The Quiet Transformation in California’s Cash Management

August 29, 2019

Gabriel Petek

Gabriel Petek

Legislative Analyst

California’s absence from the short-term debt markets again this summer is one measure of how much the state’s overall fiscal health has improved since the recession ended. As described in our recent report, Managing California’s Cash, the state’s standard practice until recently was to issue short-term notes in the capital markets—typically in August or September—for cash management purposes. California’s constitutional balanced budget requirement notwithstanding, some form of short-term borrowing is necessary because cash receipts and disbursements within the year do not line up. General Fund disbursements are spaced relatively evenly throughout the fiscal year while a majority of tax collections are received later in the year. To bridge the resulting cash-gap, the state arranges for short-term loans to the General Fund. Traditionally, this involved tapping financial markets for at least some of the funds. Now and for the past several years, however, California has had the fiscal wherewithal to self-finance its interim cash deficits.

Larger Budget Reserves Structurally Changed California’s Cash Management

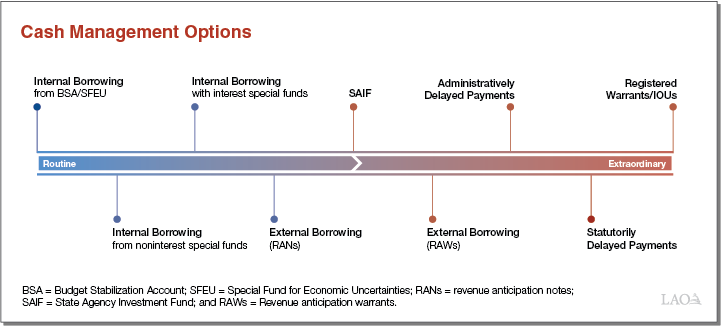

As with the state’s budget position, there is a cyclical quality to California’s cash condition. The state’s cash situation is often revealed by the tools the State Controller employs for cash management, which we describe as falling along a spectrum. In good economic times, revenues often outpace budget assumptions, causing the state’s overall cash position, both in the General Fund and its special funds, to strengthen. Higher cash balances allow the state to cover more of its interim cash needs through routine forms of internal borrowing. Conversely, when the economy enters a downturn, the state’s cash position is prone to erosion. Historically, it was common that the further the state’s internal liquidity deteriorated, the more extraordinary the cash management actions it required. One constant, however, was that for more than three decades from 1982 through 2014, the state almost always relied on some amount of external borrowing, regardless of the business cycle. (There was one exception, in 2000, during which the state did not borrow externally.) Although external borrowing is relatively common for governments and corporations alike—placing it nearer the routine end of the spectrum—it amounts to a confirmation that internal liquidity is periodically insufficient. Municipal bond investors had come to expect California’s external borrowing as a perennial event, deemed necessary by the pronounced seasonality of the state’s cash flows.

Given this history, it is notable that in 2015 the state discontinued its practice of borrowing externally for cash management purposes. This partly reflected cyclical factors, including the ongoing economic recovery that was instrumental in helping increase cash balances in the special funds. There were also structural changes that deepened the state’s reservoir of internal liquidity. As part of its response to the state’s recession-related liquidity crisis in 2009, the Legislature passed several laws that broadened the list of internally borrowable funds. Several years later, in 2014, the Legislature placed Proposition 2 on the ballot which changed the rules of the Budget Stabilization Account (the state’s main budget reserve). The strengthened reserve provisions of Proposition 2 proved to be pivotal in California’s cash management history. Prior to the election, proponents of Proposition 2 argued that a robust budget reserve could help stabilize government operations by partially offsetting the fiscal effects of economic cyclicality. There was less emphasis on the potential for the state’s reserves—when combined with other sources of internal liquidity—to transform its cash management activities. Nevertheless, the evidence in subsequent years suggests the state’s enhanced reserve policy and increased balances have had a profound effect on the state’s cash management capacity. In 2015‑16—soon after the reserve provisions of Proposition 2 took effect—the state managed its cash deficits without any external borrowing. The state’s self-sufficient approach to cash management has also been sustained, as 2019‑20 is now the fifth consecutive year during which the state anticipates managing its cash needs exclusively with its internal resources.

