The 2020-21 Budget:

California's Fiscal Outlook

See a list of this year's fiscal outlook material, including the core California's Fiscal Outlook report, on our fiscal outlook budget page.

LAO Contact

November 20, 2019

The 2020-21 Budget

The Fiscal Outlook for

Schools and Community Colleges

- Introduction

- Background

- 2018‑19 and 2019‑20 Updates

- 2020‑21 Estimates

- Outlook Through 2023‑24

- Key Issues for Consideration

- Appendix

Summary

Relatively Strong Growth Projected in School and Community College Funding. Each year, the state calculates a “minimum guarantee” for school and community college funding based upon a set of formulas established by Proposition 98 (1988). Under our outlook, the 2020‑21 minimum guarantee is up $3.4 billion (4.2 percent) over our revised estimate of the 2019‑20 guarantee. The state could use $1.1 billion of this increase to cover a 1.79 percent statutory cost‑of‑living adjustment (COLA) for school and community college programs and changes in student attendance. The state also would be required to deposit $350 million into the Proposition 98 Reserve. After accounting for these and other adjustments, we estimate the state would have $2.1 billion available for new commitments in 2020‑21.

Legislature Faces Key Trade‑Offs in Upcoming Budget Decisions. The statutory COLA rate is relatively low compared with the cost pressures that districts are facing. If the Legislature were to provide no other ongoing increase in general purpose funding, most districts likely would need to dedicate nearly all of the increase to covering their higher pension costs. The Legislature could help districts address these cost pressures by using a portion of the $2.1 billion for a larger COLA. Alternatively, the Legislature could take a more targeted budget approach—for example, equalizing per‑student funding rates for special education (an area of longstanding legislative concern). The Legislature also could consider prioritizing one‑time spending. In part because certain indicators suggest the chances of an economic slowdown are higher than normal, we encourage the Legislature to set aside at least half of the $2.1 billion for one‑time spending. This approach creates a buffer that helps protect ongoing programs in case the guarantee drops in 2020‑21 or 2021‑22. Using one‑time funding to pay down districts’ pension liabilities more quickly would be particularly beneficial, as these payments would improve the funding status of the pension systems and likely reduce district costs on a sustained basis.

Introduction

Report Provides Our Fiscal Outlook for Schools and Community Colleges. State budgeting for schools and the California Community Colleges is governed largely by Proposition 98 (1988). The measure establishes a minimum funding requirement for K‑14 education commonly known as the minimum guarantee. This report examines how the minimum guarantee might change over the coming years. The report has five parts. First, we explain the formulas that determine the minimum guarantee. We then explain how our estimates of Proposition 98 funding in 2018‑19 and 2019‑20 differ from the estimates included in the June 2019 budget plan. Next, we estimate the 2020‑21 guarantee. Fourth, we explain how the minimum guarantee could change through 2023‑24 under two possible economic scenarios. Finally, we identify the amount of funding that would be available for new spending commitments in the upcoming year and describe some issues for the Legislature to consider as it prepares to allocate this funding. (The 2020‑21 Budget: California’s Fiscal Outlook contains an abbreviated version of our Proposition 98 outlook, along with the outlook for other major programs in the state budget.)

Background

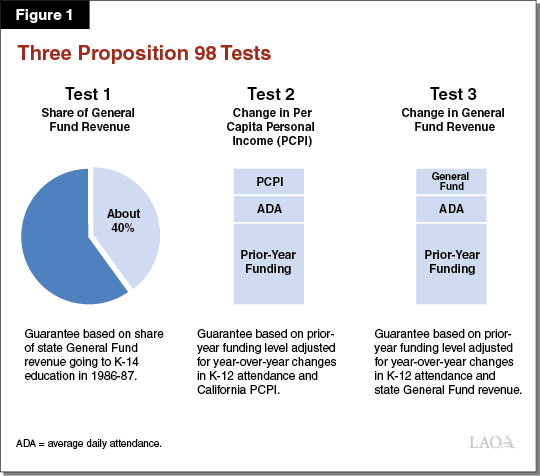

Minimum Guarantee Depends Upon Various Inputs and Formulas. The California Constitution sets forth three main tests for calculating the minimum guarantee. Each test has certain inputs. The most notable inputs are student attendance, per capita personal income, and per capita General Fund revenue (Figure 1). Whereas Test 2 and Test 3 build upon the amount of funding provided the previous year, Test 1 links school funding to a minimum share of General Fund revenue (about 40 percent). The Constitution sets forth rules for comparing the tests, with one of the tests becoming operative and used for calculating the minimum guarantee that year. The state meets the guarantee through a combination of General Fund and local property tax revenue. Although the state can provide more funding than required, in practice it usually funds at or near the guarantee. With a two‑thirds vote of each house of the Legislature, the state can suspend the guarantee and provide less funding than the formulas require that year.

