LAO Contacts

- Jason Constantouros

- Medi-Cal

- Managed Care

- Family Health

- Health Care Affordability and Workforce Development

- Karina Hendren

- Medi-Cal

- Long-Term Care

- Developmental Services

- Ryan Miller

- Medi-Cal

- Behavioral Health

- Covered California

- CalHHS Agency Issues

- Will Owens

- Public Health

- Behavioral Health

- State Hospitals

February 14, 2024

The 2024‑25 Budget

Medi-Cal Analysis

- Introduction

- Overview

- Caseload

- MCO Tax Budget Solution

- MCO Tax‑Funded Provider Payment Increases

- Other Budget Solutions

Summary

Under Governor’s Budget, Budget Solutions Help Reduce General Fund Spending on Medi‑Cal. The Governor’s budget includes $35.9 billion General Fund spending in 2024‑25 on Medi‑Cal, the state’s Medicaid program. This amount reflects a $1.4 billion (3.8 percent) reduction from the previous‑year level. The net decline in General Fund spending primarily is driven by a series of proposed fund shifts, delays, and reductions to help address the state’s budget problem. Absent these proposals, spending in Medi‑Cal would grow by $1.3 billion in 2024‑25 under the Governor’s budget.

State’s Efforts to Limit Impacts of Continuous Coverage Unwinding Appear to Be Working. The Governor’s budget estimates that Medi‑Cal caseload will decline by about 1 million enrollees in 2024‑25 over the previous year—to 13.7 million. This decline reflects that the state and counties currently are redetermining eligibility for a historic high number of Medi‑Cal enrollees, as a result of the unwinding of a federal policy that resulted in rapid caseload growth since the start of the pandemic. The state has in place several federally approved flexibilities meant to maximize continuity of coverage for enrollees during this time. Based on our review of recently released data, the state’s efforts appear to be working. Specifically, caseload is coming in much higher than was previously assumed to be the case—both by the administration and our office. The Governor’s budget caseload estimates are broadly reflective of the recent data on continuous coverage unwinding and therefore are reasonable.

Proposed Managed Care Organization (MCO) Tax Budget Solution Is Worth Considering. As a budget solution, the Governor proposes to modify last year’s MCO tax package by (1) increasing the tax rate on Medi‑Cal enrollment and (2) shifting funds out of a reserve for planned augmentations in Medi‑Cal and other health programs. The administration states that the proposal, which would provide an additional $4.6 billion in General Fund savings through 2026‑27, would advance the timing of when the reserve is expected to be depleted. In light of the fiscal constraints facing the state in the near term, we recommend the Legislature consider approving the proposal after the administration shows that it stands a reasonable chance of receiving federal approval. That said, it also would be prudent to begin planning for the long‑term sustainability of the MCO package after the reserve is depleted.

There Are Many Issues to Weigh Around Proposed Provider Payment Increases. In response to direction from the Legislature in last year’s budget package, the Governor proposes a plan to increase Medi‑Cal payments for several kinds of services. The proposed plan also would make several changes to the way Medi‑Cal pays providers. In concept, several aspects of the proposed package could make Medi‑Cal’s provider payment system more rational, equitable, and efficient. That said, these impacts depend on many forthcoming details and there are risks and uncertainties associated with the package. We offer five key concepts for the Legislature to keep in mind as it weighs its own options to increase Medi‑Cal provider payments and learns more about the Governor’s proposal in the coming months.

Other Proposed Budget Solutions Are Reasonable but Additional Solutions Likely Needed. Outside of the MCO tax package, the Governor proposes $1.2 billion in budget solutions across 2023‑24 and 2024‑25. Given the substantial budget problem facing the state, these proposed solutions are warranted. Moreover, considering additional options now would be wise in light of the state’s deteriorating budget condition. For example, if voters approve Proposition 1 in March, we recommend the Legislature consider shifting the remaining $481 million General Fund for the Behavioral Health Continuum Infrastructure Program to bond funds.

Introduction

This brief analyzes the Governor’s proposals in the 2024‑25 budget for Medi‑Cal, California’s Medicaid program. It first provides an overview of Medi‑Cal and its proposed budget. It then provides our analyses of the administration’s (1) caseload estimates and projections, (2) other major current law adjustments, (3) proposed managed care organization (MCO) tax budget solution, (4) proposed MCO tax‑funded provider payment increases, and (5) other proposed budget solutions.

Overview

In this section, we provide key background on the Medi‑Cal program, describe Medi‑Cal’s overall budget picture, and summarize the key changes in General Fund spending in the current year (2023‑24) and budget year (2024‑25).

Background

Medi‑Cal Provides Health Coverage for Low‑Income Californians. Medi‑Cal, the state’s Medicaid program, provides health care coverage for low‑income Californians. Health care services covered by Medi‑Cal include visits to the doctor’s office, stays at the hospital, prescription drugs, behavioral health services, long‑term care, and dental services, among many other areas. The Governor’s budget assumes an average monthly Medi‑Cal caseload level of 14.8 million in 2023‑24, over one‑third of Californians.

Medi‑Cal Is a Sizable Portion of California’s Budget. More than half of Medi‑Cal’s budget is supported by federal funds, with the remainder supported by the General Fund and other state and local government sources. The General Fund portion of Medi‑Cal comprises a sizable share of overall state General Fund spending, ranging between 13 percent and 17 percent in most of the last ten years. As a share of General Fund spending, Medi‑Cal is the state budget’s second largest program (after Proposition 98 [1988], the California Constitution’s minimum spending requirement for K‑14 education).

Medi‑Cal Delivers Services in Many Ways. The primary way Medi‑Cal delivers services to beneficiaries is by contracting with health insurance plans, also known as managed care plans. The state provides managed care plans monthly payments to enroll Medi‑Cal beneficiaries, while the plans in turn are required to arrange for the health care of their enrollees. While most services are delivered in the managed care system, some are delivered in other ways. For example, Medi‑Cal pays for some health care services, such as pharmacy benefits, by reimbursing providers directly—known as the “fee‑for‑service” delivery system. County governments also play a key role in delivering certain services, particularly behavioral health care.

Overall Budget Picture

Overall Spending Is Up Over Enacted Level. As Figure 1 shows, the Governor’s budget estimates overall Medi‑Cal spending to be $157 billion in 2023‑24, up from $152 billion at budget enactment. Overall spending in 2024‑25 is projected to decline slightly from the revised 2023‑24 level.

Figure 1

Governor’s Budget Projects Growth in Overall Spending Over Enacted Level

Medi‑Cal Budget (Dollars in Billions)

|

2023‑24 |

2024‑25 |

Change From |

|||||

|

Enacted |

Revised |

Amount |

Percent |

||||

|

Total Spending |

$151.8 |

$157.5 |

$156.6 |

‑$0.9 |

‑0.5% |

||

|

By Fund Source |

|||||||

|

Federal funds |

$90.5 |

$95.8 |

$97.6 |

$1.8 |

1.9% |

||

|

General Fund |

37.5 |

37.3 |

35.9 |

‑1.4 |

‑3.8 |

||

|

Other funds |

23.8 |

24.4 |

23.2 |

‑1.2 |

‑5.1 |

||

|

By Program |

|||||||

|

Managed care |

$77.0 |

$79.6 |

$80.9 |

$1.3 |

1.7% |

||

|

Fee‑for‑service |

35.2 |

37.5 |

35.4 |

‑2.0 |

‑5.5 |

||

|

Other programs |

32.4 |

33.0 |

33.4 |

0.4 |

1.1 |

||

|

Local administration |

7.2 |

7.4 |

6.9 |

‑0.5 |

‑6.9 |

||

|

Note: Reflects local assistance spending in the Department of Health Care Services. Excludes state operations to administer Medi‑Cal, as well as state and local spending budgeted outside of the department used to claim federal Medicaid funds. |

|||||||

General Fund Spending in Medi‑Cal Is Down, With Proposed Budget Solutions a Key Reason. Among Medi‑Cal’s various sources of funding, the administration projects federal funding to increase but General Fund support to decrease. Specifically, General Fund spending under the Governor’s budget is revised slightly downward in 2023‑24 to $37.3 billion and then declines to $35.9 billion in 2024‑25. While many factors impact General Fund spending in the Governor’s budget (described further in the following sections), much of the decline is because the Governor proposes several budget solutions in Medi‑Cal. (There are proposed budget solutions in other programs as well. Our recent publication, The 2024‑25 Budget: Overview of the Governor’s Budget, provides more information on the overall package of proposed budget solutions.) While some of the budget solutions impact overall spending in Medi‑Cal, others reduce General Fund spending without necessarily impacting federal funding (such as by replacing General Fund spending with other fund sources).