The Advantages of Self-Sufficient Cash Flow Management

The structural misalignment between California’s receipts and disbursements make its cash management activities a crucial, albeit behind-the-scenes, aspect of government operations. The way it works is the state borrows the funds necessary to pay for its operations early in the fiscal year, when its net cash flows are negative. Later in May or June, after the bulk of state personal income tax payments are remitted in April and net cash flows turn positive, the state repays the loan. In this sense, early in the year, the state’s General Fund is temporarily illiquid, but not insolvent. Borrowing externally, by issuing short-term notes in the public debt markets, is a common method of managing interim illiquidity. Corporations issue commercial paper to finance their receivables while many U.S. state and local governments—especially those with back-loaded revenue collections (such as California)—issue tax revenue anticipation notes. Nothing says this borrowing must take place in the capital markets, however. In order to conduct its cash management activities, the state is also authorized to borrow internally from its reserves and approximately 700 special funds in the State Treasury. There are at least three nontrivial benefits that the state can realize when it has sufficient liquidity on hand to finance its interim cash deficits from internal sources.

First, managing seasonal cash flow needs exclusively from internal sources means state operations are not vulnerable to disruption in the event that credit markets freeze. While California’s general creditworthiness and name recognition make it unlikely the state would be shut off entirely from borrowing, financial markets can be unpredictable. The ability to cover temporary cash deficits from internal sources insulates the state from the risk, however remote, of losing market access at the same time it needs to borrow for operations.

Second, and relatedly, internal borrowing is generally a lower cost option than borrowing externally, even when credit markets are placid. A review of transaction documents from the last several times the state issued revenue anticipation notes (RANs) shows that the state secured cash flow financing at interest rates of 1.5 percent to 3.0 percent. Assuming they are sold at par (meaning no bond premium or discount), the state’s annualized interest expense on $5 billion in RANs issued at 2.0 percent is $100 million. This is a material sum that most policymakers would presumably prefer to use in ways other than paying interest to bond investors. Furthermore, the cost of borrowing externally is not static through the business cycle. State finances are correlated with the economy such that economic contractions tend to magnify the opportunity cost of borrowing. Budget deficits, reduced internal liquidity, and—historically at least—a less stellar reputation in credit markets all become more likely when the economy is in a downturn. In a perverse confluence, therefore, at the time when it can least afford it, the state requires larger loans that tend to be priced at higher interest rates. At some point in the future, California almost certainly will once again need to satisfy some of its cash needs by issuing RANs. The more this can be delayed or minimized, the greater the savings to the state.

Finally, internal borrowing provides the state with more operating flexibility. Estimated monthly cash flows for the recently enacted 2019‑20 budget show that from July through December, the General Fund will borrow $18.5 billion from its reserves (Budget Stabilization Account and the Special Fund for Economic Uncertainties). Throughout the second half of the year, from January through June, the General Fund will return $13.6 billion to the reserves. The difference—$4.9 billion—will carry over into the subsequent fiscal year as a balance owed by the General Fund to its reserves. This contrasts with when the state borrows externally by issuing RANs, which must be repaid upon maturity. By statute, the maturity date for RANs must be set to occur no later than the last day of the fiscal year. (The state can issue Registered Anticipation Warrants with maturity dates that cross fiscal years, though these generally represent a more extraordinary cash management tool.) A failure to repay the entire amount borrowed plus interest on the maturity date is not an option as it would constitute a default.

Considerations for Managing State Liquidity

Many of the superlatives used to describe California’s budget position in recent years are similarly applicable to its cash condition. Thanks to prudent budget management throughout the economic expansion, both the state’s budget reserves and its internally borrowable cash resources are currently at historically high levels. Cash balances have grown so much that in addition to covering its internal cash flow needs, the Legislature has in recent years authorized two loans from the cash resources. (In 2017, SB 84 [Committee on Budget and Fiscal Review] authorized a $6 billion loan from the state’s Pooled Money Investment Account for a supplemental payment to CalPERS. In 2019, AB 1054 [Holden] authorized a loan of up to $10.5 billion for wildfire liability claims.) Mirroring the broader economy, it is inevitable that at some point, the state’s revenue trends will weaken. Historically, it has proven difficult to anticipate the timing and extent of a downturn in revenue collections. Strong internal liquidity, therefore, provides state policymakers with valuable time as they consider potential corrective budget actions. In the event revenues begin to come up short, the state can rely on internal cash balances to help cover its existing budget commitments until any needed fiscal adjustments take effect. This important function warrants exercising a careful approach to using the cash balances for other purposes when the economy is still expanding.