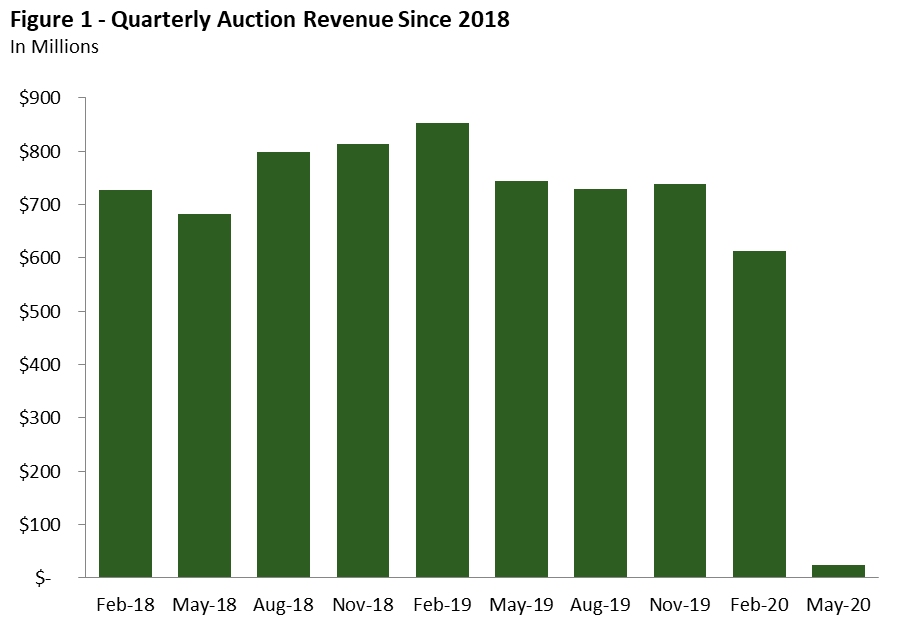

May 2020 Auction Generates About $25 Million in State Revenue. The California Air Resources Board (CARB) released a summary of the results from the most recent quarterly cap-and-trade auction held on May 20, 2020. Based on the preliminary results, the state will receive an estimated $25 million in revenue from the auction. As shown in Figure 1, this amount is much less than what the state received from recent auctions—each of which generated over $600 million. The primary difference is a decrease in the number of allowances sold. Unlike recent auctions, where essentially all state-owned allowances offered for sale were purchased, only 4 percent of the available state-owned allowances were purchased at the May 2020 auction. (About 34 percent of the overall number of allowances offered for sale were purchased—including allowances held by the state, utilities, and Quebec.) All allowances were purchased at the minimum auction price established by the CARB--$16.68.

2019-20 Auction Revenue About $300 Million Lower Than Budget Assumes. The 2019-20 budget assumes about $2.4 billion in total 2019-20 auction revenue. Based on the May auction results, the total 2019-20 revenue will be about $2.1 billion—or $300 million less than assumed in the budget.

Slightly Less Money for Continuous Appropriations in 2019-20. Under current law, continuously appropriated programs are automatically allocated about 60 percent of 2019-20 auction revenue. As a result, we estimate these programs will receive a total of $1.2 billion in 2019-20, or about $170 million less than the budget assumed. The total estimated continuous appropriations for 2019-20 are as follows:

- $493 million for high-speed rail

- $394 million for affordable housing and sustainable communities

- $197 million for transit and intercity rail

- $99 million for transit operations

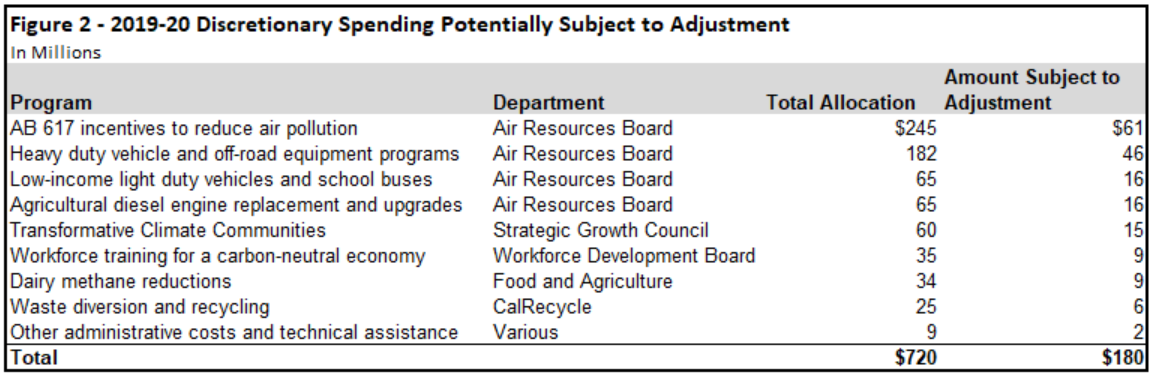

Implications for Certain 2019-20 Discretionary Budget Allocations Not Yet Clear. In accordance with provisions of the 2019-20 Budget Act, departments administering certain specified discretionary programs may not commit more than 75 percent of their 2019-20 allocation before the results of the May 2020 auction are available. This provision was intended to ensure that funding was not overcommitted if actual auction revenues came in below what was assumed in the budget plan. After the final amount of the proceeds from the May auction are determined, the Department of Finance (DOF) will make a final decision on allocations for these programs and must notify the Joint Legislative Budget Committee. Figure 2 identifies the specific programs subject to this adjustment, the total amount allocated to each program in the 2019-20 budget, and the amount of each allocation that is subject to the potential adjustment by DOF. (Other discretionary programs are not subject to the same spending adjustments.) It is not yet clear if, or how, DOF might change the allocations to these programs in the coming weeks. It is possible that there will be enough money in the fund’s reserve to cover some or all of the lower revenue.

2020-21 Auction Revenue Subject to Substantial Uncertainty. As we mentioned in our recent Overview of the Governor’s May Revision Proposals for Resources and Transportation Programs, there is significant uncertainty about 2020-21 auction revenue. In light of this uncertainty, the Governor’s May Revision proposes to modify a budget control section to make Greenhouse Gas Reduction Fund (GGRF) allocations contingent on the amount of revenue collected at auctions in 2020-21. In concept, we think making allocations contingent on future auction revenue and establishing a mechanism to prioritize revenue under lower revenue scenarios is a reasonable approach. However, there are different mechanisms that could be used, and the Legislature will want to ensure that its preferred programs are prioritized in the final expenditure plan. In the coming weeks, we plan to post additional information about potential 2020-21 revenue scenarios and considerations for the Legislature as it develops its GGRF expenditure plan.