Table of Contents

Chapter 1

Key Features of the 2018‑19 Budget Package

Chapter 2

Spending by

Program Area

October 2, 2018

The 2018-19 Budget

California Spending Plan (Final Version)

Chapter 2: Spending by Program Area

Other Provisions

Proposition 2 Infrastructure

Proposition 2 Requires Infrastructure Spending After BSA Reaches Maximum Level. Under Proposition 2, the state is required each year to set aside funds for reserves, debt payments, and—potentially—infrastructure. In particular, the state must deposit funds into the rainy day fund—the BSA—until it reaches its maximum level of 10 percent of General Fund tax revenue. (The state can suspend or withdraw these deposits when facing a budget emergency.) Once the BSA reaches this maximum, required deposits that would bring the fund above 10 percent of General Fund taxes instead must be spent on infrastructure. Under the budget plan’s revenue assumptions, the maximum BSA level is $13.8 billion. With both a required and optional deposit, the budget package sets aside enough funds so that the BSA reaches its maximum level at the end of 2018‑19.

Proposition 2 Infrastructure Spending to Begin in 2019‑20 if Economy Continues to Grow. Each year that General Fund tax revenues increase, the maximum level of the BSA also increases (typically by several hundred millions of dollars). Beginning in 2019‑20, any Proposition 2 requirement in excess of the amount needed to max out the reserve must be dedicated to infrastructure. For example, if the 2019‑20 Proposition 2 requirement is $1.5 billion, around $1 billion would be allocated to infrastructure projects.

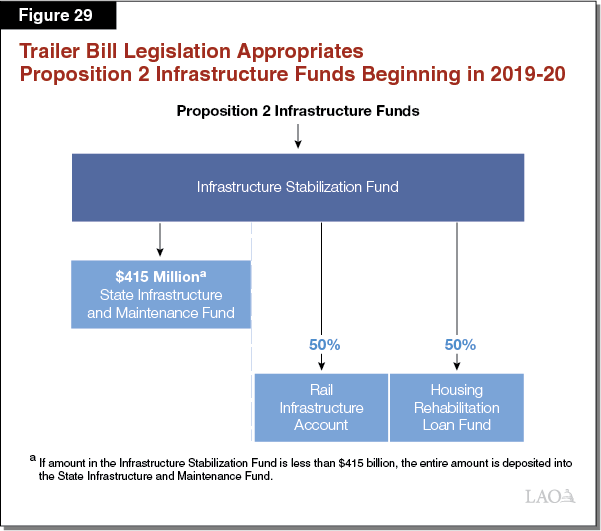

Trailer Bill Appropriates These Funds to Three Uses. Chapter 43 (AB 1831) appropriates future available Proposition 2 infrastructure funds to the Infrastructure Stabilization Fund (from 2019‑20 through 2021‑22). As shown in Figure 29, the legislation distributes these funds to the following three uses:

- State Infrastructure and Maintenance Fund. The first $415 million available is dedicated to fund state capital outlay, lease payments related to state capital outlay, and deferred maintenance. The Legislature will appropriate these funds for these dedicated purposes in future annual budget bills.

- Rail Infrastructure Account. After dedicating $415 million to state infrastructure, Chapter 43 continuously appropriates half of the remaining funds to the Transportation Agency for the newly established Rail Modernization Improvement Program. The Secretary of Transportation will allocate the funds to high‑priority rail projects, including those that benefit shared use corridors and station areas.

- Housing Rehabilitation Loan Fund. Chapter 43 continuously appropriates the other half of the remaining Proposition 2 infrastructure funds to the Multifamily Housing Program, administered by the California Department of Housing and Community Development. This program funds the construction and rehabilitation of affordable rental housing for lower‑income households.

Deferred Maintenance and Other Infrastructure

Deferred Maintenance. As summarized in Figure 30, the budget includes $305 million on a one‑time basis from the General Fund (non‑Proposition 98) for deferred maintenance projects at 20 state departments in 2018‑19. The departments have up to three years to expend these funds. (The budget also includes $28 million in Proposition 98 General Fund for community college projects.) The budget includes a provision that allows departments to use up to 10 percent of their allocations—up to $5 million—to conduct assessments of department infrastructure.