Legislature Decides How to Allocate Proposition 98 Funding. Whereas Proposition 98 establishes a total minimum funding level, the Legislature decides how to allocate this funding to specific school and community college programs. Since 2013‑14, the Legislature has allocated most funding for schools through the Local Control Funding Formula (LCFF). A school district’s allotment under this formula depends on its size (as measured by student attendance) and the share of its students who are low income or English learners. Regarding community colleges, the Legislature allocates most funding through apportionments. A college’s apportionment funding depends on its enrollment, share of low‑income students, and performance on certain outcome measures. The LCFF and apportionments are the primary sources of general purpose funding for schools and community colleges. In the 2019‑20 budget plan, the Legislature allocated 85 percent of all Proposition 98 funding through these two formulas. It allocated the remaining 15 percent for targeted purposes, such as providing services to students with disabilities.

At Key Points, State Recalculates Minimum Guarantee and Certain Proposition 98 Costs. The guarantee typically changes from the level initially assumed in the budget act as a result of updates to the relevant Proposition 98 inputs. The state continues to update Proposition 98 inputs for up to nine months after the close of a fiscal year. The state also revises its estimates of certain school and college costs, including LCFF and apportionments. When student attendance estimates change, for example, the cost of funding LCFF tends to change in tandem.

Growth in K‑12 Funding Is Now Directly Linked to Growth in the Minimum Guarantee. When the minimum guarantee is growing, the state generally funds a cost‑of‑living adjustment (COLA) for LCFF, community college apportionments, and certain other education programs. The COLA rate is based on a national price index designed to reflect the cost of goods and services purchased by state and local governments across the country. As part of the 2019‑20 budget package, the state adopted a new policy of automatically reducing the COLA rate for K‑12 programs under certain conditions. Specifically, for years in which growth in the Proposition 98 minimum guarantee is insufficient to cover the statutory COLA for these programs, the COLA is to be reduced to fit within the guarantee. Though statute is silent on what might happen to community college programs, the COLA rate for these programs also likely would be affected.

State Recently Made First Deposit Into Proposition 98 Reserve. Proposition 2 (2014) created a state reserve specifically for schools and community colleges—the Public School System Stabilization Account (Proposition 98 Reserve). Proposition 2 requires the state to make deposits into this reserve when a series of conditions are met. These conditions are relatively restrictive (see the nearby box). Despite consistent increases in the minimum guarantee over the past several years, the state did not make any deposits into the Proposition 98 Reserve from 2014‑15 through 2018‑19. In 2019‑20, the state met all of the conditions for the first time—making a deposit of $377 million. In the coming budget cycle, the state will adjust the amount of the 2019‑20 deposit when it updates the relevant inputs.

Key Rules Governing the Proposition 98 Reserve

Below, we describe the rules governing Proposition 98 Reserve deposits and withdrawals.

Deposits Predicated on Four Main Conditions. To determine whether a deposit is required, the state first determines whether all of the following conditions are met:

- Revenues From Capital Gains Are Relatively Strong. Deposits are required only when the state receives an above‑average amount of revenue from taxes paid on capital gains (a relatively volatile source of General Fund revenue).

- Test 1 Is Operative. Test 1 years historically have been associated with relatively strong growth in the minimum guarantee due to strong growth in state revenue.

- Formulas Are Not Suspended. If the Governor declares a “budget emergency” (based on a natural disaster or slowdown in state revenues), the Legislature can reduce or cancel a Proposition 98 Reserve deposit. Additionally, if the Legislature votes to suspend the minimum guarantee, any required deposit is automatically canceled.

- Obligations Created Before 2014‑15 Are Retired. Proposition 2 (2014) specified that no deposits would be required until the state paid certain school funding obligations (known as “maintenance factor”) that it accrued during the Great Recession. The state met this condition starting in 2019‑20.

Amount of Deposit Depends Upon Additional Formulas. If the state determines that the conditions for a deposit are satisfied, it performs several calculations to determine the size of the deposit. Generally, the size of the deposit tends to increase when revenue from capital gains is relatively high and the guarantee is growing quickly relative to inflation. More specifically, the deposit equals the lowest of the following four amounts:

- The Portion of the Guarantee Attributable to Above‑Average Capital Gains. The state calculates what the Proposition 98 guarantee would have been if the state had not received any revenue from capital gains in excess of the historical average. Deposits are capped at the difference between the operative guarantee and the hypothetical alternative guarantee without the additional capital gains.

- The Difference Between the Test 1 and Test 2 Levels. Deposits are capped at the difference between the higher Test 1 and lower Test 2 funding levels.

- Growth Relative to the Prior Year. The state calculates how much funding schools and community colleges would receive if it adjusted the previous year’s funding level for changes in student attendance and inflation. (The inflation factor is the higher of the statutory cost‑of‑living adjustment or growth in per capita personal income.) Deposits are capped at the difference between the Test 1 funding level and the inflation‑adjusted prior‑year funding level.

- Room Available Under a 10 Percent Cap. The Proposition 98 Reserve has a cap equal to 10 percent of all funding allocated to schools and community colleges. Deposits are only required to the extent the existing balance is below this threshold.

Withdrawals Required When Guarantee Is Growing Relatively Slowly. Proposition 2 requires the state to withdraw funds from the Proposition 98 Reserve if the minimum guarantee is not growing quickly enough to support the prior‑year funding level, as adjusted for student attendance and inflation.

