May 4, 2026

How Will the Changing Landscape Affect

California’s Health Care System?

- Introduction

- Background

- Effects of Changing Landscape

- Issues to Consider

- Conclusion

- Works Referenced in Report

Executive Summary

Overview

The Health Policy Landscape Is Changing. Over the past decade, federal and state policy changes have expanded access to health care in California. This policy landscape is changing, however. In June 2025, the Legislature enacted numerous state budget solutions in Medi‑Cal, California’s Medicaid program, to help address the state budget’s structural deficit and control rising programmatic costs. Then in July 2025, Congress enacted H.R. 1, which makes additional changes to Medicaid and the health insurance marketplace. Both sets of changes likely will have notable effects on access to health care and the state’s health care system.

Report Analyzes Projected Effects on California’s Health Care System. This report builds on previous Medi‑Cal‑focused analyses by assessing the changing landscape for the broader health care system. Our analysis is subject to considerable uncertainty, however. As such, it should be treated as preliminary. Actual effects could be quite different from our projections. Moreover, our analysis focuses on what we understand to be the largest effects, but is not comprehensive in addressing every effect or policy change.

Effects of Changing Landscape

More Californians Will Become Uninsured. Currently, around 2 million Californians (5 percent of the state) do not have health insurance. We project this amount to roughly double by 2030. Most of the increase in the uninsured population (nearly 90 percent) will be due to eligibility changes under H.R. 1, most notably from community engagement requirements. We project the remainder of the increase to come from people leaving Covered California coverage due to a series of federal policy changes. We also project that another 1.3 million adults with unsatisfactory immigration status (UIS)—mostly undocumented immigrants—will leave comprehensive coverage in Medi‑Cal due to several state policy changes. Our projections assume that people in this latter group remain enrolled in Medi‑Cal, but only with emergency coverage.

Hospitals and Clinics Likely Will Face Tighter Finances. The increase in the uninsured population will place greater financial pressures on hospitals and clinics. This is because many providers will still provide some care to these populations without receiving reimbursement, also known as uncompensated care. We project the aggregate cost increase in uncompensated care for hospitals and clinics could be at least a few billion dollars by 2030. Coverage reductions for adults with UIS and upcoming Medi‑Cal reimbursement reductions could add to these effects, but the magnitude is difficult to predict due to limited data. These impacts likely will have bigger impacts on certain kinds of providers, such as safety‑net hospitals and clinics.

Some Private Health Insurance Premiums Could Increase at Faster Rates. Departures from Covered California are also expected to drive up average premiums in the individual health insurance marketplace. The reason is that healthier enrollees are more likely to leave coverage, leaving behind a higher‑risk pool for insurance plans. Initial data suggest this effect explains around one‑fifth of the growth in gross premiums in 2026, though longer‑term effects in future years are uncertain. Effects on employer‑sponsored health insurance premiums are more uncertain and largely depend on the health acuity of new enrollees.

Counties Face Increasing Cost Pressures. State law tasks counties with providing basic health care to low‑income uninsured residents. In practice, county indigent health programs have served as a last resort of care for the uninsured. Caseloads in these programs have notably declined over the last decade, due to various expansions in Medicaid and marketplace insurance coverage. As the uninsured population rises in the coming years, however, counties likely will experience additional demand for services and greater cost pressures. Pinpointing these costs is challenging, as counties have flexibility to determine program eligibility and benefits. That said, we estimate that costs to provide county services to an increased population could be as high as the low billions of dollars annually (including some uncompensated care for county hospitals).

Issues to Consider

In Short Term, Enhance Oversight and Consider Targeted Responses. The magnitude of the effects we describe is uncertain. Moreover, the state’s fiscal situation is notably constrained due to projected structural deficits. Given these issues, we recommend the Legislature focus in the short term on bolstering its oversight over hospitals, clinics, and county programs as the nature and extent of the impacts from forthcoming policy changes come into clearer focus. This oversight could include more systematically tracking caseloads and fiscal conditions of affected entities. The Legislature also could explore providing limited‑term, targeted assistance for entities particularly at risk of near‑term financial distress.

In Long Term, Weigh Trade‑Offs of More Structural Changes. With more information available over time, the Legislature could explore structural policy changes to adjust to the new health financing landscape. For example, the Legislature could revisit its existing expectations of providers and counties, either by tightening requirements to ensure more consistent service delivery statewide, or by loosening requirements to allow more flexibility to manage costs. The Legislature also could revisit long‑term financing approaches, such as its funding approach for county indigent health programs, to better reflect the new landscape.

Transition Could Be Challenging, but Not Unprecedented. Health care consumers, providers, and payors in California will face heightened fiscal constraints as a result of the changing fiscal and policy landscape. The circumstances of these constraints are not unprecedented, however—much of the new landscape likely will resemble conditions that existed more than a decade ago. This is because these changes unwind some eligibility and financing changes that occurred after state implementation of federal health policy reforms in 2014. Moreover, from an access standpoint, the state will still be in a better position than before 2014, with key reforms (such as the Covered California marketplace) still intact. Keeping this broader context in mind, the Legislature, administration, providers, and counties likely will need to work collaboratively to adjust policies, financing structures, and services to align with the new landscape and fiscal realities.

Introduction

The fiscal and policy landscape is changing for health care in California. In our previous 2025 report, Considering Medi‑Cal in the Midst of a Changing Fiscal and Policy Landscape, we described how this new landscape could affect Medi‑Cal, California’s Medicaid program. Our follow‑up budget briefs more specifically projected the associated costs in Medi‑Cal and analyzed the implications for county administrative costs. In recent months, members of the Legislature have expressed interest in understanding the implications of this new landscape for the state’s broader health care system, including on health care coverage, providers, and county health programs. This report aims to provide this broader analysis.

Projecting the impacts on the state’s health care system is challenging for two key reasons. First, the state’s health care system is complex, involving different kinds of services, consumers, providers, and payors. Second, several key forthcoming policy changes are largely new to California, making the magnitude of their effects difficult to predict. With so much uncertainty, our analysis should be treated as preliminary, with actual effects potentially being quite different from our projections. Moreover, our analysis focuses on what we understand to be the largest effects, but is not comprehensive in addressing every effect or policy change.

We first provide background on California’s health care system and the changing landscape. Next, we analyze the changes’ potential effects on California’s health care system—health care coverage, hospitals and clinics, private insurance, and counties. We conclude with key issues for the Legislature to consider.

Background

Below, we provide background on California’s health care system and the changing landscape.

California’s Health Care System

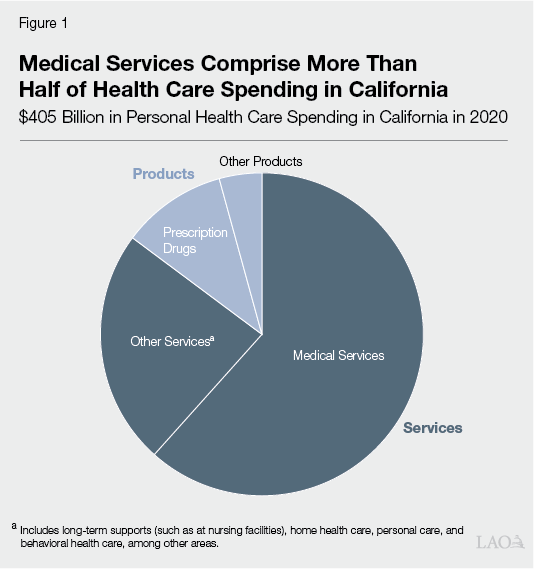

Californians Access Numerous Kinds of Health Care Services. Health care consists of products and services that aim to improve people’s health, including by treating illnesses and other ailments. As Figure 1 shows, medical care provided at doctor’s offices, hospitals, and clinics comprised more than half of personal health care spending in California in 2020 (the most recent year available). Other services include long‑term supports (such as at nursing facilities), home health care, personal care, and behavioral health care. Health care in aggregate comprises around 15 percent of California’s economy.

