LAO Contact

November 18, 2020

The 2021-22 Budget

The Fiscal Outlook for Schools

and Community Colleges

- Introduction

- Background

- 2019‑20 and 2020‑21 Updates

- 2021‑22 Estimates

- Outlook Through 2024‑25

- Key Considerations

Summary

Dramatic Rebound in the Outlook for School and Community College Funding. Each year, the state calculates a “minimum guarantee” for school and community college funding based upon a set of formulas established by Proposition 98 (1988). When the state enacted the budget in June, it had anticipated steep declines in state revenue and the minimum guarantee. Based on the much stronger revenue projections in our outlook, we estimate the 2020‑21 guarantee is up $13.1 billion (18.5 percent) over the June budget act level. We estimate the 2021‑22 guarantee is up another $595 million (0.7 percent) over our revised 2020‑21 estimate. Under a law enacted in June, the state also would be required to make a $2.3 billion supplemental payment on top of the guarantee in 2021‑22. After accounting for various baseline adjustments—including prior‑year revisions, a 1.14 percent statutory cost‑of‑living adjustment (COLA), and required deposits into the Proposition 98 Reserve—we estimate the Legislature has $13.7 billion in one‑time funds and $4.2 billion in ongoing funds available for allocation in the upcoming budget cycle.

Legislature Will Face Major Budget Decisions in the Coming Year. Under our outlook, the state has enough one‑time funds to reverse all of the payment deferrals it implemented in the June 2020 budget plan. By paying down deferrals, the Legislature could improve cash flow for schools and community colleges and reduce pressure on future Proposition 98 funding. Regarding ongoing funds, we think the Legislature should reassess the supplemental payments after reviewing all of its budget priorities. The funding decline these new payments were intended to address no longer exists, and the minimum guarantee is projected to grow faster than the cost of the COLA over the next several years. Regardless of its decision about supplemental payments, the Legislature might want to set aside some 2021‑22 funding for one‑time activities. Such an approach creates a buffer that helps protect ongoing programs in case the guarantee drops in the future. Potential uses for this one‑time funding include addressing student learning loss, paying down future pension costs, and building reserves.

Introduction

Report Provides Our Fiscal Outlook for Schools and Community Colleges. State budgeting for schools and the California Community Colleges is governed largely by Proposition 98. The measure establishes a minimum funding requirement for K‑14 education commonly known as the minimum guarantee. This report provides our estimate of the minimum guarantee for the upcoming budget cycle. The report has five parts. First, we explain the formulas that determine the minimum guarantee and review the key actions and assumptions in the 2020‑21 enacted budget. We then explain how our estimates of the Proposition 98 guarantee in 2019‑20 and 2020‑21 differ from the June 2020 estimates. Next, we estimate the 2021‑22 guarantee. Fourth, we examine how Proposition 98 funding could change through 2024‑25. Finally, we identify the amount of funding that would be available for new commitments in the upcoming year and describe some issues for the Legislature to consider as it prepares to allocate this funding. (The 2021‑22 Budget: California’s Fiscal Outlook contains an abbreviated version of our Proposition 98 outlook, along with the outlook for other major programs in the state budget.)

Background

Calculating the Guarantee

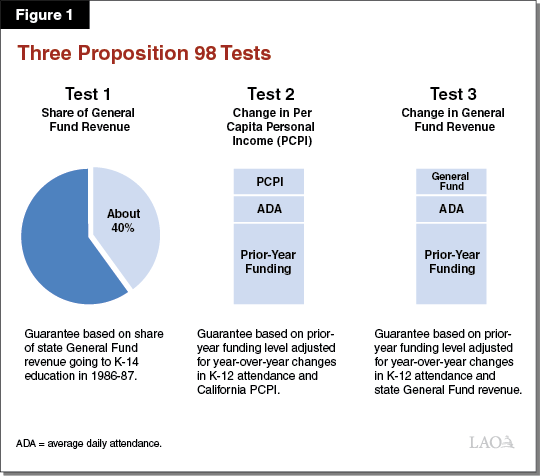

Minimum Guarantee Depends Upon Various Inputs and Formulas. The California Constitution sets forth three main tests for calculating the Proposition 98 minimum guarantee. Each test takes into account certain inputs, including General Fund revenue, per capita personal income, and student attendance (Figure 1). Whereas Test 2 and Test 3 build upon the amount of funding provided the previous year, Test 1 links school funding to a minimum share of General Fund revenue. The Constitution sets forth rules for comparing the tests, with one of the tests becoming operative and used for calculating the minimum guarantee that year. Although the state can provide more funding than required, in practice it usually funds at or near the guarantee. With a two‑thirds vote of each house of the Legislature, the state can suspend the guarantee and provide less funding than the formulas require that year. The state meets the guarantee through a combination of General Fund and local property tax revenue.

Legislature Decides How to Allocate Proposition 98 Funding. Whereas Proposition 98 establishes a minimum funding level, the Legislature decides how to allocate this funding among specific school and community college programs. Since 2013‑14, the Legislature has allocated most funding for schools through the Local Control Funding Formula (LCFF). A school district’s allotment under this formula depends on its size (as measured by student attendance) and the share of its students who are low income or English learners. The Legislature allocates most funding for community colleges through apportionments. A college’s apportionment funding depends on its enrollment, share of low‑income students, and performance on certain outcome measures.

At Key Points, State Recalculates Minimum Guarantee and Certain Proposition 98 Costs. The guarantee typically changes from the level initially assumed in the budget act as the state updates the relevant Proposition 98 inputs. The state continues to update these inputs until May of the following fiscal year. The state finalizes its calculation of the guarantee through a process known as certification, which involves the publication of all underlying inputs and a period for public review and comment. The most recently certified year is 2018‑19. The state also revises its estimates of certain school and community college costs, including LCFF and apportionments. When student attendance estimates change, for example, the cost of LCFF tends to change in tandem.

School and Community College Programs Typically Receive COLA. When the minimum guarantee is growing, the state generally funds a COLA for LCFF, community college apportionments, and certain other programs. The COLA rate is based on a national price index designed to reflect the cost of goods and services purchased by state and local governments across the country. Prior to 2019‑20, the Legislature approved funding for the COLA through the annual budget process. The 2019‑20 budget plan implemented a new policy for LCFF. Under this policy, LCFF receives an automatic COLA unless the minimum guarantee—as estimated in the enacted budget—is insufficient to cover the associated costs. In these cases, the COLA for LCFF (and other K‑12 programs) is reduced to fit within the guarantee. Though statute is silent on community college programs, the state generally aligns the COLA rate for these programs with the K‑12 rate.

