LAO Contacts

- Jason Constantouros

- Provider Taxes

- Karina Hendren

- Overview

- Oversight and Development of Budget Solutions

- Min Lee

- Base Spending

- H.R. 1 Implementation

- Will Owens

- Oversight and Development of Budget Solutions

March 2, 2026

The 2026-27 Budget

Medi‑Cal Analysis

- Introduction

- Overview

- Base Spending

- Provider Taxes

- H.R. 1 Implementation

- Oversight and Development of Budget Solutions

Executive Summary

Medi‑Cal Spending Continues to Rise. Over the last decade, spending in Medi‑Cal, California’s Medicaid program, has more than doubled both on a General Fund and total funds basis—faster than the growth in the overall state budget. Spending continues to grow under the Governor’s budget, with estimated Medi‑Cal spending reaching an all‑time high of $49 billion General Fund ($222 billion total funds) in 2026‑27.

More Information Needed to Fully Assess Drivers of Base Spending Growth. Base spending (spending on core services to enrollees) has been the primary driver of spending growth in Medi‑Cal over the last decade. We estimate most of the spending growth has been driven by per‑enrollee cost increases, with a much smaller share coming from changes in the caseload level and composition. These per‑enrollee cost increases have been due to greater utilization of services, higher service costs, and recent state benefit expansions. These trends, however, are difficult to fully assess without better data on key expenditures, such as managed care costs and costs for undocumented beneficiaries. We recommend the Legislature enhance its oversight by directing the administration to provide richer data on the Medi‑Cal program moving forward.

Provider Taxes Are Ramping Down. In recent years, the state has turned to certain taxes on health care providers to help cover growing Medi‑Cal costs. Under new rules in the recently enacted federal H.R. 1 legislation, however, the state will need to notably reduce two large provider taxes—a tax on health plans and a fee on private hospitals. The reductions will result in billions of dollars of lost revenue. The state appears to have limited ability to pursue a higher private hospital fee under the new federal rules. However, the state may have more options to pursue a larger health plan tax if it shifted more costs onto private health plans and their consumers. This change would require amending Proposition 35 (2024). We recommend weighing the policy trade‑offs of pursuing a larger health plan tax in light of the state’s fiscal challenges.

Legislature Faces Choices to Implement H.R. 1’s Eligibility Changes. The administration has released a plan to implement H.R. 1’s changes to Medicaid eligibility rules. The plan includes a number of key policy choices—most notably, ending comprehensive coverage for certain immigrant groups and applying work requirements to others. These proposals come amid a challenging fiscal backdrop, so the administration’s concern about the feasibility of backfilling lost federal funding for certain groups is understandable. At the same time, the proposals would apply different rules across immigrant groups, raising equity concerns and implementation challenges. The Legislature may want to consider whether alternative approaches such as income‑based eligibility or modified benefit designs could achieve comparable savings while preserving access to high‑priority services.

Limiting Cost Growth in Medi‑Cal Could Raise Key Trade‑Offs. In response to rising Medi‑Cal costs and the state’s tight fiscal situation, the Legislature enacted a number of budget solutions in Medi‑Cal in the 2025‑26 budget. The amount of savings ramps up in 2026‑27 under the Governor’s budget, largely as planned. The feasibility of these estimated savings is subject to a fair amount of uncertainty. Even if the savings materialize as intended, however, the state budget is still projected to have sizable structural deficits in future years. As such, the Legislature may need to begin considering more ongoing solutions across the budget. Options exist in Medi‑Cal to further limit spending growth, but most raise key trade‑offs around access to health care for low‑income people.

Introduction

This report analyzes the Governor’s proposals in the 2026‑27 budget for Medi‑Cal, California’s Medicaid program. It first provides an overview of Medi‑Cal and its proposed budget. We then analyze the Governor’s proposals regarding base program spending (spending driven by caseload, service utilization, and provider rates), provider taxes, implementation of recent federal legislation (H.R. 1), and budget solutions enacted in 2025. Throughout this brief, we discuss General Fund spending growth in Medi‑Cal over the last several years, including information on the cost drivers of this growth and the levers available to the Legislature to further contain it.

Overview

In this section, we provide key background on the Medi‑Cal program, analyze recent programmatic spending trends, and describe Medi‑Cal spending in the Governor’s proposed budget.

Background

Medi‑Cal Provides Health Coverage for Low‑Income Californians. Medi‑Cal, the state’s Medicaid program, provides health care coverage for low‑income Californians. Health care services covered by Medi‑Cal include visits to the doctor’s office, stays at the hospital, prescription drugs, behavioral health services, long‑term care, and dental services, among many other areas. The Governor’s budget estimates an average monthly Medi‑Cal caseload level of 14.5 million people in 2025‑26, about one‑third of Californians.

Medi‑Cal Is a State‑Federal Partnership. The state and the federal government share programmatic and fiscal responsibilities for Medi‑Cal. The federal government created Medicaid and imposes program requirements on states, such as covering a minimum set of services for certain populations. The state, in turn, is responsible for implementing Medi‑Cal. California has chosen to go beyond the minimum federal requirements, such as by covering optional services and expanding eligibility to additional populations (many of which come with matching federal funds). California has also received waivers from certain federal rules over the years, generally to test new approaches for serving beneficiaries and delivering care.

Medi‑Cal Delivers Services in Many Ways. The primary way Medi‑Cal delivers services to beneficiaries is by contracting with health plans (also known as managed care plans). The state provides health plans monthly payments to enroll Medi‑Cal beneficiaries, while the plans in turn are required to arrange for the health care of their enrollees. While most services are delivered in the managed care system, some are delivered in other ways. For example, Medi‑Cal pays for some health care services, such as pharmacy benefits, by reimbursing providers directly; this arrangement is known as the “fee‑for‑service” delivery system. County governments also play a key role in delivering certain services, particularly behavioral health care.

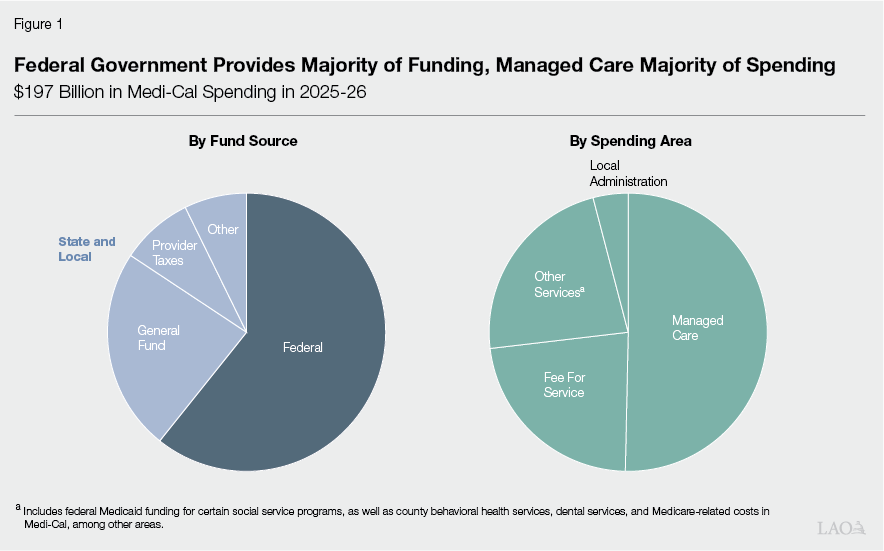

Many Sources Support Medi‑Cal’s Budget. The federal government and the state also share fiscal responsibilities for Medi‑Cal. The federal share of Medi‑Cal cost varies by service—it is 50 percent in most cases, but higher or lower for some populations and services. As Figure 1 shows, these varied formulas result in a net federal share that is more than half of cost. The state is responsible for covering the remaining share. The primary source of support is the state’s General Fund. The second largest source is a handful of taxes and fees specifically on certain health care providers (such as health plans and hospitals). Many other sources also help cover the state share of cost, including funds from local governments.

Managed Care Comprises Just Around Half of Spending. Though managed care is Medi‑Cal’s primary delivery system, it comprises just around half of overall programmatic spending. Fee‑for‑service comprises around one‑quarter, with other services and county administrative costs comprising the remainder. Fee‑for‑service’s relatively outsized portion of spending is largely from pharmacy benefits being paid for all Medi‑Cal members—including those in the managed care system—on a fee‑for‑service basis. Much of the funding for other services reflects federal Medicaid funding for certain social service programs in the Department of Social Services and Department of Developmental Services. The federal funds are initially reflected in Medi‑Cal’s budget, but ultimately transferred to the other departments.

Recent Medi‑Cal Spending Trends

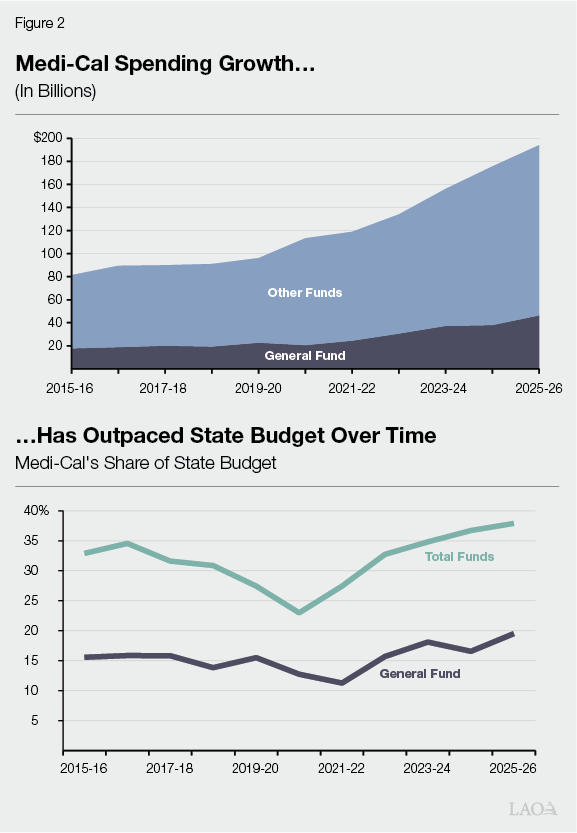

Medi‑Cal Is a Sizable Portion of State Budget. Medi‑Cal is one of the largest programs in the state budget. On a total funds basis, it is the largest, comprising nearly 40 percent of spending from all sources (including federal funds to California) in recent years. Its share is smaller just on a General Fund basis, currently comprising around 20 percent of all General Fund spending. This makes Medi‑Cal the second largest program in terms of General Fund spending (after Proposition 98 [1988], the state’s minimum spending requirement for K‑14 education).