Current‑Year General Fund Changes

General Fund Spending Down Due to Budget Solutions. As Figure 2 shows, the Governor’s budget estimates General Fund spending in 2023‑24 would be $1 billion higher than the enacted level, absent adopting budget solutions. The Governor’s budget solutions, some of which would begin in 2023‑24, more than offset these upward revisions. (Figure 4 summarizes the Governor’s proposed budget solutions.) The net result of these changes is a slight reduction in General Fund spending.

Figure 2

Current‑Year Spending Is Down Slightly

General Fund Changes in Medi‑Cal (In Billions)

|

Item |

Amount |

|

2023‑24 Enacted |

$37.5 |

|

Adjustments, Before Applying Budget Solutions |

|

|

Increased limited‑term spending |

$0.7 |

|

Higher caseload |

0.6 |

|

Other adjustments (net) |

‑0.3 |

|

Total Adjustments |

$1.0 |

|

Budget Solutions |

‑$1.2 |

|

Total Changes |

‑$0.2 |

|

2023‑24 Revised |

$37.3 |

Two Factors Largely Drive Increase in Spending Under Current Law. We estimate two key factors primarily drive the upward revision in spending under current law. First, the administration anticipates limited‑term spending to be higher in the current year than originally assumed in the 2023‑24 budget. Some of this increase is the result of higher costs associated with a one‑time retroactive repayment to the federal government. The timing of some one‑time spending also shifts from 2022‑23 to 2023‑24, further contributing to the upward revision. Second, the administration estimates caseload to be higher than assumed when the budget was enacted, resulting in increased General Fund spending.

Budget‑Year General Fund Changes

Budget Solutions Also Offset Growth in Budget Year. As Figure 3 shows, prior to accounting for proposed budget solutions, the Governor’s budget anticipates General Fund spending in Medi‑Cal to grow in 2024‑25. The growth is the net result of several factors. After including the proposed solutions, General Fund spending decreases in the budget year.

Figure 3

Spending Declines in Budget Year

General Fund Changes in Medi‑Cal (In Billions)

|

Item |

Amount |

|

2023‑24 Revised |

$37.3 |

|

Adjustments, Before Applying Budget Solutions |

|

|

Backfill of declines in other fund sourcesa |

$3.0 |

|

Per‑enrollee cost growth |

1.8 |

|

Full‑year impact of 26‑49 undocumented expansion |

1.6 |

|

Other (net)b |

‑0.1 |

|

Reduction in caseload |

‑1.8 |

|

Ramp down of limited‑term spending |

‑3.2 |

|

Total Adjustments |

$1.3 |

|

Budget Solutions |

‑$2.7 |

|

Total Changes |

‑$1.4 |

|

2024‑25 Proposed |

$35.9 |

|

aPrimarily consists of (1) reduction in General Fund offset in the MCO tax package, before applying the MCO tax budget solution; (2) the end of a one‑time boost in support in 2023‑34 from the Hospital Quality Assurance Fee; and (3) a projected reduction of Proposition 56 funds. bIn addition to various adjustments under current law, amount consists of two new proposals: (1) $6 million to reimburse counties for costs associated with an existing justice‑involved initiative and (2) $4.1 million for a new wellness coach benefit. |

|

|

MCO = managed care organization. |

|

Budget Solutions Increase in Budget Year. As Figure 4 shows, the largest proposed budget solution in Medi‑Cal involves the MCO tax. This budget solution first impacts General Fund spending in 2023‑24 and ramps up in 2024‑25. The Governor also proposes several other budget solutions in Medi‑Cal, most of which are one time and impact spending in 2024‑25.

Figure 4

Governor’s Budget Includes Several Budget Solutions in Medi‑Cal

General Fund Solutions (In Millions)

|

2023‑24 |

2024‑25 |

|

|

MCO Tax Budget Solutiona |

||

|

Shift in funds from provider payment reserve |

$625 |

$2,081 |

|

Increase in size of the tax |

395 |

698 |

|

Totals |

$1,020 |

$2,779 |

|

Other Budget Solutions |

||

|

Withdrawal of end of checkwrite hold |

— |

$533 |

|

Delay in behavioral health initiatives |

— |

375 |

|

Medi‑Cal Drug Rebate Fund reserve sweep |

$135 |

28 |

|

Reduction in supplemental physician payments |

— |

77 |

|

Reversion of clinic workforce stabilization payments |

15 |

— |

|

Totals |

$150 |

$1,013 |

|

Grand Totals |

$1,170 |

$3,792 |

|

aIn addition to amounts in this table, this budget solution also impacts General Fund spending in 2025‑26 and 2026‑27. The total impact from 2023‑24 through 2026‑27 is $4.6 billion. |

||

|

MCO = managed care organization. |

||

Caseload

In this section, we assess the administration’s estimates of Medi‑Cal caseload. We first provide context on (1) the federal continuous coverage requirement that lead to a substantial increase in caseload since the beginning of the pandemic and (2) the state’s strategy to limit the impact of the unwinding of that requirement on Medi‑Cal enrollees. We then assess the Governor’s budget estimates of caseload, which are considerably higher than previous projections produced by our office and the administration, and are consistent with continuous coverage unwinding apparently having a smaller impact on caseload than was previously assumed to be the case. While the Governor’s budget caseload estimates are reasonable, estimates based on updated caseload data will be available to incorporate into the budget after the May Revision.

Background

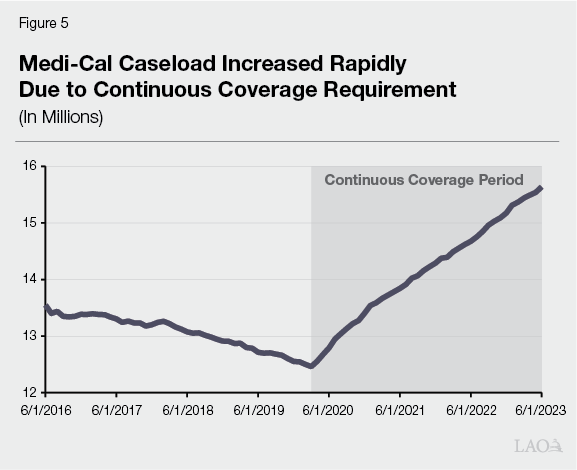

Federal COVID‑19 Policies Led to Substantial Increase in Caseload. In 2020, Congress approved a temporary increase in federal funding for most Medicaid costs. To be eligible for this increased federal funding, states were required to comply with several requirements on top of standard Medicaid rules, the most important being the continuous coverage requirement, which prohibited states from terminating eligibility for existing beneficiaries except in limited circumstances. Largely as a result of these policies, caseload and associated Medi‑Cal spending across all fund sources have increased substantially since the beginning of the pandemic. As shown in Figure 5, Medi‑Cal caseload increased by over three million (25 percent) between March 2020 and June 2023—roughly the effective term of the continuous coverage requirement.

Effect of Eligibility Redeterminations First Observed in July 2023 Caseload Data. Prior to continuous coverage, annual eligibility redeterminations for existing enrollees were staggered throughout the year. The continuous coverage requirement expired at the end of March 2023. The redetermination process for a given enrollee generally takes up to about three months. Thus, when counties resumed processing eligibility redeterminations on a monthly basis beginning April 1, 2023, it was for enrollees whose renewal month was June 2023. This means that the first individuals determined to be no longer eligible for Medi‑Cal lost coverage on July 1, 2023.

