Ann Hollingshead

Table of Contents

Appendix 1: General Fund Discretionary Spending Proposals

Appendix 2: General Fund Spending Solutions

Appendix 3: May Multiyear Revenue Outlook

Update (5/21/26): Upon further review and receipt of additional information from the administration, we estimate the amount of discretionary spending in the May Revision is $1.1 billion, rather than $1.3 billion.

May 18, 2026

The 2026-27 Budget

Initial Comments on the Governor's May Revision

- Introduction

- May Revision Balanced on Higher Revenues and Reserves

- Solutions and Discretionary Choices in May Revision

- Budget Condition

- Comments

- Recommendations

- Conclusion

Executive Summary

Despite Revenue Boom, Budget Architecture Relies on $20 Billion in Reserves. The May Revision’s estimate of tax revenues in the current year represents over 30 percent growth from three years ago. Much of this growth is driven by the personal income tax, which is up nearly 50 percent during that same period. Periods of elevated revenues like these are typically when the state should be strengthening its fiscal position. Instead, the May Revision draws it down—relying on roughly $20 billion in reserve withdrawals and suspended deposits, as well as $4 billion in borrowing (on top of tens of billions of dollars in existing borrowing), to achieve budget balance.

Structural Problem Is Now Upon the State. For several years, we have cautioned that structural deficits were emerging and would soon require corrective action. Despite the current revenue boom, the state now faces a structural budget imbalance—meaning ongoing revenues are insufficient to support ongoing expenditures.

Future Deficits Have Come Down Substantially, but State Ill‑Prepared for a Slip Up in Revenues. In January, we noted that our office and the administration estimated the state faced future deficits between $20 billion and $30 billion per year. Due to a combination of higher revenue estimates, lower baseline spending, and ongoing proposals (which both raise revenue and reduce spending), the May Revision cuts these future deficits in half. Despite this progress, the underlying budget condition is not sound. First, the existence of any operating deficits during a revenue boom of this magnitude is itself a warning sign. Further, given the state’s diminished reserves and already accumulated wall of debt, California is ill‑prepared for even a slip up in revenues. Even just a repeat of the 2022 market declines, which were mild by historical standards, could quickly push the budget into deep deficits. Alarmingly, given current market conditions, the dot‑com bust probably is a better parallel. If such scenario were to repeat, the revenue hole could be $100 billion.

Recommendations. The state’s current fiscal situation is genuinely unprecedented. Despite booming revenues, the budget position is overextended, reflecting: a structurally higher spending base, diminished reserves, an already accumulated wall of debt, and an operating deficit. As such, we recommend the Legislature take action to put the budget on sound fiscal footing, including:

- Maintaining Amount of Ongoing Solutions Proposed by Governor. We recommend the Legislature maintain at least the amount of ongoing solutions included in the May Revision.

- Making a $20 Billion Discretionary Reserve Deposit. In light of current revenue conditions, we recommend the Legislature make a $20 billion discretionary deposit into the Budget Stabilization Account (BSA) this year. This would make notable progress toward the administration’s proposal that the state raise BSA reserves to 20 percent of General Fund tax revenues.

- Setting Aside $4 Billion for Potential Settle‑Up Obligation. We recommend the Legislature set aside $4 billion to pre‑fund this likely obligation.

Taken together, these recommendations require the state to identify roughly $24 billion in new budget capacity—or solutions—relative to the Governor’s May Revision. The Legislature could make significant progress toward this total by rejecting the proposals to set aside nearly $10 billion for next year and about $1 billion in new discretionary spending.

Introduction

On May 14, 2026, Governor Newsom presented a revised state budget proposal to the Legislature. This annual proposed revised budget is referred to as the May Revision. In this report, we provide a summary of and comments on this revised budget, focusing on the overall condition of the state General Fund—the budget’s main operating account. In the coming days, we will analyze the plan in more detail and provide additional comments in hearing testimony. (The information presented in this brief is based on our understanding of the administration’s proposals as of May 15, 2026. In many areas, our understanding of the proposals will continue to evolve.)