Medi‑Cal Spending Has Outpaced Overall State Budget in Recent Years. Medi‑Cal is not simply a large program—it also is growing. As Figure 2 shows, Medi‑Cal spending has more than doubled over the last ten years, both on a General Fund and total funds basis. Spending across the overall state budget also grew over this time, nearly doubling. Because Medi‑Cal grew at a faster rate, its share of the state budget increased, particularly following the COVID‑19 pandemic. Medi‑Cal’s spending growth is due to underlying programmatic trends, as well as policy changes expanding eligibility, benefits, and provider rates.

Growth in Per‑Enrollee Spending Has Driven Most of Spending Growth. Virtually all of the growth in General Fund spending has come from changes in the number and composition of enrollees, as well as spending per enrollee. (On a total funds basis, other unrelated factors, such as growth in federal Medicaid funding for certain social service programs, also are key drivers.) We estimate that growth in the number of enrollees and shifts in the population mix—generally, relatively more costly seniors becoming a larger share of the caseload—account for around 10 percent to 20 percent of the growth. This means that per‑enrollee spending—reflecting changes in benefits, service utilization, and service costs—have driven most of spending. (We further describe the key drivers of this growth in the “Base Spending” section.)

Recent Fund Shifts Have Helped Limit General Fund Spending Growth. In recent years, the Legislature has sought to offset a portion of General Fund spending growth by using other fund sources. Most notably, the state significantly increased a tax on health plans (known as the managed care organization tax) to help cover costs. In the 2025‑26 budget, the Legislature also approved a loan from state cash reserves to temporarily cover costs. We estimate these combined actions offset over $6 billion in General Fund spending growth over the last ten years.

Growth Prompted Legislature to Enact Ongoing Budget Solutions in Medi‑Cal. The sizable growth in Medi‑Cal spending, coupled with a structural deficit in the state budget, prompted the Legislature to enact several ongoing budget solutions in Medi‑Cal in the 2025‑26 budget. The solutions cover several areas, including limiting some of the undocumented immigrant expansions and imposing new approaches to limit drug utilization. These solutions are scheduled to ramp up over time. As a result, most of the savings likely will be realized in future years.

Recent Federal Legislation Likely Will Drive Up Some Medi‑Cal Costs. Subsequent to the Legislature enacting the 2025‑26 budget in June 2025, federal policymakers passed in July 2025 H.R. 1—titled the One Big Beautiful Bill Act. This legislation includes about $1 trillion in federal Medicaid reductions nationwide over ten years, representing the most significant changes to federal Medicaid policy since the Patient Protection and Affordable Care Act. Only a handful of changes under H.R. 1 took effect immediately. The legislation sets out a schedule for the remaining changes to be implemented over the next few years. These changes will drive up state spending on Medi‑Cal, likely offsetting some of the savings anticipated from the state’s enacted budget solutions. We describe H.R. 1 provisions in our 2025 report, Considering Medi‑Cal in the Midst of a Changing Fiscal and Policy Landscape.

Governor’s Budget

Estimates Continued Growth in Medi‑Cal Spending. As Figure 3 shows, the Governor’s budget estimates total Medi‑Cal spending from all fund sources to be nearly $200 billion in 2025‑26, the same amount assumed at budget enactment in June 2025. From this level, it increases to over $220 billion in 2026‑27. While spending grows across all of Medi‑Cal’s fund sources, there is less growth in General Fund spending compared to federal and other sources. Medi‑Cal spending growth continues to equal or exceed spending growth in the state budget as a whole, with Medi‑Cal comprising about 20 percent of overall state General Fund spending and over 40 percent of the state’s total funds spending in 2026‑27.

Figure 3

Medi‑Cal Spending Continues to Rise in Governor’s Budget

(Dollars in Billions)

|

2025‑26 |

2026‑27 |

Change From 2025‑26 Revised |

|||||

|

Enacted |

Revised |

Proposed |

Amount |

Percent |

|||

|

Total Spending |

$196.7 |

$196.7 |

$222.4 |

$25.7 |

13.1% |

||

|

By Fund Source |

|||||||

|

Federal funds |

$119.7 |

$119.4 |

$137.5 |

$18.0 |

15.1% |

||

|

General Fund |

44.9 |

46.4 |

48.8 |

2.4 |

5.2 |

||

|

Other funds |

29.7 |

28.3 |

36.1 |

7.8 |

27.6 |

||

|

By Program |

|||||||

|

Managed care |

$100.4 |

$99.0 |

$123.2 |

$24.2 |

24.5% |

||

|

Fee for service |

45.6 |

44.8 |

43.5 |

‑1.4 |

‑3.1 |

||

|

Other programs |

43.3 |

44.8 |

48.0 |

3.2 |

7.2 |

||

|

Local administration |

7.5 |

8.0 |

7.7 |

‑0.3 |

‑3.9 |

||

General Fund Spending Is Up in Current Year, Primarily From One‑Time Repayments. Though overall 2025‑26 spending for Medi‑Cal remains unchanged, General Fund spending is $1.4 billion higher, with equivalent downward revisions from federal and other sources. Much of the increase in General Fund spending is due to higher repayments to the federal government. These repayments generally reflect corrections to erroneous federal claiming for state‑only services provided to enrollees with unsatisfactory immigration status (UIS). A few other smaller factors also drive the increase, such as lower‑than‑projected savings in 2025‑26 for certain budget solutions the state enacted last year.

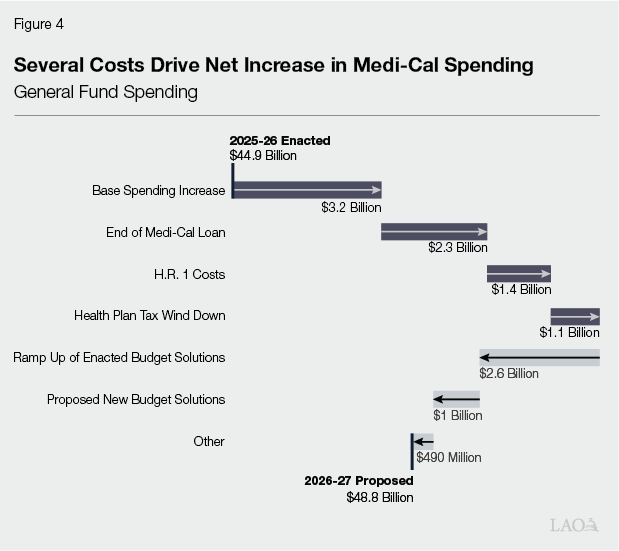

General Fund Spending, on Net, Up in Budget Year for Several Key Reasons. As Figure 4 shows, several factors drive the net increase in General Fund spending in 2026‑27 over 2025‑26 levels. The largest driver is base spending increases from caseload, service utilization, and service costs. Additionally, a one‑time loan to Medi‑Cal in 2025‑26 ends in 2026‑27, requiring a backfill from the General Fund. (The budget anticipates repaying the loan over time beginning in 2027‑28.) Other key drivers include new costs associated with the federal H.R. 1 legislation, as well as the winding down of the state’s provider tax on health plans. Some savings, such as the ramp up of enacted budget solutions in 2026‑27 and proposed new budget solutions, partially offset some of these spending increases.

In Budget Year, Timing of Certain Provider Payments Drives Some of the Increase in Other Fund Sources. The factors driving the growth in General Fund base spending also drive the growth in spending from non‑General Fund sources in 2026‑27. Aside from base spending factors, the growth in spending from non‑General Fund sources appears to be due to a change in timing for certain supplemental provider payments. Most notably, the administration projects a $16 billion (154 percent) increase in supplemental payments in 2026‑27 through the state’s fee on private hospitals. The administration states that it expects to disburse payments to private hospitals on an accelerated timeline, resulting in 24 months of payments being released in the budget year. Additionally, a lag in the implementation of provider payments funded by the state’s health plan tax also results in payments occurring in 2026‑27, rather than in 2025‑26 as initially expected.

Base Spending

In this section, we analyze key trends and estimates around base spending (core spending on services to beneficiaries) in Medi‑Cal. We first provide background on the key drivers of base spending. Next, we analyze recent trends around each driver. We then describe the estimates in the Governor’s budget. We conclude by assessing these trends and estimates and offering associated recommendations.

Background

Base Spending Is Driven by Size of Caseload… Medi‑Cal base spending is the product of (1) the number of enrollees served and (2) the average cost per enrollee. As a result, even modest changes in caseload can have sizable budget effects.