Proposition 98 Reserve Deposits Required Under Certain Conditions. Proposition 2 (2014) created a state reserve specifically for schools and community colleges—the Public School System Stabilization Account (Proposition 98 Reserve). The Constitution requires the state to make deposits into this reserve under certain conditions. The most notable conditions are strong year‑over‑year growth in the guarantee and above average revenue from capital gains (see the box below). The state made its first deposit into the reserve in 2019‑20, but rescinded this deposit after revising its estimate of the minimum guarantee downward.

Key Rules Governing the Proposition 98 Reserve

Deposits Predicated on Four Main Conditions. To determine whether a deposit is required, the state first determines whether all of the following conditions are met:

- Revenues From Capital Gains Are Relatively Strong. Deposits are required only when the state receives an above‑average amount of revenue from taxes paid on capital gains (a relatively volatile source of General Fund revenue).

- Test 1 Is Operative. Test 1 years historically have been associated with relatively strong growth in the minimum guarantee due to strong growth in state revenue.

- Formulas Are Not Suspended. If the Governor declares a “budget emergency” (based on a natural disaster or slowdown in state revenues), the Legislature can reduce or cancel a reserve deposit. Additionally, if the Legislature votes to suspend the minimum guarantee, any required deposit is canceled automatically.

- Obligations Created Before 2014‑15 Are Retired. Proposition 2 (2014) specified that no deposits would be required until the state paid certain school funding obligations (known as “maintenance factor”) that it accrued during the Great Recession. The state met this condition starting in 2019‑20.

Amount of Deposit Depends Upon Additional Formulas. If the state determines that the conditions for a deposit are satisfied, it performs several calculations to determine the size of the deposit. Generally, the size of the deposit tends to increase when revenue from capital gains is relatively high and the guarantee is growing quickly relative to inflation. More specifically, the deposit equals the lowest of the following four amounts:

- Portion of the Guarantee Attributable to Above‑Average Capital Gains. The state calculates what the Proposition 98 guarantee would have been if the state had not received any revenue from “excess” capital gains (the portion exceeding the historical average). Deposits are capped at the difference between the operative guarantee and the hypothetical alternative guarantee without the excess capital gains.

- Difference Between the Test 1 and Test 2 Levels. Deposits are capped at the difference between the higher Test 1 and lower Test 2 funding levels.

- Growth Relative to the Prior Year. The state calculates how much funding schools and community colleges would receive if it adjusted the previous year’s funding level for changes in student attendance and inflation. (The inflation factor is the higher of the statutory cost‑of‑living adjustment or growth in per capita personal income.) Deposits are capped at the difference between the Test 1 funding level and the inflation‑adjusted, prior‑year funding level.

- Room Available Under a 10 Percent Cap. The Proposition 98 Reserve has a cap equal to 10 percent of all funding allocated to schools and community colleges. Deposits are only required to the extent the existing balance is below this threshold.

Withdrawals Required When Guarantee Is Growing Relatively Slowly. Proposition 2 requires the state to withdraw funds from the Proposition 98 Reserve if the minimum guarantee is not growing quickly enough to support the prior‑year funding level, as adjusted for student attendance and inflation. The Legislature can allocate withdrawals for any school or community college programs.

Proposition 98 Reserve Deposits Linked With Cap on School Districts’ Local Reserves. A state law enacted in 2014 and modified in 2017 sets a cap on local school district reserves after the balance in the Proposition 98 Reserve reaches a certain threshold. Specifically, the cap applies if the balance in the Proposition 98 Reserve in the previous year exceeded 3 percent of Proposition 98 funding allocated for K‑12 schools that year. Once the cap is operative, medium and large districts (those with more than 2,500 students) must limit their reserves to 10 percent of their annual expenditures. Smaller districts are exempt. The law also excludes certain categories of reserves, including reserves that are legally restricted to specific activities and reserves set aside by a district’s governing board for specific purposes. In addition, the law allows a district facing “extraordinary fiscal circumstances” to receive an exemption from its county office of education for up to two consecutive years. To date, the cap has not been operative.

Recap of 2020‑21 Budget Plan

Enacted Budget Assumed Significant Drop in the Minimum Guarantee. The emergence of the coronavirus disease 2019 (COVID‑19) led to an abrupt recession beginning in March 2020. By May, the administration had revised its previous revenue estimates down $42 billion across 2019‑20 and 2020‑21. These declines, combined with higher costs for the state’s safety net programs—including Medi‑Cal and California Work Opportunity and Responsibility to Kids—resulted in a $54.3 billion shortfall in the state budget. Regarding Proposition 98, the lower revenue estimates led to significant reductions in the minimum guarantee. The June 2020 budget plan assumed the guarantee would drop $3.4 billion (4.2 percent) in 2019‑20 and $10.2 billion (12.5 percent) in 2020‑21 relative to the 2019‑20 level estimated in June 2019.

Budget Plan Relied Heavily on Payment Deferrals. As a significant part of its effort to address the budget shortfall, the state reduced school and community college funding to the lower estimates of the minimum guarantee. It implemented these reductions primarily by deferring $12.5 billion in payments for LCFF, community college apportionments, and special education. (When the state defers payments from one fiscal year to the next, it can reduce spending while allowing districts to maintain programs by borrowing or using cash reserves.) These deferrals began with a $2.2 billion shift from the end of 2019‑20 to the following fiscal year. For 2020‑21, the budget plan maintained these deferrals and implemented $10.3 billion in additional deferrals. Under the modified payment schedule, portions of the payments otherwise scheduled for the months of February through June will be paid over the July through November period. The total amount deferred equates to about one‑fourth of the General Fund allocated for LCFF, community college apportionments, and special education. Other than implementing deferrals, the enacted budget largely held school and community college programs flat. (The budget did not include funding for the statutory COLA of 2.31 percent for 2020‑21.)