Figure 30

Deferred Maintenance

2018, Non‑Proposition 98 General Fund (In Millions)

|

Department |

Amount |

|

Water Resources |

$100 |

|

Judicial Branch |

50 |

|

California State University |

35 |

|

University of California |

35 |

|

California Exposition and State Fair |

15 |

|

Developmental Services |

10 |

|

General Services |

10 |

|

State Hospitals |

10 |

|

Corrections and Rehabilitation |

9 |

|

Science Center and African American Museum |

7 |

|

Military |

4 |

|

Office of Emergency Services |

4 |

|

State Special Schools |

4 |

|

Veterans Affairs |

4 |

|

California Fairs |

3 |

|

Forestry and Fire Protection |

2 |

|

Employment Development |

1 |

|

Food and Agriculture |

1 |

|

Conservation Corps |

0.5 |

|

Hastings College of Law |

0.5 |

|

Total |

$305 |

Because the administration has not identified all of the specific projects that departments will undertake with the funding, the budget requires DOF to provide a list of projects to the Joint Legislative Budget Committee (JLBC) 30 days prior to allocating funds to a department. Subsequent to the allocation of funds, departments may change their list of projects subject to approval by DOF. DOF must notify the JLBC of any projects added with estimated costs of greater than $1 million, as well as provide a quarterly report of all changes to the list of projects. The budget also requires DOF to provide the JLBC with an annual report on the status of funded projects.

Capitol Annex. The budget sets aside $630 million from the General Fund into the State Project Infrastructure Fund (SPIF) for the renovation of the State Capitol Annex, originally constructed in 1952. Budget trailer legislation authorizes the use of lease revenue bonds of up to $756 million for the renovation in the event that total funding in SPIF (including $128 million of previously available fund balance) is not sufficient to cover project costs. The legislation also authorizes lease revenue bonds of $423 million to construct a new office building near the State Capitol to be used as “swing space” for legislators and staff during the renovation of the Annex.

Sacramento Area State Office Buildings. The budget includes $29.6 million from the General Fund for the initial planning phase—known as the performance criteria phase—for three state office building projects in the Sacramento area. These capital outlay projects are:

- Construction of Richards Boulevard Building ($18.1 Million). The budget provides funding for the performance criteria phase of a project to construct a complex of four buildings with a total of 1 million net usable square feet at the former site of the state printing plant. The total estimated cost of this project is about $1 billion. The facility is expected to house the California Department of Tax and Fee Administration; the Board of Equalization; and various departments within the Business, Consumer Services, and Housing Agency.

- Renovation of the Bateson Building ($5.2 Million). This project will involve the renovation of the 215,000 net usable square foot building constructed in 1981. The total cost of the project is estimated at $161 million. The building is expected to house various departments currently in leased space, such as the Department of Parks and Recreation, Department of Water Resources, and Department of Forestry and Fire Protection.

- Renovation of the Unruh Building ($6.3 Million). This building was constructed in 1929 and has 125,000 net usable square feet. The total cost of the project is estimated at $90 million. The State Treasurer’s Office—the building’s major tenant—is expected to relocate back to the Unruh Building after completion of the renovation.

Debt Service. The budget provides $7.6 billion from various funds for debt service payments in 2018‑19. This represents an increase of 6 percent from 2017‑18. This total includes $6.5 billion for general obligation bonds ($5 billion from the General Fund), and $1 billion for lease revenue bonds ($623 million from the General Fund).

Employee Compensation

Labor Agreements Increase State Annual Costs. Assuming union members ratify agreements with Bargaining Units 9 and 10, the state has active memoranda of understanding (MOU) with 20 of the 21 state rank‑and‑file employee bargaining units. (The MOU with Bargaining Unit 5 [Highway Patrol] expired in July 2018.) In 2018‑19, the budget assumes that state costs to pay for salary and benefits (excluding retirement benefits) for rank‑and‑file employees and their managers will increase by $1.4 billion ($725 million from the General Fund). In addition, various provisions in MOUs will significantly increase state annual costs for years to come. These include scheduled salary increases, funding state contributions to prefund retiree health benefits, increases in health care costs, and increases in other benefit costs.

