The 2021-22 Budget: May Revenue Outlook

May 17, 2021

This post provides commentary on our May Outlook revenues. We begin with a discussion of the impact of the existing and future economic landscape on state revenues. We then present our May revenue outlook. We conclude with more detailed observations on trends in the state’s major revenue sources. In about a week, we will publish our Multi-Year Outlook, which compares our revenue estimates to our estimates of the ongoing costs of the Governor’s May Revision proposals.

Despite Pandemic, Tax Collections Are Way Up

State tax collections over the last year have been extraordinary. Not only has much of the state’s tax base—such as payrolls, taxable retail sales, and business profits—been surprisingly resilient, but tax collections have grown well beyond their pre-pandemic baseline. Through March, collections from the state’s three largest taxes—personal income, sales, and corporation taxes—are up 20 percent from 2019-20 and 27 percent from 2018-19. Such growth would be extraordinary in a normal year, let alone during a pandemic. The rapid onset of this revenue surge makes it difficult to pin down its exact causes. That being said, our current understanding is that several factors are at work:

- Continued Success of Technology Sector. While many businesses have struggled throughout the pandemic, California’s technology sector has thrived. Several major firms posted historically high earnings. Expanding firms raised record amounts of funding via initial public offerings. Venture funds continued to flow to California startups. When technology firms do well, compensation to their employees rises. This, in turn, bolsters state income tax collections.

- Asset Prices Are Up. Asset prices have risen rapidly over the last year. Price of stocks and homes have posted double digit growth above pre-pandemic levels. With asset prices rising, collections from taxes on capital gains—profits from the sales of assets—also have risen. Historically low interest rates likely play a role in this trend. Low interest rates boost asset prices in several ways. For example, lower borrowing costs make businesses more profitable, thereby increasing the value of their stock.

- Corporation Tax Policy Changes. Last year, faced with a projected budget shortfall, the Legislature temporarily limited the ability of businesses to use prior year losses and tax credits to reduce their tax payments. These limits increased business tax collections by several billion dollars in 2020-21. These increased collections will carry over into 2021-22, before beginning to ramp down in 2022-23.

- Rebound in Consumer Spending. After collapsing last spring at the onset of the pandemic, consumer spending has rebounded over the last year. Key to this rebound has been a shift to e-commerce, as well as federal and state efforts to boost household incomes through stimulus checks and unemployment benefits.

Will Recent Revenue Strength Continue?

Growth in Budget Year More Likely Than Not But Far From Certain. With revenue growth in the current year being such a surprise, it is reasonable to wonder whether these gains are one-time or instead will be sustained—or even continue growing—moving forward. We cannot answer this question with much confidence. That being said, our best guess is that it is more likely than not that current year revenues will be sustained and continue to grow in the budget year. Several observations are consistent with this forecast:

- Consensus of Economists Expects Strong Economic Growth. The consensus among professional economists is that economic expansion will continue over the next year. For example, respondents to a widely-cited survey of economists (Blue Chip Economic Indicators) expect gross domestic product to grow at the fastest pace in nearly 40 years.

- Full Impact of Stimulus Payments Yet to Be Realized. Over the last year, the federal government has provided roughly $80 billion in stimulus payments to Californians. Evidence suggests that many households used this money to increase savings and pay down debts. Household savings rates are at all-time highs, while credit card balances have decreased significantly. This creates a foundation for robust consumer spending over the next year as the economy reopens further.

- Interest Rates Expected to Remain Low. The Federal Reserve, which influences interest rates via monetary policy, has signaled an intention to maintain low interest rates for the foreseeable future. This should continue to boost economic activity and buoy asset prices moving forward.

- Investment in Technology Firms Remains Strong. Investment in California technology firms has remained robust thus far in 2021. While the future decisions of investors are difficult to predict, strong returns from recent initial public offerings of California firms may attract additional investment over the coming year.

Continued revenue growth, however, is far from certain. Any number of conceivable and inconceivable scenarios could result in revenue declines in the budget year. For instance, a shortage of materials and labor as the economy ramps up after the pandemic could result in elevated inflation. Elevated inflation could spur the Federal Reserve to raise interest rates sooner than anticipated in an attempt to keep the economy from “overheating.” This, in turn, could lead to lower business profitability, falling asset prices, and reduced investor interest in California technology firms, all of which would drag down state revenues.