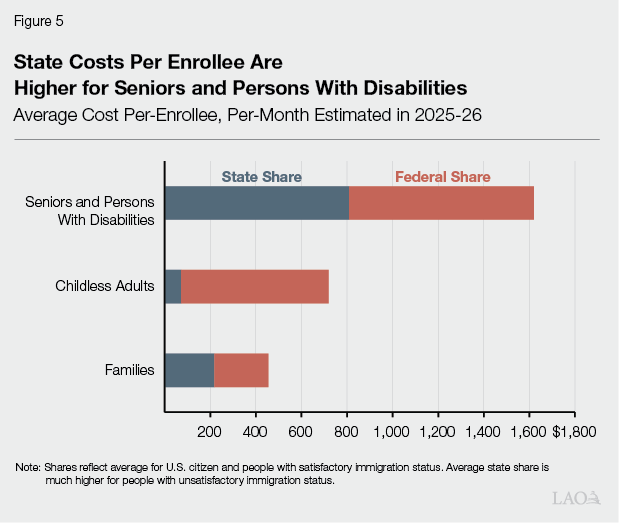

…Composition of Caseload… Base spending is also affected by the mix of enrollees across populations. This is because some populations use more services or rely on more costly services (such as long‑term care), resulting in higher costs on average. As Figure 5 shows, seniors and persons with disabilities have average costs that are more than double those of families and childless adults. Consequently, shifts in caseload toward higher‑cost groups can increase total spending even when overall enrollment is stable or declining.

…Benefits… What benefits are offered to beneficiaries also influences costs. This is because some services—such as hospital inpatient stays and long‑term care—are much costlier than others. Many key Medi‑Cal benefits are mandatory, meaning that the state must offer them under federal law. States have the option to add more benefits above the mandatory minimum. In recent years, for example, Medi‑Cal added new benefit components including enhanced care management, community supports, and coverage for wellness coach services. In addition, many undocumented adults have moved from restricted‑scope coverage (limited to certain services) to full‑scope coverage.

…And Utilization and Unit Costs, Primarily in Four Key Areas. In addition to benefits covered, per‑enrollee costs depend on how often enrollees use these services and the unit cost per service. Most changes in underlying utilization and unit costs show up in one of the following:

- Managed Care Capitated Rates. Most Medi‑Cal enrollees receive services through managed care plans that are paid fixed monthly amounts per enrollee (capitation). Capitation rates are intended to cover the projected cost of providing covered benefits for a defined population and period. In general, these rates reflect past spending data, adjusted using actuarial assumptions about future utilization and costs.

- Fee‑for‑Service Payments. The state directly pays for a smaller share of Medi‑Cal services on a fee‑for‑service basis, where spending is driven by utilization and unit costs. Like capitation, fee‑for‑service spending can grow even when program enrollment or benefits remain the same, due to changes in prices, service intensity, and service mix.

- Pharmacy Costs. Unit costs in pharmacy are driven by the underlying price of drugs, as well as the amount of rebates connected to the drugs. (Rebates are negotiated savings drug makers pay to Medi‑Cal after the drug is purchased.) Tracking pharmacy spending over time is somewhat challenging because Medi‑Cal’s method of paying for outpatient prescription drugs shifted from a combination of managed care and fee‑for‑service to fee‑for‑service only in 2021 (known as Medi‑Cal Rx).

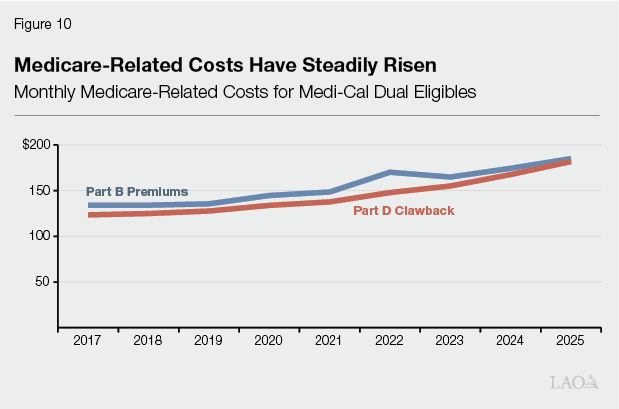

- Medicare‑Related Costs. For beneficiaries who are dually eligible for Medicare and Medi‑Cal, Medi‑Cal generally pays their Medicare premiums (in addition to certain other cost sharing). Medi‑Cal also incurs the Part D “clawback,” which is a state payment to the federal government for a portion of prescription drug costs of dual eligibles who receive drug coverage through Medicare instead of Medicaid. As a result, growth in the number of dual eligibles or in Medicare premiums and the Part D clawback can increase Medi‑Cal spending.

Federal Cost Sharing Also Affects General Fund Costs. Finally, growth in General Fund spending can arise from not only higher total costs, but also changes in how costs are financed. Federal matching rates vary across eligibility groups; for example, childless adults generally receive a 90 percent federal match, whereas individuals with UIS do not receive federal matching funds for most nonemergency services. As a result, shifts in enrollment toward groups with lower federal cost sharing can increase General Fund costs even when total spending is unchanged.

Recent Trends and Cost Drivers

Section Looks at Key Recent Trends in Caseload and Per‑Enrollee Costs. In this part, we describe trends in Medi‑Cal enrollment and per‑enrollee costs from 2017‑18—the first year for which some of our data are available—through 2025‑26, and highlight the factors that appear to be driving spending growth. As the nearby box explains, our methodology aims to isolate the effect of a given component by holding all other components constant. Given significant data limitations, however, our estimates should be interpreted as rough and subject to measurement error.

How Did We Analyze Base Spending Trends?

Analyzes Key Department Data. Most of our trend analyses utilize data from the Department of Health Care Services. For example, our caseload analysis considers monthly caseload data that is publicly available, coupled with limited data on costs from past department estimates. We also analyze managed care rate trend data that the department generally provides our office annually. We used similar sources for fee‑for‑service, pharmacy, and Medicare data.

Holds Certain Factors Constant to Isolate Effects. To isolate the effects of different factors, we aimed to hold other factors constant. For example, to assess the fiscal impact of caseload changes, we hold per‑enrollee costs constant over the time period. Similarly, to analyze the effects of utilization changes over time, we hold unit costs constant.

Has Three Key Limitations. Three key factors limit the conclusions we could draw.

- Data Limitations. Most notably, most data on utilization and costs in managed care—Medi‑Cal’s primary delivery system—are confidential. As such, we had to rely on very limited data provided by the department to analyze trends. In some cases, we also had to make certain assumptions about trends in later years when the department’s data ended before 2025‑26.

- Effects of Policy Changes. Our analysis was not able to fully disentangle the effects of certain policy changes. This is partly due to data limitations, which do not allow us to capture many policy changes after 2023. Many of our analyses also hold the General Fund share of spending within aid categories constant over time, which means that financing shifts—such as the increased state‑only financing associated with expansion of full‑scope coverage to undocumented adults—are generally not captured in the estimates of individual spending drivers.

- Shifts Between Delivery Systems. Over time, the state has shifted certain populations and services from fee‑for‑service to managed care. These shifts can influence cost trends within each delivery system. For example, having fewer beneficiaries in fee‑for‑service likely results in higher costs per beneficiary over time, as those who remain in fee‑for‑service tend to be costlier populations with significant medical needs.

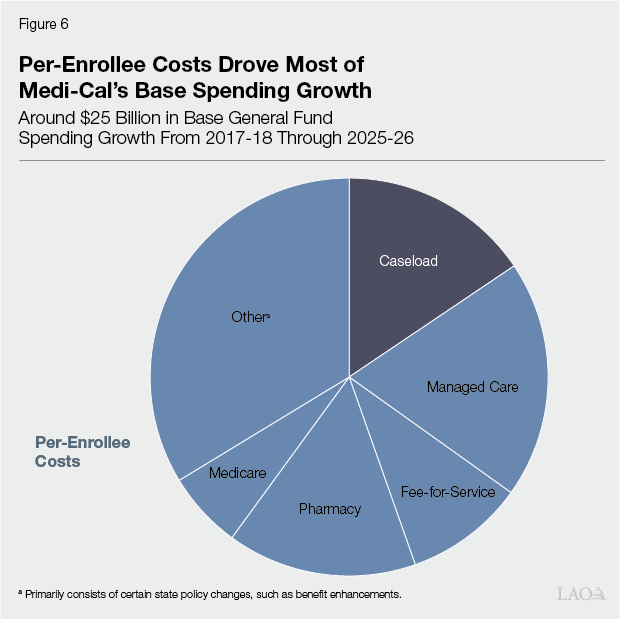

Per‑Enrollee Costs Appear to Account for Most of the Recent General Fund Growth. We estimate General Fund base spending in Medi‑Cal increased by about $25 billion from 2017‑18 to 2025‑26—an average annual increase of about 8 percent. As Figure 6 shows, our estimates suggest that growth in per‑enrollee costs accounts for a larger share of this spending increase than changes in caseload (level and composition). Due to data limitations, however, our analysis was not able to account fully for the growth in per‑enrollee costs. As we discuss later, the remainder is likely from major policy changes enacted since 2017‑18, the effects of which are difficult to disentangle from underlying trends. We describe each component driving base spending growth further below.