Retirement Costs Continue to Grow. The state’s costs to pay for pension and retiree health benefits continue to grow. The budget assumes that the state’s costs to pay for active and retired state employees’ pension benefits will increase by $340.5 million ($189 million General Fund) in 2018‑19 to a total contribution of $6.2 billion ($3.6 billion from the General Fund). State pension costs are expected to grow for the foreseeable future due to CalPERS phasing in the effects of actuarial assumption changes and salary growth. In addition, the budget assumes that the state’s costs to pay for health benefits received by retired state employees will increase by about $170 million to a total of $2.2 billion in 2018‑19. These costs also are expected to grow for the foreseeable future due to increases in health premiums and the number of retired state employees and eligible dependents receiving the benefit.

Financial Information System for California (FI$Cal)

An Integrated Financial Management System. For the last several years, the administration has been engaged in the design, development, and implementation of the FI$Cal project. This information technology (IT) project will replace the state’s aging and decentralized IT financial systems with a new system integrating state government processes in the areas of budgeting, accounting, cash management, and procurement. Since the project began, it has changed considerably in scope, schedule, and cost from what was initially anticipated. These changes have been documented in special project reports (SPRs). In February 2018, the California Department of Technology approved the seventh SPR for FI$Cal.

New Project Plan. The new project plan—SPR 7—changes the scope of the FI$Cal project in two significant ways. First, it ends the project before the State Controller’s Office’s (SCO’s) accounting functions fully transition onto FI$Cal. Second, it changes the “onboarding” approach so that not all departments that were previously anticipated to transition to FI$Cal will actually transition. Although SPR 7 makes significant changes to the scope of the FI$Cal project, it only reflects very minor changes in overall project costs. Based on SPR 7, the total estimated cost for the project is $918 million ($493 million General Fund) and is estimated to be completed in July 2019. The 2018‑19 spending plan provides $53.5 million ($52.2 million General Fund) to continue with the FI$Cal project and maintain and operate the FI$Cal system.

SCO’s Integrated Solution. In light of persistent challenges, SPR 7 establishes a new approach for deploying the accounting functions related to SCO. Rather than transitioning fully to FI$Cal, as prior SPRs planned, SPR 7 introduced the Integrated Solution. Under the Integrated Solution, SCO will run the FI$Cal system and its existing legacy accounting systems in tandem. The Integrated Solution develops interfaces between both FI$Cal and SCO’s legacy systems so that data is entered only once (in either system) but then both systems share the data. This way each system can perform the accounting and cash management functions for the state. The administration proposed this approach because of SCO’s continued concern regarding the performance and accuracy of the FI$Cal system. The Integrated Solution allows additional time for testing and validating the FI$Cal system using reports produced by SCO’s legacy systems before SCO fully transitions.

The cost of the Integrated Solution is not reflected as a project cost in SPR 7. Instead the 2018‑19 spending plan provides SCO $5.4 million ($3.1 million General Fund) to support the Integrated Solution. In total, SCO anticipates it will cost $25.6 million (all funds) through 2021‑22 to (1) develop and test the new accounting and cash management functions in FI$Cal, (2) develop the Integrated Solution, and (3) support the maintenance and operations of the FI$Cal project once the legacy systems are decommissioned. None of these costs are reflected in the total FI$Cal project cost. However, as a means of tracking project costs, the Legislature adopted supplemental reporting language as part of the 2018‑19 budget that requires the Department of Finance to provide a list of enacted budget proposals related to the Integrated Solution by January 1, 2020.

Cannabis Regulation and Enforcement

As summarized in Figure 31, the budget includes an increase of $129 million (primarily from the Cannabis Control Fund and Cannabis Tax Fund) for several departments to regulate cannabis businesses. This amount roughly doubles the amount provided in 2017‑18. The funding is provided on a two‑year limited‑term basis. A majority of the funding supports the departments responsible for licensing and compliance oversight of cannabis businesses, including retailers, cultivators, and manufacturers. Other activities supported by the funding include administrative hearings of appeals filed by licensees, tax collection, and implementation of an information technology system (IT) to track cannabis products from cultivation through retail. The budget act allows the amounts provided from the Cannabis Control Fund for the Bureau of Cannabis Control, Department of Public Health, and Department of Food and Agriculture to be augmented by the Department of Finance (DOF) for additional resources needed to implement IT, licensing, and enforcement activities. The budget also authorizes a $59 million loan from the General Fund to the Cannabis Control Fund in case licensing revenues are not sufficient to cover costs.