State Planned Extensively and Supplemented County Funding in Preparation for Redeterminations. For most of the pandemic, the precise end date of the continuous coverage requirement was unknown because the federal government acted several times to continue its enforcement. However, given the long duration of the requirement, DHCS and counties were able to plan for its eventual end. In May 2022, DHCS released the Medi‑Cal COVID‑19 Public Health Emergency Operational Unwinding Plan, which detailed how the state intended to resume normal eligibility operations. In addition, DHCS has communicated its plans through stakeholder engagement and direction to counties. That said, Medi‑Cal caseload is extraordinarily high relative to historical levels, making the unwinding of continuous coverage a huge administrative effort for counties. In recognition of this, the 2022‑23 budget supplemented county administration funding with $146 million ($73 million General Fund) over multiple fiscal years to support the increase in county workload to process eligibility determinations. (County administration funding is over $2 billion per year, with about 30 percent coming from the state General Fund.)

Several Waivers and Flexibilities Meant to Limit Disruption to Enrollees and Simplify Process for Counties and Enrollees. A stated goal of the administration during the unwinding of continuous coverage is to maximize continuity of coverage for those enrolled in Medi‑Cal. In addition, DHCS has sought to increase county capacity to process redeterminations in light of the extraordinary administrative task they face. To achieve these goals, the state has secured federal approval for a number of flexibilities. These flexibilities are detailed in the box below.

Flexibilities Intended to Minimize Impacts of Continuous Coverage Unwinding

In light of the massive task of continuous coverage unwinding, the state has received federal approval for several waivers intended to minimize disruption in health care coverage for enrollees and simplify processes for enrollees and counties. Generally, these flexibilities are in place at least through December 31, 2024, although the Department of Health Care Services has indicated its intent to extend some of them (to the extent allowable by the federal government). It is not fully clear at this time which flexibilities are likely to continue.

Increasing Use of an Automatic Renewal Process. The “ex‑parte” review process allows counties to automatically renew enrollees in Medi‑Cal in cases in which eligibility‑related information from federal and state sources allow for renewal without any contact with the beneficiary. Ex‑parte renewals are a key tool in increasing the overall number of county redeterminations per month. Flexibilities that increase ex‑parte renewals allow:

- Ex‑parte renewals in certain cases in which income under 100 percent of the federal poverty level was verified in the previous 12 months.

- Ex‑parte renewals for households with income generally derived from stable sources, such as Social Security or pensions.

- Expanded use of asset verification reports for ex‑parte renewals until the elimination of the asset test on January 1, 2024.

Reducing Documentation Requirements. The state has also received approval for flexibilities that reduce county workload and simplify processes for enrollees. Specifically:

- When self‑attested information cannot be verified with electronic data sources, a beneficiary can provide a reasonable explanation for the discrepancy in lieu of needing to provide documentation.

- Counties can assume no change in assets (and renew on an ex‑parte basis) when asset verification data returns no information within a reasonable time frame (20‑30 days depending upon the circumstance) rather than seek additional verification from the enrollee.

- Counties can use updated contact information provided by managed care plans, Program of All‑Inclusive Care for the Elderly (PACE) organizations, and the United States Postal Service in lieu of requiring confirmation by the beneficiary.

- Counties can extend a renewal date by 12 months when contact is made with certain hard‑to‑reach populations, including individuals experiencing homelessness, seniors, and persons with disabilities.

- The amount by which income reported by a beneficiary can deviate from that shown in federal data sources is increased from 10 percent to 20 percent.

- The requirement that applicants apply for certain types of available income (such as unemployment or veteran’s benefits) and medical support from a non‑custodial parent within 90 days of approval is waived.

Governor’s Budget Caseload Estimates

Modest Decline in 2023‑24 Followed by Decline of About 1 Million in 2024‑25, Reflecting Redeterminations. Figure 6 details the administration’s estimates of caseload built into the Governor’s budget. As shown in the figure, the administration estimates a 7 percent decline in overall caseload from 2023‑24 to 2024‑25, reflecting the result of redeterminations. The caseload decline is almost exclusively concentrated in the ACA optional expansion (largely childless adults) and families and children categories. This concentration is unsurprising, given that 94 percent of the cumulative increase in caseload during the continuous coverage period (March 2020 through June 2023) was in the ACA optional expansion (53 percentage points) and families and children (41 percentage points) categories.

Figure 6

Governor’s Budget Estimates of Medi‑Cal Caseload

Average Monthly Enrollment

|

2022‑23 |

2023‑24 |

2024‑25 |

Change From 2023‑24 |

||

|

Number |

Percent |

||||

|

Families and Children |

7,835,000 |

7,492,000 |

6,950,100 |

‑541,900 |

‑7% |

|

ACA Optional Expansion |

5,085,400 |

4,925,300 |

4,493,100 |

‑432,200 |

‑9 |

|

Seniors |

1,203,200 |

1,218,900 |

1,209,900 |

‑9,000 |

‑1 |

|

Persons With Disabilities |

1,087,100 |

1,062,900 |

1,044,200 |

‑18,700 |

‑2 |

|

Other |

63,300 |

64,700 |

64,100 |

‑600 |

‑1 |

|

Totals |

15,274,000 |

14,763,800 |

13,761,400 |

‑1,002,400 |

‑7% |

|

ACA = Patient Protection and Affordable Care Act. |

|||||

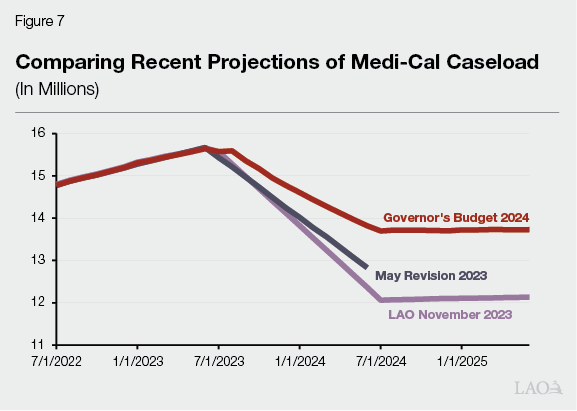

Comparison to Recent Administration and LAO Projections. Figure 7 compares caseload estimates incorporated into the Governor’s budget (estimated as of November 2023) with the most recent projections from our office (estimated as of November 2023) and the administration at May Revision (estimated as of April 2023). As shown in the figure, the Governor’s budget reflects a significant upward revision to caseload compared with the administration’s 2023 May Revision estimates. Specifically, the administration now projects caseload will decline to 13.8 million at the end of 2023‑24, about 1 million enrollees higher than for the same month as of the 2023 May Revision. The Governor’s budget also reflects substantially higher caseload than our office projected in our November Fiscal Outlook report. The administration now projects caseload to bottom out at around 13.7 million at the start of 2024‑25, about 1.6 million (12 percent) more enrollees than our projected low point in caseload. We estimate that this higher caseload results in increased General Fund costs of more than $2 billion in 2024‑25 relative to our estimates.

Assessment

LAO and Administration November Estimates Completed When Limited Data on Redeterminations Were Available. Statute requires DHCS to submit the Medi‑Cal Estimate (which includes caseload estimates for the upcoming budget year) to the Department of Finance by November 1 (for preparation of the Governor’s budget). This is around the same time our office typically finalizes Medi‑Cal caseload projections for our Fiscal Outlook report. At this time, enrollment data were only available through July 2023, reflecting only one month of redeterminations. In addition to enrollment data, DHCS has published a monthly dashboard and posted its monthly reports to the Centers for Medicare and Medicaid Services (CMS) that detail initial redeterminations data. The administration indicates that they were able to factor these early redetermination results into their Governor’s budget caseload projections. Our estimates, on the other hand, were based upon projections of caseload given economic and demographic factors rather than incorporating early redeterminations data, which were of limited use for projecting caseload principally because of the large number of redeterminations still shown as pending.

Wide Gap Between Projections Illustrates Extent of Uncertainty of Continuous Coverage Unwinding. Historically, most categories of Medi‑Cal caseload have tended to follow long‑term trends, meaning they can typically be projected in the near term within a relatively small margin of error. (Exceptions to this have occurred historically, such as with uncertainty surrounding the ACA optional expansion.) In the years immediately preceding the pandemic, our office and the administration had differing assessments of caseload from time to time, but generally those differences—and the resulting impacts on the budget—were relatively minor. The wide gap between recent projections truly is a notable occurrence. That said, it is illustrative of the extraordinary circumstance in which the state finds itself after three years of continuous coverage.