Caseload Level and Composition

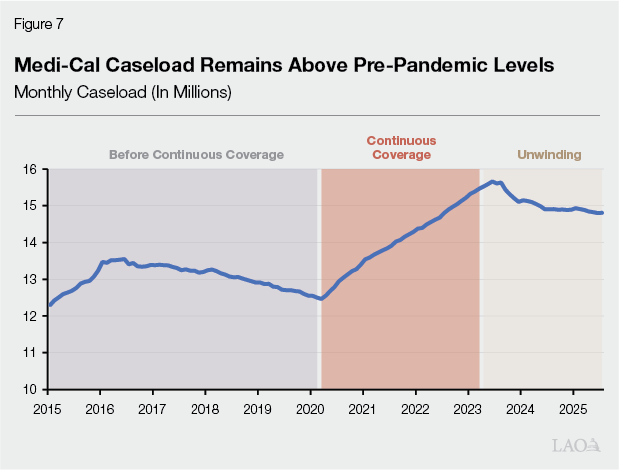

Pandemic Notably Changed Caseload Trends. Prior to the COVID‑19 pandemic, Medi‑Cal caseload showed signs of a sustained, gradual decline, especially among childless adults and families. This changed beginning in March 2020, when the federal continuous coverage requirement prohibited states from disenrolling most beneficiaries. With new enrollees continuing to enter the program but very few exiting, Medi‑Cal’s caseload reached an all‑time high of nearly 16 million people by mid‑2023, as Figure 7 shows.

Caseload Has Remained Above Pre‑Pandemic Levels During Unwinding Period. The continuous coverage requirement expired in the second half of 2023, causing states to resume 12‑month redeterminations. However, caseload continued at somewhat elevated levels. At least some of this phenomenon could be attributed to temporary federal approval of streamlining certain renewal processes to help mitigate disenrollments. This federal approval expired in 2025, potentially setting the stage for further declines than observed to date, although the pace and magnitude remain uncertain.

Caseload Mix Has Become More Expensive. Over time, seniors and persons with disabilities have increased as a share of Medi‑Cal enrollment, from about 16 percent in 2017‑18 to 18 percent in 2025‑26. This pattern primarily reflects robust growth in the senior population both before and after the pandemic. Because seniors and persons with disabilities have substantially higher per‑enrollee costs than the average Medi‑Cal beneficiary, relatively modest shifts in caseload mix can still translate into meaningful increases in overall spending.

Caseload Growth and Changes in Caseload Mix Have Had Distinct Fiscal Effects. We estimate that the increase in Medi‑Cal caseload from about 13.3 million enrollees in 2017‑18 to 14.5 million in 2025‑26 (with a somewhat different caseload mix) increased General Fund base spending in 2025‑26 by about $4 billion. The fiscal impact of the change in caseload mix on its own is relatively modest. This is because the increased costs from a rising share of seniors and persons with disabilities are partially offset by compositional shifts among other groups, including a declining share of higher‑cost families and a rising share of lower‑cost childless adults.

Managed Care Capitated Rates

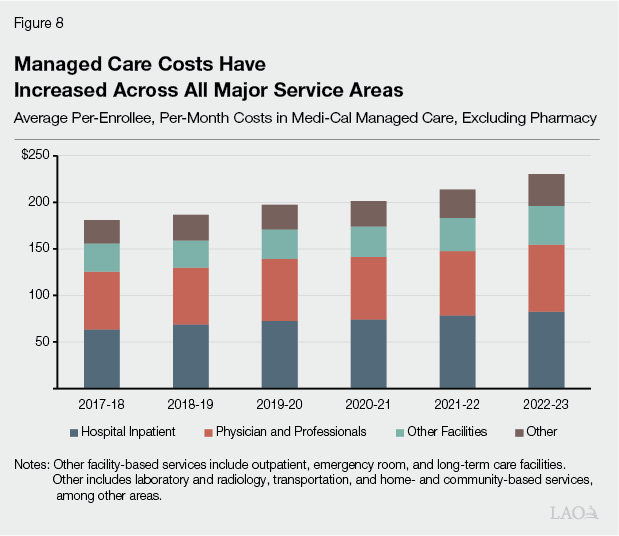

Managed Care Rates Have Risen, With Particularly Rapid Growth for Higher‑Cost Populations. As Figure 8 shows, managed care capitated rates have risen since 2017‑18, with increases evident across all major service areas. On a General Fund basis, the average per‑enrollee cost grew by about 4.6 percent annually through 2023 (the most recent year available). Growth varied by population, with the highest rate for seniors and persons with disabilities (7 percent) and the lowest for childless adults (3 percent).

Rising Per‑Enrollee Costs Translate Into Several Billion Dollars of Additional General Fund Spending. We estimate that higher managed care per‑enrollee costs increase General Fund spending by roughly $5 billion in 2025‑26 over 2017‑18 levels. A little more than half of this increase is attributable to seniors and persons with disabilities, followed by adults with children (about a quarter). By service category, inpatient hospital services account for the largest estimated increase (about 35 percent), followed by other services (28 percent), which include laboratory and radiology, transportation, and home‑ and community‑based services, among others.

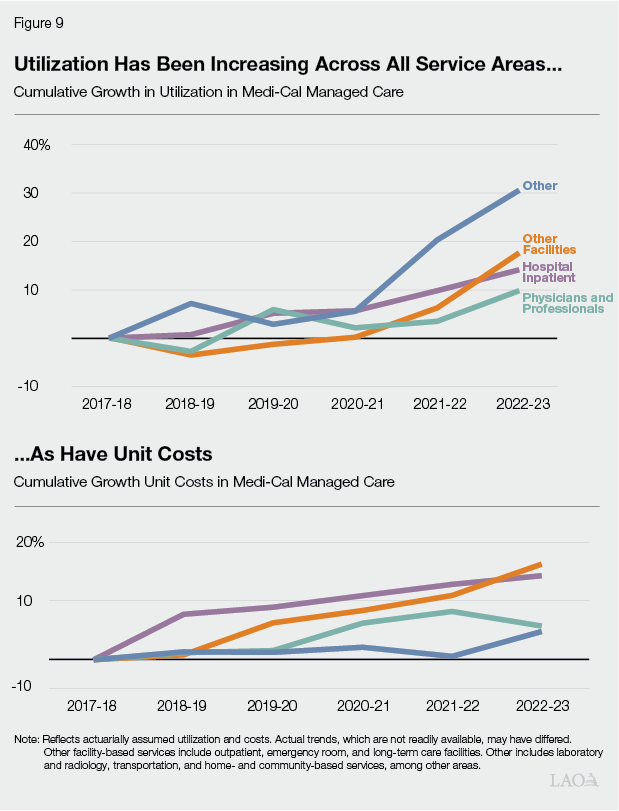

Higher Service Use and Unit Costs Appear to Be Driving Managed Care Cost Growth. As Figure 9 shows, both utilization and unit costs appear to be rising across most service areas of managed care. We estimate that roughly 60 percent of the increase in capitation spending is attributable to higher utilization, with the remaining 40 percent attributable to higher unit costs. The relative importance of these factors varies across populations and services. For example, the 60‑40 percent split holds for seniors and persons with disabilities, whereas unit costs account for nearly 90 percent of the spending growth among children.

Other Per‑Enrollee Cost Trends

Fee‑for‑Service Costs (Other Than Pharmacy) Also Have Increased, With Growth Driven Largely by Higher Unit Costs. Although fee‑for‑service now represents a smaller share of Medi‑Cal spending than managed care, we estimate that average monthly costs per user—excluding pharmacy—have increased by 5.4 percent per year since 2017‑18. This growth translates to around $2.5 billion in additional General Fund spending. In contrast to managed care, where rising utilization appears to play a larger role, we attribute 86 percent of this spending increase to the growth in unit costs. Growth has been particularly rapid in certain areas, most notably payments to safety net clinics (which tend to grow over time based on medical inflation).

Pharmacy Has Been a Major Driver of Per‑Enrollee Cost Growth. Across both managed care and fee‑for‑service, we estimate that General Fund pharmacy costs per enrollee have increased by nearly 13 percent per year since 2017‑18. The estimate reflects net pharmacy costs after accounting for federal and state drug rebates. This per‑enrollee growth translates to nearly $4 billion in additional General Fund spending in 2025‑26. We have limited data to fully assess the drivers, but they likely reflect a combination of increased utilization and higher costs for some existing drugs. (Our 2025 publication on Medi‑Cal prescription drug spending provides more information on recent trends.)

Medicare‑Related Payments Also Contribute to Cost Growth. As Figure 10 shows, Medicare‑related costs also have grown steadily over time—4.8 percent per year for premiums and 5.2 percent for Part D clawback costs. We estimate this growth translates to $1.6 billion General Fund, of which more than half is from the Part D clawback.

Other Key Policy Changes Likely Drove Per‑Enrollee Spending. Under our analysis, about $8 billion of base spending growth—roughly one‑third—remains unaccounted. This remainder is likely explained by major policy changes enacted since 2017‑18, such as the expansions of comprehensive coverage to undocumented adults and the creation of enhanced care management and community supports benefits. Disentangling these policy changes from underlying trends is challenging. Moreover, limited data make it difficult to precisely estimate their fiscal effects.

Governor’s Budget Estimates

Projects Continued Increase in Base Spending. Based on the administration’s budget documentation, we estimate the Governor’s budget reflects an overall General Fund base spending increase of about $3.2 billion (6 percent) in 2026‑27 over the enacted 2025‑26 level. Nearly all of this increase occurs in 2026‑27, with revised 2025‑26 base spending levels only slightly higher than enacted levels.

Caseload Costs Down on Net, Primarily From Decline in Lower‑Cost Populations. We estimate caseload‑related General Fund base spending in 2026‑27 is slightly lower than the enacted 2025‑26 level. This reflects an overall reduction in baseline caseload (excluding the effects of budget solutions and H.R. 1, discussed later) of nearly 300,000 enrollees. The reduction is concentrated among childless adults and families, while seniors and persons with disabilities are projected to increase slightly.