Figure 31

Summary of Funding Increases for Cannabis Regulation and Enforcement

2018‑19 (In Millions)

|

Department |

Primary Purposes |

Amount |

|

Bureau of Cannabis Control |

Licensing and enforcement of retailers, distributors, and other licensees; grants to equity applicants |

$54.3 |

|

Food and Agriculture |

Licensing and enforcement of cultivators |

28.3 |

|

General Services |

Administrative hearings on behalf of licensing departments |

13.0 |

|

Public Health |

Licensing and enforcement of manufacturers |

10.6 |

|

GO‑Biz |

Grants for substance abuse treatment and other services |

10.0 |

|

Employment Development |

Administration of employment tax program |

3.7 |

|

Highway Patrol |

Develop protocols for determining when drivers are under the influence of cannabis |

3.0 |

|

Tax and Fee Administration |

Administration of cultivation and retail excise taxes |

2.3 |

|

University of California |

Research on effects of cannabis |

2.0 |

|

Cannabis Control Appeals Panel |

Hearing appeals of decisions made by cannabis licensing departments |

1.4 |

|

Secretary of State |

Business filings and trademark registration |

0.4 |

|

Finance |

Audit of Bureau of Cannabis Control |

0.4 |

|

Total |

$129.4 |

|

|

GO‑Biz = Governor’s Office of Business and Economic Development. |

||

Voting Equipment

Reimbursement to Counties for Voting Equipment. The budget includes up to $134.4 million General Fund for the state to reimburse counties for costs counties incur to replace voting systems. Counties may seek reimbursement for costs to replace voting systems incurred after April 29, 2015. The Secretary of State will determine the maximum amount of state funding available to each county based on the size of the county, the number of voters registered in the county, and the Secretary of State’s estimate of need for county voting equipment.

Census

Over $90 Million for Census Outreach. The budget provides $90 million to the Government Operations Agency for outreach activities related to the decennial census through 2020‑21. Outreach will be led by the Complete Count Census (a committee established for the purpose of ensuring California has a complete and accurate census count). The budget package requires the Complete Count Census to report on various elements of census preparation—including the media campaign and funding allocations for local, targeted outreach—over the next three years. These reports are due to the Joint Legislative Budget Committee, the Assembly Select Committee on the Census, and the Senate Select Committee on the 2020 United States Census various progress.

Office of Emergency Services (OES)

The budget provides OES with $1.5 billion (more than two‑thirds from federal funds) in 2018‑19. This is a net increase of $38 million, or about 3 percent, compared to the estimated spending level in 2017‑18. In addition to the augmentations described below, the budget includes $10 million from the General Fund to support local domestic violence shelters (discussed in the “Homelessness” section of this report).

California Disaster Assistance Act (CDAA). The budget includes an increase of $88.1 million in 2018‑19 and $23.5 million ongoing from the General Fund for CDAA (for a total of $127.2 million in 2018‑19 and $62.6 million ongoing for CDAA). Most of the increase in 2018‑19 is expected to be used to provide reimbursements to local governments related to damage to local infrastructure caused by storms in early 2017 and fires in late 2017. The ongoing funding represents the average of spending on CDAA in recent years.

California Earthquake Early Warning (CEEW) System. The budget includes $15.8 million from the General Fund in 2018‑19 and $750,000 from the General Fund annually thereafter to support the CEEW system. Of the total in 2018‑19, $15 million is to complete the build‑out of 283 remaining planned sensor stations required for the system.

Military Department

The budget provides $231 million for the California Military Department (CMD), including $104 million from the General Fund and $125 million from federal funds. This total is an increase of $16 million, or 7 percent, from 2017‑18 estimated expenditures.