2018‑19 and 2019‑20 Updates

Higher Revenues Across 2018‑19 and 2019‑20. Compared to the estimates underlying the June 2019 budget package, we estimate revenues from the state’s three largest taxes—the personal income tax, the corporation tax, and the sales tax—are up almost $1 billion in 2018‑19 and about $160 million in 2019‑20. The increase in 2018‑19 is largely driven by higher than anticipated personal income tax collections. The increase in 2019‑20 is smaller because wage growth and quarterly estimated payments from higher‑income earners have been slower thus far this fiscal year.

Proposition 98 Minimum Guarantee Revised Up in 2018‑19 but Down in 2019‑20. Compared with the estimates included in the June 2019 budget plan, we estimate that the minimum guarantee has increased $194 million in 2018‑19 and decreased $185 million in 2019‑20 (Figure 2). The increase in 2018‑19 is due primarily to our estimate of higher General Fund revenue. The decrease in the 2019‑20 guarantee is due to our estimate of lower local property tax revenue. (When Test 1 is operative, as it is in 2019‑20, changes in local property tax revenue directly affect Proposition 98 funding. In these years, changes in property tax revenue do not offset General Fund spending.) Our lower property tax estimate mainly reflects reductions in the amount of associated funding shifted from cities, counties, and other local governments to schools and community colleges.

Figure 2

Updating Prior‑ and Current‑Year Estimates of the Minimum Guarantee

(In Millions)

|

2018‑19 |

2019‑20 |

||||||

|

June Budget Plan |

November LAO Estimates |

Change |

June Budget Plan |

November LAO Estimates |

Change |

||

|

Minimum Guarantee |

|||||||

|

General Fund |

$54,445 |

$54,617 |

$172 |

$55,891 |

$55,985 |

$95 |

|

|

Local property tax |

23,701 |

23,723 |

22 |

25,166 |

24,886 |

‑280 |

|

|

Totals |

$78,146 |

$78,340 |

$194 |

$81,056 |

$80,871 |

‑$185 |

|

|

Operative Test |

2 |

1 |

Yes |

1 |

1 |

No |

|

School and Community College Spending Down in 2018‑19 and 2019‑20. For the prior year and current year, we also update our estimates of costs for LCFF and other Proposition 98 programs (Figure 3). For 2018‑19, the latest available data show that costs are down slightly ($32 million) from the estimates included in the June budget package. For 2019‑20, we estimate that costs are down a net of $270 million compared with the June estimates. The drop in 2019‑20 mainly reflects our estimate that student attendance is likely to decline by 0.5 percent rather than 0.2 percent as assumed in June. This drop, in turn, reduces LCFF costs. These savings are partially offset by costs for community college apportionments being slightly above previous estimates.

Figure 3

Additional Spending Required to Meet Guarantee in Prior and Current Year

(In Millions)

|

2018‑19 |

2019‑20 |

||||||

|

June Budget Plan |

November LAO Estimates |

Change |

June Budget Plan |

November LAO Estimates |

Change |

||

|

Minimum Guarantee |

$78,146 |

$78,340 |

$194 |

$81,056 |

$80,871 |

‑$185 |

|

|

Costs |

|||||||

|

Local Control Funding Formula |

$61,150 |

$61,152 |

$1 |

$62,989 |

$62,685 |

‑$304 |

|

|

Community college apportionmentsa |

6,709 |

6,694 |

‑15 |

6,973 |

7,016 |

43 |

|

|

Special education |

3,969 |

3,960 |

‑9 |

4,698 |

4,695 |

‑3 |

|

|

Other programs |

6,318 |

6,308 |

‑10 |

6,020 |

6,014 |

‑7 |

|

|

Total Costs |

$78,146 |

$78,114 |

‑$32 |

$80,680 |

$80,409 |

‑$270 |

|

|

Proposition 98 Reserve Deposit |

— |

— |

— |

$377 |

$177 |

‑$200 |

|

|

Settle‑Up Payment |

— |

$226 |

$226 |

— |

285 |

285 |

|

|

aReflects community college apportionment costs after accounting for student fee revenue. |

|||||||

Deposit Into Proposition 98 Reserve Also Revised Down in 2019‑20. Under our outlook, the required deposit into the Proposition 98 reserve in 2019‑20 drops from $377 million to $177 million. This $200 million decrease occurs primarily because of slower year‑to‑year growth in the minimum guarantee. Whereas the enacted budget assumed the 2019‑20 guarantee would grow 0.5 percent faster than attendance and inflation, our outlook has a difference of only 0.2 percent.

State Required to “Settle Up” to Meet Guarantee in 2018‑19 and 2019‑20. Our revised estimates of the minimum guarantee and program costs, coupled with the change in the size of the required reserve deposit, result in a spending level that is $226 million below the 2018‑19 guarantee and $285 million below the 2019‑20 guarantee. When spending drops below the guarantee, the state must make a one‑time payment to settle up for the difference. The state could allocate the $511 million in total settle‑up payments for any one‑time Proposition 98 purposes.