Increase Largely From Per‑Enrollee Cost Growth. Consistent with the projected decline in caseload, we estimate that most of the increase in base spending is due to higher per‑enrollee costs. The assumed rate of growth varies by component. In managed care, the administration projects capitated rate growth of around 6 percent to 7 percent (varying by managed care model). In non‑pharmacy fee‑for‑service, the cost per user is projected to grow by around 4 percent. Net pharmacy spending per Medi‑Cal member (after accounting for drug rebates) is projected to increase by about 12 percent. Based on federal projections, average Medicare premium costs are projected to increase by about 8 percent, and the Part D clawback by 5 percent.

Assessment

Administration’s Estimates Appear Reasonable, but Uncertain

Caseload Projections Are Largely in Line with Recent Trends. To assess the administration’s caseload assumptions, we developed an independent caseload forecast based on recent trends. Our baseline estimates are very similar to the administration’s—nearly identical in 2025‑26, and only slightly lower in 2026‑27 (14 million versus 14.3 million). The difference in 2026‑27 largely stems from our assumption of a somewhat stronger downward trajectory for the family and childless adult caseloads. Given uncertainty about how enrollment will respond to the recent renewal and eligibility changes, the administration’s assumption appears reasonable at this time.

Per‑Enrollee Cost Assumptions Are Generally Consistent With Recent Experience, With Higher Growth in a Few Areas. The administration’s assumed per‑enrollee cost growth for pharmacy and non‑pharmacy fee‑for‑service appears slightly below recent historical trends. By contrast, assumed growth rates appear to exceed historical averages for (1) Medicare premiums (about 3 percentage points higher) and (2) managed care capitation rates (about 2 to 2.5 percentage points higher). Medicare premium growth mostly reflects federal assumptions, whereas managed care rate growth more directly reflects conditions in California. Given substantial uncertainty in the trends, however, the administration’s projections also seem plausible.

Legislature Will Have More Information in May. By the May Revision, additional months of caseload data should allow a clearer read on underlying enrollment trends and the pace of recent disenrollments associated with policy changes. These include not only changes to renewal flexibilities and the asset limit, but also the freeze on new full‑scope enrollment for certain adults with UIS. The May Revision should additionally include updated fee‑for‑service spending estimates including pharmacy, providing more recent data on enrollment, utilization, and cost trends to help evaluate the administration’s assumptions.

Better Data Needed to Assess Base Spending Growth

Data Limitations Significantly Hamper Trend Analysis. Medi‑Cal spending growth can reflect many overlapping factors—such as changes in enrollee and provider behavior, technology, prices, delivery system arrangements, and other policy changes—making it difficult to isolate specific drivers even with detailed data. In practice, however, data are very limited in many cases. For example, information on enrollment and costs for the UIS population remains sparse, even though coverage for this population has significant General Fund implications. Likewise, consistent and recent trend information on managed care capitated rates and pharmacy spending—two of Medi‑Cal’s largest cost drivers—is limited. Without better data, it is difficult to refine estimates of what is driving Medi‑Cal cost growth.

Better Information Would Support Budget Planning. More timely and detailed data would improve transparency and strengthen legislative oversight. The need for better information on Medi‑Cal base spending is particularly important given the state’s fiscal constraints. Without such data, the Legislature faces the challenge of making targeted decisions to slow spending growth without clear information on the fiscal effects, including anticipated savings, of various options.

Recommendations

Withhold Action on Base Spending Until May. Given the uncertainty that remains around both caseload and per‑enrollee costs, the administration’s estimates of base spending generally provide a reasonable basis for preliminary budget planning. At the same time, we recommend the Legislature avoid making final budget decisions on base Medi‑Cal spending assumptions until the May Revision, when additional months of data should provide a clearer picture of caseload and cost trends.

Direct Administration to Provide Richer Data. To strengthen legislative oversight of Medi‑Cal spending growth, we recommend the Legislature direct the administration to provide more recent, granular information for legislative evaluation during each year’s budget process. At a minimum, such information should include: (1) more recent managed care rate trend information; (2) more data on caseload, costs, and utilization for members with UIS; and (3) more detailed pharmacy data on users, utilization, and net unit costs by therapeutic class and drug. Together, these data improvements would help the Legislature better identify the underlying drivers of cost growth and evaluate policy options with greater specificity.

Provider Taxes

In this section, we provide background on provider taxes in Medi‑Cal, summarize assumptions about these taxes in the Governor’s budget, assess these assumptions, and provide our recommendation.

Background

Most States Help Support Medicaid Programs by Taxing Health Care Providers. Provider taxes—also known in federal law as “health care‑related taxes”—are taxes and fees specifically on health care providers that states typically use to help pay for their Medicaid programs. According to Kaiser Family Foundation, all but one state has at least one provider tax, and most have three or more. States most commonly impose taxes on hospitals and long‑term care facilities. Other examples include charges on health plans and ambulance providers, among other areas.

Provider Taxes Typically Draw Down More Federal Funding. Because states typically use provider taxes to support their Medicaid programs, the associated revenue results in federal matching funds. States can use the resulting federal funds to help pay for their existing Medicaid programs or expand them. States also often use their Medicaid programs to pay providers back for some or all of the cost the tax, sometimes even providing them net funding increases through supplemental payments. As a result, much of the net cost of provider taxes tends to fall on the federal government, rather than states or providers.

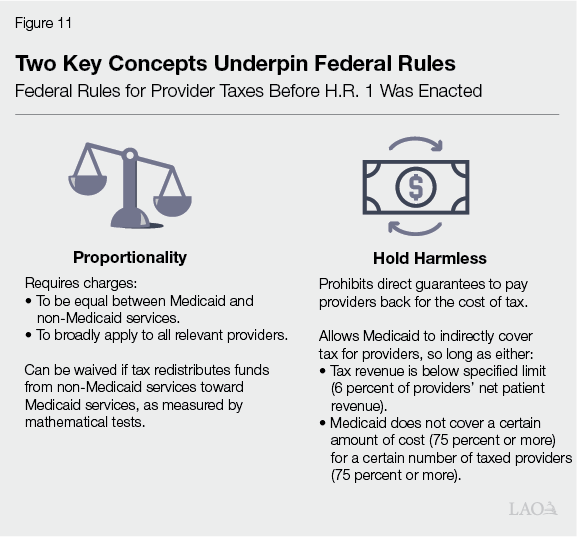

Federal Rules Regulate Provider Taxes. Because provider taxes result in higher costs to the federal government, federal law regulates how states structure their taxes. As Figure 11 shows, the rules generally aim to make the taxes proportionate between Medicaid and non‑Medicaid services and to limit how much funding providers receive back from Medicaid to cover the cost of the taxes. States can receive waivers to the proportionality rules under certain conditions. Waivers are for limited periods of time, often requiring states to periodically renew their federal approval.

California Has Two Large Provider Taxes. As Figure 12 shows, California has four provider taxes or fees that it uses to help support Medi‑Cal. Two of them are particularly large:

- Health Plan Tax. Also known as the “managed care organization tax,” the tax is levied on each health plans’ Medi‑Cal and commercial enrollment. Nearly all of the revenue comes from taxing Medi‑Cal enrollment, as the Medi‑Cal tax rate is more than 100 times larger than the commercial tax. Accordingly, California has needed to request a waiver from federal proportionality rules. The current tax generates between $7 billion and $8 billion in net revenue annually, with most of the funding to date (around 75 percent) offsetting General Fund spending in Medi‑Cal. The smaller remaining share of funding (around 25 percent) supports certain programmatic augmentations, primarily Medi‑Cal provider rate increases. (These estimates net out funds that are redirected back to the health plans to help cover the cost of the tax on Medi‑Cal enrollment. Annual gross revenue is over $12 billion.) Prior to H.R. 1, the current tax, including the waiver from federal proportionality rules, was approved through the end of December 2026.

- Private Hospital Fee. Also known as the “hospital quality assurance fee,” the fee is levied on each private hospital’s inpatient days and outpatient visits. (Public hospitals, such as those owned by counties, are exempt from the fee.) Like the health plan tax, the fee charges higher rates on Medi‑Cal services than on non‑Medi‑Cal services, requiring a waiver from federal proportionality rules. The most recently approved version of the fee was in effect through 2024, generating $5.9 billion in fee revenue in that year. Relative to the health plan tax, a smaller share of revenue (around 25 percent) offsets General Fund spending in Medi‑Cal, with a larger share (75 percent) used for rate increases to private hospitals.

Figure 12

California Has Four Provider Taxes and Fees

|

Tax or Fee |

Charged Providers |

Approximate Annual Revenue |

General Use |

|

Managed Care Organization Tax |

Health plans |

$7.5 billion (net)a |

Increased Medi‑Cal provider rates and General Fund savings. |

|

Hospital Quality Assurance Fee |

Private hospitals |

Over $5 billion |

Supplemental Medi‑Cal payments to private hospitals and General Fund savings. |

|

Long‑Term Care Quality Assurance Fees |

Long‑term care facilities |

$650 million to $700 million |

Portion of state cost of long‑term care facility reimbursement rates. |

|

Ground Emergency Medical Transport (GEMT) Quality Assurance Fee |

Private GEMT providers |

$55 million |

Increased Medi‑Cal payments to private ground emergency transport providers and General Fund savings. |

|

aReflects revenue that is directly available to the state for higher provider rates and General Fund savings. Gross revenue is over $12 billion annually. |

|||

California Recently Pursued Increases to Two Largest Provider Taxes. Federal rules include an overall limit on how much revenue provider taxes can generate. California historically has set its provider taxes and fees well below this revenue limit. In recent years, however, California pursued notably larger taxes, getting much closer to the federal limit. The current health plan tax, enacted in 2023 and expanded in 2024, generates more than three times the revenue of previous versions. This higher revenue level is essentially at the maximum of the current federal revenue limit. In 2025, the state also submitted a one‑year private hospital fee, generating around $11 billion in revenue, for federal approval. The federal government has not yet approved this higher fee.