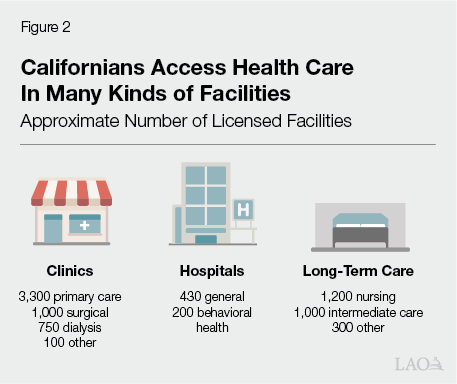

Health Care Is Mostly Provided in Privately Owned Facilities. A likely sizable portion of health care services occurs in doctor’s offices or at people’s homes. The remainder generally occurs at licensed health care facilities. As Figure 2 shows, there are numerous kinds of licensed facilities, including clinics, hospitals, and long‑term care facilities. While many health care providers are employed by private entities and practice in privately owned facilities, there are some publicly owned entities. For example, California has a handful of public hospitals owned by the University of California, counties, and special health care districts.

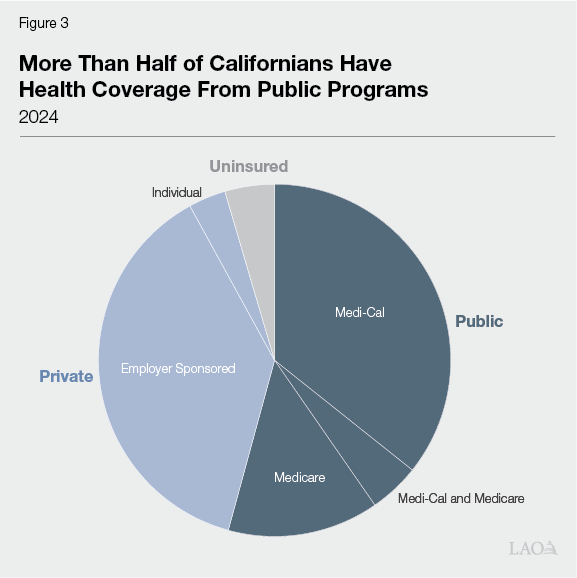

Public Programs Provide a Larger Share of Health Care Coverage. Most health care consumers in California do not directly pay for the full cost of services at the point of care. Instead, most people in the state have health coverage that helps pay for services. As Figure 3 shows, more than half of Californians obtain coverage through public sources. Most of the remainder have health insurance through their employer or purchase it themselves. Federal, state, and local governments promote health coverage in five key ways:

- Medi‑Cal. Medi‑Cal, California’s Medicaid program, covers health care services for low‑income people. Like other state Medicaid programs, Medi‑Cal is jointly administered and funded by federal, state, and local governments. It is the single largest source of coverage in the state, with around 15 million enrollees, or over one‑third of all Californians.

- Medicare. Medicare is a federal program that covers health care for seniors and persons with disabilities. It is generally funded through a mix of payroll taxes, premiums, and direct federal support. Around 7 million Californians (around 20 percent) are enrolled in Medicare. This includes 1.5 million low‑income seniors and persons with disabilities enrolled in both Medi‑Cal and Medicare (also known as dual eligibles). For these dually enrolled people, Medicare is the first payor of certain services, with Medi‑Cal covering remaining costs.

- Covered California. Covered California—established pursuant to the federal Patient Protection and Affordable Care Act (ACA)—is the marketplace that enables individuals to purchase health coverage from various private insurers. Consumers can choose from a range of lower‑ and higher‑cost plans. Certain lower‑income consumers may also be eligible to receive federal and/or state subsidies that reduce their costs.

- Private Health Insurance Mandates. California and federal law place several requirements around accessing private health insurance. For example, federal law requires large employers to offer insurance to their employees. State law also requires individuals to have health coverage or face tax penalties. Moreover, federal and state law includes numerous requirements on health plans to offer certain services and meet certain standards.

- County Indigent Health Programs. Longstanding state law tasks counties with providing health care to low‑income, uninsured people. Counties do so by operating indigent health programs. In practice, these programs are a place of last resort for low‑income, uninsured people to access basic coverage. State law grants counties flexibility to determine eligibility rules, benefits, and cost‑sharing requirements. Counties also vary in the way they deliver services; some contract with providers while others operate their own hospitals and clinics. Most rural counties participate in a consolidated program called the County Medical Services Program, which provides health care services to enrolled individuals in member counties.

The Changing Landscape

Over the Last Decade, Health Care Coverage and Benefits Have Expanded. Prior to recently enacted changes, federal and state health policy focused on expanding coverage and services. Figure 4 shows the main changes. One key driver of the growth in coverage was state implementation of the ACA—federal legislation focused on expanding Medicaid and private coverage. Though many key portions of the ACA became optional due to court rulings, California elected to implement the optional provisions. The Legislature also enacted several expansions at the state level, most notably by extending comprehensive Medi‑Cal coverage to undocumented people.

Figure 4

Federal and State Actions Have Expanded Health Care in California

Key Federal and State Actions Over the Last Decade, Prior to 2025

|

Federal Actions |

|

Patient Protection and Affordable Care Act |

|

|

Other Key Changes |

|

|

State Actions |

|

Medi‑Cal Eligibility |

|

|

Other Key Changes |

|

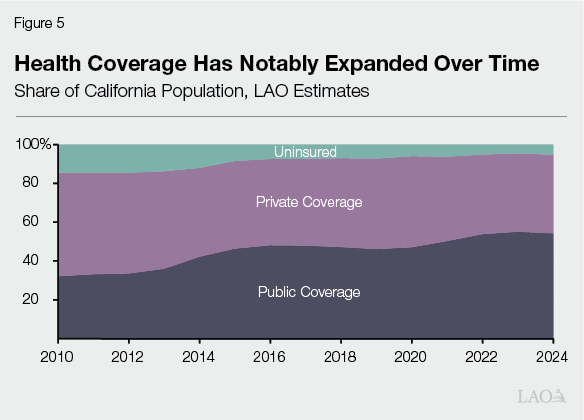

Expansions Notably Reduced Uninsured Rate. As Figure 5 shows, health coverage has expanded over the last several years, mostly in public programs. As a result of this expansion, the state’s uninsured rate (the percent of the population without health insurance) fell from over 14 percent in 2012 to around 7 percent by 2016. The rate has continued to decline over time, reaching around 5 percent by 2024. Three key factors were largely behind this coverage expansion, described below:

- Medi‑Cal Coverage for Childless Adults. As part of the ACA, the state expanded Medi‑Cal eligibility to income‑eligible childless adults (as well as some higher‑income parents). This population today consists of around 5 million people. Federal funding covers most of the cost (90 percent) of this expansion, a much larger share of federal cost than for most populations (50 percent).

- Private Insurance Expansions. State policymaking under the ACA created several other policies to expand private insurance coverage. These included the creation of the Covered California marketplace, coverage mandates for employers and individuals, and prohibitions around denying coverage for preexisting conditions.

- Comprehensive Medi‑Cal Coverage for Undocumented Immigrants. Undocumented immigrants have long been technically eligible for Medi‑Cal, but only for emergency care (including visits to the emergency room, pregnancy‑related care, and long‑term care). The state expanded these populations’ eligibility for comprehensive Medi‑Cal coverage in phases.

Medi‑Cal caseload also has been at temporarily elevated levels in recent years due to limited‑term, pandemic‑related policies. Many of these policies have since ended, with overall caseload expected to decline over time.

