest amount of outstanding general obligation and lease revenue bonds issued by the state to finance capital infrastructure.

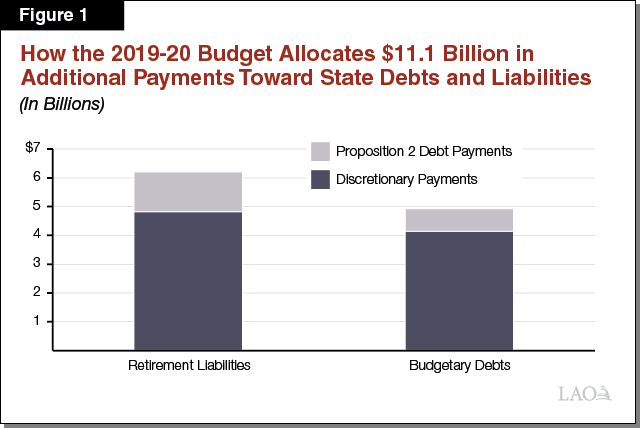

Budget Package Repays $11.1 Billion in Debts and Liabilities in 2019‑20. The annual budget pays down several billion dollars of liabilities each year under set constitutional and statutory repayment schedules. These include, for example, billions of dollars in debt service on government obligation bonds. In addition to these routine payments, the 2019‑20 budget package makes significant additional payments toward paying down debts in liabilities in two of these categories: retirement liabilities and budgetary borrowing. Altogether, as Figure 1 shows, the budget makes $11.1 billion in outstanding debts and liabilities repayments, falling into two categories:

- Discretionary Payments. The spending plan uses $9 billion in discretionary General Fund money (funding that could be used for any public purpose) to pay down debts and liabilities. Of this total, the spending plan allocates $4.8 billion to paying down retirement liabilities and $4.1 billion toward budgetary debts.

- Proposition 2 Payments. The spending plan also allocates $2.2 billion in required Proposition 2 (2014) debt payments among various purposes. The total amount of these payments is set by a constitutional formula under the provisions of Proposition 2, but the Legislature can make choices about how much of that funding to allocate among different allowable uses. Of this total, the spending plan allocates $1.4 billion to paying down retirement liabilities and $781 million toward budgetary debts.

This post describes the actions the 2019‑20 budget took in these areas in more detail.

Retirement Liabilities

State Payments Towards State Liabilities

State Has Large Retirement Liabilities. An unfunded liability exists when actuaries determine that—after accounting for various actuarial assumptions about the future—there are insufficient assets on hand to pay benefits that have been earned to date. As of June 30, 2018, the state has large unfunded liabilities associated with pensions for state employees (administered by CalPERS) and teachers (administered by CalSTRS) and retiree health benefits earned by state employees.

- Pensions. Between the two pension systems, the state’s pension unfunded liabilities are estimated to total $93.1 billion ($59.7 billion at CalPERS for state employee pensions and $33.4 billion at CalSTRS for teachers’ pensions). These pension unfunded liabilities largely are due to (1) historical contributions being below recommended amounts, (2) past actual investment returns being lower than actuaries assumed, and (3) changes to actuarial assumptions (for example, assuming that people will live longer and that the system’s investment returns will be lower in the future).

- Retiree Health. Whereas the state has prefunded pension benefits for many decades, the state only recently began setting money aside to prefund retiree health benefits. Actuaries estimate that the state has only $874.3 million in assets for a liability of $86.5 billion—meaning the state has an unfunded retiree health liability of $85.6 billion.

Supplemental Payments to Retirement Liabilities. A supplemental payment is a contribution to prefund a retirement benefit that is above what otherwise would be contributed. As discussed below, the 2019‑20 budget package made a number of supplemental payments to reduce the state’s retirement unfunded liabilities. (In addition, as we discuss elsewhere, the budget directs state funds to reduce school districts’ unfunded liabilities at CalSTRS and CalPERS.)

- $2.8 Billion General Fund Payment to CalPERS Over Four Fiscal Years. Chapter 33 of 2019 (SB 90, Committee on Budget and Fiscal Review) appropriates a General Fund supplemental payment to CalPERS in 2018‑19 ($2.5 billion), 2020‑21 ($265 million), 2021‑22 ($200 million), and 2022‑23 ($35 million). (The payment made in 2018‑19 is part of the 2019‑20 budget package, but was attributed to 2018‑19 for budgetary purposes.) Chapter 33 specifies that these supplemental payments be apportioned based on a pension plan’s share of the state’s General Fund contribution to CalPERS. Accordingly, the money would be apportioned so that 55 percent went to the Peace Officer/Firefighter pension benefit, 34 percent to the Miscellaneous pension benefit, 7 percent to the Safety pension benefit, and 3 percent to the Industrial pension benefit. Legislation ratifying the memorandum of understanding (MOU) between the state and Bargaining Unit 5 (Highway Patrol)—Chapter 859 (AB 118, Committee on Budget)—changed the 2020‑21 supplemental payment so that $243 million General Fund goes to the Highway Patrol pension benefit and $22 million is apportioned as described above, based on General Fund annual contributions to CalPERS.