California Cadet Corps. The budget provides an additional $7.2 million in General Fund support in 2018‑19 (increasing to over $8 million annually in future years) to more than triple the size of the cadet corps program from its current level of 51 schools and 6,000 cadets to 175 schools and 21,875 cadets by 2022‑23. This increase in support will fund a greater share of program costs that are currently paid for by schools in areas such as commandant training, supplies, and activities. It will also fund uniforms and state‑level activities for these additional participating schools. Finally, it will fund curriculum updates, improved facilities for CMD staff, and a larger state‑level staff (12 additional positions in 2018‑19 and 11 thereafter).

Military Academies. The budget includes $3.6 million from the General Fund in 2018‑19 ($3.3 million ongoing) to enable CMD to support activities at both the California Military Institute (CMI) and Porterville Military Institute (PMI). Most of this funding is to support 21 military personnel to run the military program component of the schools, similar to the support currently provided at the Oakland Military Institute (OMI).

Labor Programs

New Statewide Prison to Employment Initiative. The spending plan includes $36 million General Fund over two years ($16 million in 2018‑19 and $20 million in 2019‑20) for the California Workforce Development Board (State Board) to distribute grants to local workforce boards to fund employment training opportunities for at least 1,000 ex‑offenders and to integrate local employment training with programs offered by parole and probation departments. Funds could be used for a variety of services, including English language learning, basic skills and adult education, training stipends, industry‑approved certification programs, pre‑apprenticeship, and on‑the‑job training, among others. In addition to direct employment services, the spending plan funds supportive services for ex‑offenders who participate in job training. Supportive services are services that an ex‑offender may require in order to attend job training and commonly include bus passes, childcare vouchers, and housing assistance. Ex‑offenders who participate in employment services would be eligible for up to $5,000 each in supportive services. Funding would also be provided to support the creation of regional partnerships between the local boards, California Department of Corrections and Rehabilitation, parole centers and county probation departments, and community‑based reentry service providers. These funds would be used to facilitate collaboration among the partner organizations in order to customize job placement based on each ex‑offender’s training history, education needs, and work experience. The State Board will perform a study of the initiative in 2021‑22, evaluating the degree to which individuals who receive services under the initiative are able to successfully complete workforce training programs and successfully transition into the labor market and broader workforce education system.

Funds the Breaking Barriers to Employment Initiative. The spending plan includes $15 million General Fund to provide workforce training support grants pursuant to Chapter 824 of 2017 (AB 1111, E. Garcia), known as the Breaking Barriers to Employment grant program. Grant funds will supplement workforce development services for individuals with barriers to employment in order for them to successfully enter, participate in, and complete existing training programs. Eligible individuals include, among others, out‑of‑school youth, the long‑term unemployed, English language learners, the California Work Opportunity and Responsibility to Kids (CalWORKs) participants, seasonal farmworkers, and persons with disabilities.

Expanded Funding for Apprenticeship Consultants. The 2018‑19 spending plan includes $3.5 million special funds to support 22 new apprenticeship consultant staff positions at the Division of Apprenticeship Standards within the Department of Industrial Relations. These staff will support new apprenticeship training programs in nontraditional industries, including certain state civil service classifications, information technology, and healthcare services. The budget plan includes ongoing funding of $5.6 million special funds to support a total of 42 apprenticeship consultants by 2021‑22. These positions will be funded out of the Employment Training Fund, which consists of revenue from an existing payroll tax on employers. Typically, these funds are used by the Employment Training Panel to distribute workforce training grants to businesses.

Department of Veterans Affairs

The spending plan for California Department of Veterans Affairs (CalVet) includes $414 million General Fund in 2018‑19, an increase of $9.2 million (2.3 percent) over revised estimates for 2017‑18. This amount is expected to be offset by $76 million from federal reimbursements for Veterans Homes.

Additional Reporting Requirements for Veterans Homes Master Plan. The 2017‑18 budget included language that requires CalVet to develop a systemwide master plan for the veterans homes by July 1, 2019. Key components of the master plan include (1) an assessment of current demand for services, (2) projecting future long‑term care needs among California’s veterans, and (3) determining how to align the veterans homes system to meet current and future demand across all levels of care.