Since These Expansions, California’s Budget Situation Has Tightened… Over the past three years, the state has solved $125 billion in budget deficits. Moreover, as we have noted in previous publications, the state budget is projected to face sizable structural budget deficits starting in 2027‑28. At the same time, Medi‑Cal spending has grown somewhat faster than the rest of the state budget in recent years, with a particularly larger‑than‑expected increase in 2025‑26.

…Resulting in the Legislature Enacting Several Reductions in Medi‑Cal in June 2025. With the state’s fiscal situation tightening and Medi‑Cal costs rising, the Legislature enacted several budget solutions in Medi‑Cal as part of the 2025‑26 budget. Some solutions partially overturned recent state expansions. Most of these solutions are ongoing, with savings expected to ramp up over time.

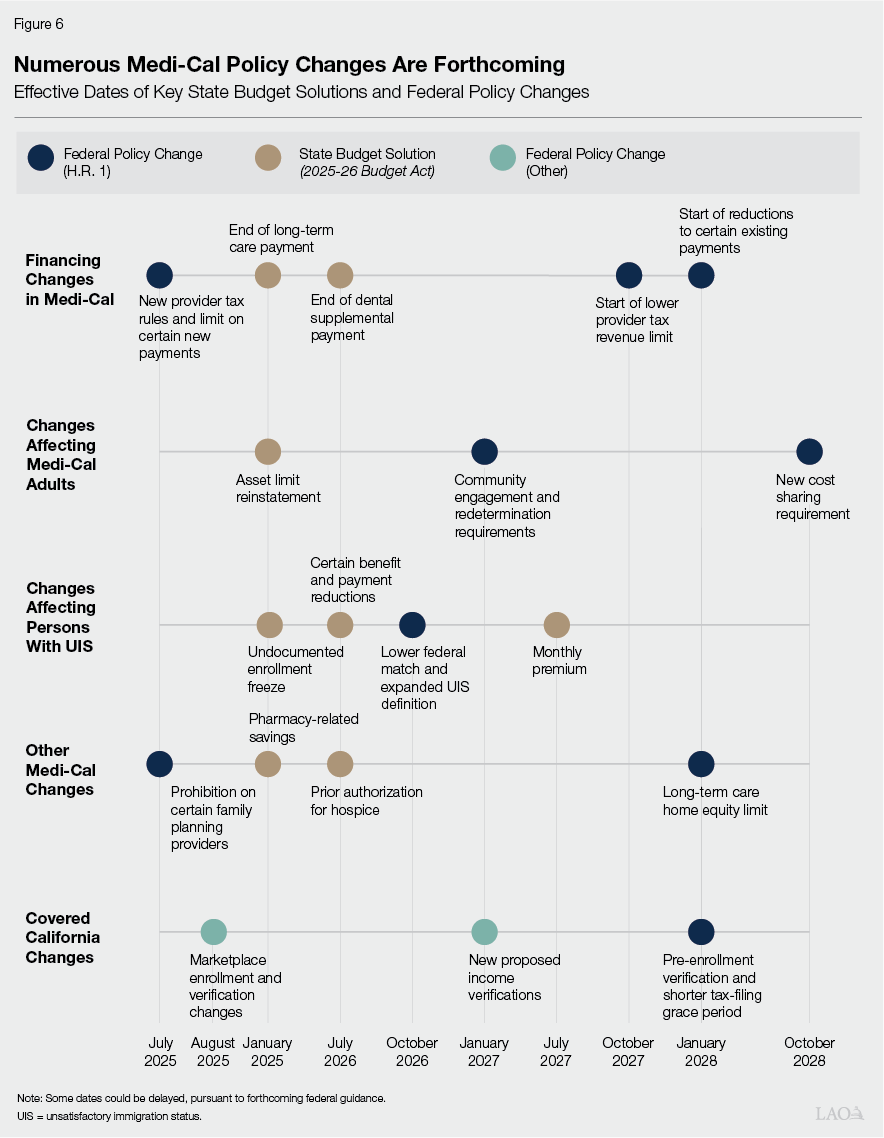

Several Federal Policy Changes Also Affect Health Policy in California. After the state’s enactment of the 2025‑26 Budget Act in June 2025, Congress enacted H.R. 1 in July. Among other areas, H.R. 1 makes several significant changes to federal Medicaid and marketplace policy, many of which are intended to reduce federal costs. In addition, federal actions outside of H.R. 1 also affect California’s health coverage landscape, particularly Covered California. As Figure 6 shows, many of these changes also are scheduled to take effect over time.

Effects of Changing Landscape

In this section, we analyze the effects of the changing landscape on health coverage, hospitals and clinics, private health insurance, and counties. As we describe in several boxes throughout the section, these effects reflect projections using available data and existing literature.

Effects on Health Coverage

H.R. 1 Includes Two Key Changes Affecting Medicaid Eligibility for Childless Adults. As part of H.R. 1, childless adults face two key eligibility changes, both effective January 2027:

- Work Requirements. Childless adults will now need to work (or attend school or complete community service) to remain eligible for Medi‑Cal. The requirement is 80 hours per month (or a dollar equivalent based on the federal minimum wage). Beneficiaries will have to demonstrate compliance in the month before enrolling (for new enrollees) or in at least one month since their last renewal (for existing enrollees). As Figure 7 shows, H.R. 1 mandatorily exempts certain adults from these requirements, and states can adopt certain additional exemptions.

- Six‑Month Renewal. Childless adults will have to renew their eligibility every six months, rather than every 12 months as under pre‑H.R. 1 rules.

Figure 7

H.R. 1 Has Several Exemptions to the Work Requirements

Exemptions Under H.R. 1

|

Required Exemptions |

|

|

|

|

|

|

|

|

|

|

Optional Exemptions (to Be Decided by State) |

|

|

|

|

|

aIncludes physical, intellectual, and developmental disabilities; complex medical conditions; substance use disorders; and disabling mental health disorders. bSpecifically counties with unemployment rates at least at 1.5 times the national average or 8 percent. |

H.R. 1 Eligibility Changes Will Apply to a Few Million Enrollees… Currently, nearly 5 million childless adults are enrolled in Medi‑Cal. All will be subject to the six‑month renewal requirement, but some will not be subject to the work requirements. This is because some enrollees will fall under H.R. 1’s exemptions. Estimating the number of exempt adults is somewhat imprecise due to data limitations. There also is uncertainty because a key exemption is based on counties’ unemployment rates, which vary over time. That said, we estimate that around 1 million to 2 million childless adults could be exempt, leaving about 3 million to 4 million subject to the work requirements.

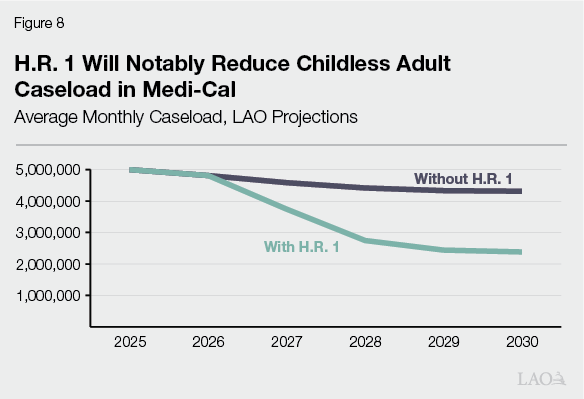

…Likely Resulting in Many Disenrollments From Medi‑Cal. Both the work and six‑month renewal requirements will result in fewer people enrolled in Medi‑Cal. The size of this effect is uncertain, particularly for the work requirements. As we noted in our 2025 report on the changing landscape, previous Medicaid and food assistance work requirements have not been found to induce work. Based on this, we infer that most of the people who do not meet the requirements today probably will disenroll from Medi‑Cal (rather than find work and stay enrolled) once the requirements become effective. Research also suggests that some beneficiaries who work enough hours will nonetheless disenroll due to the higher burden of proving eligibility. This latter effect is far more uncertain and depends on the way that the state will implement the new requirements. Based on the best available evidence and data, we project that nearly 2 million people will be disenrolled by the end of 2030. As Figure 8 shows, this disenrollment will notably reduce childless adult caseload in Medi‑Cal.

