Bottom Line: Economic data suggest the state’s economy showed promising improvement in October, but this one-month uptick should be viewed with some caution.

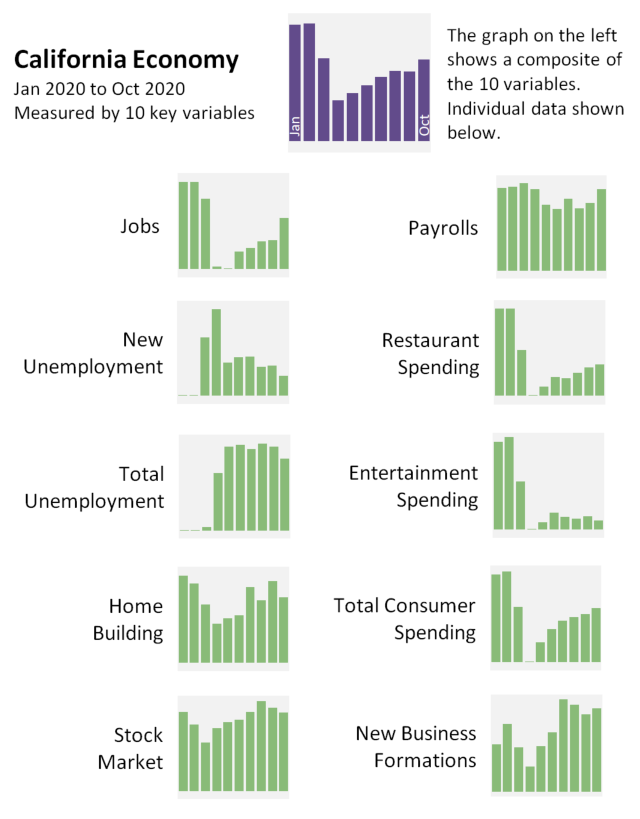

The COVID-19 pandemic has reshaped the California economy. Over the last several months, the state has experienced abrupt and dramatic swings in economic activity. While a variety of data is available to track developments in the state economy, drawing clear conclusions from these disparate data points can be difficult. To help make sense of this varied data, this post pulls together and synthesizes ten key data points on the state economy. Our goal is to provide a quick, simple snapshot of recent trends in this data. The graphic below provides this snapshot.

We display each variable as a standardized index that shows how the current level of each variable compares to historic norms. At the top of the graphic, we aggregate the ten variables into a single measure that attempts to capture what changes in the individual variables can tell us about the overall trend in the state’s economy.

As this measure shows, California’s economy experienced a precipitous drop in the spring, followed by a rapid rebound. The indicators suggest the pace of the recovery slowed in August and September. October data, however, suggest another major positive jump in the state’s economic situation, but there are reasons to interpret this apparent uptick with caution. In particular, a key driver in the uptick is a large increase in employment. According to the official survey, California’s total employment jumped almost 900,000 in October, 40% of the entire national increase and the single largest monthly increase since the recovery began. Most of this increase is attributed to self-employed workers and independent contractors. While it is possible that California really did see a dramatic employment increase in October, it is important to note that the monthly employment estimates are noisy and subject to measurement error. The actual increase was likely below 900,000.