A Clearer Picture of Redeterminations Is Now Emerging. Since our office and the administration each produced our most recent projections of Medi‑Cal caseload, DHCS has released additional months of initial redeterminations data and updates to the June 2023 through August 2023 reports that reveal the outcome of most previously pending redeterminations. These recently released data show enrollees being retained in the program at a higher rate than was the case in previous reports. In addition, we now have caseload data through January 2024. While near‑term caseload is still subject to an unusual degree of uncertainty, these updated data now provide a clearer picture of what caseload will look like through the end of 2024‑25.

About Three‑Quarters of Redeterminations Have Resulted in Renewals. Through December, about three‑quarters of processed redeterminations have resulted in renewals. Assuming that trends observed in recent data continue, we project that the share of enrollees renewed in the program would exceed 80 percent. As of late‑January 2024, only five states and the District of Columbia have renewal rates exceeding 80 percent, based on national redeterminations data compiled by KFF.

Administration Caseload Estimates Reasonable, but Full Caseload Impact of Continuous Coverage Unwinding Still Uncertain. Based on information available to us through late January, the Governor’s budget caseload estimates are reasonable. Our assessment is predicated on a key assumption—that the increased rates of enrollee renewals shown in recently released data continue. If this assumption does not come to pass, caseload could wind up lower than under the Governor’s budget estimates, resulting in General Fund savings. While we now have a clearer picture of caseload through 2024‑25 than our office or the administration had last fall, waiting to approve any change to the Medi‑Cal budget until after release of the May Revision would be prudent, as the picture will become even clearer by then. We will make our final assessment and recommendations based on the administration’s revised estimates at that time.

Administration’s Caseload Estimates Possibly an Indication of Positive Impact of Flexibilities… As described earlier, our November Fiscal Outlook projections of Medi‑Cal caseload were based upon our office’s projections of economic and demographic factors. In general, we estimated what Medi‑Cal caseload would have been absent the continuous coverage requirement and brought caseload down to that level over the unwinding period. We did not factor in early months of preliminary data on redeterminations, nor did we make explicit assumptions about the extent to which the state’s several federally approved flexibilities would impact caseload. The Governor’s budget projects that caseload will bottom out around 1.6 million enrollees higher than we projected in November 2023. This appears to be an indication that the state’s efforts to maximize the continuity of coverage for Medi‑Cal enrollees are working. Another indication of the success of these efforts is the state’s performance relative to other states.

...But What Happens to Enrollees If Flexibilities Expire? In December 2023, CMS announced that it will extend flexibilities past the end of continuous coverage unwinding through at least the end of 2024. DHCS has communicated its intent to continue some of the eligibility flexibilities (to the extent permitted by the federal government) while letting others expire. Depending upon future federal and state actions, the state’s recent success in minimizing the impact of continuous coverage unwinding on enrollees may only be temporary. The extent to which the state’s efforts continue to be successful or, alternatively, caseload begins to return to more normal levels over the next few years, will be an important issue to watch.

MCO Tax Budget Solution

In this section, we analyze the Governor’s proposed MCO tax budget solution. We first provide background on the MCO tax and last year’s MCO tax package. Next, we describe the Governor’s proposed budget solution. We then conclude with our assessment and recommendations.

Background

MCO Tax Provides Net Fiscal Benefit to State, While Imposing Minimal Cost to Health Insurance Plans. The MCO tax is a tax on health insurance enrollment in the Medi‑Cal program and in the commercial sector. Though MCOs (organizations that offer health insurance plans to consumers) pay the tax, they bear very little of the tax’s cost. Instead, most of the cost of the tax is covered by the Medi‑Cal program, using a portion of MCO tax proceeds and federal funds. Because federal funds help cover the cost of the tax, the tax still provides the state a net fiscal benefit. The state must receive approval from the federal government to use the tax to draw down federal funds.

Last Year’s Budget Package Enacted New, Much Larger MCO Tax. The Legislature has not permanently authorized the MCO tax. Instead, it has authorized and renewed it for limited periods of time. Most recently, the Legislature enacted Chapter 13 of 2023 (AB 119, Committee on Budget), establishing a new version of the MCO tax from April 2023 through December 2026. The tax is structured similarly to the version preceding it, with one key difference—the tax rate on Medi‑Cal enrollment is more than triple that of the previous version. As a result, the new tax is expected to generate $19.4 billion in net fiscal benefit over its term, which is several billion dollars more than past versions. (Our past post, The 2023‑24 California Spending Plan: Health, provides more detail on the enacted MCO tax package.)

New Tax Is to Offset General Fund Spending in Medi‑Cal and Support Health Program Augmentations. As Figure 8 shows, the 2023‑24 budget designated two key uses for the new MCO tax’s net fiscal benefit. The first purpose is to offset General Fund spending in the existing Medi‑Cal program. The second purpose is to support augmentations in Medi‑Cal and other health programs. Funds for this second purpose are deposited into a new special fund called the Medi‑Cal Provider Payment Reserve Fund. Some augmentations were enacted by the Legislature as part of the 2023‑24 budget, comprising a small portion of available funding in the reserve. Last year’s health trailer bill (Chapter 42 of 2023 [AB 118, Committee on Budget]) directed the administration to propose a plan for the remaining funds as part of the 2024‑25 budget process. (We describe the Governor’s proposed augmentations further in the “MCO Tax‑Funded Provider Payment Increases” section that follows.)

Figure 8

There Are Two Key Intended Uses of the MCO Tax

MCO Tax Package Enacted in 2023‑24 Budget (In Millions)

|

2023‑24 |

2024‑25 |

2025‑26 |

2026‑27 |

Totals |

|

|

Net State Fiscal Benefit |

|||||

|

Total revenue |

$8,269 |

$8,527 |

$8,762 |

$6,704 |

$32,261 |

|

Portion of tax on Medi‑Cal enrollment covered by statea |

‑3,860 |

‑3,415 |

‑3,507 |

‑2,077 |

‑12,860 |

|

Totals |

$4,410 |

$5,112 |

$5,254 |

$4,626 |

$19,402 |

|

Uses of Net State Fiscal Benefit |

|||||

|

Offset of General Fund spending in Medi‑Cal |

$3,389 |

$1,858 |

$2,019 |

$1,050 |

$8,316 |

|

Reserve for augmentations |

1,021 |

3,254 |

3,235 |

3,576 |

11,086 |

|

Totals |

$4,410 |

$5,112 |

$5,254 |

$4,626 |

$19,402 |

|

aRemaining portion of tax on Medi‑Cal enrollment will be covered by federal funding. |

|||||

|

MCO = managed care organization. |

|||||

Package Anticipated Funding Shortfall in Future, After Reserve Funds Are Fully Spent. At the time the Legislature enacted the new version of the MCO tax, DHCS staff emphasized the next version following this one likely would not be as large. This is because DHCS reported that federal administrators, in private discussions with the department, signaled intent to change the rules around approving taxes like the MCO tax in the future. Recognizing this risk, last year’s package anticipated some funds in the Medi‑Cal Provider Payment Reserve Fund would be held in reserve and be available, along with funds from a much smaller future MCO tax, to sustain the augmentations after the end of the term of this tax. The administration stated at the time that the reserve would be fully spent around the end of 2029. Absent the Legislature modifying the augmentations or identifying another fund source, the shortfall would fall on the General Fund to backfill.

Federal Government Recently Approved Enacted Tax… Very shortly after budget enactment, DHCS submitted a new MCO tax‑related waiver to the federal government for approval. In December 2023, the federal government announced its approval of this waiver, enabling the MCO tax to into effect under California law and for the tax to draw down federal Medicaid funds under federal law.

…But Also Signaled Intent to Change Rules to Approve Tax in the Future. As part of its approval letter, the federal government noted its concern that the MCO tax, while technically meeting current federal rules, falls disproportionately on Medi‑Cal services. That is, the tax derives 99 percent of its revenue from Medi‑Cal enrollment, even though Medi‑Cal comprises around 50 percent of taxable enrollment. This is of concern to the federal government because nearly all of the cost of the tax falls on the Medi‑Cal program—which is partly supported by federal funds—rather than more proportionately between Medi‑Cal and private insurance. To address this concern, the letter states intent to change the rules around approving the MCO tax. The letter does not specify the scope of the rule changes or the timeline to enact them.