2020‑21 Estimates

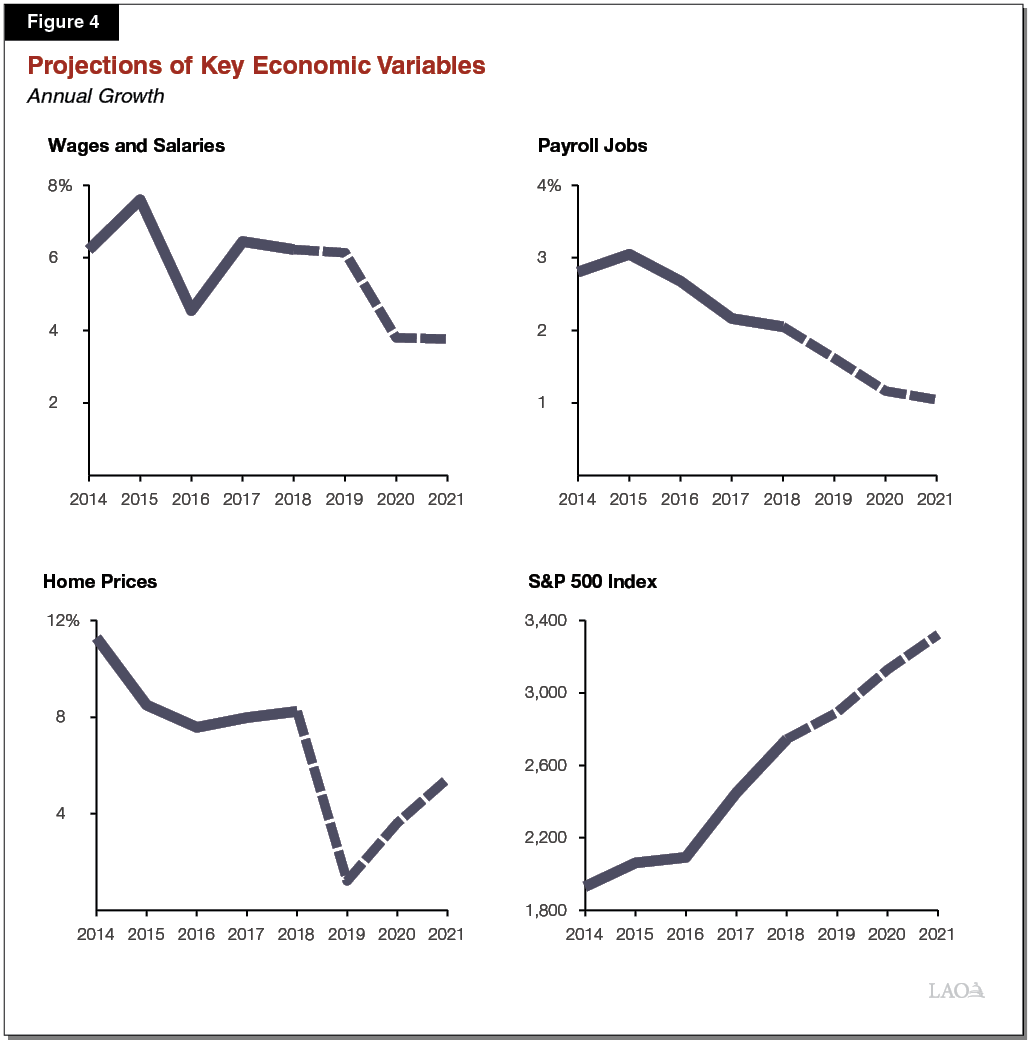

2020‑21 Outlook Assumes Continued Growth of the California Economy. The consensus among professional economists (according to a collection of forecasts compiled by Moody’s Analytics) is that the national economy will continue to grow in the coming years, although at a somewhat slower pace than in recent years. Based on these expectations, we project a similar growth trend in the California economy. California, for example, is expected to continue adding jobs but more slowly than in recent years. Figure 4 displays some of the key assumptions underlying our economic outlook. Although we assume continued economic growth, recent weakening of some economic indicators suggests the outlook in 2020‑21 is somewhat more susceptible to downside risk compared to recent budgets. (The 2020‑21 Budget: California’s Fiscal Outlook, covers economic and revenue trends in more detail.)

Near‑Term Outlook Assumes Continued—Though Somewhat Slower—Growth in State Revenue. Consistent with our economic assumptions, we estimate that state General Fund revenue will continue to grow. For 2020‑21, our outlook assumes revenue from the state’s three largest taxes increases $5 billion (3.5 percent). This is slightly higher growth than estimated for 2019‑20 (2.8 percent), but notably lower growth than in 2018‑19 (6 percent) and 2017‑18 (10 percent).

2020‑21 Guarantee Estimated to Grow $3.4 Billion. Under our outlook, the minimum guarantee grows to $84.3 billion in 2020‑21, an increase of $3.4 billion (4.2 percent) compared with our revised estimate of the 2019‑20 guarantee (Figure 5 ). Test 1 is operative, with the majority of the increase attributable to growth in General Fund revenue. The rest of the increase is attributable to growth in local property tax revenue. Our local property tax projections reflect an estimated 5.7 percent increase in assessed property values, which is somewhat slower than growth the past several years but close to the average over the past two decades (5.8 percent).