May Revision Balanced on Higher Revenues and Reserves

Higher Revenues Improve Budget Condition. Relative to the Governor’s budget, the administration’s May Revision estimate of revenues across the budget window (2024‑25 to 2026‑27) are higher by about $16 billion. This upgrade is almost entirely attributable to expectations for income tax collections, which are being driven by enthusiasm around artificial intelligence (AI) and the related stock market boom. This improves the budget’s bottom line.

Higher Spending Somewhat Offsets Higher Revenues. Under two initiatives, the State Constitution requires the state to set aside a share of revenues for schools and community colleges (Proposition 98, 1988) and debt payments and reserve deposits (Proposition 2, 2014). In line with the administration’s higher revenue estimates, both these requirements are also up. Across the rest of the budget, however, spending is slightly lower, largely reflecting updated estimates of state employee pension costs, which are driven by a technical correction.

Solutions and Discretionary Choices in May Revision

Solutions

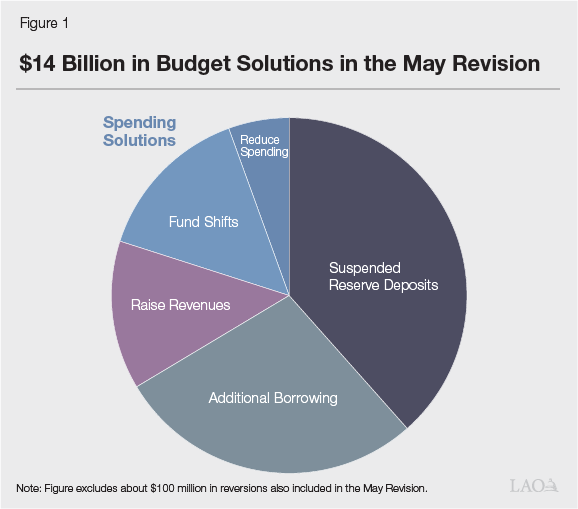

The May Revision includes $14 billion in solutions in 2025‑26 and 2026‑27 as shown Figure 1. This includes: $2 billion in revenue‑related proposals, nearly $3 billion in spending‑related solutions (including spending reductions and fund shifts), $4 billion in new borrowing, and suspended reserve deposits of more than $5 billion. These solutions reflect all of those included in the May Revision, as well as those originally proposed in January. The remainder of this section walks through each of these components in more detail.

Revenue‑Related Solutions

Proposes Larger Managed Care Organization (MCO) Tax. The MCO tax is a specific tax on health plans (such as Kaiser Permanente and Anthem Blue Cross) that helps pay for Medi‑Cal. It currently provides around $7 billion to $8 billion annually. It is set to expire at the end of 2026. The Governor’s budget assumed renewal of the tax in 2027, but at a much lower level—just tens of millions of dollars in annual revenue. The expected sizable reduction reflected the administration’s understanding of recent federal and state policy changes. The administration now believes it can pursue a larger tax and remain legally compliant. Accordingly, the May Revision proposes a 2027 MCO tax that provides around $2 billion annually. The Governor proposes using all of the revenue to offset General Fund costs in Medi‑Cal, resulting in annual savings of $575 million in 2026‑27 and around $2 billion in subsequent years.

Proposes Permanent Limit on Business Tax Credits. California allows corporations to claim a variety of tax credits that reduce their tax liability on a dollar‑for‑dollar basis. Taxpayers that have enough credits are allowed to reduce their tax bill down to $800. Under the May Revision, beginning in 2027, businesses would only be allowed to use tax credits to reduce their corporation tax liability by 50 percent or $5 million, whichever is greater. In contrast to recent limits on business credits, this change would be permanent. The administration estimates this would increase corporation tax revenues by $850 million in 2026‑27 and $1.7 billion in 2027‑28.

Apply Sales Tax to Retail Sales of Digital Prewritten Software. Software not customized for a particular client is called prewritten software. The state’s sales tax currently applies to prewritten software delivered on tangible media but not to other sales of software. The May Revision proposes to apply the state’s sales tax to prewritten software delivered in other ways—such as downloads and remote access—beginning in 2027. Custom software would remain exempt. The administration estimates that this would raise General Fund revenue by $450 million and local sales tax revenue by $560 million in 2026‑27, growing to $900 million General Fund and $1.1 billion local revenue in 2027‑28.

