Heather Gonzalez

April 3, 2025

The 2025-26 Budget

Department of Financial Protection and Innovation

Background

The Department of Financial Protection and Innovation (DFPI) Regulates Financial Service Providers in California. DFPI licenses financial services, products, and professionals, and regulates franchises and securities offerings in California. The department also educates consumers on how to avoid scams, investigates suspected fraud, and (in certain instances) takes legal action to collect restitution for lost money. The revised 2024-25 budget provides DFPI with $177 million—almost exclusively from four special funds, which themselves are largely funded by revenue from regulatory fees, licenses, and permits—and 878.3 positions.

DFPI Oversees a Mix of Established and New Programs. DFPI operations can be divided into various established programs dedicated to regulating specific professions and entities as well as other activities. These include the following:

Investment Program. Regulates the offer and sale of certain financial securities and franchises, and licenses and examines broker-dealers and investment advisors. (Financial securities are tradable financial assets, such as stocks and bonds.)

Lender-Fiduciary Program. Licenses and regulates businesses engaged in financial transactions, such as mortgage loan originators, finance lenders, and escrow agents, as well as residential mortgage lenders and servicers.

Licensing and Supervision of Banks and Trust Companies Program. Also known as the Banking program, this program regulates, supervises, and examines various entities, including state-licensed banks and trust companies, business and industrial development corporations, public banks, industrial banks, and premium finance companies.

Money Transmitters Program. Regulates, supervises, and examines businesses that receive money for transmission and sell or issue payment instruments and stored value. (These can include businesses that issue money orders and traveler’s checks, as well as those that offer digital payments, such as PayPal and Stripe.)

Credit Unions Program. Regulates, supervises, and examines credit unions.

Between 2021 and 2023, the Legislature also added the following three new programs to DFPI’s suite of responsibilities:

California Consumer Financial Protection Program. Chapter 157 of 2020 (AB 1864, Limón)—known as the California Consumer Financial Protection Law—broadened DFPI’s authority in various ways beginning January 1, 2021. For example, previously, the department was authorized to oversee only those companies that fell under a limited list of entities, such as banks, escrow agents, and brokers. Under AB 1864, the department has broad authority to oversee those same entities as well as any firm or person providing consumer financial products or services. New industries now under department oversight include those providing private postsecondary education financing and debt relief.

Debt Collector Program. Chapter 163 of 2020 (SB 908, Wieckowski) requires DFPI to establish a regulatory and licensing system to oversee debt collectors. DFPI began implementing SB 908 on January 1, 2021 and started accepting applications for licensure on September 1, 2021.

Digital Financial Assets Program. Chapter 792 of 2023 (AB 39, Grayson) requires DFPI to regulate crypto assets (which are sometimes referred to as cryptocurrencies, virtual currencies, or digital financial assets). Chapter 781 of 2023 (SB 401, Limón) requires DFPI to regulate digital financial asset transaction kiosks. DFPI is expected to begin licensing under this program on July 1, 2026.

Majority of Funding for DFPI Comes from Financial Protection Fund. Although DFPI receives funding from four special funds, in a typical year the overwhelming majority of the department’s funding (85 to 90 percent) comes from one special fund, the Financial Protection Fund. Most of the Financial Protection Fund’s revenues are generated by licensing and registration fees, program assessments (charges levied on regulated entities to cover oversight costs), and examination fees (to cover costs associated with specific audits or inspections).