People Also Will Leave Covered California Plans, Primarily Due to Three Policy Changes. Access to Covered California, the state’s individual health insurance marketplace, also is expected to tighten under the changing federal landscape. Three key policies are likely to reduce enrollment:

- End of Enhanced Premium Subsidies. During the pandemic, the federal government temporarily increased premium subsidies and expanded eligibility for them. These enhancements were extended through the end of 2025, but Congress allowed them to expire thereafter. As a result, beginning in 2026, households above 400 percent of the federal poverty level no longer qualify for premium assistance, and some households that remain eligible receive smaller subsidies.

- H.R. 1 Provisions. H.R. 1 makes several changes affecting both access to premium subsidies and marketplace enrollment processes. Most notably, beginning in 2027, the law limits premium subsidies for lawfully present immigrants to a smaller set of immigration categories. Beginning in 2028, it also requires marketplace exchanges to verify applicant eligibility before applicants can receive premium subsidies.

- Marketplace Rules. In 2025, the federal government finalized several marketplace rules affecting eligibility, enrollment, and subsidy administration. While some changes took effect in August 2025, others have been blocked by litigation and reproposed for plan years 2027 or 2028. The reproposed rules generally require additional income verification in some cases and increase the risk of losing premium subsidies due to noncompliance.

Covered California has estimated up to 400,000 to 500,000 people could leave the state marketplace as a result of these changes.

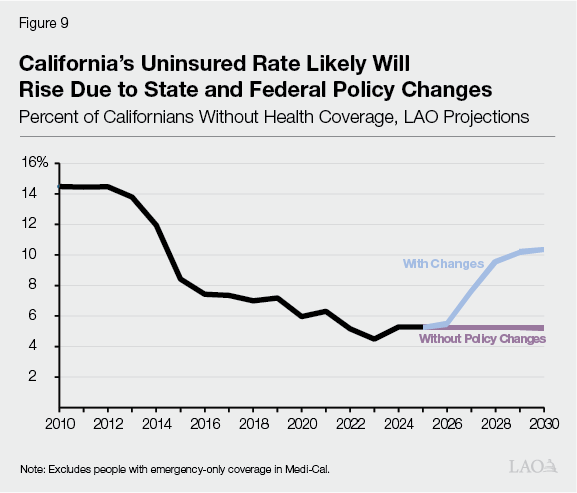

Most Disenrolled People Likely Will Become Uninsured. Many people who disenroll from Medi‑Cal and subsidized Covered California coverage likely will become uninsured, with a relatively smaller share potentially accessing other kinds of coverage. This is because disenrolled people will face key barriers accessing other kinds of coverage. With regard to Medi‑Cal enrollees, those losing coverage due to the new work requirements likely will not be working enough hours to have access to employer‑sponsored insurance. H.R. 1 also bars these individuals from accessing federally subsidized coverage in Covered California. Most of those who leave Covered California will earn too much income to qualify for Medi‑Cal. As Figure 9 shows, we estimate the uninsured rate could roughly double compared to current levels, with most of the increase from people leaving Medi‑Cal. (The nearby box provides more information on how we came to this projection.) We project these elevated uninsured rates would remain below pre‑ACA levels.

How Do We Project Medi‑Cal Disenrollments, Covered California Departures, and the Uninsured Population Under the Changing Landscape?

For Medi‑Cal Disenrollments, Consider Employment Trends. Based on our review of the American Community Survey, we estimate around 23 percent of childless adults who would otherwise be eligible for Medi‑Cal would not meet H.R. 1’s new work or education requirements. Given evidence that work requirements generally do not lead to increased employment, we assume this population either disenrolls from Medi‑Cal or does not newly enroll beginning in 2027. We also assume another smaller share of childless adults (around 3 percent) loses or fails to obtain coverage due to the heightened administrative burden of proving eligibility.

For Covered California Departures, Build From State Projections. Covered California has conducted its own multiyear modeling on health plan enrollment changes due to policy changes. Generally, these models estimate around 400,000‑500,000 people leave the marketplace by 2030. Accordingly, we build our projections from Covered California’s modeling, resulting in a similar level of disenrollment over the time period.

For the Uninsured Population, Project Based on Recent Studies. Previous H.R. 1 analyses, such as those conducted by the Congressional Budget Office, generally project that most people who leave Medicaid due to policy changes will become uninsured. This is because of the many barriers these people will face accessing private health insurance. As a rough estimate, we assume 90 percent of projected disenrolled Medi‑Cal adults become uninsured. For those who leave Covered California, recent modeling from the Urban Institute suggests a smaller proportion—around half—become uninsured. This population is more likely to obtain other kinds of private insurance than those leaving Medi‑Cal because they are higher income. A recent Kaiser Family Foundation survey also found that younger adults were likelier to be uninsured than older adults. We apply the results of these studies to project how many disenrolled adults become uninsured.

Projections Are Uncertain. Our population projections reflect our best understanding of the evidence on the effects of recent policy changes. They are subject to considerable uncertainty, however. For example, California’s efforts to minimize the administrative burden around the work requirements could be more or less successful than we assume, notably affecting how many people disenroll from Medi‑Cal.

Two Key State Actions Also Will Limit Scope of Coverage for Certain Immigrant Groups. Recent state actions also will affect Medi‑Cal coverage for people deemed to have unsatisfactory immigration status (UIS). This population primarily consists of undocumented immigrants, though other groups also fall under the definition. Federal cost sharing for this group is only available for emergency coverage, with the state covering most of the cost of the remaining services. Two state policy changes, however, will notably scale back this population’s access to comprehensive Medi‑Cal coverage:

- Undocumented Expansion Freeze. Beginning in January 2026, newly eligible undocumented adults are barred from enrolling in comprehensive Medi‑Cal coverage. Those with preexisting comprehensive coverage will continue to be covered so long as they maintain eligibility.

- Monthly Premium. Beginning in July 2027, many adults with UIS will have to pay a $30 monthly premium to remain eligible for comprehensive Medi‑Cal coverage.

Individuals who do not comply with these requirements will be limited to emergency coverage in Medi‑Cal—making them technically insured, but with a narrower set of benefits.

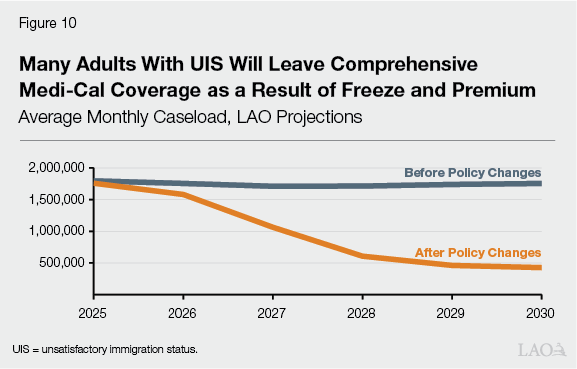

Policies Likely Will Reduce Coverage for Millions of Adults. Both policies likely will result in fewer adults with UIS enrolled in comprehensive coverage, and therefore more adults with emergency coverage only. The magnitude of this effect, however, is uncertain. In particular, it is uncertain how many adults will be unable or unwilling to pay the new premium. As Figure 10 shows, based on existing data and literature, we project 1.3 million adults with UIS will leave comprehensive Medi‑Cal coverage by 2030 due to state actions.