Multiyear Revenue Forecast Highly Uncertain. Even during less turbulent times, consistently predicting the state’s economy or tax revenues multiple years in the future is not possible. A wide range of revenue outcomes are plausible and all forecasts will be wrong to some extent. Faced with such unpredictability, our review of research on this topic finds that a straightforward approach—such as assuming continuation of a historical average—tends to be least wrong most often. Consistent with this evidence, our out-year revenue forecast largely assumes long-term historical norms will continue.

Tradeoffs of Different Revenue Assumptions Should Be Considered. Even the best forecasting approach will result in major errors at some point. As such, we suggest the Legislature weigh the risks associated with various revenue assumptions. In general, revenue assumptions that are higher than historic norms present a greater risk of budget shortfalls in future years. Conversely, revenues that are lower than historic norms heighten the risk off inefficient budget decisions. In good times, the Legislature will miss opportunities to enhance public services or provide tax relief. In bad times, the Legislature will cut services or raise taxes more than is needed. How the Legislature balances these competing risks should dictate how it thinks about revenues in the out years. Our main revenue outlook gives roughly equal weight to both risks. But other assumptions that balance these risks differently could be reasonable. To assist the Legislature in considering alternatives, our outlook estimates how far revenue could deviate from our main forecast based on historical experience.

LAO Revenue Outlook

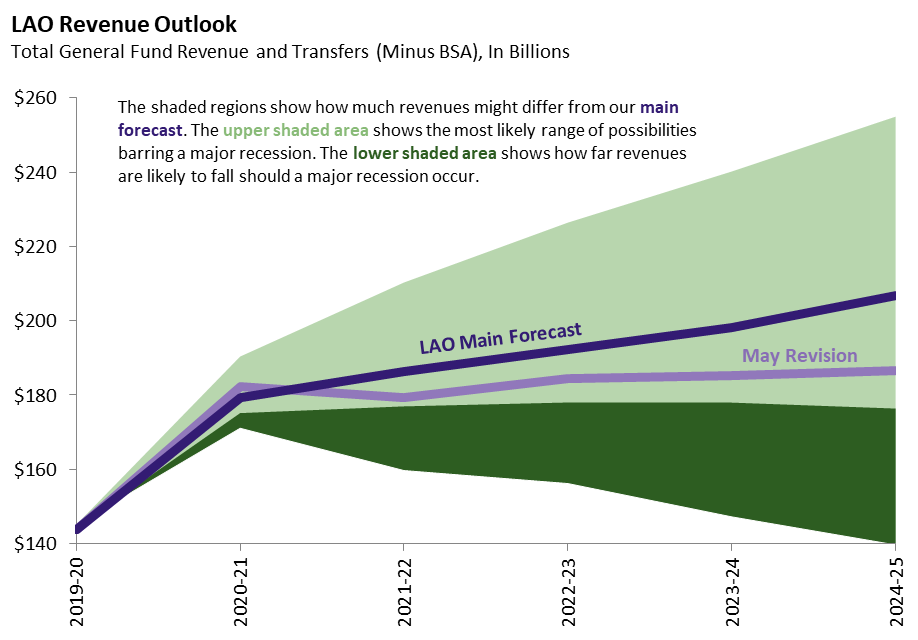

The graphic below summarizes our multiyear revenue outlook.