New Supplemental Payments Set to Begin in 2021‑22. The 2020‑21 budget plan included a statutory provision to accelerate school funding significantly in future years. This provision has two components. First, it requires the state to make temporary payments equal to 1.5 percent of annual General Fund beginning in 2021‑22. These payments will continue until the state has paid $12.4 billion—the difference between the June 2020 estimates of the guarantee for 2019‑20 and 2020‑21 and the amount of funding schools and community colleges could have received if state revenues had continued to grow. (Technically, the obligation equals the difference between the Test 1 and Test 2 funding levels in those years.) Second, it requires the state to increase the minimum share of General Fund revenue allocated to schools and community colleges from 38 percent to 40 percent on an ongoing basis. This increase is set to phase in over the 2022‑23 and 2023‑24 fiscal years. The supplemental payments are on top of the existing minimum guarantee, and the state can allocate them for any school or community college purpose.

2019‑20 and 2020‑21 Updates

Rapid Rebound for Many Parts of the Economy. In the spring of 2020, due to the COVID‑19 pandemic, millions of Californians lost their jobs, businesses closed, and consumers deeply curtailed spending. By the summer, the economy had begun to improve. Employment in the state started to recover. New business creation accelerated in July and has remained relatively strong. By October, consumer spending had recovered to within roughly 10 percent of its pre‑pandemic level. Some parts of the economy have done particular well. The stock market surpassed its pre‑pandemic level in August, and many technology companies—including several headquartered in California—have experienced strong growth. Despite these improvements, some parts of the economy remain depressed. Employment in the leisure and hospitality sector, for example, is about one‑third lower than its pre‑pandemic level. Many low‑wage workers—who experienced job losses at much higher rates than high‑wage workers—remain unemployed. (We provide more information on these trends in The 2021‑22 Budget: California’s Fiscal Outlook.)

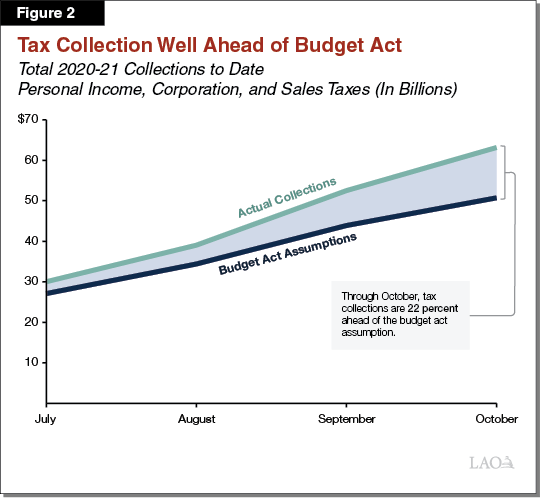

Significantly Higher Revenues Compared With June Assumptions. Tax collections for the state’s three largest taxes—the personal income tax, the corporation tax, and the sales tax—have been very strong over the past several months. Between August and October, collections were up 9 percent compared with the same period the previous year and 22 percent compared with June 2020 estimates (Figure 2). Tax collections at the end of 2019‑20 also exceeded expectations. Across the entirety of each fiscal year, we estimate General Fund tax revenues are up more than $4 billion in 2019‑20 and nearly $34 billion in 2020‑21 relative to the June 2020 estimates. Although these increases might seem at odds with high levels of unemployment, they are consistent with the more stable employment picture for high‑income workers, who account for a large share of state tax payments.

Proposition 98 Guarantee Revised Up Significantly. Compared with the estimates included in the June 2020 budget plan, we estimate the minimum guarantee is up $1.6 billion in 2019‑20 and $13.1 billion in 2020‑21 (Figure 3). These increases are due almost entirely to our higher General Fund revenue estimates. Test 1 remains operative in both years, with the increase in the General Fund share of the guarantee equating to about 38 percent of the higher revenue. Regarding local property tax revenue, our estimates are essentially unchanged from June in 2019‑20 and slightly higher in 2020‑21. The increase in 2020‑21 reflects faster growth in assessed property values and additional revenue attributable to the dissolution of redevelopment agencies. These property tax increases yield dollar‑for‑dollar increases in the minimum guarantee. (When Test 1 is operative, changes in local property tax revenue directly affect Proposition 98 funding. They do not offset General Fund spending.) Similar to the June budget, we also assume the state addresses a recent issue related to property tax allocations in certain counties (see box below).

Figure 3

Updating Prior‑ and Current‑Year Estimates of the Minimum Guarantee

(In Millions)

|

2019‑20 |

2020‑21 |

||||||

|

June |

November |

Change |

June |

November |

Change |

||

|

Minimum Guarantee |

|||||||

|

General Fund |

$52,656 |

$54,310 |

$1,655 |

$45,066 |

$57,818 |

$12,752 |

|

|

Local property tax |

25,022 |

24,973 |

‑49 |

25,824 |

26,157 |

333 |

|

|

Totals |

$77,678 |

$79,283 |

$1,606 |

$70,890 |

$83,975 |

$13,085 |

|

|

General Fund Tax Revenue |

$138,685 |

$143,012 |

$4,328 |

$118,666 |

$152,176 |

$33,510 |

|

Property Tax Estimates Assume State Resolves a Recent Issue

Schools and community colleges receive a portion of their property tax revenue through local accounts known as Educational Revenue Augmentation Funds (ERAF). These accounts, created in the early 1990s, facilitate various property tax shifts between educational agencies and other local governments (including cities, counties, and special districts). As we described in a report earlier this year, a few counties have been allocating a portion of their ERAF revenues in ways that seem contrary to state law and shift too much revenue from schools to other local agencies. On a statewide basis, the total amount of revenue at issue is nearly $350 million per year. In response to these findings, the Legislature adopted trailer legislation requiring the State Controller to issue instructions for the allocation of these revenues by December 31, 2020. The legislation also allowed the Controller to obtain an expedited court order for any county not complying with its new instructions. We assume these provisions result in this revenue being allocated to schools and community colleges.

Program Costs Down Across 2019‑20 and 2020‑21. For the prior and current year, we also update our estimates of costs for LCFF and other Proposition 98 programs (Figure 4). For 2019‑20, the latest available data show costs are down slightly ($28 million) from the state’s previous estimate. For 2020‑21, we estimate costs are down $476 million. This drop mainly relates to LCFF. Whereas the June budget had assumed LCFF costs would increase by more than $300 million on a year‑over‑year basis, our estimate reflects a year‑over‑year decrease of $112 million. Our estimate reflects several factors, including lower attendance costs carrying forward from 2019‑20 and continuing attendance declines in 2020‑21. We also account for the temporary changes to attendance funding included in the June 2020 budget plan, which limit the conditions under which growing districts can receive funding for higher attendance.