Effects on Hospitals and Clinics

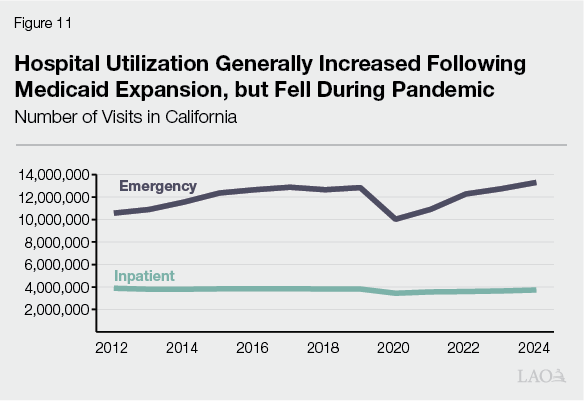

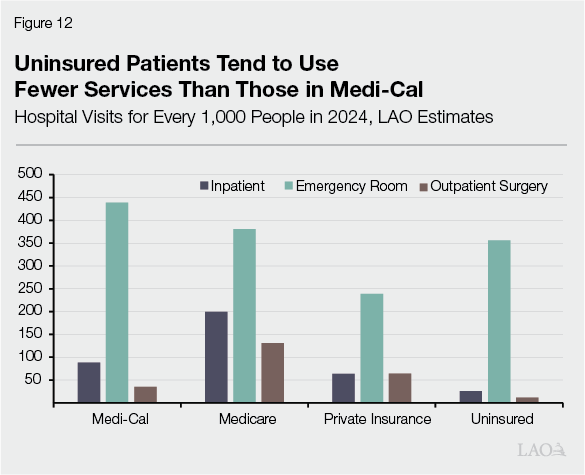

Service Utilization Has Risen and Fallen Over Time. Hospital and clinic utilization has changed over time. As Figure 11 shows, some services, such as hospital emergency room visits, increased following full implementation of the ACA in 2014. The rise in utilization likely stemmed from more people gaining Medi‑Cal and private insurance coverage. As Figure 12 shows, Medi‑Cal patients tend to use more services—including emergency room services—than uninsured people. Utilization continued to rise over time, until it sharply fell in 2020 during the pandemic. Since then, service use has largely rebounded.

Loss of Coverage Will Have Uncertain Effect on Utilization… Because gaining Medi‑Cal coverage tends to be associated with more service utilization, loss of this coverage could cause hospital and clinic utilization to fall. The magnitude of this effect is uncertain, however. This is because the utilization patterns of those who previously had coverage but then become uninsured is unknown. It is possible, for example, that newly uninsured childless adults could use more services than other populations that have never had insurance due to more experience navigating the state’s health care system. (As we note in the box nearby, however, utilization trends over the long term are uncertain.)

How Do We Project Hospital and Clinic Utilization and Finances?

Assume Current Utilization Trends. We assume today’s utilization patterns are indicative of patterns in the future. For example, in 2023, we estimate the Medi‑Cal population has an average of 1.3 clinic visits, compared to 1.2 visits for each uninsured person. We hold these amounts constant over time. (For hospitals, where service utilization has somewhat varied over time, we roughly carry forward current trends into the future.) We also assume that every newly uninsured person has the same utilization patterns as today’s uninsured person. Thus, changes in the number of services per person reflect shifts in coverage, with uninsured populations using fewer services per person than groups with coverage.

Project Net Revenue and Costs for Services. We assume revenues and costs per service follow past growth trends, according to hospital and clinic financial data from the Department of Health Care Access and Information.

Projections Have Two Key Uncertainties. Though we aimed to ground our analysis in the best available data, there are two key uncertainties with our approach:

- Future Utilization Trends. Today’s utilization patterns might not reflect future patterns among those who become uninsured. On the one hand, at least some newly uninsured childless adults—who are currently enrolled in Medi‑Cal—will have had experience interacting with the state’s health care system. This experience could influence their future behavior, potentially causing them to use more services once uninsured than we assume. On the other hand, those who become disenrolled may be lower acuity than the typical uninsured or Medi‑Cal patient, resulting in lower utilization than we assume.

- Future Revenues and Costs. Recent years may not be good indicators of future revenue and cost trends. For example, hospitals and clinics have recently grown nonclinical revenue, such as government grants, donations, and investment income. These future trends are uncertain. Also, the state’s Office of Health Care Affordability has recently set health care spending targets aimed at slowing growth in overall spending. This policy could result in slower hospital and clinic cost growth relative to past years.

…But a Likely Increase in Uncompensated Care at Hospitals… Research also suggests that while loss of coverage could result in reduced health care utilization, a greater share of remaining services occur without payment to providers. In the case of hospitals, this would result in more free care (charity care) and unpaid charges (bad debts)—together known as uncompensated care. In 2024, hospital uncompensated care was estimated to be a little over $2 billion. Based on available data, we estimate this amount could increase by as much as a few billion dollars annually by 2030 due to disenrollments resulting from Medicaid and Covered California eligibility changes.

…And Clinics. The concept of uncompensated care is not as clearly defined or readily tracked for clinics compared to hospitals. We estimate, however, that clinics collectively spend several hundred million dollars annually on care to the uninsured, much of which is free or discounted. The cost of this care likely will increase for clinics as well. (Certain clinics must provide care to the uninsured to qualify for federal financing arrangements.) Based on available data, we estimate the increase could be roughly up to $1 billion annually by 2030.

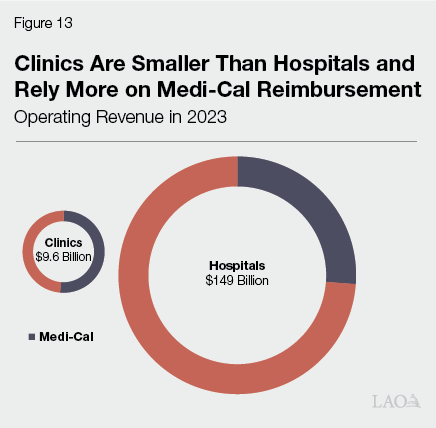

On Net, Margins Likely Will Be Lower, Particularly for Clinics. The dollar amount of uncompensated care, on its own, provides little information about the overall financial health of hospitals and clinics. This is because uncompensated care is only one component of providers’ overall costs. A more comprehensive measure of financial health is a facility’s annual margins—the share of revenue providers earn after accounting for expenses. Generally, hospitals and clinics aim to have positive margins in most years to sustain operations and avoid deficits. Based on available data, we estimate hospitals in aggregate could face margin reductions ranging from about 0.5 percentage points to a couple percentage points due to H.R. 1. The reduction in clinic margins probably would be more notable; we estimate at least a few percentage points decrease. There are two reasons that clinics could face more significant financial effects, both summarized by Figure 13. First, clinics’ operating revenues are much smaller on average than hospitals, providing them with less capacity to absorb sizable cost increases. Second, clinics tend to rely more heavily on Medi‑Cal funding as a share of total revenues than hospitals, making them particularly susceptible to changes in Medi‑Cal utilization and reimbursement.

State Coverage Reductions for Adults With UIS Could Compound Effects of H.R. 1… The above effects do not consider coverage losses in Medi‑Cal for adults with UIS due to state actions. Individuals who fail to find alternative comprehensive coverage will generally have no coverage for services delivered at hospitals and clinics, unless they receive emergency care. Given the number of people potentially losing comprehensive Medi‑Cal coverage, hospitals and clinics could face additional uncompensated care and reductions to their margins.

…But Magnitude Is Uncertain. While there likely will be added cost pressures on hospitals and clinics from adults with UIS losing comprehensive Medi‑Cal coverage, the magnitude of this effect is uncertain. This is because it is difficult to project this population’s utilization patterns. Research has generally found that undocumented immigrants on average use less health care than citizens and other immigrant groups, largely because they tend to be younger and face certain barriers to accessing care, such as language barriers and immigration‑related concerns. That said, the state’s recent expansions of Medi‑Cal coverage for undocumented immigrants appear to cost notably more than initial estimates, in part because the state underestimated this population’s utilization of services.

