-

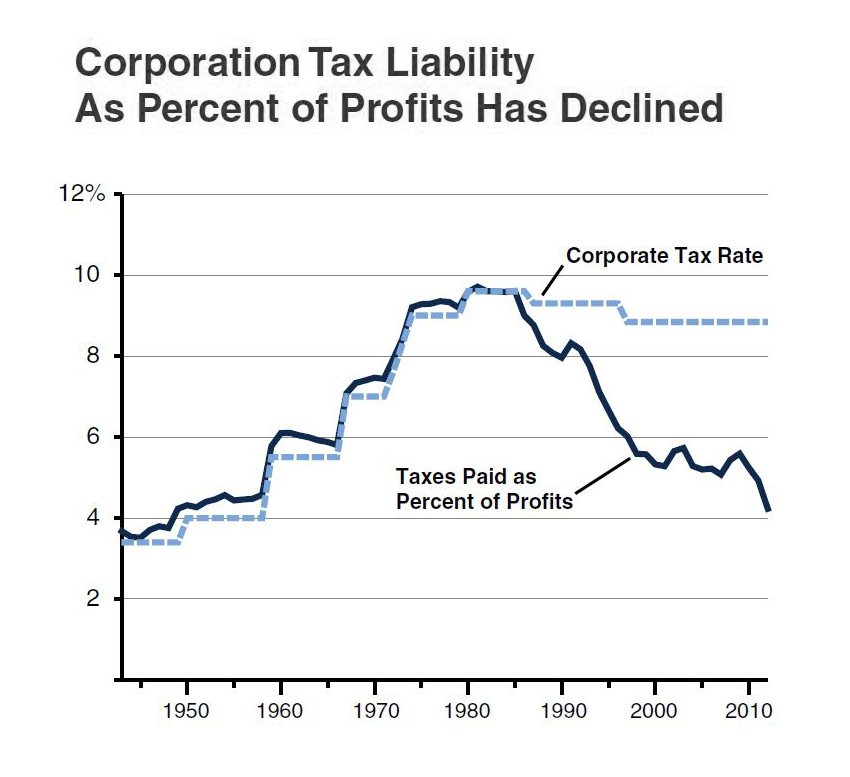

California State Corporate Income Tax Rates. The main tax rate for a traditional C-corporation is 8.84 percent. Banks pay a higher rate. S-corporations, which pass on their income directly to shareholders, pay much lower rates.

-

Tax Liability Can Be Reduced Using Credits and Other Tax Law Provisions. Using various provisions of state tax law, such as tax credits, corporations may reduce their tax liability. This can result in firms’ final tax liabilities—as a percent of their California profits—being less than the applicable corporate tax rate in state law. The average tax liability as a percent of profits is sometimes called the effective average tax rate (EATR).

-

Corporation Tax Liability, As a Percent of Profits, Less Than Half of the Statutory Rate. Across all corporations reporting positive net income, the EATR (displayed above as "taxes paid as percent of profits") was 4.2 percent in 2012, based on May 2014 Franchise Tax Board (FTB) data. This is less than half of today's main 8.84 percent California corporate tax rate and is the lowest corporation tax EATR recorded in California since about 1950. (In 1950, the main corporation tax rate was 4.0 percent, and the EATR was slightly higher in part because of the higher rate paid by banks.) Recent data suggest that in 2013 the EATR may have risen somewhat. (Data on corporation profits and tax liability for 2012 and some prior years is from Exhibit B-2, page 2, of FTB's May 2014 revenue estimating exhibits.)

-

Corporate EATR Has Been Falling Since the Mid-1980s. Historically, the EATR has closely tracked the statutory tax rate. This relationship changed beginning in the mid-1980s as the state made various major changes in corporate tax law. Three of the more significant factors include:

-

The state has expanded the amount of some tax credits.

-

The state has increased over time corporations’ ability to deduct prior losses from current income.

-

The number of S-corporations has been increasing.

-

- For More Information... For more information on long term trends in the state corporation tax, see our March 2014 letter to Senate budget committee members on the topic. (Some data has been updated in this post, compared to information included in that letter.)