Voters Have Made Largest Provider Taxes Permanent in State Law. California voters have made the state’s two largest provider taxes permanent in state law. Proposition 52 (2016) made the private hospital fee permanent, while Proposition 35 (2024) made the health plan tax permanent. The two provider taxes are not permanent in federal law, however—periodic federal approval is still required to draw down federal funds. The two measures also include rules around how to structure the taxes and spend their associated revenues. For example, Proposition 35 generally limits the tax rate on commercial enrollment at roughly its current levels.

Federal H.R. 1 Legislation Makes Three Key Changes to Provider Tax Rules. Among other changes, H.R. 1 prohibits states from adopting new provider taxes or increasing their existing ones. The legislation also includes changes to federal approval rules, requiring states, including California, to adjust their existing provider taxes. There are three key changes, described further below:

- Proportionality. H.R. 1 tightens the existing rules around proportionality, generally prohibiting states from charging higher rates on Medicaid services than non‑Medicaid services. This notably limits states’ ability to obtain a waiver from proportionality rules. The new rules are already technically in effect, though the federal Department of Health and Human Services can grant states additional time to comply with the new rules. Initial federal guidance released late last year suggested that California might have to restructure its health plan tax in June 2026, with potentially more time available for other kinds of provider taxes. More recent final guidance released earlier this year, however, suggests California can keep its existing health plan tax in place until its current waiver expires at the end of December 2026.

- Revenue Limit. H.R. 1 gradually reduces the federal revenue limit on provider taxes beginning in federal fiscal year 2028 (roughly corresponding to California’s 2027‑28 fiscal year), until the limit reaches nearly half its current level by federal fiscal year 2032 (roughly corresponding to California’s 2031‑32 fiscal year). The reduction will require states that are near the current revenue limit, like California, to gradually reduce their provider taxes.

- Limit on Directed Payments. H.R. 1 also reduces an existing limit on payments directed to certain providers through Medicaid managed care plans. These payments will now be set at the comparable rate paid by Medicare, rather than the average rate paid by private health plans. This lower limit indirectly affects certain provider taxes, as some states—including California—use their provider taxes to help pay for these directed payments.

Proposal

Assumes Current Version of Health Plan Tax Expires at End of 2026… The Governor’s budget assumes the current structure of the health plan tax remains in effect through the end of December 2026. This assumed timing reflects state law and federal approval prior to H.R. 1.

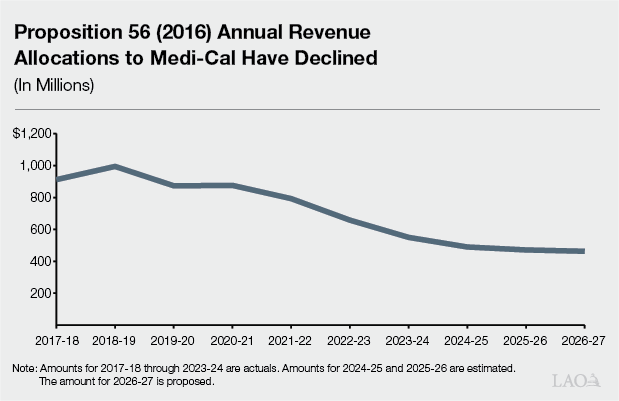

…With a Much Smaller Tax Beginning in 2027. The Governor’s budget assumes there will still be a health plan tax in 2027, but at a much smaller revenue level than before. The administration has not provided detailed information on its assumed new tax, but we understand it would generate net revenue in the mid‑tens of millions of dollars. The smaller tax is due to an interaction with the new H.R. 1 rules and the commercial enrollment tax limits established in Proposition 35.

Adjusts Health Plan Tax Spending Plan. The administration also adjusts its spending plan for a portion of health plan tax funds. Under Proposition 35, the state must spend $300 million each in 2025 and 2026 on behavioral health‑related services. As part of the 2025‑26 budget, the administration developed an initial spending plan focused on data sharing and housing subsidies. Under the new plan in the 2026‑27 budget, much of the funds would instead be spent on certain previously approved Medi‑Cal initiatives, such as transitional rent supports and community‑based mobile crisis services.

Downgrades Planned Increase to Private Hospital Fee. The Governor’s budget assumes the state receives retroactive approval for a private hospital fee for 2025, but that the fee is about equal to its level in 2024, rather than the much larger level originally submitted for approval. The Department of Health Care Services (DHCS) says it based its assumption on recent communication with federal administrators. Most of the decrease in fee revenue would result in fewer supplemental payments to private hospitals. There also will be less revenue available to fund existing service levels in Medi‑Cal, which the administration estimates will cost $652 million General Fund in 2026‑27 to backfill.

Assessment

Administration’s Assumptions Generally Appear Reasonable in Light of Federal Guidance and State Law. Under H.R. 1, California will need to adjust the structure of its health plan tax and private hospital fee. The administration’s assumptions generally appear to reflect the state’s best understanding to date of federal rules and the associated transition periods. Most notably, the administration’s assumed expiration of the existing health plan tax at the end of 2026 appears aligned with the most recent federal guidance.

State Could Contemplate Larger Health Plan Tax Revenues in Short Term. The reduction to the state’s health plan tax revenue is not necessarily required by H.R. 1 in the short term. Rather, the lower revenues are due to the interaction of H.R. 1’s new proportionality rules with Proposition 35’s limit on taxing commercial enrollment. As we noted in our recent report Considering Medi‑Cal in the Midst of the Changing Fiscal and Policy Landscape, the state likely could amend Proposition 35 with a three‑fourths vote in each house, so long as the changes are consistent with the purpose and intent of the measure. Amending the limits in Proposition 35 could allow for a more proportionate, large tax—albeit with potentially higher costs for commercial health plans and their consumers. For example, we estimated that a more proportionate tax netting around $7 billion in revenue could cost around $30 per member, per month—about a 5 percent increase on average to commercial health plan premiums. Aside from this short‑term option, any changes over the long term may need to comply with the gradual reduction to the federal revenue limit, generally beginning 2027‑28.

State’s Options on Private Hospital Fee, by Contrast, May Be More Limited. In concept, similar trade‑offs exist for the private hospital fee—whether to pursue a large fee with higher costs imposed on some private hospitals, or a lower fee with less revenue available for Medi‑Cal. According to DHCS, however, federal administrators have communicated that there are fairly limited options to structure the private hospital fee in 2025 (see the nearby box). Given these limited options, the administration’s assumptions around the private hospital fee appear to be reasonable.

What Have Federal Administrators Indicated About the Private Hospital Fee in 2025?

According to the Department of Health Care Services (DHCS), federal administrators have requested changes to the state’s submitted fee for 2025. This is because the submitted 2025 fee is much larger than the 2024 version, and H.R. 1 prohibits states from increasing their existing provider taxes. (The 2025 fee was submitted for approval in March 2025, a few months prior to Congress enacting H.R. 1, but it has not yet been approved.) DHCS also states that complying with this federal request may qualify California for an up to three‑year transition period to make the fee more proportionate.

Federal Rules Continue to Emerge, Creating Some Uncertainty for Structuring Provider Taxes. H.R. 1 grants the federal Department of Health and Human Services a fair amount of flexibility to implement its new provider tax rules and provide transition periods for states. As such, the state’s understanding of the new federal rules, as well as when conforming changes will need to happen, is evolving. While some key rules appear to have been finalized, continued caution likely is warranted when exploring different approaches to restructure the health plan tax, the private hospital fee, or other provider taxes.

Recommendation

Treat Administration’s Assumptions as Starting Point, but Begin Considering Other Approaches for Health Plan Tax. In light of what is known to date about the new federal rules, we recommend the Legislature treat the administration’s assumptions around the health plan tax and private hospital fee as a reasonable starting point. That said, given the magnitude of the fiscal challenges facing the state, we also recommend the Legislature begin weighing the merits and trade‑offs of pursuing a larger health plan tax. In considering these trade‑offs, the Legislature likely will want to weigh the additional revenue generated against the higher cost to commercial health plans and their consumers. The Legislature also will want to keep in mind the changes in the revenue limit, which may constrain the state’s ability to rely on these taxes in the coming years.

H.R. 1 Implementation

Background

H.R. 1 Will Affect Medi‑Cal Beyond Provider Taxes. In addition to affecting how states can finance Medicaid through provider taxes, H.R. 1 introduces several changes to Medi‑Cal eligibility and enrollment rules that will affect caseload and administrative workload beginning in 2026‑27. This section focuses on (1) new community engagement requirements, (2) the new six‑month renewal requirement, and (3) changes that eliminate federally funded full‑scope (comprehensive) Medi‑Cal coverage for certain immigrant groups. (Our 2025 report, Considering Medi‑Cal in the Midst of a Changing Fiscal and Policy Landscape, provides more information on other H.R. 1 changes.)

Community Engagement Requirements Increase Risk of Coverage Loss Among Certain Adults. Beginning January 1, 2027, H.R.1 requires states to implement a community engagement requirement for certain able‑bodied adults between ages 19 and 64 (mostly childless adults). Individuals must generally work, study, or volunteer at least 80 hours per month, or meet an earnings threshold (about $580 per month, equivalent to 80 hours at the federal minimum wage) unless they qualify for certain exemptions (such as having young children or being medically frail). While states are expected to use available administrative data to determine compliance and exemptions, otherwise eligible individuals could lose coverage if they fail to document or report required information.