Figure 4

Additional Spending Required to Meet Guarantee in Prior and Current Year

(In Millions)

|

2019‑20 |

2020‑21 |

||||||

|

June |

November |

Change |

June |

November |

Change |

||

|

Minimum Guarantee |

$77,678 |

$79,283 |

$1,606 |

$70,890 |

$83,975 |

$13,085 |

|

|

Funding Allocations |

|||||||

|

Local Control Funding Formula (LCFF) |

$62,707a |

$62,676 |

‑$31 |

$63,037 |

$62,565 |

‑$473 |

|

|

Other K‑14 programs |

17,151a |

17,154 |

3 |

18,167 |

18,164 |

‑3 |

|

|

Savings from payment deferrals |

‑2,181 |

‑2,181 |

— |

‑10,314 |

‑10,314 |

— |

|

|

Proposition 98 Reserve deposit |

— |

— |

— |

— |

1,529 |

1,529 |

|

|

Totals |

$77,678 |

$77,649 |

‑$28 |

$70,890 |

$71,943 |

$1,053 |

|

|

Settle‑Up Payments |

— |

$1,634 |

$1,634 |

— |

$12,031 |

$12,031 |

|

|

aAmounts adjusted for Chapter 110 (SB 820, Committee on Budget and Fiscal Review), an August trailer bill that reduced LCFF cost estimates and allocated the savings for additional school meal reimbursements. |

|||||||

Proposition 98 Reserve Deposit Required in 2020‑21. Under the June 2020 budget plan, the Constitution did not require any deposit into the Proposition 98 Reserve because the state was projecting weak revenue from capital gains and the minimum guarantee was declining. Under our outlook, however, $1.5 billion of the growth in the guarantee is attributable to excess capital gains revenue. In addition, the year‑over‑year growth in the guarantee is well above the rate of inflation. Under these conditions, a $1.5 billion reserve deposit is required. (Our estimate assumes the deposit is not suspended. On June 25, 2020, the Governor declared a budget emergency related to the COVID‑19 pandemic, potentially allowing the Legislature to reduce or cancel the reserve deposit.)

State Required to “Settle Up” to Meet the Guarantee. After accounting for increases in the minimum guarantee, lower program costs, and the newly required reserve deposit, we estimate that spending is $1.6 billion below our estimate of the 2019‑20 guarantee and more than $12 billion below our estimate of the 2020‑21 guarantee. Across the two years, the state would be required make one‑time payments totaling $13.7 billion to settle up for the difference. The Legislature could allocate these payments for any Proposition 98 purposes.

2021‑22 Estimates

Guarantee Estimated to Grow Slightly Over Revised 2020‑21 Level. Under our outlook, the guarantee grows to $84.6 billion in 2021‑22. Relative to the 2020‑21 enacted budget level, this increase is substantial—$13.7 billion (19.3 percent). Compared with our revised estimate of 2020‑21, however, the increase is only $595 million (0.7 percent). Test 1 is operative, with the growth in the guarantee attributable to steady growth in local property tax revenue, partially offset by a small decline in General Fund revenue relative to our revised 2020‑21 estimate (Figure 5). (Our General Fund revenue estimates reflect our main economic forecast, discussed in the next section.)

Figure 5

Proposition 98 Near‑Term Outlook

LAO Estimates (Dollars in Millions)

|

2019‑20 |

2020‑21 |

2021‑22 |

|

|

Minimum Guaranteea |

|||

|

General Fund |

$54,310 |

$57,818 |

$57,285 |

|

Local property tax |

24,973 |

26,157 |

27,285 |

|

Totals |

$79,283 |

$83,975 |

$84,570 |

|

Change From Prior Yeara |

|||

|

General Fund |

‑$435 |

$3,507 |

‑$533 |

|

Percent change |

‑0.8% |

6.5% |

‑0.9% |

|

Local property tax |

$1,197 |

$1,184 |

$1,127 |

|

Percent change |

5.0% |

4.7% |

4.3% |

|

Total guarantee |

$762 |

$4,691 |

$595 |

|

Percent change |

1.0% |

5.9% |

0.7% |

|

Supplemental Paymentb |

— |

— |

$2,262 |

|

Total Funding With Supplemental Payment |

$79,283 |

$83,975 |

$86,831 |

|

Change from prior year |

762 |

4,691 |

2,857 |

|

Percent change |

1.0% |

5.9% |

3.4% |

|

General Fund Tax Revenuec |

$143,012 |

$152,176 |

$150,778 |

|

Growth Rates |

|||

|

K‑12 average daily attendance |

‑0.5% |

‑0.5%d |

‑0.5% |

|

Per capita personal income (Test 2) |

3.9 |

3.7 |

‑1.7 |

|

Per capita General Fund (Test 3)e |

‑0.1 |

7.0 |

‑0.7 |

|

Operative Test |

1 |

1 |

1 |

|

Proposition 98 Reserve |

|||

|

Deposit (+) or withdrawal (‑) |

— |

$1,529 |

$1,352 |

|

Cumulative balance |

— |

1,529 |

2,882 |

|

aExcluding supplemental payment. bConsists entirely of General Fund. cExcludes nontax revenues and transfers, which do not affect the calculation of the minimum guarantee. dFor the purpose of calculating the minimum guarantee, Chapter 24 of 2020 (SB 98, Committee on Budget and Fiscal Review) deems the change in attendance in 2020‑21 to be the same as the change in 2019‑20. eAs set forth in the State Constitution, reflects change in per capita General Fund plus 0.5 percent. |

|||

|

Note: No maintenance factor obligation is created, paid, or owed over the period. |

|||

Supplemental Payment Estimated at $2.3 Billion. On top of growth in the minimum guarantee, we estimate the state is required to make a supplemental payment of $2.3 billion. This payment represents the first installment toward the temporary component of supplemental payments (the ongoing component begins the following year). Including this payment, total Proposition 98 funding in 2021‑22 is up $2.9 billion (3.4 percent) over the revised 2020‑21 level.