Three Key Financing Changes Likely Will Reduce Medi‑Cal Reimbursements. In addition to serving fewer Medi‑Cal patients, hospitals and clinics also will face certain reductions in Medi‑Cal reimbursements due to federal and state policy changes:

- Lower Managed Care Payments to Hospitals. Under H.R. 1, California will have to reduce certain payments to hospitals so that their overall reimbursement in Medi‑Cal managed care is no greater than what Medicare pays. Previously, this limit was set at the average rate paid by commercial health plans, which tend to pay higher rates than Medicare. States must begin ratcheting down their provider payments over time beginning in January 2028.

- Lower Rates to Clinics for Services Provided to Adults With UIS. Medi‑Cal pays safety net clinics for each visit from a Medi‑Cal beneficiary. Each clinic’s rate is set based on its reported costs. As a budget solution, the state will reduce these rates for visits from adult Medi‑Cal enrollees with UIS beginning in July 2026.

- Lower Provider Taxes. Under H.R. 1, the state will need to reduce certain taxes on private hospitals and health plans used to help support Medi‑Cal. These charges also help support rate increases for hospitals and clinics.

Effect of Financing Changes is More Uncertain. These financing changes likely will result in additional losses for hospitals and clinics. The exact size of these losses, however, is difficult to project because of limited data. Most notably, we are not aware of consistent data comparing hospital Medi‑Cal payments to Medicare. Even if better information were available, guidance from federal administrators on the new hospital payment limit is still forthcoming. The Department of Finance has provided more concrete projections around the UIS‑related change for clinics, estimating the associated state savings—and cost to clinics—at around $1 billion annually. Limited data, however, prevent us from independently assessing this estimate.

Many Financing Losses Will Reflect Missed Opportunities, Rather Than Reductions to Current Operations. Though financing changes will result in reduced reimbursements to providers in the future, many of these changes will reflect missed opportunities, rather than direct reductions to current operations. This is because many of the financing changes will overturn recently enacted or expected increases in funding. For example, as we noted in our 2025 report, the state likely will need to reduce two key provider taxes—a tax on health plans and a fee on private hospitals—to comply with the new limit under H.R. 1. These taxes help pay for rate increases to hospitals. In the case of the health plan tax, however, hospitals only began receiving such increases in 2025. In the short run, it appears the state will still be able to charge a similarly sized private hospital fee, rather than pursue a notable increase in 2025.

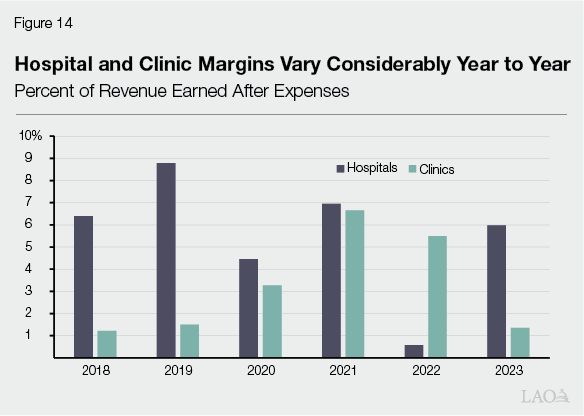

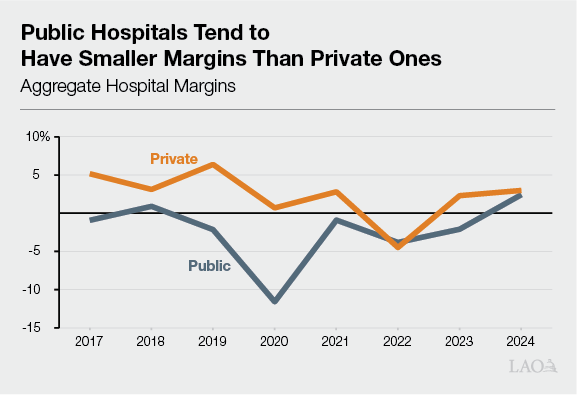

Margin Reductions Could Be Difficult for Some Hospitals and Clinics to Manage—Though Risk Is Uncertain. The degree to which reductions in margins pose serious operational risks to hospitals and clinics is uncertain and could vary across individual facilities. As Figure 14 shows, provider margins are quite volatile year to year and difficult to predict. Even without H.R. 1 in effect, margins have tended to swing by as much as several percentage points year to year. That said, these trends are aggregate estimates, with some facilities facing operating losses while others are profitable. For context, in 2022 when several hospitals faced financial distress, aggregate margins fell to less than 1 percent.

Impacts Likely Will Be Greater for Certain Kinds of Hospitals and Clinics. Looking at financial pressures in aggregate can mask important institution‑specific effects. Some providers, particularly those primarily serving patients with private insurance, may see relatively limited effects from these changes. In contrast, providers serving larger numbers of Medi‑Cal and uninsured patients likely will experience more notable effects. For example, numerous hospitals and clinics are considered “safety net,” meaning that they serve a disproportionate number of low‑income and uninsured patients and thus incur a large share of the state’s uncompensated care. One recent study estimated safety net hospitals could face an additional 0.5 percentage point to 1 percentage point reduction in their margins relative to the aggregate averages for all hospitals. Public hospitals also could face heightened pressures given their specific financing situation in Medi‑Cal. (The box nearby provides more information on public hospitals.)

How Will the Changing Landscape Affect Public Hospitals?

Public Hospitals Have Somewhat Different Financing Approaches in Medi‑Cal. Public hospitals—those owned by the University of California (UC), counties, and local health care districts—have different financing arrangements than their private counterparts. Generally, public hospitals tend to fund a greater portion of the nonfederal share of Medi‑Cal costs using their own local contributions, such as from local funds or funds from other payors. These hospitals also tend to serve more Medi‑Cal and uninsured patients than private hospitals, though there is considerable variation. As a result, as the nearby figure shows, public hospital margins tend to be lower than at private hospitals.

Changing Landscape for Public Hospitals Different in Two Key Ways. Public hospitals will share many of the same fiscal changes as their private counterparts under the changing landscape. Two key dynamics, however, will be unique to public hospitals:

- Temporarily Higher Directed Payments. Prior to Congress enacting H.R. 1, the state sought federal approval for sizable increases to hospital Medi‑Cal directed payments in 2025 relative to past years. Following H.R. 1’s enactment, the payment increases to private hospitals cannot occur, as they would have been supported by the larger private hospital fee. However, the increased public hospital payments received federal approval prior to H.R. 1 because they are funded by local contributions, rather than provider taxes. These increases will be temporary, as they will need to be reduced over time to comply with the new Medicare limit.

- Additional Costs to Backfill Federal Funding Reductions. Some H.R. 1 changes do not directly affect most hospitals, but instead require a backfill from the state General Fund. For example, H.R. 1 reduces the federal share of cost for emergency care to certain immigrant groups. As an exception, however, UC and county hospitals will have to backfill the lost federal funding themselves. This is because they use local contributions to fund the nonfederal share of cost of these services.

Hospitals and Clinics Could Pursue Six Key Approaches to Manage Higher Costs. The above effects are hypothetical, assuming recent utilization patterns and financing trends continue into the future. In reality, hospitals and clinics could respond to financial pressures in various ways, pursuing one or more of the following six potential strategies:

- Absorb the Costs. Hospitals and clinics with ample margins today may accept having lower margins in the future without adjusting their operations.

- Cost Shift to Other Payors. Some providers might try to make up costs by negotiating higher rates from other payors, such as private insurance and Medi‑Cal managed care plans. Their ability to do so, however, is uncertain. Research suggests that market power largely determines rate negotiations, with some larger providers having substantial leverage and others having very little. In fact, providers with less market power might seek to obtain more private insurance contracts by reducing rates to be more competitive when bidding for contracts.