Six‑Month Renewals Are Expected to Further Increase Disenrollment. H.R. 1 also requires eligibility to be redetermined every six months rather than every year (as currently is the case) for many nonelderly childless adults beginning January 1, 2027. More frequent renewals will likely increase the risk of disenrollment even among otherwise eligible individuals, due to the increased frequency of needing to submit required documentation. Like community engagement requirements, more frequent renewals are also expected to increase administrative workload for county eligibility systems, at least in the short run.

Federal Changes for Certain Immigrant Groups Create State Fiscal Pressure. Beginning October 1, 2026, H.R. 1 eliminates federal funding for full‑scope Medicaid coverage among certain lawfully present immigrants, such as refugees, asylees, and battered noncitizens. Affected individuals generally remain eligible for federally funded emergency and pregnancy‑related services. In addition, lawfully residing individuals who are pregnant or under age 21 can retain eligibility for federally funded full‑scope Medi‑Cal coverage through the state option under the Children’s Health Insurance Program Reauthorization Act.

Governor’s Budget

Projects Disenrollment Due to Community Engagement Requirements and Six‑Month Renewals. The administration estimates the community engagement requirement would result in about 233,000 fewer enrollees by June 2027 and reduce General Fund spending by $102 million in 2026‑27. The caseload estimate is developed by identifying current enrollees subject to the requirement, removing those expected to be exempt or compliant, and then assuming that half of those remaining would be disenrolled due to noncompliance. The administration has indicated that it is still refining exemption estimates for certain categories that are not currently reflected in the disenrollment total (such as medical frailty), and therefore the projected disenrollment may be adjusted downward in the future. Beyond the budget year, the administration estimates that total coverage losses could reach about 1.4 million by June 2028. Separately, the administration estimates that the new six‑month renewal requirement would result in about 289,000 fewer enrollees by June 2027 and lower General Fund spending by about $74 million in 2026‑27, with total coverage losses reaching about 400,000 by June 2028. All of these estimates incorporate the administration’s proposal to apply the community engagement and renewal requirements to adults regardless of their immigration status (as discussed later).

Administration Identifies Several Strategies to Mitigate Disenrollment Impacts. The administration has indicated it will prioritize using administrative data to automatically identify individuals who are excluded or exempt from the community engagement requirement. For example, the administration proposes using multiple data sources—including state wage records, Internal Revenue Service data, and third‑party employment and income data (such as Equifax’s The Work Number)—to verify income and work activity, and using diagnosis or utilization information to help identify medically frail individuals. The administration also plans to apply optional exemptions for short‑term hardship that are allowed under federal law, such as residing in high‑unemployment counties. Finally, federal guidance provides states discretion in setting the number of months over which enrollees are required to document compliance with qualifying activities (such as working 80 hours per month) at application and renewal. To mitigate disenrollment impacts of the H.R. 1 requirements, the administration generally plans to require enrollees to demonstrate a single month of qualifying activities at application and renewal.

Administration Proposes to Extend Community Engagement Requirements and Six‑Month Renewals to Adults With Unsatisfactory Immigration Status (UIS). Although H.R. 1 does not require states to apply the community engagement requirement and six‑month renewals to adults with UIS (whose Medi‑Cal full scope coverage is entirely state‑funded), the administration proposes to do so. The administration’s stated rationale is to “maintain parity” across the nonelderly, childless adults who are receiving full‑scope Medi‑Cal benefits. At the same time, the administration has stated that verifying compliance for UIS adults using existing income data sources may be more challenging and that it would rely on information provided by the individual when available data are insufficient. The administration has not provided a clear estimate of the disenrollment or General Fund savings attributable to this proposal.

Administration Also Proposes to Move Newly UIS Immigrant Groups to Restricted‑Scope Medi‑Cal. Beginning October 1, 2026, the administration proposes to transition the immigrant groups losing eligibility for federally funded full‑scope Medi‑Cal under H.R. 1—such as refugees, asylees, and battered noncitizens—from full‑scope coverage to restricted‑scope coverage. The administration estimates this would affect about 200,000 Medi‑Cal enrollees and reduce General Fund spending by about $786 million in 2026‑27 and $1.1 billion in subsequent years. The savings would be a result of not backfilling the loss of federal funding to maintain full‑scope benefits for this population.

Assessment

Budget Estimates of H.R. 1 Caseload Impacts

Administration’s Estimates Appear Reasonable. Overall, the administration’s estimates of caseload impacts from the community engagement requirement and six‑month renewals appear reasonable. Using survey and administrative data together with available literature, we developed an independent estimate and found a similar share of already‑enrolled nonelderly, childless adults could disenroll due to the community engagement requirement (about 26 percent, compared to the administration’s estimate of about 30 percent). Looking at the combined effects of the two policy changes over time, we estimate total coverage losses could reach about 2.1 million by June 2028, compared to the administration’s estimate of about 1.8 million. One possible reason for our higher estimate is that our model reflects not only disenrollment among current enrollees, but also reduced enrollment flows over time and a persistent risk of disenrollment among eligible individuals due to added administrative burden.

Significant Uncertainty Remains Around the Magnitude and Pace of Caseload Impacts. Though our estimates are broadly comparable to the administration’s, the magnitude and pace of caseload changes remain uncertain and likely will depend on behavioral responses and implementation choices. Key drivers include how burdensome beneficiaries find the new reporting and documentation requirements, the extent to which the administration can leverage existing data sources for automated determinations, and the readiness of county eligibility systems to implement new processes in a clear and consistent manner. Pending federal guidance on issues such as definitions of specific exemptions (for example, medical frailty), acceptable verification methods, and self‑attestation standards could also materially affect the number of individuals who receive exemptions or who lose coverage for procedural reasons. Finally, the timing of caseload reductions is also uncertain and has important implications for the budget year. Our estimate of total coverage losses by June 2027 is higher than the administration’s by about 280,000, largely because we assume most disenrollment among existing enrollees would occur within roughly 12 months of implementation rather than 18 months.

Governor’s Policy Choices Affecting UIS Population

UIS‑Related Proposals Come Amid a Challenging Fiscal Backdrop, but Some Fiscal Effects Remain Unclear. The proposals to extend the H.R. 1 requirements to adults with UIS and to transition newly UIS groups to restricted‑scope coverage are policy choices. At the same time, these proposals come in the context of the state’s projected structural budget deficits. As such, the administration’s view that backfilling the loss of federal funding for the newly UIS groups would be fiscally difficult is understandable. When it comes to the existing UIS population, however, the administration has not provided a breakout estimate for the caseload and General Fund impacts of extending the H.R. 1 requirements to this group. As a result, the Legislature lacks a complete picture of how much savings these policy choices would generate. It is also unclear to what extent these savings may be reduced by costs associated with increased administrative workload on county eligibility systems.

Governor’s Discretionary Proposals Involve Access‑Related Trade‑Offs… Both discretionary proposals achieve savings largely by reducing enrollment in full‑scope Medi‑Cal coverage, which could reduce access to care for affected individuals. Newly UIS individuals also will lose access to Covered California premium tax credits starting January 2027, limiting affordable options for those who lose Medi‑Cal coverage. Some of the newly UIS groups include refugees and certain victims of human trafficking or domestic violence, who may have relatively acute health care needs.

…And Raise Other Issues. Beyond the access‑related implications noted above, the discretionary proposals could also affect different groups in different ways, raising equity considerations and potentially introducing additional complexity for beneficiaries and county eligibility systems. We discuss these issues below.

Extending H.R. 1 Requirements to UIS Adults Could Have Different Practical Effects. The administration’s proposal seems intended to apply a consistent set of requirements across nonelderly adults, regardless of immigration status. In practice, though, adults with satisfactory and unsatisfactory immigration status may experience the requirements differently. Some UIS adults face legal barriers to employment, which can narrow the set of pathways to meet the community engagement requirement. In addition, certain UIS adults who lose full‑scope coverage for noncompliance could have more limited options to regain coverage, given the state’s freeze on new full‑scope enrollment for groups like undocumented adults. At the same time, UIS adults who cannot satisfy community engagement requirements may generally remain eligible for restricted‑scope Medi‑Cal coverage, an option not available to adults with satisfactory immigration status.

Transitioning Newly UIS Groups to Restricted‑Scope Coverage Would Create a Patchwork of Full‑Scope Eligibility. Under the administration’s proposal, newly UIS adults such as refugees, asylees, and battered noncitizens would be shifted to restricted‑scope Medi‑Cal coverage, while other UIS adults such as undocumented individuals and some with interim or pending statuses would continue to qualify for full‑scope Medi‑Cal coverage (barring the enrollment freeze for new undocumented individuals). As a result, eligibility for full‑scope benefits could differ across relatively similar groups and, in some cases, change based on a person’s immigration status. For example, an individual with a pending asylum application may remain eligible for full‑scope coverage but could lose that eligibility if approval results in being classified as an asylee subject to the restricted‑scope transition. This interaction could be difficult to navigate for beneficiaries and complicate administration of the program, especially given that existing policies (such as the full‑scope enrollment freeze and premium requirements) already apply differently across immigrant groups.

Legislature May Wish to Consider Whether Alternative Approaches Could Better Balance Savings, Consistency, and Access. Given the trade‑offs described above, the Legislature may want to take time to consider any proposed Medi‑Cal changes alongside alternative ways of achieving budgetary savings. Even under the premise that budgetary actions should focus on UIS populations whose coverage does not draw federal funding, other approaches may be available. For example, the income threshold for state‑funded full‑scope coverage could be reduced to better target higher‑need populations while applying a more consistent rule across immigrant groups. Another option could be to adopt a modified state‑funded benefit package that is more comprehensive than restricted‑scope (such as certain primary care, outpatient services, and generic drugs) but less comprehensive than full‑scope coverage. Exploring alternatives could help identify options that achieve savings more efficiently, apply more consistently across groups, and preserve access to high‑priority services.