Proposals

Proposes MCO Tax Budget Solution to Increase General Fund Offset. As part of the Governor’s package of proposed budget solutions intended to address the state’s budget problem, the Governor proposes to modify the recently enacted MCO tax package. The proposal, which would increase the General Fund offset by $4.6 billion from 2023‑24 through 2026‑27, is the result of two key actions, described further below.

Increases Size of MCO Tax. The administration proposes early action trailer bill legislation to increase the MCO tax rate on Medi‑Cal enrollment. As Figure 9 shows, the increase would be effective January 2024, assuming it receives federal approval. The tax rate on commercial enrollment would remain unchanged from the enacted levels. With an increase in the rate on Medi‑Cal enrollment, the MCO tax would yield more revenue and a larger net fiscal benefit ($1.5 billion over the multiyear).

Figure 9

Proposal Would Increase Rate on Medi‑Cal Enrollment in Most Years

MCO Tax Rate on Medi‑Cal Enrollmenta

|

2023a |

2024 |

2025 |

2026 |

|

|

Enacted in 2023‑24 budget |

$182.50 |

$182.50 |

$187.50 |

$192.50 |

|

Proposed in 2024‑25 Governor’s Budget |

182.50 |

205.00 |

205.00 |

205.00 |

|

Percent increase |

— |

12% |

9% |

6% |

|

aRate applies to each plan’s aggregate monthly enrollment level between 1,250,001 and 4,000,000 member months during calendar year 2022, with certain adjustments. The tax rate on commercial enrollment, which ranges between $1.75 and $2.25 depending on the year, remains at the enacted levels in the Governor’s budget. bRate applies from April through December 2023. |

||||

|

MCO = managed care organization. |

||||

Reduces Overall Funding in Provider Payment Reserve. The administration proposes to deposit less funding in the Medi‑Cal Provider Payment Reserve Fund than originally planned, freeing up more MCO tax funds to further offset General Fund spending in Medi‑Cal ($3.1 billion over the multiyear). According to the administration, the change would not reduce annual spending levels for Medi‑Cal augmentations, but instead would shift the timing of when the reserve funds would be fully spent. Specifically, the administration indicates that the reserve would be fully spent at around mid‑2028, rather than at the end of 2029 as originally anticipated in the 2023‑24 budget.

Leaves Small Reserve by the End of the Term of the Tax. Accounting for the proposed budget solution, the administration has submitted a multiyear spending plan for the MCO tax package. As Figure 10 shows, under the plan, the annual offset to General Fund spending would begin to decline in 2025‑26, as the cost of the proposed augmentations ramp up. When the tax ends in 2026‑27, the state would have $841 million of MCO tax funds left in reserve. This reserve would be available to help sustain—but not fully cover—the augmentations in the MCO tax package in 2027‑28 (potentially shifting up to the low billions of dollars of cost pressure to the General Fund). By contrast, without the proposed fund shift, the reserve would be around $4 billion in 2026‑27, enough to cover the augmentations over a somewhat longer period of time. (The reserve would be even larger in 2026‑27 were the state to renew the MCO tax in 2027, with the amount of funds depending on the size of the future version of the tax.)

Figure 10

Multiyear Plan Leaves Small Reserve to Help Sustain Proposed Augmentations

Revised MCO Tax Package Proposed in the Governor’s Budget (In Millions)

|

2023‑24 |

2024‑25 |

2025‑26 |

2026‑27 |

Totals |

|

|

Net Fiscal Benefit |

$4,805 |

$5,810 |

$5,721 |

$4,524 |

$20,859 |

|

Uses of Net Fiscal Benefit |

|||||

|

Offset to General Fund spending in Medi‑Cal |

$4,409 |

$4,637 |

$2,485 |

$1,349 |

$12,880 |

|

Augmentations |

|||||

|

Medi‑Cal provider payment increases |

$121 |

$1,065 |

$2,267 |

$2,399 |

$5,852 |

|

Other augmentations |

275 |

105 |

450 |

450 |

1,280 |

|

State administrative costs |

— |

2 |

2 |

2 |

7 |

|

Totals |

$4,805 |

$5,809 |

$5,205 |

$4,200 |

$20,019 |

|

Remaining Funds at the End of the Year |

— |

$1 |

$516 |

$324 |

$841 |

|

MCO = managed care organization. |

|||||

Assessment

In Concept, Tax Increase Worth Considering. As we emphasized in The 2023‑24 Budget: Analysis of the Medi‑Cal Budget, enacting an MCO tax makes budgetary sense. The tax is a key source of support for the Medi‑Cal program while imposing a minimal cost on the health insurance industry. Following this same logic, it also makes sense for the state to maximize the benefit it can achieve from the tax. Moreover, increasing the size of the MCO tax is a particularly attractive budget solution relative to other options as it does not necessitate scaling back core programs or imposing substantial new costs to California taxpayers. In considering the proposed increase, the Legislature will want to ensure the revised tax still complies with federal rules and therefore stands a reasonable chance of receiving federal approval.

Reducing Provider Payment Reserve Also Worth Considering, Though Fiscal Risks Remain. The Governor’s proposed reduction to the provider payment reserve would help address the state’s budget problem over the next few years, but also accelerate when the potential MCO tax funding shortfall occurs by around one year. The best available data strongly suggest the state is facing a notable budget problem now and likely faces budget deficits over the next few years. The state’s fiscal situation in the longer term, when the shortfall is expected, is less certain. Because of the likely fiscal constraints in the near term, tapping into the reserve to help address the immediate situation is reasonable. That said, it also would be prudent for the Legislature to begin planning for the long‑term sustainability of the MCO tax package. Were the General Fund to have limited capacity when the MCO tax shortfall begins, the Legislature could face pressure at that time to pull back some of the package’s augmentations or to sustain them by identifying reductions elsewhere.

Recommendation

Consider Proposed Budget Solution as a Starting Point. Given the fiscal challenges in the state budget, we recommend the Legislature consider adopting the proposed MCO tax budget solution. The Legislature likely will want to condition such action on the administration demonstrating that the proposed tax increase stands a reasonable chance of receiving federal approval. To the extent the Legislature does not adopt some or all of the proposal, it will need to identify a like amount of budget solutions in other areas of the budget. Alternatively, the Legislature could consider using even more MCO tax funding to address the budget problem, potentially avoiding reductions in other areas. The Legislature likely would want to weigh such an action against its interest in increasing provider payments in Medi‑Cal, further described in the next section.

MCO Tax‑Funded Provider Payment Increases

In this section, we analyze the Governor’s proposed provider payment increases in the MCO tax package. We first provide background on the existing way Medi‑Cal pays providers in the fee‑for‑service and managed care systems, as well as the provider payment increases enacted in last year’s budget. Next, we describe the proposed package of payment increases. We then provide our initial assessment and recommendations.

Background

Provider Payments in Fee‑for‑Service System

In Fee‑for‑Service, Medi‑Cal Pays Providers Directly. Under the fee‑for‑service system, DHCS oversees a network of providers across the state, approves the delivery of certain services, and—critically—directly pays providers. While it is Medi‑Cal’s traditional delivery system, over time the state has shifted most beneficiaries out of fee‑for‑service. Around 5 percent of Medi‑Cal’s enrollment, as well as 23 percent of program spending, is projected to be in the fee‑for‑service system in 2024‑25.

Medi‑Cal Takes Several Approaches to Pay for Services. While fee‑for‑service often is described as a single delivery system, there is not one approach to pay providers. Rather, as Figure 11 shows, payment approaches vary, depending on the service. For example, physician and professional services are paid based on the procedure provided. Medi‑Cal contains thousands of codes for each kind of procedure, with different rates tied to each code. For other services, such as inpatient services at University of California (UC) and county hospitals and long‑term care services, providers are paid based on their reported costs to provide care to patients. Still in other cases, Medi‑Cal uses a prospective payment system, in which payment is provided for an episode of care. As an example, private and district hospitals are paid for each inpatient stay, with the rate depending on the patient’s diagnosis and acuity. The payment generally does not change depending on the patient’s length of stay or utilization of services. Thus, in this system, hospitals bear the risk of costs being higher or lower than expected.