Proposition 98 Reserve Deposit Triggers District Cap in 2022‑23. Under our revenue estimates, the state is required to make a Proposition 98 Reserve deposit of $1.4 billion in 2021‑22. This deposit, coupled with the 2020‑21 deposit, would bring the balance in the reserve to $2.9 billion—nearly 4 percent of our estimated funding for schools. By exceeding the 3 percent threshold, it also would make the district reserve cap operative the following year (2022‑23). (For this calculation, we assume the state allocates 89 percent of all Proposition 98 funding to schools and 11 percent to community colleges, consistent with its historical practice.) Based on the latest available data, we estimate that 129 of the medium and large districts that would be subject to the cap hold reserves exceeding 10 percent of their expenditures. The total amount above the cap is $1.3 billion—approximately one‑third of the reserves held by these 129 districts. Districts affected by the cap could respond by reclassifying their reserves to avoid the 10 percent limit, seeking exemptions from their county offices of education, or spending down their reserves.

Guarantee Is Moderately Sensitive to Changes in Revenue Estimates. We examined how the minimum guarantee would change if state revenue comes in higher or lower than our outlook assumptions. In general, the sensitivity of the guarantee depends on which Proposition 98 test is operative and whether another test could become operative with higher or lower revenue. Under our outlook, Test 1 is operative in 2020‑21 and 2021‑22. Test 1 is likely to remain operative even if revenues differ significantly from outlook assumptions, largely due to declining student attendance (a trend that tends to favor Test 1 compared with the other two tests). In Test 1 years, the guarantee changes about 40 cents for each dollar of higher or lower General Fund revenue.

Changes in Revenue Also Influence Reserve Deposits. Although the minimum guarantee would change in response to higher or lower revenues, the size of the Proposition 98 Reserve deposit also would change. Changes in the required deposit would tend to mitigate changes in the amount available for school and community college programs. In a scenario where revenue increases a couple billion dollars in 2021‑22 (with no change in 2020‑21), at least a portion of the increase likely would have to be deposited into the reserve. The required deposit also would tend to grow in scenarios where revenue increases in both the current and budget years. On the downside, a drop in revenues and the minimum guarantee would tend to reduce the size of the required reserve deposits. Although this reduction would cushion school and community college programs, the relatively small size of the deposit means this buffer would disappear quickly. (Our analysis holds all other Proposition 98 inputs constant, though changes in these inputs also could affect the guarantee and the size of the deposit.)

Outlook Through 2024‑25

Proposition 98 Funding

Certain Assumptions Underlie Our Main Economic Forecast. To develop our main economic forecast for the next several years, we build upon the average of numerous forecasts prepared by professional economists. This “consensus forecast” anticipates the national economy will grow slowly over the next several years. Regarding the state economy, we assume employment does not recover to pre‑pandemic levels until at least 2025. We expect wages and salaries to recover more quickly, however, because high‑wage workers have experienced relatively few job losses. We also assume that housing markets, which have rebounded sharply from the early months of the pandemic, remain strong. Although these assumptions reflect our best assessment, they are subject to many uncertainties. Questions about the COVID‑19 pandemic—such as whether the spread of the virus worsens and to what extent vaccines or treatments become available—significantly increases these uncertainties compared with previous forecasts.

Modest Growth in the Guarantee Under Our Main Forecast. Under our main forecast, the minimum guarantee grows to $91.2 billion in 2024‑25, an increase of $7.3 billion compared with the 2020‑21 level (Figure 6). The average annual increase is $1.8 billion (2.1 percent). Test 1 is operative, with most of the increase attributable to our estimates of higher local property tax revenue. Our property tax estimates are driven primarily by projected growth in assessed property values ranging from 5.5 percent to 5.8 percent per year. These estimates reflect the recovery in home prices, sales, and construction activity over the past several months. They also account for reductions in some smaller property tax components. (In the box below, we explain how the recent passage of Proposition 19 could have a minor positive effect on our property tax estimates.) General Fund revenue, by contrast, accounts for a relatively small share of the increase in the guarantee because the state’s three largest taxes grow at an average annual rate of less than 1 percent.

Figure 6

Proposition 98 Funding Under LAO Main Forecast

(Dollars in Billions)

|

2020‑21 |

2021‑22 |

2022‑23 |

2023‑24 |

2024‑25 |

|

|

Inputs and Calculations |

|||||

|

Minimum Guaranteea |

|||||

|

General Fund |

$57.8 |

$57.3 |

$57.0 |

$57.7 |

$59.8 |

|

Local property tax |

26.2 |

27.3 |

28.6 |

30.0 |

31.5 |

|

Totals |

$84.0 |

$84.6 |

$85.6 |

$87.8 |

$91.2 |

|

Supplemental Payments |

— |

$2.3 |

$4.5 |

$5.3 |

$6.3 |

|

General Fund Tax Revenueb |

$152.2 |

$150.8 |

$150.0 |

$151.8 |

$157.1 |

|

Growth Rates |

|||||

|

K‑12 average daily attendance |

‑0.5% |

‑0.5% |

‑0.5% |

‑1.0% |

‑1.3% |

|

Per capita personal income (Test 2) |

3.7 |

‑1.7 |

3.4 |

4.6 |

4.3 |

|

Per capita General Fund (Test 3)c |

7.0 |

‑0.7 |

‑0.5 |

1.3 |

3.7 |

|

Outcomes With Supplemental Payments |

|||||

|

Total Proposition 98 Funding |

$84.0 |

$86.8 |

$90.1 |

$93.0 |

$97.5 |

|

Annual growth |

4.7 |

2.9 |

3.3 |

2.9 |

4.5 |

|

Percent |

5.9% |

3.4% |

3.8% |

3.2% |

4.8% |

|

Operative Test |

1 |

1 |

1 |

1 |

3 |

|

Proposition 98 Reserve |

|||||

|

Deposit (+) or withdrawal (‑) |

$1.5 |

$1.4 |

— |

‑$0.3 |

— |

|

Cumulative balance |

1.5 |

2.9 |

$2.9 |

2.6 |

$2.6 |

|

K‑14 Share of General Fund Tax Revenue |

38.0% |

39.5% |

41.0% |

41.5% |

42.0% |

|

Outcomes Without Supplemental Payments |

|||||

|

Total Proposition 98 Funding |

$84.0 |

$84.6 |

$85.6 |

$87.8 |

$91.2 |

|

Annual growth |

4.7 |

0.6 |

1.0 |

2.1 |

3.5 |

|

Percent |

5.9% |

0.7% |

1.2% |

2.5% |

3.9% |

|

Operative Test |

1 |

1 |

1 |

1 |

1 |

|

Proposition 98 Reserve |

|||||

|

Deposit (+) or withdrawal (‑) |

$1.5 |

$1.3 |

— |

‑$0.9 |

— |

|

Cumulative balance |

1.5 |

2.8 |

$2.8 |

1.9 |

$1.9 |

|

K‑14 Share of General Fund Tax Revenue |

38.0% |

38.0% |

38.0% |

38.0% |

38.0% |

|

aExcluding supplemental payments. bExcludes nontax revenue and transfers, which do not affect the calculation of the minimum guarantee. cAs set forth in the State Constitution, reflects change in per capita General Fund plus 0.5 percent. |