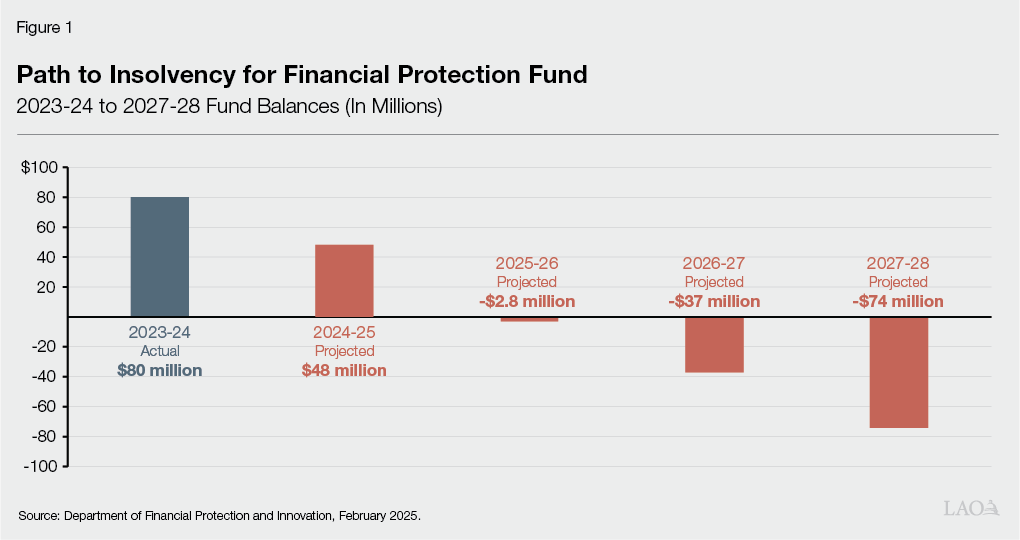

Financial Protection Fund on Track to Insolvency. A DFPI fund condition report provided to the Legislature on February 25, 2025 indicates that the Financial Protection Fund will become insolvent toward the end of 2025-26 and face growing deficits in future years as shown in Figure 1.

Independent Study Found Expenditures Outpacing Revenues for Both Established and New Programs. In 2024, DFPI asked an independent accounting firm to conduct a fiscal and cost study of its programs. The resulting report identified a structural deficit dating to 2020-21 caused by both cost and revenue factors. Cost factors included annual salary adjustments and startup costs for the three new programs. On the revenue side, the report identified static fee levels and a decrease in Banking program revenue from recent large bank closures (including the collapse of Silicon Valley Bank). Several DFPI fees that have not been adjusted were established in the late 1980s through early 2000s, with one not being changed since 1959.

Independent Study Found Expenditures Outpacing Revenues for Both Established and New Programs. In 2024, DFPI asked an independent accounting firm to conduct a fiscal and cost study of its programs. The resulting report identified a structural deficit dating to 2020-21 caused by both cost and revenue factors. Cost factors included annual salary adjustments and startup costs for the three new programs. On the revenue side, the report identified static fee levels and a decrease in Banking program revenue from recent large bank closures (including the collapse of Silicon Valley Bank). Several DFPI fees that have not been adjusted were established in the late 1980s through early 2000s, with one not being changed since 1959.

Study Concluded That DFPI Needs $193.2 Million in Additional Funding for Certain Established and New Programs Through 2027-28. The independent accounting firm’s report estimated that the department requires an additional $80.4 million through 2027-28 to support 8 of 13 established programs and subprograms, as well as an estimated $112.8 million through 2027-28 for its three new programs, for a total of $193.2 million. (Five of the 13 established programs and subprograms were not found to be facing structural deficits.) Figure 2 summarizes projected revenues and costs for the eight established DFPI programs and subprograms that the report identified as facing cumulative structural deficits from 2023-24 through 2027-28.