Spending‑Related Solutions

Expands Package of Medi‑Cal Solutions. The May Revision includes additional spending‑related budget solutions in Medi‑Cal relative to the Governor’s budget. In 2026‑27, the additional savings would be $1.8 billion, mostly from a limited‑term proposal to use more funding from Proposition 35 (2024) to help pay for Medi‑Cal provider rate increases. The May Revision also includes several new ongoing solutions, including proposals to lower the asset limit for seniors and persons with disabilities and to increase the monthly premium charged to adults with unsatisfactory immigration status. Including proposals from January, the May Revision solutions associated with Medi‑Cal are $2.2 billion in 2026‑27, including $400 million in reductions and $1.8 billion in fund shifts.

All Other Spending‑Related Solutions Total $500 Million. Across the rest of the budget, the May Revision includes $500 million in other spending‑related solutions (including both proposals that persist from January and new proposals in May). These are relatively evenly split between spending reductions and fund shifts. For example, other spending‑related solutions include: about $200 million in behavioral health offsets across a variety of departments, $50 million in savings to align In‑Home Supportive Services eligibility with Medi‑Cal, and $50 million in a reduction in the cost‑of‑living adjustment for child care.

Borrowing

May Revision Includes $4 Billion “Settle‑Up” Obligation. The May Revision generates a $4 billion settle‑up payment by providing less than the constitutionally required funding level for schools and community colleges in 2025‑26. (The Governor’s budget had proposed a larger settle‑up payment of nearly $6 billion.) Settle up gives the state more budget capacity this year, but if revenues meet expectations for 2025‑26 it would eventually require the state to make a payment of this amount to schools and community college districts. (Conversely, if revenues fall short of their projections, the state’s settle‑up obligation would decline.) We understand this proposal is intended, in part, to acknowledge revenue risks and avoid unintentionally spending more than the minimum requirement if revenues decline and the requirement drops.

May Revision Would Bring Total Borrowing Close to $30 Billion. Recent budgets have relied on over $25 billion in budgetary borrowing to close budget gaps. These are amounts that will need to be repaid in the coming years—most of which will add to the state’s existing structural deficits. We call this budgetary borrowing the state’s new “wall of debt,” in line with a Great Recession era term that described budgetary borrowing accumulated to partially address the state’s persistent budget problems. The May Revision proposal to create nearly $4 billion in settle up would add to the wall of debt by that amount. (The May Revision also reflects some repayments of certain debts.)

Suspended Reserve Deposits

Suspends Budget Stabilization Account (BSA) True‑Up Deposit of $5.4 Billion. Proposition 2 outlines the formulas by which the state must, each year, make deposits into the BSA, unless those requirements are suspended under a budget emergency. Proposition 2 also requires the state to revisit—or “true up”—its estimates of BSA deposits twice: once in each subsequent fiscal year. These true‑ups are required even if the initial deposit was suspended; however, true‑ups can themselves be suspended, as well. The state already suspended a $1.6 billion initial deposit for 2025‑26. Under the administration’s revenue estimates, an additional $5.4 billion true‑up deposit is now required for that year. The May Revision proposes the state suspend this entire true‑up deposit.

New Commitments

Revenue and Spending Commitments

New Discretionary Proposals of $1.3 Billion. The May Revision includes $1.3 billion in new discretionary proposals (some of which were proposed at Governor’s budget). These use budget capacity and mean that more solutions are required to balance the budget. This entire amount is driven almost exclusively by many small proposals rather than a few larger proposals. For example, some of the largest of these items are: $76 million for utility replacement and site improvements at Exposition Park; a $68 million reappropriation for broadband last‑mile infrastructure; and $56 million for a disaster rebuilding program. The remainder of the list includes about 100 proposals, mostly less than $20 million. (This also includes $25 million for one new revenue‑related proposal in 2026‑27 which grows to $100 million in 2027‑28.)