|||||

Property Tax Changes Under Proposition 19

Background on Property Tax Assessment. The taxable value of a residential property generally depends on its purchase price, adjusted for inflation by up to 2 percent per year. When a property changes ownership, its taxable value resets to its purchase price. These rules have a few exceptions. Eligible homeowners (generally consisting individuals who are over age 55 or severely disabled, or whose property has been damaged by a natural disaster) can move within the same county and keep paying the same amount of property taxes if their new home is less expensive than their old one. Some counties extend this policy to homeowners moving from other counties. Eligible homeowners can generally use this rule once in their lifetime. Another exception relates to inherited properties. It allows properties to pass from parents to children with no increases in taxes.

Changes Under Proposition 19. Proposition 19, recently approved by voters in the November election, expands the conditions under which eligible homeowners can sell their property and keep their lower tax bills. Specifically, the new rules allow these homeowners to (1) move anywhere in the state, (2) purchase more expensive homes (in these cases, homeowners would pay somewhat higher taxes), and (3) use these special rules up to three times in their lifetime. These new rules take effect on April 1, 2021. Proposition 19 also narrows the exception for inherited properties. Under the new rules, inherited properties can avoid reassessment only if the children receiving those properties use them as primary residences or for farming. In addition, the new rules provide for partial reassessment of inherited properties worth more than $1 million. These limitations take effect on February 16, 2021.

Minor Increases in Property Tax Revenue Likely. Expanding the exception that allows eligible homeowners to sell their properties and keep paying the same property tax bill will tend to reduce property tax revenue. On the other hand, narrowing the exception for inherited properties will tend to increase property tax revenue. Overall, the increases in property tax revenue are likely to outweigh the decreases. We estimate that schools and community colleges could gain tens of millions of dollars per year over the next few years. (Other local governments also will receive higher property tax revenue.) These gains are on top of the property tax growth projected in our outlook. Over time, these gains could grow to a few hundred million dollars per year. Regarding Proposition 98, these gains would function like existing school property tax revenue. Specifically, they would increase the minimum guarantee in Test 1 years and offset required General Fund spending in Test 2 and Test 3 years.

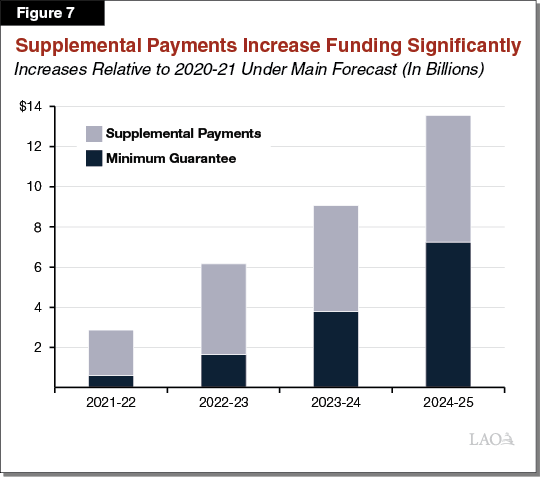

Notably Faster Growth With Supplemental Payment Included. By 2024‑25, the supplemental payments total $6.3 billion per year. Under our main forecast, overall Proposition 98 funding, including the supplemental payment, increases by $13.6 billion from 2020‑21 to 2024‑25 (Figure 7). The average annual increase is $3.4 billion (3.8 percent). As a share of the state budget, total General Fund spending on schools and community colleges grows from 38 percent to nearly 42 percent over the period.

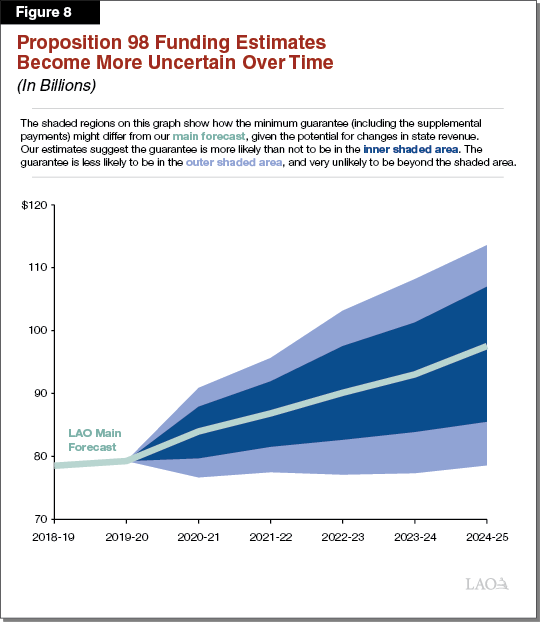

Uncertainty in Our Proposition 98 Estimates Increases Over Time. Over the coming years, the minimum guarantee will vary from the estimates reflected in our main forecast. The most uncertain input is General Fund revenue. To explore this uncertainty, we examined the extent to which revenues might end up above or below the estimates in our main forecast. For this analysis, we looked at how much revenue forecasts tended to differ from actual revenues over the last 50 years. We then used this historical relationship to determine the likely range of revenues over the next several years. Figure 8 displays our estimate of the guarantee (including the supplemental payment) under the various revenue ranges. The dark shaded area shows what the minimum guarantee would be under the revenue scenarios most likely to occur. The light shaded area would reflect notable departures from the assumptions in our main forecast. A major departure might be tied to a series of negative developments (such as delayed vaccine deployment, widespread business failures, or instability in rental housing markets) or series of positive developments (surge in consumer spending, smooth transition of unemployed workers back to their jobs, or major new federal fiscal stimulus). The estimates of the guarantee in the figure also assume growth in property tax revenue. This growth offsets much of the decline in the guarantee that otherwise would occur when General Fund revenue is significantly less than our main forecast. As the figure shows, the uncertainty in our estimates increases each year of the outlook period.