Figure 2

Structural Deficits in Selected DFPI Programs

Cumulative 2023‑24 Through 2027‑28

|

Program/Subprogram |

Projected |

Projected |

Difference |

|

Investment Program |

|||

|

Broker‑Dealers Investment Adviser |

$91.7 |

$110.3 |

‑$18.6 |

|

Franchise Investment |

7.0 |

13.5 |

‑6.4 |

|

Lender‑Fiduciary Program |

|||

|

Mortgage Bankers |

$17.7 |

$30.4 |

‑$12.7 |

|

California Finance Lenders |

39.7 |

46.0 |

‑6.3 |

|

Escrow |

23.9 |

35.2 |

‑11.2 |

|

Deferred Deposit Transaction |

8.2 |

11.3 |

‑3.1 |

|

Banking Program |

|||

|

Banks |

$151.6 |

$173.1 |

‑$21.5 |

|

Money Transmitters Program |

|||

|

Money Transmitters Program |

$36.0 |

$36.5 |

‑$0.5 |

|

Totals |

$375.8 |

$456.2 |

‑$80.4 |

|

Notes: Numbers rounded. In millions. |

|||

|

DFPI = California Department of Financial Protection and Innovation. |

|||

Governor’s Proposal

Governor Requests Authority to Raise Certain DFPI Fees. The Governor proposes trailer bill language that would increase fees for some established DFPI subprograms that are facing deficits, as shown in Figure 3. The Governor also proposes language that would allow the department to set hourly examination rates based on its estimated average cost, including overhead, for the Money Transmitters, Banking, and Credit Union programs. (Currently, the department receives a flat rate of $75 an hour.)

Figure 3

Proposed Fee Changes, by DFPI Subprogram

2025‑26 Governor’s Proposed Budget: Proposed Trailer Bill

|

Program/Subprogram |

Purpose of Fee |

Year Fee Established |

Current Fee |

Proposed Fee |

|

Investment Program |

||||

|

Broker‑Dealer Agent/Investment Advisor Representative |

Application (Individual) |

1959 |

$25 |

$50 |

|

Broker‑Dealer Agent/Investment Advisor Representative |

Renewal (Individual) |

2013 |

Up to 35 |

50 |

|

Franchise Investment |

Registration of Offer of Franchises |

1989 |

675 |

1,865 |

|

Franchise Investment |

Renewal of Registration of Offer of Franchises |

1989 |

450 |

1,245 |

|

Franchise Investment |

Initial Notice of Exemption |

1989 |

450 |

1,245 |

|

Franchise Investment |

Consecutive Subsequent Notice of Exemption |

1989 |

150 |

415 |

|

Franchise Investment |

Notice of Violation |

— |

675 |

1,865 |

|

Lender‑Fiduciary Program |

||||

|

California Residential Mortgage Lending Act (Mortgage Bankers) |

Assessment |

2000 |

Prorated $1,000 min $5,000 max |

Prorated $3,000 min $15,000 max |

|

Escrow |

Assessment |

2001 |

Not to exceed $2,800 per office location |

Not to exceed $7,215 per office location |

|

Examination Rates |

||||

|

Money Transmitters |

Exam Hourly Fee |

1997 |

$75 |

Determined by DFPI |

|

Banking |

Exam Hourly Fee |

1997 |

75 |

Determined by DFPI |

|

Credit Union |

Exam Hourly Fee |

1998 |

75 |

Determined by DFPI |

|

DFPI = California Department of Financial Protection and Innovation. |

||||

Governor Not Requesting Increased Fees for Certain Programs and Subprograms. DFPI indicates that it can increase program assessment fees for three of the established programs facing structural deficits—the California Finance Lenders, Deferred Deposit Transaction, and Banks subprograms—without the need for additional legislative action. Accordingly, this proposal does not request fee increases for these subprograms. DFPI also expects that revenue generated from the new programs, once they are fully operational, will cover their costs. As a result, no fee increases are proposed for these programs either.

Assessment

DFPI Does Not Have the Funds Necessary to Achieve Its Mission. The Financial Protection Fund is facing insolvency in 2025-26. This is largely driven by a structural deficit dating to 2020-21. This deficit was caused by a combination of increasing costs and insufficient revenue. To address this, DFPI must reduce costs, raise fees, or seek alternative sources of funding, such as the General Fund.

Reducing Costs Without Impacting Regulatory Activities May Be Challenging. The independent assessment of DFPI’s financial condition identified annual salary adjustments (agency-wide) and start-up costs for new programs as the main sources of increased expenditures at DFPI. One option for policy makers would be to reduce these costs, chiefly by reducing staffing or by delaying the implementation of (or eliminating) costly new programs that are not yet collecting sufficient revenue. However, reducing staff could impact service levels and is likely to limit the department’s capacity to meet its current oversight and regulatory mission. There are drawbacks to delaying the implementation of new programs as well. Failing to complete implementation means foregoing the revenue these programs expect to collect when fully operational. It could also result in the loss of some of the money already spent in their development, such as funds spent on training staff who might need to be rehired and retrained if the programs were delayed.