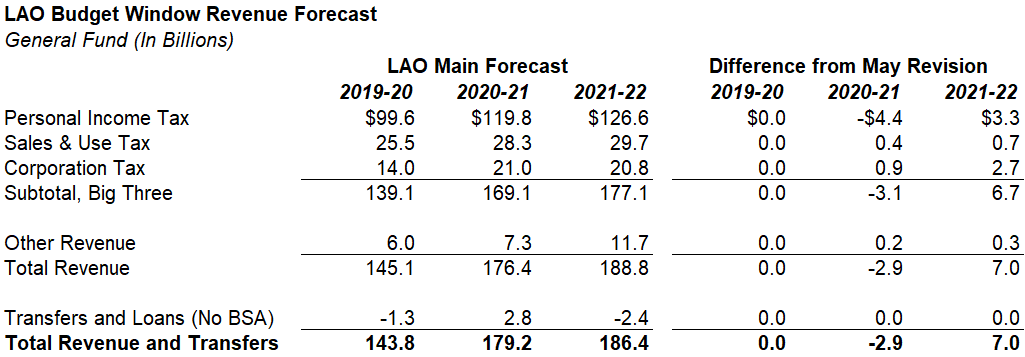

Main Forecast Relatively Close To Administration Over the Budget Window. Our main forecast expects total General Fund revenues (including transfers and loans) to be $179 billion in 2020-21. Revenues are projected to increase to $186 billion in 2021-22. Over the budget window (2019-20 through 2021-22), our estimates are $4 billion higher than the administration’s May Revision estimates. Given the scale of recent upward revisions, this difference between our office and the administration is modest.

Wide Range of Outcomes Possible in Budget Year. Even without additional major economic disruptions, it is entirely plausible that revenues could end up $10 billion below or above our main forecast for 2021-22. Should another recession begin sometime in the next year, revenues could be expected to fall $15 billion to $30 billion below our main forecast.

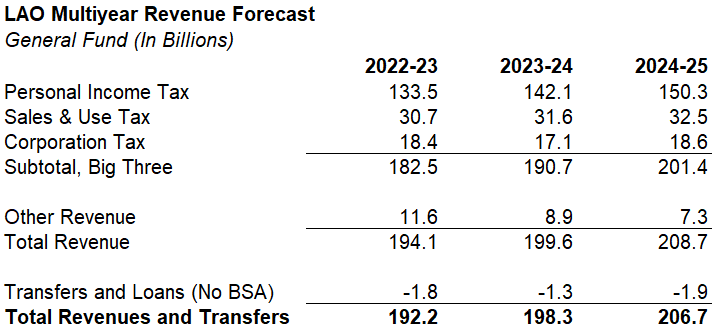

Out Year Forecast Is Middle-of-the-Road Among Potential Outcomes. Our main forecast anticipates annual revenue growth to average 4 percent over 2022-23 to 2024-25, resulting in revenues reaching $207 billion by 2024-25. This growth rate is a bit slower than the average over the last 20 years of 5.5 percent, reflecting the expected effects of recent tax policy changes. While our main forecast presents the estimates we think are most likely to be least wrong, they will be wrong to some extent. As shown in the graph above, historical experience suggests that revenues ultimately could end up $50 billion higher or lower than our estimates for 2024-25.

Administration’s Out Year Forecast More Cautious But Still Highly Plausible. By 2024-25, our main forecast is about $20 billion above the administration’s May Revision forecast of $187 billion. While this difference seemingly is significant, it should be interpreted in the context of the uncertainty surrounding these estimates. Even without an additional recession, we estimate that it is possible that revenues could wind up as low as $175 billion in 2024-25. Thus the administration’s estimates, despite being below our main forecast, are still well within the range of highly plausible outcomes. As such, should the Legislature wish to build in additional caution against future budget shortfalls, the administration’s estimates are a reasonable starting point.

Comments on Major Revenue Sources

Personal Income Tax (PIT)

2020-21 PIT Revenue On Pace For Very Strong Growth. Collections to date in 2020-21 have been strong and suggest that revenues will finish well ahead of 2019-20. Through April, 2020-21 withholding on workers’ wages, salaries, bonuses, and stock options is up 13 percent over 2019-20. Estimated payments on upper-income filers’ nonwage income (such as business income, dividends, interest, and capital gains) similarly have been up in 2020-21. Payments between August 2020 and March 2021 (data for July 2020 and April 2021 are not comparable due to deadline changes) were up 41 percent from 2019-20. Based mainly on these withholding and estimated payments numbers, we expect 2020-21 General Fund PIT revenue to end up at $120 billion, a 19 percent increase from 2019-20.

PIT Revenue Growth Should Moderate in 21-22. Our main revenue forecast expects growth in PIT revenues in 2021-22 to slow from the torrid pace of 2020-21. Our current projection is for $127 billion of General Fund PIT revenue, a 6 percent increase from 2020-21. We expect taxable income growth from wages and salaries and business activities to slow somewhat, and income from capital gains to level off.