Discretionary Reserves and Set‑Asides

Sets Discretionary Reserve Balance to $4.5 Billion. The Special Fund for Economic Uncertainties (SFEU) is a general‑purpose reserve commonly used to provide capacity for unanticipated expenditures, including state costs associated with disasters and other emergencies. On a technical basis, it can be thought of as the end balance of the state’s General Fund—the money that remains after accounting for all of the state’s expected revenues and spending. The State Constitution has a balanced budget requirement, which means the balance of the SFEU must be set above zero for the upcoming fiscal year (2026‑27). Any level above that is up to the discretion of the Legislature. As a result, we consider the entire balance of the SFEU to be a discretionary choice. That said, recent budgets have set the SFEU between $3.5 billion and $4.5 billion, so the Governor’s budget proposal to set the balance to $4.5 billion is in line with recent policy.

Deposits $10 Billion Into Temporary Surplus Holding Account (TSHA). The May Revision proposes a first‑time deposit of nearly $10 billion into the TSHA—an account created to help the state avoid overcommitting a surplus when revenues are surging. That said, although revenues are currently surging, by our count, there is no “surplus” to overcommit. The box below describes this account and proposal in more detail.

What Is the Temporary Surplus Holding Account (TSHA)?

Revenues Are Both Volatile and Uncertain. State revenues are volatile—they can grow or shrink rapidly from year to year, particularly because California’s tax system relies heavily high‑income taxpayers. This means that, in some years, the state will collect significantly less in tax revenue than it has in spending commitments—resulting in large budget problems. Relatedly, there is significant uncertainty about near‑term revenue estimates—that is, even for the upcoming fiscal year, revenues can come in significantly above or below projections, resulting in large forecasting errors. This is especially common when revenues are growing or shrinking rapidly. Reserves can help address both challenges—volatility and uncertainty. Historically, however, the state’s reserves have primarily been used to manage revenue volatility across economic cycles rather than short‑term uncertainty in forecasting.

TSHA Was Set Up to Avoid Overspending a Surplus. In 2024, the Legislature created the TSHA as a tool intended to manage near‑term revenue uncertainty. As we understand it, the account was designed for periods when the state is experiencing surpluses during rapid revenue growth and might otherwise risk committing to new spending based on uncertain revenue estimates that might not materialize. The Legislature initially considered establishing formulas or rules governing deposits into the account. Ultimately, however, the TSHA was enacted as a flexible and largely discretionary mechanism.

Governor Proposes Using TSHA for First Time in May Revision. The May Revision proposes depositing $9.7 billion into the TSHA in 2026‑27 and withdrawing the same amount in 2027‑28. We understand the administration derived this amount from the remaining resources available after accounting for baseline costs, budget solutions, and new proposals, including a Special Fund for Economic Uncertainties balance of $4.5 billion. In effect, the TSHA proposal uses anticipated resources from 2026‑27 to help balance the budget in 2027‑28.

Budget Condition

Budget Condition This Year

Figure 2 shows the General Fund condition under the May Revision. The state would end 2026‑27 with $4.5 billion in the SFEU. The SFEU is the state’s operating reserve and essentially functions like an end‑of‑year balance. The State Constitution prohibits the state from enacting a negative SFEU for the upcoming fiscal year, in this case 2026‑27.

Figure 2

General Fund Condition Summary

(In Millions)

|

2024‑25 |

2025‑26 |

2026‑27 |

|

|

Prior‑year fund balance |

$54,124 |

$56,576 |

$56,190 |

|

Revenues and transfers |

233,639 |

245,442 |

222,875 |

|

Expenditures |

231,187 |

245,828 |

246,566 |

|

Ending fund balance |

$56,576 |

$56,190 |

$32,498 |

|

Encumbrances |

$27,998 |

$27,998 |

$27,998 |

|

SFEU Balance |

$28,578 |

$28,192 |

$4,500 |

|

Reserves |

|||

|

BSA |

$18,596 |

$11,497 |

$15,075 |

|

SFEU |

28,578 |

28,192 |

4,500 |

|

Safety net |

— |

— |

— |

|

Total Reserves |

$47,174 |

$39,689 |

$19,575 |

|

SFEU = Special Fund for Economic Uncertainties and BSA = Budget Stabilization Account. |

|||

Under May Revision, Reserves Would Total Nearly $20 Billion at End of 2026‑27. Under the Governor’s May Revision proposals and assumptions, general‑purpose reserves would total nearly $20 billion by the end of 2026‑27. This includes an SFEU balance of $4.5 billion and about $15 billion in the state’s main constitutional reserve, the BSA. These balances would be available to mitigate a future budget problem. (In addition, the state would have about $10 billion in the Proposition 98 Reserve, available only for school and community college programs.)