Figure 11

Several Approaches Exist to Pay Providers

Summary of Key Base Provider Payment Approaches in Medi‑Cal Fee‑for‑Service

|

Service |

How Rates Are Set |

How Rates Are Adjusted |

|

Physician and professional services |

Set rate for each procedure. |

Generally not adjusted. |

|

Hospital outpatient services |

Set rate for each procedure. |

Generally not adjusted. |

|

Inpatient services at UC and county hospitals |

Cost‑based reimbursement. |

Adjusted based on changes in cost. |

|

Inpatient services at private and district hospitals |

Global payment for each stay, based on patient diagnosis and acuity. |

Set to maintain overall spending at around $3.2 billion total funds each year. |

|

Services at federally qualified health centers |

Rate for each visit, with rates tied to the average cost of care. |

Adjusted using the Medicare Economic Index, a measure of medical cost inflation. |

|

Long‑term care |

Projected cost of care, including state mandated services. |

Generally adjusted based on projected changes in cost. |

|

Pharmacy |

Cost to acquire drug and rate for dispensing drug. |

Generally adjusted based on changes in drug acquisition costs. |

Some Rates Are Adjusted Over Time, but Others Generally Have Remained Unchanged. Medi‑Cal takes different approaches to adjust fee‑for‑service rates for providers. For example, cost‑based payments are adjusted over time based on changes in actual or projected costs. By contrast, payments for physician and professional services tend to not be adjusted over time. Instead, these rates usually are set initially at 80 percent of the comparable rate paid by Medicare, a federal program that covers health care for the elderly and disabled. The rates then remain at their initially enacted levels, unless the Legislature explicitly provides funding for a rate increase.

Many Providers Receive Supplemental Payments. Over the years, the state has established supplemental payments in Medi‑Cal for certain providers. Sometimes these payments add to the base rate and therefore are allocated based on the relevant base payment methodology (such as utilization or reported costs.) In other cases, the approach is tied to other criteria. For example, some supplemental payments are tied to meeting certain performance outcomes, delivering high‑value services, or serving disproportionate numbers of Medi‑Cal or uninsured patients.

Medi‑Cal Uses Different Fund Sources to Support Base and Supplemental Payments. The cost of fee‑for‑service payments generally is shared by federal funds and state and local government sources. For most services, the federal share of cost is 50 percent, but can be higher in some cases (for example, 90 percent for family planning services) and lower in other cases (for example, federal funds generally are not provided for abortion services). The state tends to use different sources to cover the nonfederal share of cost, described below:

- Base Payments. The General Fund covers the nonfederal share of cost of base fee‑for‑service payments, with some exceptions. In particular, UC and county hospitals, which are considered government agencies under Medi‑Cal rules, use their own local funds to cover the nonfederal share of cost. That is, Medi‑Cal only pays for the federal share of cost for these providers.

- Supplemental Payments. The state tends to use non‑General Fund sources to support supplemental payments. For example, Proposition 56 (2016), which increased taxes on tobacco products, supports supplemental payments to physicians, family planning providers, and several other providers. Quality assurance fees charged to private health care providers also are used to draw down federal funds for supplemental payments. Moreover, some public providers use their local funds to draw down supplemental federal funding.

Provider Payments in Managed Care

Managed Care Is Medi‑Cal’s Primary Delivery System. In the managed care system, the state contracts with MCOs to enroll Medi‑Cal beneficiaries in health plans. The plans are responsible for arranging for the care of beneficiaries, primarily using their networks of providers. Managed care plans are responsible for providing most of the same services as in the fee‑for‑service system, with some exceptions. Managed care is now Medi‑Cal’s primary delivery system, projected to serve 95 percent of beneficiaries in 2024‑25.

State Pays Managed Care Plans, Which in Turn Pay Providers for Services. Critically, Medi‑Cal does not directly pay health care providers in the managed care system. Instead, Medi‑Cal pays the managed care plans on a monthly basis for each enrollee and plans in turn use the resulting funds to pay providers in their networks. The federal government annually approves the methodology to pay managed care plans.

Managed Care Plans Have Different Ways of Paying Providers. Historically, the state has not mandated how managed care plans are to pay for most services. Rather, the plans are responsible for negotiating payments as part of their contracts with providers, including the payment methodology and how much to pay. These arrangements are confidential and therefore comprehensive information is not available. Many managed care plans have told our office that at least some of their provider payments are set at 100 percent or more of the relevant Medi‑Cal fee‑for‑service rate. Managed care plans also attest to having many other kinds of arrangements. For example, some managed care plans subcontract with other plans or provider groups to oversee the care of some of their enrollees. In these arrangements, the plans provide monthly per‑enrollee payments, much like how Medi‑Cal pays the plans.

State Also Can Provide Directed Payments. Federal rules allow states to provide what are known as “directed payments” in the managed care system. Most commonly, directed payments work like supplemental payments, with the state providing additional funds to plans to be directed toward specific providers and services. In fact, many fee‑for‑service supplemental payment programs, such as those supported by Proposition 56 funds, also support managed care directed payment programs. States also can establish minimum fee schedules for managed care plans to pay for services. For example, California law currently requires plans to pay for long‑term care and certain transplant services at the Medi‑Cal fee‑for‑service rate.

Different Fund Sources Also Support Payments to Managed Care Plans. Like fee‑for‑service payments, the cost of payments to managed care plans is covered by federal funds and other sources. For base payments, the state generally covers the nonfederal share of cost using General Fund. Much like fee‑for‑service supplemental payments, the nonfederal share of cost for supplemental directed payments tends to be covered by other sources, such as Proposition 56 funds, quality assurance fee revenue, and local government contributions.

Provider Payments in Recent MCO Tax Package

MCO Tax Package Included Plan to Increase Provider Payments. As part of the recently enacted MCO tax package (described further in the “MCO Tax Budget Solution” section of this report), the Legislature established a plan to spend the resulting funds in trailer bill legislation (Chapter 42 of 2023 [AB 118, Committee on Budget]). Under the plan, a sizable portion of funds are designated to support augmentations to Medi‑Cal and other health programs. Below, we describe the major Medi‑Cal augmentations.

A Provider Payment Increase for Specified Services Was Enacted in the 2023‑24 Budget. Under the trailer legislation, the MCO tax package supports a provider payment increase, effective January 2024. The increase, currently estimated to cost $291 million MCO tax funds annually, specifically sets Medi‑Cal fee‑for‑service rates for primary care, maternity care, and non‑specialty mental health services at least at 87.5 percent of the comparable rate in Medicare. The legislation also requires managed care plans to pay at this level for these services. In the box below, we describe how DHCS has implemented the new policy. (In addition to increasing Medi‑Cal provider payments, the legislation enacted two other MCO tax‑funded augmentations—$75 million ongoing for graduate medical education programs at UC and $200 million one time in 2023‑24 for hospital relief programs at the Department of Health Care Access and Information.)

Implementation Update on 2024 Provider Payment Increases

Department Recently Released Fee‑for‑Service Rate Schedule. On December 1, 2023, the Department of Health Care Services (DHCS) published new fee‑for‑service rates for codes related to primary care, obstetric care, and non‑specialty mental health care. DHCS set these rates at 87.5 percent of what Medicare pays, as required under state law. To set these rates, DHCS included both existing base rates and Proposition 56‑supported supplemental rates. The rates also were set at the lowest regional Medicare rate. (Medicare varies its rates for California among 32 localities, intended to reflect differences in regional cost.) As an exception, DHCS did not adjust rates (after accounting for Proposition 56 funds) that already exceeded the Medicare benchmark.

Managed Care Plans Have Longer Time Line to Adopt Payment Increases. State law also requires managed care plans to pay at least the same as the fee‑for‑service rates for these services. Implementing these rate increases will not be a simple task for many plans, as they will have to update their payment systems and provider contracts. Accordingly, DHCS has signaled that plans will have several months to comply with the new requirements. Specifically, plans with fee‑for‑service payment arrangements with providers will not be required to implement the rate increases on a go‑forward basis until July 31, 2024. However, plans also will be required to make retroactive payments from January through July 2024, with those payments due by the end of October 2024. For plans that make contracted monthly payments to other plans and providers, plans must attest to DHCS that their payments align with the new policy by the end of December 2024. DHCS indicates that it will provide more guidance to plans on how to implement the provider rate increases in these arrangements at a future date.