Oversight and Development of Budget Solutions

In this section, we first provide an update on the package of Medi‑Cal budget solutions enacted in the 2025‑26 budget and assess the status of those enacted solutions. We then discuss the levers available to the Legislature to further contain future cost growth in the Medi‑Cal budget (and the trade‑offs those solutions may entail) in an overall effort to help address the state’s projected structural deficits. (Separately, in the “H.R.1 Implementation” section of this brief, we discuss the Governor’s proposals that we consider to be of a budget solution nature.)

Update on 2025‑26 Solutions

Background

Medi‑Cal Expenditures Greater Than Anticipated Last Year. The 2025‑26 Medi‑Cal budget changed significantly over the course of the budget development process due to higher‑than‑anticipated costs in the Medi‑Cal program as well as the state’s worsening fiscal condition. In April 2025, the Legislature took early action to provide cash flow support and supplemental appropriations to Medi‑Cal in 2024‑25. The administration stated that increasing Medi‑Cal costs were due to several factors, including increased utilization of high‑cost anti‑obesity drugs, increased enrollment of seniors and persons with disabilities following the elimination of the state’s asset test, and the higher than anticipated costs associated with the state’s expansion of full‑scope Medi‑Cal coverage to all individuals regardless of immigration status. While the administration did not propose any significant solutions in Medi‑Cal as part of the Governor’s January budget last year, the Governor’s May Revision proposed several new solutions totaling nearly $5 billion General Fund in response to higher cost estimates. Medi‑Cal’s share of General Fund expenditures was increasing, contributing to the budget problem that had emerged between the Governor’s budget and May Revision.

2025‑26 Enacted Budget Included Several Solutions in Medi‑Cal Program. The Legislature ultimately adopted, revised, or rejected budget solutions that had been proposed by the Governor. We discuss the enacted solutions in detail in The 2025‑26 California Spending Plan: Health. The majority of solutions focused on limiting coverage for individuals with UIS. Other solutions included partially restoring the asset test for seniors and persons with disabilities, ending coverage of anti‑obesity drugs, and ending supplemental payments for dental services in Medi‑Cal. In June, the ongoing reductions associated with these solutions was estimated to be nearly $9 billion when fully implemented by 2028‑29.

Governor’s Proposal Reflects Updated Savings Estimates

Updated Estimates. As shown in Figure 13, the Governor’s proposed budget updates the estimated savings for several budget solutions enacted in the 2025‑26 Budget Act. The total savings across all budget solutions is lower, with a $400 million reduction in savings in 2025‑26 and a $200 million net reduction in 2026‑27. The savings reductions are concentrated in a few solutions, with lower estimated savings from newly collected drug rebates (a $400 million total reduction in savings across 2025‑26 and 2026‑27) and the end of coverage for most adult dental services for individuals with UIS (a $170 million reduction in savings in 2026‑27). The Governor’s budget also reflects a few upward adjustments in savings estimates which include increased savings from the end of coverage for anti‑obesity drugs, asset limit reinstatement, and a one‑year acceleration of assumed savings from a third‑party contract intended to achieve operational efficiencies. We discuss this last item below.

Figure 13

Estimated Savings From Budget Solutions Enacted Last Year

(In Millions)

|

2025‑26 |

2026‑27 |

||||||

|

2025 Budget Act |

Governor’s Budget (January 2026) |

Difference |

2025 Budget Act |

Governor’s Budget (January 2026) |

Difference |

||

|

Medi‑Cal Financing |

|||||||

|

Medi‑Cal loan repayment delay |

$1,291 |

$1,291 |

— |

— |

— |

— |

|

|

Proposition 35 support of program growth |

1,289 |

1,214 |

‑$75 |

$264 |

$339 |

$75 |

|

|

Additional Medi‑Cal loan |

1,000 |

1,000 |

— |

— |

— |

— |

|

|

BHSF offset |

100 |

100 |

— |

— |

— |

— |

|

|

Adults With Unsatisfactory Immigration Status |

|||||||

|

Enrollment freeze and premiums |

$78 |

$55 |

‑$23 |

$713 |

$715 |

$2 |

|

|

Clinic finance changes |

— |

— |

— |

1,037 |

1,011 |

‑26 |

|

|

End of adult dental coverage |

— |

— |

— |

308 |

135 |

‑173 |

|

|

Prescription Drugs |

|||||||

|

New aggregator to increase rebates |

$370 |

$123 |

‑$247 |

$600 |

$435 |

‑$165 |

|

|

End of anti‑obesity coverage |

85 |

86 |

1 |

215 |

364 |

149 |

|

|

Prescription Drug Utilization Management |

25 |

19 |

‑6 |

50 |

41 |

‑9 |

|

|

Pharmacy step therapy protocols |

88 |

66 |

‑22 |

175 |

145 |

‑30 |

|

|

HIV/Cancer drug rebates |

75 |

— |

‑75 |

150 |

150 |

— |

|

|

Prior authorization for continuation of drug therapy |

63 |

47 |

‑16 |

125 |

104 |

‑21 |

|

|

End of over‑the‑counter drug coverage |

3 |

2 |

‑1 |

6 |

5 |

‑1 |

|

|

Other |

|||||||

|

Asset limit reinstatement |

$45 |

$47 |

$2 |

$343 |

$349 |

$7 |

|

|

Operational efficiencies |

— |

— |

— |

— |

120 |

120 |

|

|

PACE capitation rate limit |

— |

— |

— |

13 |

13 |

— |

|

|

Long‑term care directed payment elimination |

70 |

70 |

— |

140 |

140 |

— |

|

|

Skilled nursing facility back‑up power requirement suspension |

98 |

98 |

— |

140 |

140 |

— |

|

|

End of dental supplemental payments |

— |

— |

— |

362 |

311 |

‑51 |

|

|

Prior authorization for hospice services |

— |

— |

— |

50 |

50 |

— |

|

|

Reduction to Proposition 56 Loan Repayment Program |

26 |

26 |

— |

— |

— |

— |

|

|

Totals |

$4,706 |

$4,245 |

‑$461 |

$4,690 |

$4,567 |

‑$123 |

|

|

BHSF = Behavioral Health Services Fund and PACE = Program of All‑inclusive Care for the Elderly. |

|||||||

Almost Half of Savings From Enacted Budget Solutions Focused on Adults With UIS. Over the past several years, the state has expanded access to comprehensive Medi‑Cal coverage to all individuals regardless of immigration status, but the actual costs of this expansion have significantly exceeded original estimates. In light of the state’s budget deficit and to address growing costs in Medi‑Cal, the Legislature enacted several budget solutions. After updates in the Governor’s proposed budget, these solutions total $55 million in 2025‑26 and $1.9 billion in 2026‑27. These savings are estimated to grow to nearly $5.5 billion by 2028‑29. The solutions include a freeze on undocumented adults enrolling in full‑scope Medi‑Cal, a $30 monthly premium for undocumented individuals who remain in full‑scope coverage after the freeze, a reduction in payments to safety net clinics for services provided to individuals with UIS, and elimination of most dental coverage for UIS adults.

Solutions Related to Prescription Drugs Have Lower Estimated Savings in 2025‑26. The Legislature also enacted solutions targeted at reducing increasing pharmacy expenditures in Medi‑Cal and generating additional drug rebates. The Governor’s 2026‑27 proposal estimates around $350 million in savings in 2025‑26 (only half of the savings estimated at the time of the enacted budget in June 2025) and about $1.2 billion in 2026‑27. Nearly one‑third of the savings are based on the state negotiating rebates with drug manufacturers for drugs provided to UIS members (a population that has not previously received rebates). The Legislature also ended coverage for certain drugs, with most savings resulting from the end of coverage for drugs used to treat obesity.

Governor’s Proposed Budget Assumes Additional Savings From Operational Efficiencies in 2026‑27. The administration is currently contracted with third party to develop a number of recommendations across three departments (including DHCS) to improve department operations and realize savings from operational efficiencies. The potential workstreams associated with DHCS include strengthened oversight over managed care organizations, enhanced fraud and improper claims detection, and improved hospital payment methodologies. While at budget enactment savings from these operational efficiencies were not anticipated to begin until 2027‑28, the Governor’s proposed budget includes an additional $120 million in General Fund savings in 2026‑27 for this item. (The estimated savings in 2027‑28 and 2028‑29 have been revised downward to $435 million in each year.)

Assessment of Updated Savings Estimates

Most Updated Estimates Appear Reasonable, Though Uncertainties Remain. While we find most of the administration’s updated savings estimates generally to be reasonable, many of the largest enacted budget solutions carry significant uncertainty. This is due to unknown behavioral responses among affected parties, potential administrative implementation challenges, and interactions with other policies. The rest of this section highlights some of the solutions for which the Legislature may consider closer oversight to track implementation and ultimate budget savings.

Savings From Enrollment Freeze and Premiums for UIS Adults Are Inherently Uncertain. The amount of savings from the enrollment freeze depends on the extent to which what would otherwise be new enrollment is limited (this is hard to predict). The amount of savings from the premiums depends on the extent to which the premiums cause disenrollment (which is a hard‑to‑predict behavioral response). It is possible that the healthiest individuals are more likely to disenroll, which could reduce the savings realized. Accordingly, estimating these savings is inherently uncertain, confounded by the fact that full implementation of these budget solutions is several years out. As disenrollment and new enrollment data become available, the state may need to significantly revise the cost savings from the solutions.