Reserves

Proposition 98 Reserve Balance Relatively Steady Under Main Forecast. Under our main forecast, the balance in the Proposition 98 Reserve remains relatively steady after 2021‑22. The formulas would require a small withdrawal in 2023‑24, but no other deposits or withdrawals during the outlook period. At the end of 2024‑25, the balance in the Proposition 98 Reserve is $2.6 billion. Reserve deposits likely would be somewhat higher if the guarantee were to grow faster and somewhat lower if the guarantee were to grow more slowly. Deposits also can be extremely sensitive to changes in capital gains revenue. Even if overall state revenues follow the trajectory in our main forecast, the required deposits or withdrawals could be higher or lower than our estimates. (We also assume the Legislature does not suspend or reduce any deposits otherwise required by the Constitution.)

Local Reserve Cap Would Remain Operative for a Few Years. As the minimum guarantee grows, the balance in the Proposition 98 Reserve decreases as a percentage of school funding. Under our main forecast, the balance would drop from nearly 4 percent in 2021‑22 to just below 3 percent in 2024‑25. As a result, the district reserve cap would be operative for three years beginning in 2022‑23.

Program Costs

Statutory COLA Projected to Remain Relatively Low. Our assumptions about the statutory COLA rate also reflect the consensus forecast. Compared with the historical average of 2.6 percent, the current consensus projections are relatively low. Specifically, the projected rates are 1.14 percent in 2021‑22, 1.36 percent in 2022‑23, 1.56 percent in 2023‑24, and 1.51 percent in 2024‑25. In practice, the rates can swing notably from year to year and sometimes diverge from broader trends in the economy. Over the previous four years, for example, the statutory COLA rate has varied from 0 percent to 3.26 percent despite relatively steady growth in the economy.

K‑12 Attendance Projected to Continue Declining. School attendance has been declining slowly since 2014‑15. We project this decline will continue over the outlook period and accelerate somewhat beginning in 2023‑24. Our estimates primarily reflect declining births in California—a trend that began more than a decade ago and accelerated somewhat in 2018. This reduction in births is due to a few factors, including the state having fewer adults of child‑rearing age. Regarding migration, we assume higher levels of net outmigration from the state in 2020 and 2021, driven primarily by the large drop in employment in spring 2020. In subsequent years, we assume a recovery in employment results in overall migration into and out of the state returning to lower and steadier levels.

Net Cost of COLA and Attendance Changes Around $900 Million Per Year. Under our main forecast, funding the statutory COLA for school and community college programs would cost roughly $1.2 billion per year over the outlook period. Declines in K‑12 attendance, by contrast, would reduce costs for most school programs by roughly $300 million per year. Accounting for both adjustments, the net increase in costs is roughly $900 million annually.

Key Considerations

Several Important Issues in the Year Ahead. In this part of the report, we highlight a few issues for the Legislature to consider as it begins planning for the upcoming budget cycle. Specifically, we (1) analyze the amount of new funding available for school and community college programs, (2) describe upcoming changes in district pension costs, and (3) comment on a few of the issues in our outlook.

Funding for New Commitments

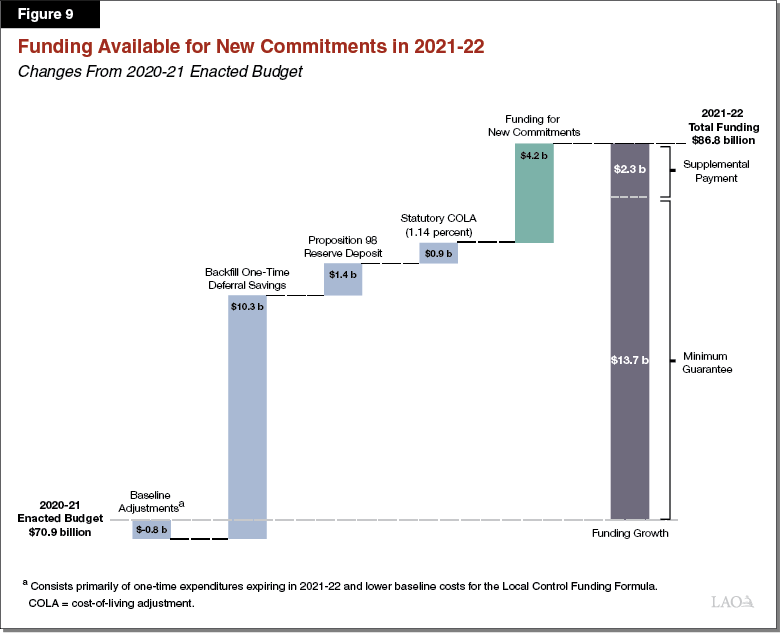

State Could Cover COLA and Make New Commitments in 2021‑22. Figure 9 shows our estimate of the changes in costs and funding relative to the 2020‑21 enacted budget level. The most notable adjustment relates to deferrals. The enacted budget obtained $10.3 billion in one‑time savings from the payment deferrals that began in 2020‑21. Although our outlook assumes those deferrals continue in 2021‑22, the state receives no savings because it is not shifting any additional payments. The $10.3 billion increase in Figure 9 reflects the cost of replacing the one‑time savings with ongoing funds in 2021‑22. (It does not reflect the additional one‑time costs the state would incur to eliminate the deferrals and restore the regular payment schedule.) We also estimate that covering the 1.14 percent statutory COLA would cost $870 million. After accounting for these cost increases, the required reserve deposit, and growth in funding, we estimate the Legislature has $4.2 billion available for new commitments in 2021‑22. Of this amount, $2.3 billion is attributable to the supplemental payment and $1.9 billion to growth in the minimum guarantee.

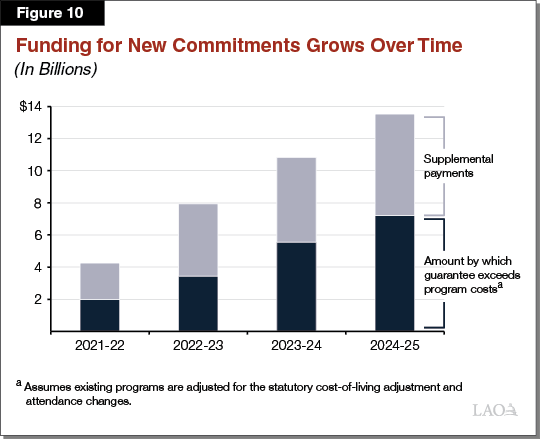

Funding for New Commitments Grows Over Outlook Period. Under our main forecast, the average annual COLA costs (roughly $900 million) are notably lower than the average annual increase in the minimum guarantee ($1.8 billion) and the annual increase including the supplemental payment ($3.4 billion). Due to these differences, the amount of funding available for new commitments grows over time (Figure 10). Focusing on the guarantee alone, the available funding grows to more than $7 billion by 2024‑25. Including the supplemental payment, the available funding grows to more than $13 billion.