Legislature Tasked Administration With Developing Plan for Remaining Increases. The trailer bill legislation did not set forth what augmentations would be supported from the remaining MCO tax funds. Rather, the legislation directed the administration to propose which augmentations to support as part of the 2024‑25 budget process. The legislation stated intent that the proposal advance access, quality, and equity for Medi‑Cal beneficiaries and promote provider participation in the Medi‑Cal program. The legislation also specified which areas should be increased. As Figure 12 shows, these areas cut across several parts of Medi‑Cal and health programs.

Figure 12

Legislature Specified Several Areas for Augmentations

Areas Specified in Chapter 42 of 2023 (AB 118, Committee on Budget)a

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

aAbridged by Legislative Analyst’s Office. |

Administration Released Initial Allocation Plan After Budget Enactment, With More Details to Be Released in 2024. Shortly after budget enactment in June 2023, DHCS submitted a summary plan of how it proposed to allocate MCO tax funds annually toward each area. The summary, which totaled $2.7 billion in annual spending from MCO tax funds, identified allocations for augmentations enacted in 2023‑24 and proposed augmentations in 2024‑25. Pursuant to the direction in the trailer bill legislation, the administration planned to release more information on the 2024‑25 augmentations as part of the Governor’s budget in January.

Proposal

Proposes Increases to Payments and Changes to Payment Methodologies. On January 19, 2024, DHCS released a policy brief describing a plan for most of the $2.7 billion package in annual augmentations. As Figure 13 shows, the administration’s brief includes information for augmentations totaling $1.9 billion MCO tax funds ($4.6 billion total funds). (In addition to support for ongoing augmentations totaling $366 million enacted last year, the $2.7 billion estimate includes $375 million in MCO tax funds for two proposals—behavioral health and health care workforce—where more information is forthcoming.) The proposed Medi‑Cal increases would be effective January 2025. As Figure 13 shows, the proposal would not solely increase payments to providers. In many cases, it also would change the way Medi‑Cal pays providers. Below, we describe some of the major features of this package.

Figure 13

Medi‑Cal Provider Payments and Payment Methodologies

Would Change in Several Ways

Major Components of Governor’s MCO Tax‑Funded Provider Payment Proposal (In Millions)

|

Servicea |

Amount |

Proposal |

|

|

MCO Tax |

Total Funds |

||

|

Physician and professional services |

$1,075 |

$2,688 |

Tie most payments for primary care, obstetric care, non‑specialty mental health care, specialty care, and emergency physician services to 80 percent to 100 percent of what Medicare pays, depending on the service. Adopt Medicare payment structure, including by adjusting rates for regional variations in cost. Adopt new equity adjustment to incentivize service delivery in underserved areas. |

|

Hospital outpatient and emergency services |

500 |

1,215 |

For outpatient services, transition toward Medicare prospective payment system and Medicare adjustments for regional variations in cost. Adopt new equity adjustment to incentivize service delivery in underserved areas. For emergency services, explore extent to which prospective payment system can be applied. Enact interim rate adjustments ranging on average from 10 percent to 40 percent prior to roll out of prospective payment system. |

|

UC and county hospital inpatient services |

150 |

375 |

Transition to prospective payment system, similar to the way Medi‑Cal pays for inpatient services at private and district hospitals. |

|

Abortion |

90 |

90 |

Increase existing rates to a minimum of $1,150, with higher rates for certain geographic areas. Also sustain support for existing limited‑term supplemental payment for abortion services at non‑hospital clinics. |

|

Ground emergency medical transportation |

50 |

130 |

Increase rates to around 50 percent to 60 percent of Medicare and adopt Medicare payment structure. |

|

Clinics |

50 |

125b |

Expand and convert existing supplemental payment program for non‑hospital 340B providers into utilization and performance‑based managed care directed payment. |

|

Totals |

$1,915 |

$4,623 |

|

|

aExcludes proposed MCO tax allocations for behavioral health services and health care workforce initiatives, as the administration has not released detail on these proposals. bMaximum amount estimated by Department of Health Care Services. |

|||

|

MCO = managed care organization. |

|||

Further Ties Physician and Professional Payments to Medicare Level. Under the plan, most base payments for primary care, obstetrics, non‑specialty mental health care, specialty care, and emergency physician services would be tied to a percent of the Medicare level on an ongoing basis. The payments would range from 80 percent to 100 percent of Medicare, depending on the service. In addition, the department proposes to vary rates by geographic area to account for regional differences in costs, another feature of Medicare’s payment system.

Establishes New Prospective Payment Systems for Hospital Services. The administration’s proposal would change the way some hospital services are paid. Generally, these changes would adopt prospective payment systems, which pay for an episode of care instead of the volume of services. Specifically, DHCS proposes to establish a prospective payment system for outpatient services no sooner than 2027 and explore whether to adopt such a system for emergency room services. The department would model these payment systems largely based on the approach used in Medicare. In the interim, the department proposes to increase outpatient rates by an average of 10 percent and emergency room rates by an average of 40 percent. The administration also proposes to adopt a prospective payment system for inpatient services at UC and county hospitals, similar to the approach Medi‑Cal currently uses for private and district hospitals. This approach would replace the existing cost‑based reimbursement system and also replace a portion of local contributions with MCO tax funds.

Adopts New Equity Adjustment for Certain Services. For physician and hospital outpatient services, the administration also proposes establishing new equity adjustments. These adjustments would increase the level of payment to providers delivering services in certain geographic areas. The administration has not specified the exact parameters of the equity adjustment, but states that it could consider factors such as whether an area is a federally recognized health shortage area, whether an area is rural or is an urban health desert, the proportion of an area’s population that is enrolled in Medi‑Cal, and measures of the social determinants of health in an area. According to the administration, the goal of this proposal is to boost provider participation in Medi‑Cal in these geographic areas. The administration estimates the equity adjustment for physicians would cost $80 million MCO tax funds ($200 million total funds), or 7 percent of physician payments. The administration has not estimated how much funding would be devoted to the hospital outpatient equity adjustment.

Includes Several Other Approaches for Increases. Outside of physician and hospital services, the administration proposes various approaches to increase payments. For example, the administration also proposes to tie ground emergency transportation rates to a percent of Medicare. For abortion services, which generally do not have comparable Medicare rates, the administration proposes to increase rates to at least $1,150. According to DHCS, this level is what Oregon’s Medicaid program pays for abortion services and is among the highest rates paid among state Medicaid programs. The rates for both ground emergency medical transportation and abortion services also would vary by geographic area. For nonhospital clinics, the administration proposes to replace and expand funding for an existing supplemental payment program. The new program would be a managed care directed payment, with funds being allocated to clinics based on service utilization and performance outcomes. The Governor also proposes to extend a limited‑term fee‑for‑service supplement payment to nonhospital clinics for providing abortion services.

Sets New Payment Requirements on Managed Care Plans. In addition to increasing and changing the structure of fee‑for‑service payments, the proposal also would enact new requirements on managed care plans. For example, managed care plans would be required to pay the same fee‑for‑service rates for primary care, obstetric care, non‑specialty mental health care, specialty health care, and emergency physician services. As another example, plans would be required to increase their hospital patient and emergency room payments by 10 percent to 40 percent, similar to the proposed interim fee‑for‑service rate increases.

Assessment

Much of Proposal Remains Conceptual. In many ways, the administration’s proposal is conceptual, with key details still forthcoming. For example, the administration also has not determined key details of the proposed equity adjustment. In some cases, the time line to implement changes has not been finalized. Moreover, some aspects of the package—such as augmentations for behavioral health and health care workforce—are forthcoming.

Legislature Has Opportunity to Assess Broad Aspects of Proposal. The administration states that it is planning to release a package of trailer bill legislation on the proposed increases. Over the coming months, the Legislature likely will have more opportunity to weigh the details of each proposed increase. With more information forthcoming, we focus our assessment on the broad architecture of the package.