Figure 5

Proposition 98 Near‑Term Outlook

LAO Estimates (Dollars in Millions)

|

2018‑19 |

2019‑20 |

2020‑21 |

|

|

Minimum Guarantee |

|||

|

General Fund |

$54,617 |

$55,985 |

$57,963 |

|

Local property tax |

23,723 |

24,886 |

26,306 |

|

Totals |

$78,340 |

$80,871 |

$84,269 |

|

Year‑to‑Year Change in Funding |

|||

|

General Fund |

$1,665 |

$1,369 |

$1,978 |

|

Percent change |

3.1% |

2.5% |

3.5% |

|

Local property tax |

$1,098 |

$1,163 |

$1,420 |

|

Percent change |

4.9% |

4.9% |

5.7% |

|

Total guarantee |

$2,764 |

$2,531 |

$3,398 |

|

Percent change |

3.7% |

3.2% |

4.2% |

|

General Fund Tax Revenuea |

$143,182 |

$147,249 |

$152,535 |

|

Growth Rates |

|||

|

K‑12 average daily attendance |

‑0.8% |

‑0.4% |

‑0.5% |

|

CCC full‑time‑equivalent students |

0.1 |

0.3 |

0.5 |

|

Per capita personal income (Test 2) |

3.7 |

3.9 |

4.3 |

|

Per capita General Fund (Test 3)b |

6.2 |

2.8 |

3.6 |

|

Operative Test |

1 |

1 |

1 |

|

Proposition 98 Reserve |

|||

|

Deposit (+) or withdrawal (‑) |

— |

$177 |

$350 |

|

Cumulative balance |

— |

177 |

527 |

|

aExcludes nontax revenues and transfers, which do not affect the calculation of the minimum guarantee. bAs set forth in the State Constitution, reflects change in per capita General Fund plus 0.5 percent. Note: No maintenance factor obligation is created, paid, or owed over the period. |

|||

Deposit Into Proposition 98 Reserve Estimated at $350 Million. Under our outlook assumptions, the state would be required to deposit $350 million into the Proposition 98 Reserve in 2020‑21. This deposit would bring the total balance of the reserve to $527 million. This balance equates to 0.6 percent of the 2020‑21 minimum guarantee under our outlook.

Guarantee Is Moderately Sensitive to Changes in Revenue Estimates Over the Period. We examined how the minimum guarantee would change if state revenue comes in higher or lower than our outlook assumptions. In general, the sensitivity of the guarantee depends on which Proposition 98 test is operative and whether another test could become operative with higher or lower revenue. Under our outlook, Test 1 is the operative test over the entire period. Moreover, we found that the operative test is unlikely to change in 2020‑21 (or 2019‑20). Holding other factors constant, Test 1 would be operative given any level of General Fund revenue. This unusual situation is due primarily to declining student attendance and steady growth in local property tax revenue—two trends that tend to contribute to Test 1 being the operative test. In Test 1 years, the guarantee increases or decreases about 40 cents for each dollar of higher or lower General Fund revenue.

Changes in Revenue Affect Guarantee and Size of Reserve Deposits. Although the minimum guarantee would change in response to higher or lower revenue estimates in 2020‑21, the size of the Proposition 98 Reserve deposit also will be affected, which in turn will affect the amount available for additional Proposition 98 spending. In a scenario where revenue increases a couple billion dollars in 2020‑21 (with no change in 2019‑20), the corresponding increase in the required reserve deposit likely would equal the increase in the guarantee, leaving nothing available for additional Proposition 98 spending. The required deposit also would tend to grow in scenarios where revenue increases in both the current and budget years, though the deposit likely would not grow on a dollar‑for‑dollar basis. On the downside, a drop in revenues and the minimum guarantee would tend to reduce the size of the required reserve deposits. Given the relatively small amount in the Proposition 98 Reserve, however, this buffer would disappear quickly. (Our analysis holds all Proposition 98 inputs besides revenue constant, though changes in these inputs also could affect the guarantee and the size of the deposit.)

Outlook Through 2023‑24

Many Economic Scenarios Are Possible Over the Period. Over the next four years, state General Fund revenue will change due to various economic developments, such as changes in employment and fluctuations in the stock market. Changes in General Fund revenue, in turn, can have significant effects on the minimum guarantee. In this section, we describe how the guarantee would change through 2023‑24 under two economic scenarios: (1) a growth scenario and (2) a recession scenario.

Certain Assumptions Underlie the Two Economic Scenarios. The growth scenario assumes California continues to add jobs through 2023‑24, but at about half the pace as recent years. It also assumes wage growth continues. In this scenario, stock market growth remains strong through 2021 and then tapers off toward the end of the forecast period. The recession scenario assumes a typical post‑World War II recession begins early in 2021. Job losses likewise begin in 2021, resulting in a doubling of the unemployment rate. We also assume the stock market loses 30 percent of its value. We intend these two scenarios to be illustrative rather than predictive about the direction of the economy in the coming years.