Budget Relies on Use of $20 Billion in Reserves From BSA. One major factor allowing the budget to achieve balance in Figure 2 is the use of roughly $20 billion from the BSA. This amount reflects a combination of reserve withdrawals and the suspension of otherwise required deposits. Many of these actions were adopted in prior budgets. As a result, we treat most of them as part of the “baseline” budget rather than as budget solutions. That said, in total, the $20 billion reserve use consists of: (1) a $1.5 billion suspension of the initially required BSA deposit in 2024‑25, (2) a $5 billion BSA withdrawal in 2024‑25, (3) a $7 billion suspension of the initially required BSA deposit and true‑up now required for 2025‑26, and (4) a $7 billion BSA withdrawal in 2025‑26.

Multiyear Budget Condition

Budget Is Balanced in 2026‑27 and 2027‑28. The State Constitution requires the budget be “balanced” for the upcoming fiscal year. This means that cumulative resources available must not exceed cumulative expenditures across the budget window. In other words, the estimated SFEU for the budget year—in this case 2026‑27—must be greater than zero. (This was shown in Figure 2.) The administration also makes proposals that would result in a balanced budget in 2027‑28. The May Revision achieves this by relying on one‑time resources. These include unspent money from prior years, use of reserves, and the TSHA‑related deposit and withdrawal.

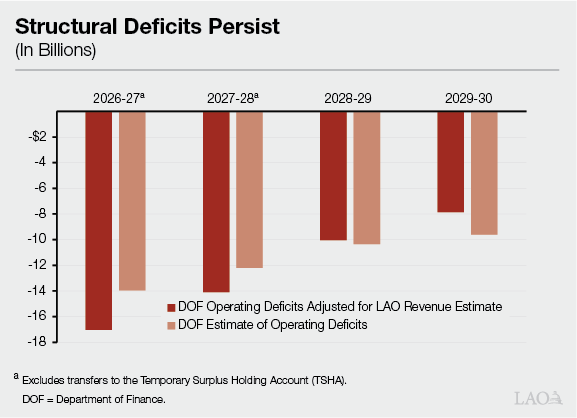

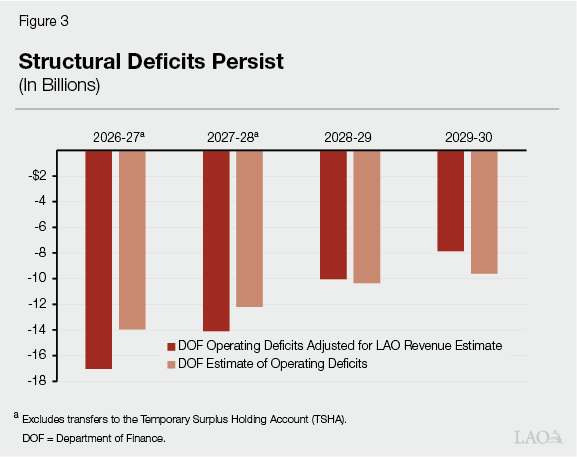

However, Structural Deficits Persist Under the Administration’s Estimates and Proposals. A budget is structurally balanced when revenues collected in a given fiscal year are sufficient to cover expenditures planned for that same year. On this basis, the administration’s estimates show operating deficits of roughly $10 billion annually from 2026‑27 through 2029‑30, as shown in Figure 3. Beginning in 2027‑28, these deficits represent the ongoing gap that would need to be addressed in future budgets.

Using Our Revenue Estimates Does Not Substantively Change the Picture. Figure 3 also shows the state’s operating deficits assuming our revenue estimates. (This shows our estimate of revenues and revenue‑driven spending, such as for Proposition 98 and Proposition 2, but takes the administration’s estimate of all other spending.) As the figure shows, the picture of the budget condition is essentially the same under our revenue estimates.

Schools and Community Colleges Budget

This section describes the May Revision spending and proposals for schools and community colleges. The information presented in this section is relative to the administration’s January proposals.