- Grow Other Revenues. Many hospitals and clinics do not balance their budgets solely from clinical revenues. They rely on other revenues, such as government grants and contracts, private donations, and investment returns to make up the difference. Some providers may seek to expand these alternative sources to the extent feasible.

- Reduce Spending. Hospitals and clinics might aim to control costs, such as by limiting compensation growth or eliminating less financially feasible services. Hospitals and clinics might also defer facility and infrastructure maintenance and renewals.

- Consolidate. Some hospitals and clinics may seek to consolidate into larger health systems to better absorb costs.

- Close. Hospitals and clinics that cannot sustain operations over the long term might close.

Effects on Private Health Insurance

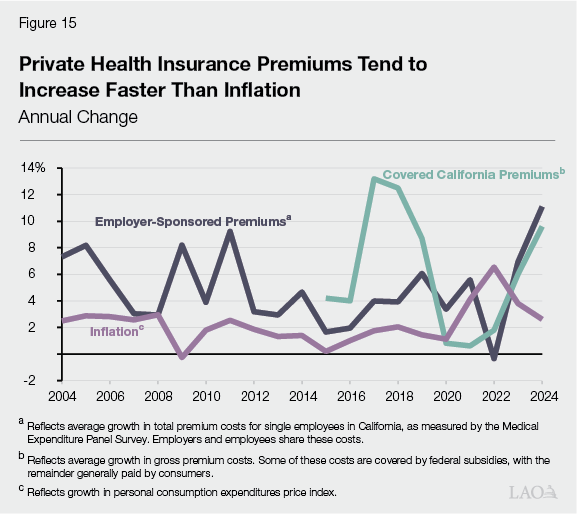

Some Evidence Suggests ACA Limited Private Premium Growth. As Figure 15 shows, employer‑sponsored and Covered California premium costs have tended to increase faster than inflation, with particularly noteworthy increases in some years. (These trends reflect broad averages, with likely considerable variation among individual health plans.) In the initial years following implementation of the ACA, growth for employer‑sponsored health insurance (which comprises around 90 percent of all private health insurance coverage) appears to have been somewhat lower than in previous years. This trend aligns with research suggesting that the ACA helped slow cost growth in the private insurance market. This is primarily because less costly populations became covered by private insurance, lowering the overall risk pool by including healthier individuals who used fewer services. That said, annual health premium growth has been notable in more recent years, sometimes exceeding 10 percent.

Covered California Departures Will Put Upward Pressure on Individual Premiums. Generally, those who leave Covered California over time are expected to be healthier than the average enrollee. This is because healthier individuals are more sensitive to changes in health care costs, such as reductions in subsidies. These departures will mean a relatively riskier and costlier population remains enrolled in Covered California, resulting in higher gross premiums (before netting out federal and state subsidies). The exact impacts are uncertain and still being assessed by health plans and the state. In 2026, health plan premiums in the exchange increased by over 10 percent relative to 2025. Initial data suggest around 2 percentage points of this growth specifically is due to enrollees leaving as a result of the end of the enhanced federal subsidies.

Covered California Enrollees Will Pay More Costs Out of Pocket. For enrollees who remain in the marketplace, many—particularly those who benefited from the enhanced subsidies—will pay higher costs out of pocket. Although California has adopted a state premium subsidy for enrollees earning up to 165 percent of the federal poverty level, other households with incomes below 250 percent of the federal poverty level have experienced a 60 percent to 70 percent growth in net premiums in 2026. Some enrollees may manage these costs by enrolling in lower‑premium health plans. These plans, however, tend to include higher cost sharing, such as deductibles, copays, and coinsurance. For example, enrollees in “bronze” plans—among the lowest‑premium plans available in Covered California—paid about $1,200 in cost sharing on average in 2024, nearly double the amount enrollees paid in the more generous “silver” plan.

Departures Could Also Affect Costs Among Other Private Insurance Plans. Some people who leave Covered California may find other kinds of private health insurance coverage, such as through their employer or by purchasing it themselves outside of the exchange. To the extent that these individuals are relatively healthy, they could improve the risk pools and reduce average per‑enrollee costs of other private health plans. This effect is uncertain, however.

Rise in Uncompensated Care Also Could Affect Premiums. Private health insurance costs also could be affected by the increase in uncompensated care and reduction in provider reimbursements. For example, providers could try to negotiate higher rates with private plans to help manage losses. On the other hand, some providers may negotiate lower rates with private health plans to encourage more contracts and increase the volume of care. These effects are uncertain and difficult to predict.

Effects on County Indigent Health Care Programs

Counties Primarily Rely on Realignment Revenue to Fund Indigent Care. Funding sources for county indigent care programs have varied over time. Prior to the 1990s, counties largely relied on General Fund support provided by the state. This arrangement changed as part of a substantial realignment of state and local programmatic and fiscal responsibilities in 1991—known as 1991 realignment. 1991 realignment has since become the primary source of support for county indigent care programs. Under this arrangement, counties now receive a dedicated portion of sales tax and vehicle license fee revenue to support certain health and human service programs, including indigent health care. The funds flow to different accounts using a complex formula (see the nearby box for more information). One account, known as the Health Subaccount, specifically supports county indigent care, as well as public health activities.

How Does Realignment Funding for County Indigent Health Work?

Funds Are First Allocated to Base Amount. Under the 1991 realignment formula, a portion of sales tax and vehicle license fee funds are allocated among various subaccounts that support certain county health and social service programs. The Health Subaccount supports county indigent health and public health programs. Each subaccount receives a minimum “base” amount of funds each year, which generally reflects the previous year’s total allocation.

Then, Growth Is Allocated. After funding the base amount, any remaining revenue is allocated to fund program cost growth. Certain social service programs get first priority for growth funds based on any increases in program caseloads. A portion (around 20 percent) of any remaining funds is then allocated to the Health Subaccount to fund indigent health and public health programs. The other around 80 percent of the remaining funds are allocated for mental health and certain other social services.

Portion Is Redirected Back to CalWORKs. Pursuant to Chapter 24 of 2013 (AB 85, Committee on Budget), a portion of health realignment funds are redirected back to the state to help fund the California Work Opportunity and Responsibility to Kids (CalWORKs) program. Most counties calculate their redirection amount as a fixed share of their realignment funds based on past allocations. As allowed in the statute, some counties have opted to calculate the amount based in part on reported health program costs.

Prior to H.R. 1, County Indigent Programs Notably Ramped Down… When the state implemented the ACA, many uninsured, childless adults shifted from county indigent health care programs to Medi‑Cal coverage. This resulted in a substantial reduction in county indigent caseloads. Based on conversations with counties, we estimate that around 10,000 people are currently enrolled in these programs statewide, down from around 850,000 before the passage of the ACA.

…And the State Redirected Substantial Realignment Funds. The reduction in indigent caseloads following the ACA resulted in numerous changes to county programs. Most notably, the state redirected a portion of funds from the Health Subaccount to help offset state General Fund costs in the California Work Opportunity and Responsibility to Kids (CalWORKs) program. This redirection was intended to reflect notably smaller county indigent programs due to the ACA. In addition, some counties have made their indigent programs’ eligibility criteria more expansive or benefits more generous given the low number of enrollees.

Rise in Uninsured Could Have Significant Effect on County Indigent Program Caseloads. With the uninsured population effectively doubling, county indigent programs likely will experience significant pressure to provide services for an expanded population. The number of people the counties will serve is uncertain. From limited information prior to the ACA, it appears that around 20 percent of the uninsured population participated in county programs. Applying this 20 percent assumption to our projected uninsured population in 2030 yields a caseload increase of around 400,000 people. However, participation could be higher. This is because people disenrolled from Medi‑Cal may have more experience with accessing health care compared to other uninsured groups. Our estimates of indigent caseload are particularly sensitive to assumed participation levels among the newly uninsured. For example, assuming a 50 percent participation rate yields nearly 1 million more people in indigent programs by 2030.