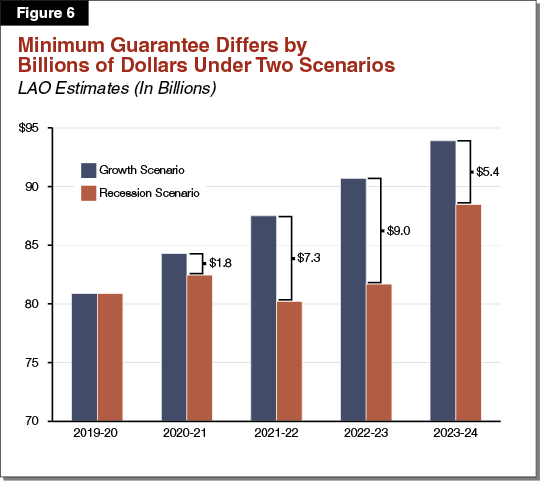

Under Growth Scenario, Minimum Guarantee Rises Steadily. The minimum guarantee increases steadily under the growth scenario from $80.9 billion in 2019‑20 to $93.9 billion in 2023‑24 (see Figure 6 and the “Appendix”). The average annual increase over this period is $3.3 billion (3.8 percent). Of this increase, just over half is attributable to growth in General Fund revenue and the remainder is attributable to growth in local property tax revenue. Regarding our property tax estimates, we assume growth in assessed property values ranges from 5.4 percent to 6 percent per year. Underlying this steady growth is an assumption that falling mortgage interest rates will lead to a modest rebound in housing markets following a slowdown over the past year.

Growth Scenario Includes Modest Deposits Into Proposition 98 Reserve. Assuming the economy continues to grow, the state is likely to continue making deposits into the Proposition 98 Reserve over the coming years. Under our growth scenario, the deposits range from $1 billion in 2021‑22 to $117 million in 2023‑24. By 2023‑24, the balance in the reserve reaches $2.2 billion. Reserve deposits, however, are highly sensitive to small changes in several inputs. For example, if per capita personal income (one of the inflation factors) were to grow 0.5 percent faster than our scenario assumes for each of the next four years, the balance would grow to only about $1.1 billion. On the other hand, if per capita personal income were to grow 0.5 percent slower for the next four years, the balance would reach $2.6 billion. A balance of this size would trigger statutory caps on local school district reserves for the following year. (The caps become operative the year after the balance reaches 3 percent of the Proposition 98 funding allocated to schools.)

State Could Likely Cover Statutory COLA Under Growth Scenario. In May, the administration’s projections had the statutory COLA hovering around 3 percent annually for the next few years. These COLA rates are in line with the historical average over the past 20 years (2.7 percent). The consensus forecast prepared by Moody’s Analytics, by contrast, has the COLA rate hovering around 1.2 percent after 2020‑21. These rates are in line with the average COLA rate since the end of the Great Recession (1.6 percent). Using either COLA assumption, the state could cover the full statutory rate under our growth scenario. This is because the guarantee grows at around 3.8 percent per year. Although some of the increase in the guarantee would be deposited into the Proposition 98 Reserve and unavailable for spending, our outlook also has attendance declining by at least 0.5 percent per year. These attendance declines free up several hundred million dollars inside the guarantee each year of the period.

Under Recession Scenario, Minimum Guarantee Drops in 2021‑22. Under the recession scenario, the minimum guarantee begins to slow down in 2020‑21 and drops $2.2 billion (2.7 percent) in 2021‑22. By 2022‑23, the guarantee is $9 billion (9.9 percent) below the level in our growth scenario (see Figure 6 and the “Appendix”). This drop mirrors the trajectory of General Fund revenue. Growth in local property tax revenue also slows to about 3.5 percent per year. Under this scenario, the state not only would be unable to provide the COLA in 2021‑22 and 2022‑23, it would need to reduce spending, assuming it funds at the lower minimum guarantee. The Legislature could do this by making reductions to ongoing programs, deferring school and college payments, or exploring possible fund swaps. The Proposition 98 Reserve would provide little relief in this scenario, as the state would enter the recession with a balance of only $177 million (about 0.2 percent of all funding currently allocated to schools and community colleges).

Key Issues for Consideration

Legislature Faces Several Important Planning Issues in the Year Ahead. In this part of the report, we highlight a few issues for the Legislature to consider as it begins planning for the upcoming budget cycle. Specifically, we (1) highlight key cost pressures that school and community college districts face, (2) analyze the amount of new funding available for school and community college programs in 2020‑21, and (3) describe the trade‑offs involved in key spending decisions.

District Cost Pressures

School and Community College Pension Costs Set to Increase. Over the past several years, district officials and Legislators have focused on rising pension costs. Required district contributions to the California State Teachers’ Retirement System (CalSTRS) and the California Public Employees’ Retirement System (CalPERS) have grown from $3.5 billion in 2013‑14 to $8.7 billion in 2019‑20. (CalSTRS administers pension benefits for teachers, administrators, and other certificated employees, whereas CalPERS administers pension benefits for classified employees, such as cafeteria workers.) The rise in costs primarily reflects efforts to address the large unfunded liabilities the two pension systems accrued over the past few decades. For 2020‑21, districts’ total contributions to CalSTRS and CalPERS are estimated to increase by roughly $1 billion. After 2020‑21, pension cost increases are likely to continue, though at a slower pace than the past several years.

Districts Face Various Other Cost Pressures. In addition to pension costs, districts face cost pressure to raise employee salaries, cover rising health benefit costs, hire more staff, and expand services. Among school districts, spending on special education also has increased notably over the past decade (in part due to more students qualifying for services, and requiring more intensive services, than in the past). Districts respond to cost pressures in different ways, with decisions about salary, benefits, and staffing often varying notably even among neighboring districts with similar student demographics and overall funding levels. Some district decisions (such as salary and staffing decisions) have important interactive effects. Most notably, districts that agree to above‑average salary and staffing increases also face above‑average increases in pension contributions (as contributions are partially determined by payroll).