District Pension Costs

Pension Costs Likely to Increase by a Few Hundred Million Dollars in 2021‑22. Rising pension costs have been a significant factor affecting district budgets over the past several years. Required district contributions to the California State Teachers’ Retirement System (CalSTRS) and the California Public Employees’ Retirement System (CalPERS) have grown from $3.5 billion in 2013‑14 to $8.4 billion in 2019‑20. (Nearly all school and community college employees are covered by one of these two pension systems.) To address rising costs, the state allocated more than $3 billion non‑Proposition 98 General Fund to provide temporary cost relief over the 2019‑20 through 2021‑22 period. Due to this relief, district pension costs are expected to be roughly flat from 2019‑20 to 2020‑21. In 2021‑22, district costs are likely to increase by at least $200 million. To the extent districts provide raises or hire additional staff, pension cost increases could be a couple hundred million dollars higher. (Salary and staffing decisions affect pension costs because the contribution rates are based on a percentage of district payroll.)

Much Larger Increase in Pension Costs Expected in 2022‑23. After the one‑time rate relief expires, district pension costs are expected to grow significantly. For 2022‑23, the underlying contribution rates currently are projected to grow more than 2 percent of pay for CalSTRS and nearly 4 percent of pay for CalPERS. Depending on district decisions about salaries and staffing, the associated cost increase is likely to range from $1.3 billion to $1.7 billion. A cost increase of this magnitude exceeds the additional funding districts are likely to receive from the statutory COLA that year.

LAO Comments

Greatly Improved Outlook for School and Community College Funding. Although the state economy remains below pre‑pandemic levels by many measures, the rebound in state revenues and the minimum guarantee is remarkable. Prior to 2020‑21, the largest increase in the guarantee relative to the enacted budget level occurred in 2014‑15, when the guarantee increased $6.3 billion (10.3 percent). The $13.1 billion (18.5 percent) increase in the 2020‑21 guarantee under our outlook would far surpass this record. Moreover, the revised 2020‑21 guarantee would represent an all‑time high on an inflation‑adjusted basis.

Legislature Could Pay Down All Existing Deferrals. One core decision facing the Legislature is how to allocate the $13.7 billion in available one‑time funds. This allotment is large enough for the state to reverse all existing payment deferrals (at a cost of $12.5 billion). We think this approach would have several advantages. Restoring the regular payment schedule would improve cash flow for schools and community colleges, reducing the need for internal or external borrowing. Paying down the deferrals also would remove pressure on future Proposition 98 funding, giving the Legislature more options to address economic downturns or fund other priorities moving forward. In addition, the state would re‑establish the link between ongoing program costs and ongoing funding. Since the deferrals are set to begin in February 2021, the Legislature would need to take early budget action if it wanted to rescind them in 2020‑21. (Alternatively, the Legislature could pay down the deferrals starting in 2021‑22.) If the Legislature does take early action, we would suggest a two‑pronged approach that pays down some deferrals immediately and the remainder contingent on state tax collections meeting expectations.

Rebound in Funding Warrants a Reassessment of the Supplemental Payments. According to the Governor’s May Revision, the supplemental payments were intended to accelerate growth in funding relative to the anticipated reductions in 2019‑20 and 2020‑21. Under our outlook, however, these reductions no longer occur. Rather than being $12.4 billion below the level needed to keep pace with the economy over those two years, the guarantee is $600 million above this level. Moreover, our main forecast suggests that in a relatively stable economic environment, growth in the guarantee would be enough to cover the statutory COLA as well as other augmentations. Based on these developments, we think the Legislature should reassess the supplemental payments after reviewing all of its budget priorities. In contrast to many other education funding decisions, the supplemental payments involve long‑term trade‑offs with other parts of the state budget. As we describe in The 2021‑22 Budget: California’s Fiscal Outlook, the state faces an operating deficit over the next several years, despite a significant windfall this year. To the extent the Legislature wants to provide funding on top of the guarantee, it has many options—such as providing a larger one‑time payment without committing to long‑term increases.

Dedicating Some 2021‑22 Funding to One‑Time Activities Would Build a Budget Cushion. Regardless of what the Legislature decides about supplemental payments, the state would have Proposition 98 funds available for additional commitments in 2021‑22. Although the state could allocate all of the 2021‑22 funding for ongoing programs, setting aside some portion for one‑time activities would provide a measure of protection against volatility in the minimum guarantee. To the extent the guarantee drops in the future, the expiration of one‑time initiatives allows the state to accommodate the lower guarantee without taking action to reduce funding, such as by cutting ongoing programs or deferring payments. When the state sets aside little one‑time funding, by contrast, budget balancing becomes more difficult. The 2019‑20 budget plan, for example, had a one‑time cushion of only $121 million. This small cushion is one reason the state had to rely heavily on other actions (mainly deferrals) when it adopted the 2020‑21 budget.

One‑Time Allocations Could Address a Range of Issues. Some reports suggest certain students have experienced significant learning loss since the closure of schools in March 2020. We think the Legislature might want to explore how one‑time funds could help districts provide additional support for these students. Prior to providing any funds, however, we encourage the Legislature to learn more about how districts spent their previous allotment of federal funding and whether other policy changes might be needed. (The 2020‑21 budget plan included more than $6 billion in one‑time federal funding for schools, the majority of which must be spent by December 30, 2020.) Regarding district budgets, the Legislature could make additional pension payments to pay down future cost increases. If the Legislature were to take this approach, we encourage it to structure these payments so they reduce costs on a long‑term basis beginning in 2022‑23, when contribution rates are scheduled to increase. The Legislature also could set aside additional funding to protect against economic downturns. For example, the Legislature could make additional deposits in the Proposition 98 Reserve or provide districts funding to build local reserves. If the Legislature were to pursue the local approach, it might need to modify the reserve cap.