- Payments to Highway Patrol Pensions. In addition to directing $243 million of the 2020‑21 General Fund supplemental payment established by Chapter 33 to the Highway Patrol pension benefit, the Unit 5 MOU also establishes two other supplemental payments to the Highway Patrol pension benefit. First, in each of the four fiscal years of the MOU (2019‑20, 2020‑21, 2021‑22, and 2022‑23), the Motor Vehicle Account will contribute $25 million—totaling to $100 million over the four years—to the highway patrol retirement benefit. The agreement specifies that the Director of Finance has the “sole discretion” to determine if there are sufficient revenues to make the scheduled payments in 2021‑22 and 2022‑23. Second, the MOU redirects about one-half of 1 percent of highway patrol officer pay during the term of the agreement as a supplemental employer pension payment to the highway patrol benefit. Over the four fiscal years, the administration estimates that this will result in about $22 million being contributed to the pension benefit above what otherwise would be contributed.

- Payments to State Unfunded Liabilities at CalSTRS. Chapter 33 appropriates additional General Fund money in 2019‑20 through 2022‑23 as a supplemental payment to the state’s unfunded liabilities at CalSTRS (these payments are counted toward the state’s Proposition 2 debt payment requirements). In 2019‑20, the budget appropriates $1.1 billion for this purpose. In the future years, the appropriation amount will depend on the annual Proposition 2 requirement, which in large part depends on state revenue performance; however, the administration assumes the state will pay $1.8 billion in these future years.

State Payments Towards School Districts’ Liabilities

Payments That Supplement School District Pension Contributions. School districts also have large unfunded retirement liabilities. The spending plan seeks to reduce these liabilities by using state General Fund money to pay down school districts’ liabilities. These state payments are supplemental payments, meaning that they are in addition to what otherwise would be contributed to the systems. Specifically, the spending plan provides about $1.6 billion towards school districts’ CalSTRS unfunded liabilities and $660 million towards school districts’ CalPERS unfunded liabilities.

Pays a Portion of Districts’ Pension Costs for the Next Two Years. The spending plan also provides additional monies to school districts by paying a portion of districts’ pension costs for the next two years. Specifically, the budget provides $606 million for the state to pay a portion of districts’ CalSTRS costs and $244 million for the state to cover a portion of districts’ CalPERS costs. These payments supplant—rather than supplement—existing pension contributions, meaning they do not reduce the state’s or districts’ outstanding debt but rather offset what districts otherwise would pay. (We describe these payments in more detail in our post The 2019‑20 Spending Plan: Education.)

Budgetary Borrowing

The spending plan made significant progress in addressing remaining budgetary borrowing amounts that fall into three categories: (1) deferrals, (2) special fund loans, and (3) settle up. This section describes each of the actions taken in this regard.

Deferrals

To address budgetary shortfalls, at various points, the state made adjustments to expenditure accounting to push costs into different fiscal years, providing a temporary budgetary benefit.

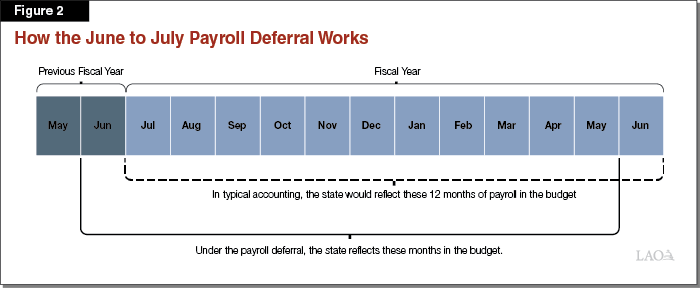

Background on the Payroll Deferral. The state pays its employees monthly. The 2009‑10 budget package included an ongoing one-month deferral of state payroll from June to early July, providing savings for the state. This action was only reflected in the state’s accounting reports—it did not affect when paychecks were actually issued to state employees. On an ongoing basis, the state’s budget documents still reflected 12 months of payroll, but rather than reflecting payroll for June of the last month of the fiscal year, they reflect June of the previous fiscal year. Figure 2 shows how this works. (For budgetary purposes, the state only recognized the deferral in the General Fund, not other funds’ statements.)