Districts With Declining Enrollment Have Extra Challenge in Addressing Cost Pressures. About 70 percent of school districts and 60 percent of community colleges have been experiencing drops in their enrollment. Some of this trend is due to drops in the number of births in California and families moving away from urban areas. In some cases, the associated declines in student enrollment have been occurring for many years. Los Angeles Unified School District, for example, has experienced enrollment declines since the early 2000s. Whether a trend that began many years ago or more recently, declining enrollment districts face an added budget challenge, as most state funding (including LCFF and apportionment funding) is allocated on a per‑student basis.

Funding Available for New Commitments

Notable Funding Available for New Commitments. Figure 7 displays our estimate of additional Proposition 98 funding available for new commitments in 2020‑21. We estimate the minimum guarantee in 2020‑21 will increase $3.4 billion and another $206 million will be freed up from the expiration of certain one‑time activities funded in 2019‑20.

Figure 7

Funding Available for New Commitments

LAO Estimates (In Millions)

|

Available Funding |

|

|

Growth in 2020‑21 minimum guarantee |

$3,398 |

|

Funding freed‑up inside guarantee |

206 |

|

Total Available |

$3,604 |

|

Cost Estimatesa |

|

|

Local Control Funding Formula |

‑$826 |

|

Community college apportionments |

‑177 |

|

Special education |

‑57 |

|

Other programs |

‑45 |

|

Total Costs |

‑$1,105 |

|

Proposition 98 Reserve Deposit |

‑$350 |

|

Remaining Funds Available |

$2,148 |

|

aReflects cost of covering statutory cost‑of‑living adjustments and changes in student attendance. |

|

After Covering COLA and Enrollment Changes, Estimated $2.1 Billion Remains. Under state law, several K‑14 programs are to receive a COLA each year. For 2020‑21, we estimate the statutory K‑14 COLA rate is 1.79 percent. Our estimate incorporates the latest federal data as of October 30 and projections from Moody’s Analytics for the two quarters of data that are not yet available. Regarding K‑12 attendance, we assume a decline of 0.5 percent, consistent with our projections that births and net migration into the state will remain at relatively low levels. For community colleges, we assume full‑time equivalent enrollment increases by 0.5 percent. This increase mainly reflects our estimate that the share of the population ages 18 to 24 attending community colleges will continue to rise, consistent with recent trends. We estimate that the total net cost of covering the statutory COLA and enrollment changes is $1.1 billion. After covering these costs and making the Proposition 98 Reserve deposit, $2.1 billion would remain available for new commitments. The Legislature could allocate this amount for any of its school and community college priorities.

Spending Trade‑Offs

Various Trade‑Offs to Consider When Making Ongoing Spending Decisions. The 1.79 percent statutory COLA rate is relatively low compared to the cost pressures most districts are facing. If the Legislature were to provide no other ongoing increase in general purpose funding, most districts likely would need to dedicate nearly all of the increase to covering their higher pension costs. Assuming the Legislature wants to provide additional ongoing funding to help districts address other cost pressures, the most straightforward approach is to fund a higher COLA rate. A 0.5 percentage point increase in the COLA rate would cost about $300 million for LCFF and $38 million for community college apportionments. Instead of providing more general purpose funding, the Legislature could prioritize targeted increases. For example, the 2019‑20 budget provided $153 million to increase special education funding in regions with historically low per‑pupil funding rates. This augmentation helped address cost pressure for school districts in these regions while making special education funding more equitable on an ongoing basis.

Risks of Economic Downturn—and Drop in Guarantee—Are Higher Than Normal. Each year, our outlook identifies various risks and uncertainties that could cause the state economy to perform worse than expected. This year, we think the downside risks are higher than normal. Several economic indicators that previously had been strong—such as trade activity, consumer spending, and business startups—have been weaker in 2019. Though such trends do not automatically imply a broader economic slowdown is imminent, they do suggest that the risks in 2020‑21 are higher compared to previous budget cycles. To the extent the economy performs worse than we expect, state revenues and the minimum guarantee also would be lower.

Dedicating Some Funding to One‑Time Activities Would Build a Budget Cushion. To address potential drops in the minimum guarantee, the state typically sets aside some portion of available Proposition 98 funding for one‑time activities. The advantage of this budgeting approach is that if the guarantee falls below projections, the expiration of these one‑time activities provides a cushion that reduces the likelihood of cuts to ongoing K‑14 programs. Over the six‑year period spanning from 2013‑14 through 2018‑19, the state set aside an average of about $700 million per year for one‑time activities. (This amount excludes one‑time funds associated with prior‑year true‑ups and settle‑up payments.) The 2019‑20 budget plan, by contrast, had a one‑time cushion of only $121 million.

