Our office recently published an updated revenue outlook to assist the Legislature as it finalizes its 2015-16 state budget plan in the coming weeks. We estimate that the state General Fund will collect somewhat more revenue in 2015-16 than the administration estimates. Most of the difference in our revenue numbers concerns the personal income tax (PIT). The LAO's higher PIT estimates for 2015-16 stem in large part from our higher projection of taxable income growth. We project that PIT filers' taxable income in 2015 will grow by 6.7%, compared to 4.7% in the administration's numbers.

The differences in our estimates, however, start with 2014 taxable income related to the PIT, as we describe below.

2014 PIT Collections. For many categories of income, our estimating process is based on past trends, which we then project forward based on the economic scenario that underpins our future budget outlook. Tax data, however, comes with an unavoidable lag. Therefore, we will not begin to receive detailed data on 2014 PIT returns filed with the state until later this year, with comprehensive data to follow next year. While no comprehensive data is yet available on what PIT filers listed in their 2014 tax returns, most of the revenue attributable to 2014 has already been collected, as follows:

- Wage and salary withholding payments submitted by employers generally were collected by the end of 2014, and these amounted to $49.1 billion.

- Quarterly estimated payments paid largely by upper-income taxpayers generally were collected by the end of January 2015. These totaled $20.4 billion.

- Some other tax payments are categorized by the Franchise Tax Board (FTB) as "final and miscellaneous" payments. (Final payments for 2014 may be the ones made by filers when they submit their April tax returns or their October extension returns. Miscellaneous payments for 2014 may be the ones made by filers in April to "settle up" for the year in advance of their October extension return submissions, withholding paid to FTB, or various other payments.) FTB has processed most of the final and miscellaneous payments ($11.9 billion to date) and refunds ($7.9 billion to date) calculated for 2014. (Last year, about 70% of final and miscellaneous payments and refunds for tax year 2013 had been processed by the end of April 2014.)

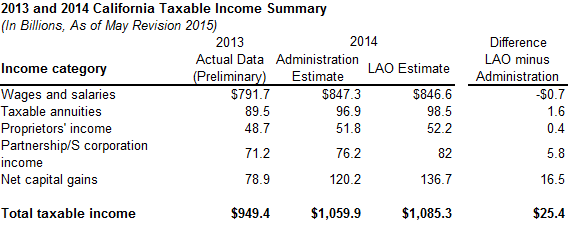

Based on this collections information, both our office and the administration have to make "best guess" estimates of what happened to 2014 taxable income as a part of our process of projecting what the state will collect in PIT revenues in 2015 and thereafter. Below, we summarize some major LAO and administration estimates of income categories for 2014, as well as the most recent FTB data on 2013 PIT returns. As shown below, most of the differences between the LAO and administration figures for 2014 are in the categories of net capital gains and partnership/S-corporation income.

2014 tax collections will continue to come in over the next few months. For the remainder of 2015, we at the LAO are estimating that final and miscellaneous payments on 2014 income will show the same year-over-year increases as April 2015 collections did relative to April 2014. This works out to year-over-year growth rates of 20.7% for final and 24.4% for miscellaneous payments. In contrast, we understand that the administration is assuming somewhat slower growth in final payments and little or no growth in miscellaneous payments over the same period. This difference likely results in a bit less than half of the difference above in 2014 estimated taxable income.

Various other differences affect our respective PIT estimates during this time period in our revenue outlook, although our differing estimating techniques make it difficult to compare the two projections precisely in all respects. For example, the two estimates likely have different assumptions about the distribution of income growth. The administration informed us that its 2014 estimates assumed that a substantial portion of 2014 wage and capital gains growth went to the highest-income taxpayers. As higher income taxpayers pay higher average tax rates, a smaller taxable income total like the administration's that is more heavily weighted toward high-income groups can produce the same revenue as a larger taxable income total more weighted to lower- and middle-income taxpayers. Moreover, our PIT estimates also have different accrual estimates.