DOF Projects Lower Wages and Salaries, Capital Gains. The administration projects lower revenue than we do in both 20-21 and 21-22. The biggest sources of this difference are the administration’s lower projections for wages and salaries and capital gains in tax years 2021 and 2022. We discuss these two areas of difference below.

LAO Forecast Expects Wage Growth For High-Earners To Continue to Outpace Others. Consistent with historical norms, our forecast anticipates that high-earners will continue to receive strong wage and salary growth relative to workers earning less. In contrast, beginning in 2022, the administration expects a growing share of wages and salaries will go to low- and middle-income workers. This would be a reversal of the pattern the state has observed in most of the past 30 years. As the PIT taxes higher-income filers more heavily than lower-income filers, assuming an income shift away from higher-income filers leads to weaker revenue growth projections.

Capital Gains Estimates Reflect Stock Price Gains. Our main forecast expects a notable uptick capital gains tax revenue in 2021-22, followed by a leveling off of capital gains revenues in the out years. Our forecast reflects the recent rapid rise in stock prices and an expectation that stock prices grow at near average historical rates for the near future—a slower price growth rate than we have observed since the start of 2019. In comparison, the administration expects a smaller uptick in capital gains in 2021-22, followed by declines in each of the out years.

Corporation Tax (CT)

Growth in Taxable Corporate Profits Drive CT Estimates. Our main forecast reflects the disparate economic effects of the COVID-19 pandemic. As discussed above, California’s technology sector has thrived while many businesses have struggled throughout the pandemic. Collections to date in 2020-21 are higher than the administration’s January CT forecast by $2.8 billion, or 31 percent. We expect that this surge in revenue primarily is due to unexpected growth in taxable corporate profits. At the same time, corporations in the most affected sectors of the economy—such as hospitality and personal services—have likely incurred significant losses. These business losses have yet to significantly affect state CT cash receipts in 2020-21 but eventually could reduce CT in future years because corporations can deduct losses from prior years when they later make a profit.

Revenue Decline Due To Expiration of Temporary CT Policy Changes. Our main forecast shows declines in CT revenue through 2023-34 despite our assumption that taxable corporate profits will continue to grow by about 5 percent annually. Last year, faced with a projected budget shortfall, the Legislature temporarily limited the use of two common business tax provisions for three years. Specifically, taxpayers with business income of $1 million or more have not been allowed to deduct losses from prior years and most business credits are limited to $5 million per tax year. Our main forecast and the May Revision assume these policies increase revenues in 2021-22 and 2022-23, with our estimates of the effect being several hundred million dollars higher. The CT declines in 2022-23 and 2023-24 because the affected taxpayers are again allowed to deduct losses and use their accumulated tax credits.

LAO Forecast Assumes Higher Corporate Profits In 2021-22 and 2022-23. Incorporating the Governor’s tax proposals, we estimate the CT will generate $21.0 billion in 2020-21, $20.8 billion in 2021-22, and $18.4 billion in 2022-23. Our estimates are more than $4 billion higher over this three year period because we assume that taxable corporate profits continue to grow in the budget year. This difference is accentuated by modestly different assumptions regarding recent tax policy changes. In addition to different assumption regarding the temporary limits on loss deductions and credits mentioned in the paragraph above, we also assumed that a change that provides tax benefits to some businesses that received pandemic-related financial assistance from the federal government would affect more pass-through businesses than corporations.

Sales Tax

Rebounding Consumer Spending, Shift to E-Commerce Boost 2020-21 Sales Tax Collections. After a short but dramatic drop in taxable spending last spring, sales tax collections have been strong in recent months. Over the last six month (November 2020 to April 2021) sales tax collections have come in 10 percent ahead of the same period in 2018-19. Reflecting this trend, our main forecast expects sales tax revenues to total $28.3 billion, an eleven percent increase over 2019-20.

Expectation of Economic Rebound Over Next Year Drives Higher 2021-22 Sales Tax Forecast. Consistent with the consensus of economists for continued economic rebound over the next year, our main forecast expects additional sales tax growth in 2021-22. Specifically, we project sale tax revenues will grow by 5 percent in 2021-22, reaching $29.7 billion.