Suggest Setting Aside at Least Half of the Available Funding for One‑Time Activities. In sizing its budget cushion, the Legislature faces some tension between providing ongoing increases (which helps districts deal with ongoing cost pressures now) and using funding for one‑time activities (which helps districts deal with future drops in the guarantee). At a minimum, we think the Legislature should consider reserving about half the available funds above the COLA for one‑time activities. Under this approach, the total cushion would be $1.4 billion ($1.1 billion from one‑time activities and $350 million from the required Proposition 98 Reserve deposit). Although the guarantee likely would drop by more than this amount over the course of a typical recession, having such a cushion would make the drop less disruptive for schools, community colleges, and the state.

Paying Down Pension Liabilities More Quickly Would Have High Long‑Term Payoff. Despite the increases in district pension contributions over the past several years, CalSTRS and CalPERS continue to have large unfunded liabilities. Assuming the Legislature allocates some Proposition 98 funding for one‑time activities, we encourage it to use this funding for paying down districts’ pension liabilities more quickly. To accomplish such acceleration, the payments would need to supplement the previously scheduled increases in district and state contributions for 2020‑21. (We discourage the Legislature from making payments that supplant what districts already plan to contribute in 2020‑21). Supplemental payments would both improve the funding status of the pension systems and tend to lower district pension contributions over the next several decades—making district budgets easier to balance on a sustained basis. (In The 2020‑21 Budget: California’s Fiscal Outlook, we also encourage the Legislature to address the state’s share of pension liabilities using non‑Proposition 98 funds.)

Appendix

Proposition 98 Outlook Under Two Economic Scenarios

LAO Estimates (Dollars in Billions)

|

2019‑20 |

2020‑21 |

2021‑22 |

2022‑23 |

2023‑24 |

|

|

Growth Scenario |

|||||

|

Minimum Guarantee |

|||||

|

General Fund |

$56.0 |

$58.0 |

$59.9 |

$61.5 |

$63.1 |

|

Local property tax |

24.9 |

26.3 |

27.6 |

29.2 |

30.8 |

|

Totals |

$80.9 |

$84.3 |

$87.5 |

$90.7 |

$93.9 |

|

Annual Change in Guarantee |

$2.5 |

$3.4 |

$3.2 |

$3.2 |

$3.2 |

|

Percent change |

3.2% |

4.2% |

3.8% |

3.7% |

3.5% |

|

General Fund Tax Revenuea |

$147.2 |

$152.5 |

$157.6 |

$161.9 |

$165.8 |

|

Growth Rates |

|||||

|

K‑12 average daily attendance |

‑0.4% |

‑0.5% |

‑0.6% |

‑0.8% |

‑1.2% |

|

Per capita personal income (Test 2) |

3.9 |

4.3 |

3.2 |

3.8 |

3.7 |

|

Per capita General Fund (Test 3)b |

2.8 |

3.6 |

3.3 |

2.7 |

2.4 |

|

Operative Test |

1 |

1 |

1 |

1 |

1 |

|

Proposition 98 Reserve |

|||||

|

Deposit (+) or withdrawal (‑) |

$0.2 |

$0.4 |

$1.0 |

$0.5 |

$0.1 |

|

Cumulative balance |

0.2 |

0.5 |

1.5 |

2.1 |

2.2 |

|

Recession Scenario |

|||||

|

Minimum Guarantee |

|||||

|

General Fund |

$56.0 |

$56.3 |

$53.1 |

$53.6 |

$59.3 |

|

Local property tax |

24.9 |

26.2 |

27.1 |

28.1 |

29.1 |

|

Totals |

$80.9 |

$82.5 |

$80.2 |

$81.7 |

$88.4 |

|

Annual Change in Guarantee |

$2.5 |

$1.6 |

‑$2.2 |

$1.5 |

$6.8 |

|

Percent change |

3.2% |

2.0% |

‑2.7% |

1.8% |

8.3% |

|

General Fund Tax Revenuea |

$147.2 |

$148.1 |

$139.8 |

$141.1 |

$156.0 |

|

Growth Rates |

|||||

|

K‑12 average daily attendance |

‑0.4% |

‑0.5% |

‑0.6% |

‑0.8% |

‑1.2% |

|

Per capita personal income (Test 2) |

3.9 |

4.3 |

3.2 |

2.2 |

1.8 |

|

Per capita General Fund (Test 3)b |

2.8 |

0.6 |

‑5.6 |

0.8 |

10.5 |

|

Operative Test |

1 |

1 |

1 |

1 |

1 |

|

Proposition 98 Reserve |

|||||

|

Deposit (+) or withdrawal (‑) |

$0.2 |

‑$0.2 |

— |

— |

— |

|

Cumulative balance |

0.2 |

— |

— |

— |

— |

|

Comparison of Scenarios |

|||||

|

Minimum Guarantee |

|||||

|

Growth scenario |

$80.9 |

$84.3 |

$87.5 |

$90.7 |

$93.9 |

|

Recession scenario |

80.9 |

82.5 |

80.2 |

81.7 |

88.4 |

|

Difference |

— |

$1.8 |

$7.3 |

$9.0 |

$5.4 |

|

aExcludes nontax revenue and transfers, which do not affect the calculation of the minimum guarantee. bAs set forth in the State Constitution, reflects change in per capita General Fund plus 0.5 percent. Note: No maintenance factor obligation is created, paid, or owed under either scenario. |

|||||