The 2018‑19 budget extends the deadline for the master plan to December 31, 2019 and requires that the master plan be updated every five years. Additionally, CalVet is required to include additional information in the master plan about (1) potential location of future veterans homes, (2) the possible provision of services through a community‑based model, and (3) the local cost of living for employees. The 2018‑19 spending plan provides $241,000 General Fund for two permanent positions beginning 2019‑20 (once the limited‑term resources provided in 2017‑18 expire) to support the future development of the master plan.

Capital Outlay. The 2018‑19 budget includes funding for two capital outlay projects:

- Veterans Home of California, Yountville Skilled Nursing Facility. The plan provides about $7 million General Fund for the beginning phase to construct a new skilled nursing and memory care facility at the Veterans Homes of California in Yountville. The new facility, which is estimated to cost a total of $293 million, would largely replace the existing skilled nursing facility and memory care unit at Yountville.

- California Central Coast Veterans Cemetery (CCCVC). The plan includes $571,000 from private donations to complete the working drawings for the expansion of the CCCVC. The expansion is estimated to result in about 3,700 in‑ground burial sites. The total cost of the project is estimated to be $9.2 million and will be covered by a combination of federal, state, and private funds.

Earned Income Tax Credit (EITC)

State EITC Adopted in 2015. The EITC is a personal income tax credit that is intended to reduce poverty among California’s poorest working families by increasing their after‑tax income. California adopted the state EITC in 2015. The state EITC builds on the similarly structured federal EITC. (For more information on the federal EITC and the prior state EITC, see our 2015‑16 State Spending Plan.) The budget package modifies the existing EITC in two ways.

Closes Age Gaps. By building on the federal EITC, the state EITC inherited certain eligibility restrictions. Specifically, under the federal EITC, eligible filers without a qualified dependent child must be at least age 25 and younger than age 65. The 2018‑19 budget plan expands the state EITC to working individuals without children who are between the ages of 18 and 25, as well as to those over age 65. The administration estimates this change will allow up to 500,000 previously ineligible filers to claim the state EITC.

Expanded to Higher Income Families. The 2018‑19 budget plan expands income eligibility to $16,800 for filers with no children and $24,960 for filers with one or more qualifying children. The higher income thresholds account for the rising minimum wage. For instance, $24,960 reflects the annual earnings of one person working fulltime at the 2019 minimum wage of $12 per hour. These changes will allow about 220,000 additional households to claim the credit. In addition, because of the higher income thresholds, the credit phases out more slowly for those eligible tax filers with higher incomes. As a result, the amount of the credit will be somewhat higher—by tens of dollars—for a filer near the high end of current qualifying range.

Increased Spending on EITC Education, Outreach, and Tax Preparation. The 2018‑19 budget provides $10 million for grants to various organizations to expand awareness of the EITC.

Business Tax Credits

Extends Film Tax Credit by Five Years. The budget package extends the motion picture tax credit through the 2024‑25 fiscal year. The California Film Commission competitively awards up to $330 million per year in tax credits to motion picture production companies. The credit amount is 20 percent of certain production expenses, such as crew wages and post‑production costs. (The credit is higher—25 percent—for independent films and relocating television productions.)

Extends California Competes and Provides $20 Million for Small Business Assistance. The budget package extends the California Competes program by five years. This program allows the administration to negotiate tax credit agreements under which selected businesses may qualify for tax credits by meeting hiring and investment targets. The budget package reduces the annual limit on available credits from $200 million to $180 million. The budget also provides $20 million per year for five years for grants to organizations that offer technical assistance services to small businesses and entrepreneurs.

Extends New Employment Credit. The budget package extends the New Employment Credit by five years. This credit is intended to provide an incentive for businesses to hire individuals who, because of their personal history, may have difficulty entering the workforce or developing employment skills. Businesses operating in specified areas of the state may claim a credit if they hire an eligible individual, pay the new employee at least 150 percent of the state minimum wage ($16.50 per hour in 2018), and comply with certain reporting requirements. The annual amount of credits allowed varies and is unrestricted. Eligible businesses claimed about $1.4 million in credits for 2016.