Increasing Regulatory Fees Is A Reasonable Approach to Addressing Regulatory Funding Shortfalls. Typically, the state uses regulatory fees to fund regulatory agencies like DFPI. This method of financing puts the cost of regulation on those who receive regulatory services (such as the issuance of a license, the review of an application, or enforcement against fraudulent actors). Consistent with this principle, it is reasonable for the department to meet its revenue challenge by increasing fees on the regulated community rather than requesting support from an alternative source such as the General Fund.

Some of the Proposed Fees Appear Reasonable… As noted in the independent study, many of the DFPI fees that the administration seeks to increase have not changed in decades. For example, the current $25 broker-dealer agent/investment advisor representative application fee was set in 1959. This fee has not kept up with department costs, and even at the proposed level ($50—a 100 percent increase), is well below inflation. (Depending on how inflation is adjusted for, the inflation-adjusted level for this fee would be between $246 to $380.) Similarly, authorizing the department to set hourly examination fees at a price that includes overhead would allow it to more fully recoup costs for a comparatively complex set of auditing and assessment tasks and services.

…While Others Are Relatively High. For example, the proposed increase in new franchise registration fees—from $675 to $1,865—would set California fees at much higher levels than other states. In other states with franchise registration fees, new franchise registration fees range from $250 to about $750. (Some states do not charge these specific fees, but may charge others.) Additionally, some of the proposed fee increases—such as the $15,000 maximum in the prorated Mortgage Bankers assessment and the $7,215 per office location Escrow assessment—outpace inflation by some measures. Given the magnitude of these fees, they may not have significant effects on decisions (such as whether to start a franchise in the state) by some of the more well-established and well-financed firms, but could have a more substantial impact on smaller firms.

Administration Has Not Presented an Adequate Plan for All Programs With Identified Insolvencies. The department indicates that the fee increases authorized by the proposed trailer bill would provide approximately $50 million in support for the underfunded established programs through 2027-28. However, the accounting firm’s evaluation of DFPI’s established programs found an additional $30 million in unfunded balances across established subprograms that are not in the administration’s proposed bill. The administration indicates that it has the authority to increase fees to address these costs based on existing law, but it has not provided a specific plan or revenue projections to that end. Similarly, the administration has not provided detailed revenue projections for the department’s new programs.

Recommendation

Approve Proposed Fee Increases on a Limited-Term Basis and Require Reporting. We recommend that the Legislature approve the proposed fee increases on a limited-term, three-year basis. We also recommend directing DFPI to report annually for three years beginning on January 10, 2026, on the amount of revenue received from each increased fee and how this compares to what the department projected would be received. This will allow the Legislature to more closely monitor the health of the Financial Protection Fund. Additionally, in order to assess the impact of the fee increases on the regulated community, we recommend directing DFPI to report to the Legislature by January 1, 2028, on the condition, health, and major challenges for the franchise, mortgage lending, and escrow industries in California, given the size of the fee increases proposed for these industries. These reports could inform the Legislature’s deliberations on the 2028-29 budget, when it would be determining whether to maintain the elevated fee levels set to expire under our recommendation.

Direct Department to Provide Key Information on Plans to Address Solvency of the Programs Not Included in the Fee Proposal. We recommend that the Legislature direct DFPI to report in spring budget hearings key information on its plans to fully fund the programs and subprograms that are not included in the Governor’s proposal. Specifically, we recommend DFPI report on the following:

The level of revenue it has collected to date and expected future revenues associated with the new programs it is implementing: the California Consumer Financial Protection Program, the Debt Collector Program, and the Digital Financial Assets Program.

Planned fee increases it intends to implement through regulations for the California Finance Lenders, Deferred Deposit Transaction, and Banks subprograms, including the size of the increases and the amount of revenue expected from these increases

What steps it would take if the fee increases alone prove insufficient to prevent the insolvency of the fund.

This will give the Legislature insight into whether the department’s plans are likely to address the insolvency of the fund in 2025-26 and whether those plans are consistent with the Legislature’s priorities.