Proposed Package Raises Several Major Issues to Consider for Medi‑Cal Program

Tying Payment Increases to Medicare Worth Considering… The administration’s proposed approach of tying certain provider payments to a percent of the Medicare level on an ongoing basis has a few advantages. First, such an approach would allow for a more rational basis to adjust rates than what currently exists. Under the current approach, many rates generally are not adjusted annually, allowing them to lag behind inflation. Also, tying these payments to Medicare would address differences across rates that lack a clear policy basis. As a result, the administration’s proposed approach would help mitigate inequities and set forth a consistent approach for annual adjustments. Moreover, using Medicare payments as a benchmark for Medi‑Cal rates in concept is reasonable, as Medicare is a publicly funded health coverage program and comprises a sizable share of the health care market.

…But Trade‑Offs Exist. While the Medicare program often is used as a benchmark for state Medicaid payment levels, there are trade‑offs to tying Medi‑Cal’s provider payments to Medicare. Most notably, such an approach would tie Medi‑Cal’s provider payment adjustments to federal policy decisions. A March 2023 nonpartisan analysis concluded that Medicare payments for physician and professional services appear adequate to enable patients to access care. That said, the analysis also found that annual adjustments to these payments since 2010 have not kept pace with the growth in medical costs, though spending per beneficiary (which accounts for the volume and intensity of services rendered, in addition to costs) kept closer pace with inflation. Future federal decisions are uncertain, and they may not always align with the needs of the Medi‑Cal program, which serves a different population than Medicare.

Proposed Prospective Payment Systems Also Worth Considering, Though Further Analysis Is Warranted. In concept, prospective payment systems have certain advantages over traditional procedure‑based reimbursements for hospitals. Most importantly, because these systems pay for an episode of care, rather than for every procedure, hospitals have incentives to avoid unnecessary services and treat patients efficiently. That said, designing effective prospective payment systems is a complex exercise. Research and analysis from DHCS is warranted to ensure these new systems provide the intended incentives and avoid unintended consequences. Also, time likely will be needed for hospitals to adjust to these new systems, particularly for those hospitals that have little experience billing Medicare for services. Moreover, because Medi‑Cal also provides supplemental payments to hospitals, some of which are allocated based on cost, the overall impact of the new base payment systems on hospital behavior is uncertain.

Proposed Equity Adjustment Worth Considering, but Impact Is Uncertain. Medi‑Cal beneficiaries have different access to services depending on where they live in the state. Some regions have fewer primary care or behavioral health providers per capita than others, likely affecting access to care. The supply of specialists also varies by region. Partly in response to these supply constraints, managed care plans apply for alternative time and distance standards in some localities. An equity adjustment could better target resources and incentivize providers to serve Medi‑Cal beneficiaries in these regions. That said, whether the adjustment as proposed would be of a sufficient size to alter provider behavior is uncertain. Moreover, it is uncertain how long it would take for providers to respond to these new incentives.

In Many Cases, Assessment of Proposal Depends on Details. In many cases, more information likely will be critical to fully weigh the administration’s proposed approach. For example, in contrast to other areas of the proposal, the administration has not clarified how abortion rates would be adjusted following the increase in January 2025. While the sizable increase in 2025 might mitigate the need for annual adjustments in the short term, over the longer term, rates likely will lag again behind inflation if they are not consistently adjusted. As another example, more information likely is needed to assess the proposed directed payment program for nonhospital clinics. As we noted in our past publication, The 2020‑21 Budget: Analysis of the Medi‑Cal Budget, the existing fee‑for‑service supplemental payment program, which is intended to backfill lost clinic pharmacy revenues, lacks a clear public purpose. Replacing this program with a directed payment tied to service delivery and performance could better incentivize access and quality. The extent of the impact, however, likely depends on how the funds will be allocated and what performance measures will be considered.

Proposal’s Overall Impact on Managed Care System Difficult to Assess. Historically, the state has sought to maintain payment adequacy in the managed care system by setting actuarially sound rates to plans and by holding plans accountable to access and quality standards. When plans find it is warranted to increase provider payments to ensure access and quality, the associated costs eventually are incorporated into the rates paid by the state to the plans, so long as the state deems these costs to be reasonable. Given this overarching system and the risk born by managed care plans in serving Medi‑Cal patients, plans historically have had flexibility to negotiate payment levels with their providers. Over time, however, the state has become more prescriptive in the level of payment managed care plans provide for services—a practice that the administration proposes to expand. Such an approach could better ensure provider payment increases are targeted to high‑priority areas, but also potentially complicate state oversight and health plan administration of payments and services.

Future Uncertainties Could Impact Proposal

Package Lacks Long‑Term Funding Strategy. As we noted in the “MCO Tax Budget Solution” section of this report, there is an expected, though not certain, shortfall in the proposed MCO tax package, estimated by the administration to begin mid‑2028. The risk of a shortfall exists because future federal rule changes may require the state to adopt a much smaller MCO tax in 2027, relative to the current version. In discussions with our office, the administration has emphasized that it intends for the provider rate increases to be ongoing but has not identified a permanent funding source.

State’s Uncertain Budget Condition Heightens Funding Risks. Since the 2023‑24 budget and the MCO tax package were enacted, the state’s budget picture has deteriorated. Under the Governor’s budget, the state is addressing a significant budget problem in the near term and is projected to face deficits in the out‑years. Absent corrective measures, the state likely will not have enough budget capacity to fund all of its ongoing commitments over the next few years. Were fiscal constraints to persist in the future, and were the next version of the MCO tax to be much smaller than the current one, the Legislature could face pressure to pull back some of the augmentations in the MCO tax package and reverse some payment changes. Doing so likely would pose challenges for managed care plans and providers, after having spent considerable time adjusting their contracts and operations to the proposed changes. Moreover, such actions could require the state to rescind plans for future changes after having spent considerable effort researching and developing them. For example, the administration proposes to adopt a new approach for paying for hospital outpatient services no sooner than 2027—potentially not long before the provider payment reserve is depleted.

If Enacted by Voters, New Voter Initiative Could Require Changes to Proposed MCO Tax Package. After the state enacted the 2023‑24 budget package, an initiative was submitted to permanently authorize the MCO tax and codify how the funds would be spent. As with many other initiatives, it is uncertain whether the measure will qualify for the November 2024 ballot and, if so, if voters would enact it. If the measure were enacted, it could require some adjustments to the proposed MCO tax package. The extent to which changes would be needed, however, is uncertain. In conversations with our office, DHCS indicated that it has not fully studied the differences between the Governor’s proposal and initiative, or the programmatic and fiscal implications of these differences. It likely will be important for the Legislature to better understand these differences and keep them in mind as it weighs its own plans for the MCO tax package.

Legislative Oversight Will Be Key

Major Changes Warrant Legislative Approval and Oversight. Because the administration has not released its proposed trailer bill legislation, it is uncertain what role is intended for the Legislature and how much flexibility will be proposed for DHCS. The Legislature likely will want to be involved in the design and approval of key elements of the proposed payment changes, given the package’s potentially far‑reaching and long‑term impacts to the Medi‑Cal program. For example, the Legislature likely will want to review the parameters of proposed equity adjustments before they go into effect.

Department and Managed Care Plans Could Face Hurdles to Implement Increases. Much of the proposal would require substantial changes to the way Medi‑Cal pays providers both in fee‑for‑service and managed care. Experience with the recently enacted provider payment increases in 2024 suggest that the department and managed care plans could face challenges going forward. Managed care plans have told our office that the 2024 rate increases are requiring changes to their contracts with providers, involving months of work. Given the much more expansive nature of this year’s proposal, it is possible unexpected challenges and disruptions could arise, potentially delaying the timing of when payment increases are disbursed to providers. Legislative oversight will be key to monitor the implementation of the proposed MCO tax package.

Data and Assessment Will Be Key for Legislature in Coming Years. Because of the uncertainties around the MCO tax package and the state’s fiscal condition in the future, the Legislature may face difficult decisions around which increases to sustain. To ensure its decisions are well informed, the Legislature likely will want to have data and analysis assessing which of the proposed augmentations had the greatest impact on access, quality, and equity.

Recommendations

Focus on Several Key Principles. Given the many issues and policy trade‑offs raised by the proposal, we recommend the Legislature begin thinking about its plans for the MCO tax package. As Figure 14 shows, we think several key principles could guide legislative decision making. We describe each principle further below.

Figure 14

Key Principles Could Guide Legislative Decisions

LAO Recommended Principles for MCO Tax‑Funded Provider Payment Increases

|

|

|

|

|