Proposition 98 Funding Requirement Revised Up Significantly. Proposition 98 sets a minimum funding requirement for schools and community colleges based on formulas in the State Constitution. Compared with the January budget, the May Revision estimates that this requirement has increased by $6.4 billion over the 2024‑25 through 2026‑27 period. This increase reflects higher General Fund revenue estimates, partially offset by lower local property tax estimates.

Other Adjustments Make Additional Funding Available. Separate from the higher minimum requirement, roughly $3.8 billion is freed up by lower baseline costs in the state’s main school funding formula over the 2024‑25 through 2026‑27 period. The Governor also scales back his January proposal to delay some Proposition 98 funding to future years, making an additional $1.6 billion available in this year’s budget. Additionally, $807 million in unspent funds from previous budgets is available for reallocation.

May Revision Deposits $6.2 Billion Into Proposition 98 Reserve. The Proposition 98 Reserve is a statewide account earmarked exclusively for schools and community colleges. The May Revision makes a $4.6 billion mandatory deposit into this reserve triggered by increased capital gains revenue. It also makes a $1.6 billion discretionary deposit. The total reserve balance would grow to $10.3 billion, which equates to 8.3 percent of the Proposition 98 funding requirement in 2026‑27.

May Revision Contains $6.9 Billion in New Spending. After accounting for changes in the Proposition 98 requirement, baseline costs, and reserve deposits, among other adjustments, the May Revision has $6.9 billion for new school and community college spending. This amount is in addition to the $10.9 billion in new spending from the January budget. The Governor proposes allocating most of the $6.9 billion for discretionary grants and augmentations to existing programs. Specifically, the May Revision prioritizes five main areas:

- A significantly larger one‑time discretionary grant for schools ($2.3 billion).

- A major ongoing increase in special education funding ($1.8 billion).

- A larger ongoing cost‑of‑living adjustment for school and community college programs ($1.5 billion).

- Additional one‑time funding for community schools, including grants for planning, implementation, and technical support ($485 million).

- Additional one‑time funding for literacy coaches that would support existing grant recipients through 2030‑31 ($440 million).

Comments

Budget Window

Revenues Are Booming, but Estimates Are Reasonable. The May Revision’s estimate of tax revenues in the current year represents over 30 percent growth from three years ago. Much of this growth is driven by the personal income tax, which is up nearly 50 percent during that same period. The May Revision anticipates these elevated revenues will be sustained in the budget year, albeit with only modest growth. These assumptions are roughly in line with our latest revenue forecast and reflect the reality of extraordinary income tax collections in recent months and a booming stock market.

Despite Revenue Boom, Budget Architecture Relies on $20 Billion in Reserves. Periods of elevated revenues, such as the current cycle of strong personal income tax receipts, are typically when the state should be strengthening its fiscal position. Instead, the May Revision draws it down—relying on roughly $20 billion in reserve withdrawals and suspended deposits, as well as $4 billion in borrowing (on top tens of billions of dollars of existing borrowing), to achieve budget balance. These actions should be reserved for addressing revenue shortfalls in downturns, not to balance the budget during a revenue boom.

Structural Problem Is Now Upon the State. For several years, we have cautioned that structural deficits were emerging and would soon require corrective action. Despite the current revenue boom, the state now faces a structural budget imbalance—meaning ongoing revenues are insufficient to support ongoing expenditures. This condition is present in both 2025‑26 and 2026‑27. The administration reports a structural deficit of $400 million in 2025‑26 and $14 billion in 2026‑27. (In 2025‑26, a one‑time withdrawal from the BSA reduces the operating deficit, but excluding that withdrawal—which is more consistent with measuring ongoing budget conditions—would result in a structural deficit of about $7.5 billion in that year.)

Multiyear

Future Deficits Have Come Down Substantively… In January, we noted that our office and the administration estimated the state faced future deficits between $20 billion and $30 billion per year. Due to a combination of higher revenue estimates, lower baseline spending, and ongoing proposals (which both raise revenue and reduce spending), the May Revision cuts these future deficits in half. As a result, under the May Revision, projected deficits are now closer to $10 billion per year. This is substantive progress and in line with our guidance in January.