Cost to Undo the Payroll Deferral. In the first year a deferral is made, it results in significant savings for the state because the state only pays the partial cost of a year’s expense. For example, in the case of the payroll deferral, the state only reflected 11 months of payroll in the 2009‑10 budget, providing hundreds of millions of dollars in budgetary savings. Undoing this deferral, conversely, means the state must reflect an additional month of payroll—13 months—in a budget, carrying an additional cost. The spending plan allocated $707 million General Fund to undo the payroll deferral. (There were no budgetary special fund costs associated with undoing this deferral.)

Background on the Pension Deferral. The state makes quarterly payments to CalPERS for pension contributions for state employees. The state pays the fourth-quarter contribution to CalPERS in the first quarter of the subsequent fiscal year. (Our office has not been able to discover the year this deferral was first done.) This means the state makes the transfer in the first few days of July. This deferral only applies to the state’s General Fund pension payments—other funds’ fourth-quarter CalPERS payments are paid in June.

Cost to Undo the Pension Deferral. Undoing the pension deferral requires transferring funds to CalPERS at the end of June instead of July. The spending plan allocated $973 million General Fund to undo the pension deferral. (There were no special fund costs associated with undoing this deferral.)

Special Fund Loans

Throughout the 2000s, particularly in response to the dot-com bust and Great Recession, the state loaned amounts to the General Fund from other state accounts, particularly special funds to address General Fund budget problems. The General Fund is required to repay special funds when needed to ensure special funds can meet the objectives for which they were created. Courts have given the Legislature latitude in making determinations about when to repay special funds under this standard.

Recent History of Special Fund Loan Repayments. The state has been making significant repayments toward special fund loans since 2013‑14. (Before this period, repayments were generally made to address special fund needs, not to significantly pay down the balance.) At the beginning of that fiscal year, the state owed over $5 billion in outstanding special fund loans. (This amount excludes weight fee loans as described later in this section.) After Proposition 2 passed in 2014, the state had a dedicated funding source with which to address these outstanding loans and repayments accelerated. In 2015‑16, for example, the state made nearly $1.4 billion in special fund loan repayments.

State Fully Repays All Outstanding Special Fund Loans in 2019‑20. The spending plan fully repays all outstanding special fund loans to the General Fund. Although recent budgets have repaid special fund loans using constitutionally required debt payments under the provisions of Proposition 2, the spending plan uses $1.3 billion in general purpose General Fund monies to repay these outstanding loans. (This figure also includes repayments to the Transportation Congestion Relief Fund, which are not displayed in the totals Figure 1.)

Weight Fees Loans—a Unique Type of Special Fund Loan—Also Are Fully Repaid. In addition, the spending plan uses $886 million to fully repay all outstanding weight fee loans to the General Fund. In 2011, budget-related legislation redirected weight fee revenues to fund bond debt service for transportation-related bonds. Initially, the amount of revenues exceeded the debt service costs and the state loaned that excess to the General Fund. Over time, debt service costs have increased such that they now exceed weight fee revenues. The General Fund has been repaying the loans by paying that difference (the state has also been counting these repayments toward required Proposition 2 debt payments). This year, the spending plan repays the entire outstanding amount of the weight fee loans by setting aside general purpose General Fund monies.

Settle-Up Obligations

Under Certain Conditions, State Creates a Proposition 98 “Settle-Up” Obligation. Proposition 98 sets a minimum funding level for schools and community colleges. The minimum required funding level is based on a series of formulas that depend on numerous factors. Most of the underlying factors are updated after adoption of the budget, and, in most cases, those changes result in changes to the minimum required funding level. When the final required funding level is higher than the initial budgeted estimate, the state is required to settle up—making an additional appropriation to schools and colleges.

State Repays All Outstanding Settle-Up Obligations in 2019‑20. Sometimes the state settles up as a fiscal year is ending, but other times, the state does not settle up immediately. In the latter cases, the state creates an outstanding fiscal obligation known as a settle-up obligation. At the beginning of 2019‑20, the state had $687 million in total outstanding settle up remaining. The 2019‑20 budget package repays all of this outstanding settle up. Of this total, the state counts $391 million toward required debt payments under Proposition 2. (A provision of Proposition 2 defined all settle-up obligations created prior to 2014‑15 as allowable debt payments.)