Costs Could Exceed Existing Resources, but Are Difficult to Pinpoint. Counties likely will face significant costs to grow their indigent care programs to meet some of the demand from the newly uninsured. The cost is uncertain and depends on the number of users as well as the average cost of services, both of which could vary significantly based on each county’s decisions around program parameters. Based on limited information, we estimate costs across all counties could be up to the low billions of dollars. By comparison, the Health Subaccount today provides around $1 billion, most of which counties use to support public health services.

Counties Could Pursue Some Strategies to Mitigate Cost Pressures. With cost pressures exceeding available realignment resources, counties likely will explore ways to limit their exposure. Most notably, counties can tighten their eligibility and benefit rules for indigent programs, serving fewer people at a lower cost per person. Stakeholders have anecdotally noted that some county boards are currently weighing such actions. Counties also could explore raising more revenue, though they face certain limitations to do so. For example, counties must gain voter approval to levy new taxes or increase existing taxes. State law also limits the types of taxes local governments can raise.

Issues to Consider

As the Legislature considers the implications of H.R. 1 and other policy changes on the state’s health care system, we recommend weighing different actions in the short term (this year’s budget process) and the long term (over future years). We describe these different considerations below.

Short‑Term Issues

Impacts of H.R. 1 Are Uncertain. The estimates described above are subject to considerable uncertainty. As a result, our projections make numerous assumptions about health coverage disenrollments, the uninsured population, health care utilization, and health care costs. With so many assumptions compounding each other, actual effects could be notably different from what we estimate.

State Has Limited Ongoing Fiscal Capacity. As we have noted in other publications, California is facing projected structural budget deficits. This means that the state has no fiscal capacity for new ongoing commitments, absent making reductions in other areas or raising new revenues. Moreover, projected deficits occur despite recent growth in state revenues from the stock market. Were the state to experience an economic downturn in the coming years, the Legislature could face an even larger budget imbalance.

Recommend Bolstering Legislative Oversight… With so much uncertainty and limited ongoing fiscal capacity, it would be prudent for the Legislature to begin tracking the effects of federal and state policy changes before taking significant action to restructure programs. To this end, we recommend the Legislature focus this year’s budget process on bolstering oversight regarding the effects on hospitals, clinics, and counties. While financial data already exist for hospitals and clinics, in‑depth and timely analysis of the fiscal effects of upcoming policy changes would be valuable. Data on county programs, by contrast, is less robust and not publicly reported on a regular basis. As a result, projections are often dependent on limited information provided by counties and their associations. Moreover, some key Medi‑Cal information, such as how Medi‑Cal hospital payments compare to Medicare, are not publicly available. The Legislature could enhance its oversight by directing the Department of Health Care Access and Information (which compiles data on hospitals and clinics) and Department of Health Care Services (which has broad responsibility for ensuring access to health care for low‑income populations) to gather information on provider and county finances, as well as county indigent program caseloads.

…And Focusing on Limited‑Term, Targeted Financial Assistance. The Legislature also could explore providing targeted, limited‑term financial assistance to providers and counties particularly at risk of distress in the near future. For example, the Legislature could explore renewing and expanding the Distressed Hospital Loan Program, which assessed need based on factors such as a hospital’s cash on hand, margins, and community impact. The state could consider a similarly structured program for county indigent programs and/or clinics.

Long‑Term Issues

Over the Long Term, Structural Changes Could Be Warranted. Barring future developments, recently enacted state and federal policy changes will significantly change California’s health care landscape. While much of the ACA remains in place, the state’s health care system faces an increase in uninsured residents in the coming years. As such, the Legislature may want to reexamine key issues in the health care landscape, described below.

Should the Legislature Tighten or Loosen Requirements on Providers and Counties? Federal and state law place requirements on certain hospitals and clinics to provide services to uninsured populations, such as by offering charity care and discounted services. State law also requires counties to provide care to the uninsured but grants counties substantial flexibility to determine eligibility and benefits. With so many people estimated to become uninsured, the Legislature could revisit these expectations. For example, it could bolster state requirements, such as by mandating more consistent service levels for counties or expanding charity care requirements for hospitals and clinics. (The Legislature likely would have to directly reimburse counties for any new requirements, pursuant to the California Constitution.) Alternatively, the Legislature could loosen certain state requirements, affording providers and counties more flexibility to manage cost pressures according to local considerations.

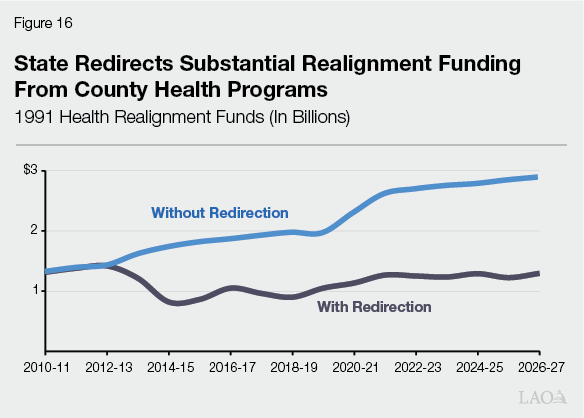

Should the Legislature Restructure Existing Financing Arrangements? The Legislature also could explore whether to revisit some of the state’s health care financing arrangements. Most notably, it could explore whether to restructure the 1991 realignment funding approach for county indigent health programs. As Figure 16 shows, we estimate the state currently redirects $1.6 billion in realignment health funds to help offset state spending in CalWORKs. Sending these funds back to counties could help cover much of the cost for indigent care, but at a cost to the state to backfill support to CalWORKs. Similarly, the Legislature also could explore whether to adjust the state’s complex Medi‑Cal hospital financing structure, which places a significant share of the cost of care on hospitals. Such an effort could build upon the Department of Health Care Services’ recent hospital finance reform initiative.

Conclusion

Health care consumers, providers, and payors in California will face heightened fiscal constraints as a result of the changing fiscal and policy landscape. The circumstances of these constraints are not unprecedented, however—much of the new landscape likely will resemble conditions that existed more than a decade ago. This is because these changes unwind some eligibility and financing changes that occurred after state implementation of the ACA in 2014. Moreover, from an access standpoint, the state will still be in a better position than before 2014, with key elements of the ACA (such as the Covered California marketplace) still intact. Keeping this broader context in mind, the Legislature, administration, providers, and counties likely will need to work collaboratively to adjust policies, financing structures, and services to align with the new landscape and fiscal realities.

Works Referenced in Report

Previous LAO Reports

- Considering Medi‑Cal in the Midst of a Changing Fiscal and Policy Landscape. (2025.)

- The 2026‑27 Budget: Medi‑Cal Fiscal Outlook. (2026.)

- The 2026‑27 Budget: County Administration and H.R. 1 Implementation. (2026.)

- The 2026‑27 Budget: Overview of the Governor’s Budget. (2026.)

Projections of Uninsured Populations

Congressional Budget Office. (2025.) Estimated Effects on the Number of Uninsured People in 2034 Resulting From Policies Incorporated Within CBO’s Baseline Projections and H.R. 1, the One Big Beautiful Bill Act.

Urban Institute. (2025.) 4.8 Million People Will Lose Coverage in 2026 If Enhanced Premium Tax Credits Expire.

Kaiser Family Foundation. (2026.) Cost Concerns and Coverage Changes: A Follow‑Up Survey of ACA Marketplace Enrollees.

Hospital and Clinic Financing

The Commonwealth Fund. (2025.) The Impact of Proposed Federal Medicaid Work Requirements on Hospital Revenues and Financial Margins.

Kaiser Family Foundation. (2025.) Key Facts on Health Coverage of Immigrants.

Department of Health Care Services. Value Strategy for Hospital Payments in Medi‑Cal Managed Care. (2025‑26 budget change proposal.)