…But State Ill‑Prepared for a Slip Up. Despite this progress, the underlying budget condition is not sound. First, the existence of any operating deficits during a revenue boom of this magnitude is itself a warning sign. Further, given the state’s diminished reserves and an already accumulated wall of debt, California is ill prepared for even a slip up in revenues. Stock market runs like the one seen in the last three years almost always end in a dramatic reversal. Many classic warning signs suggest this market run may be nearing its end. Should the stock market reverse course, tax revenues would decline significantly. Even just a repeat of the 2022 market declines, which were mild by historical standards, could quickly push the budget into deep deficits. Specifically, income tax revenues across 2022‑23 and 2023‑24 fell $65 billion below 2022‑23 Budget Act estimates. Alarmingly, given current market conditions, the dot‑com bust probably is a better parallel. If such scenario were to repeat, the revenue hole could be $100 billion. Using this year’s budget to build resilience would allow the state to weather this kind of shock without immediately needing to turn to tax hikes or cuts to ongoing services.

Recommendations

Maintain Amount of Ongoing Solutions Proposed by Governor. In January, we recommended the Legislature reduce the structural deficit by at least half. The May Revision effectively achieves that goal. We therefore recommend that—in the final budget—the Legislature maintain at least the amount of ongoing solutions included in the May Revision.

Make a $20 Billion Discretionary Reserve Deposit. While the Governor has made progress in addressing the state’s future budget problem, the May Revision relies on reserves to support near‑term budget balance despite booming revenues. The timing of these budget decisions matters. Near‑term revenues are much more certain than those projected in later years, where uncertainty compounds. As a result, building budget resilience now is just as important—if not more so—than addressing structural deficits. In light of current revenue conditions, we recommend the Legislature make a $20 billion discretionary deposit into the BSA this year, reversing the reserve reliance described above. (There is no cap on discretionary deposits into the BSA. As such, under this recommendation, total reserves would reach 17 percent of General Fund tax revenues, while also allowing for additional mandatory deposits into the BSA under the constitutional rules. This would make notable progress toward the administration’s proposal that the state raise BSA reserves to 20 percent of General Fund tax revenues.)

Set Aside $4 Billion for Potential Settle‑Up Obligation. The administration’s settle‑up proposal has merit in that it protects the budget from the risk of revenues coming in lower than anticipated and obligating the state to a spending level that is higher than constitutionally required. However, if revenues come in at or above the level currently anticipated for 2025‑26, the state will owe an additional $4 billion to schools and community colleges in a future year. In effect, this proposal allows the state to support more spending in the near‑term by creating a future obligation. We recommend the Legislature set aside $4 billion in a reserve to pre‑fund this likely obligation.

$24 Billion in Solutions Necessary to Achieve Recommendations. Taken together, the recommendations above require the state to identify roughly $24 billion in new budget capacity—or solutions—relative to the Governor’s May Revision. Redirecting the transfer to the TSHA and rejecting all of the Governor’s discretionary proposals would yield about $11 billion in capacity—making significant progress toward our recommended total. In addition, we recommend that any potential upward revisions to revenue estimates between now and the budget enactment be used for additional reserve deposits. Even with these actions, however, the Legislature would still need to identify roughly $10 billion in additional solutions, including both revenues and spending, and which could either be ongoing or one‑time.

Conclusion

The state’s current fiscal situation is genuinely unprecedented. Despite booming revenues, the budget position is overextended, reflecting: a structurally higher spending base, diminished reserves, an already accumulated wall of debt, and an operating deficit. Meanwhile, a revenue shock could be coming, as the state’s revenue outlook rests disproportionately on AI‑driven equity valuations that are trading at highs last seen at the peak of the dot‑com bubble.

These conditions warrant a disciplined and cautious fiscal approach. In our view, this means recognizing that recent revenue performance may not represent a sustainable long‑term baseline for the budget. It also means aligning ongoing spending commitments more closely with the state’s long‑run revenue capacity, prioritizing rebuilding reserves—even at the expense of additional spending cuts or revenue increases—and planning explicitly for downside scenarios. Should a significant revenue correction occur, the state may require many of the same fiscal tools—reserves, borrowing, and budget flexibility—that are currently being used to manage the existing structural imbalance.