- All Articles Property Tax

Can Local Governments' AB 8 Shares Change? February 5, 2016

Local governments' shares of the property tax were set by the laws that implemented Proposition 13. In this post, we examine the conditions under which these shares change.

A Closer Look at the Administration's Property Tax Estimates January 27, 2016

Our review of the best available evidence suggests that property tax collections in 2015-16 and 2016-17 will be higher than the administration assumes.

Why the Mid-1970s Play a Large Role in Property Taxes Today January 27, 2016

Why is it that one of the primary factors determining property tax revenues for California local governments is how much that government received in the mid-1970s?

Four Factors Affecting Cities' Property Tax Revenues January 13, 2016

This post, the fourth in our property tax series, discusses the primary factors affecting a city government's proportion of the total property taxes collected within its boundaries.

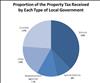

Differences in Property Tax Revenue for Counties, Cities & Special Districts January 6, 2016

We examine the revenue from California's 1 percent property tax that is available for a subset of local governments.

Local Governments' Services & Their Property Tax Revenue December 16, 2015

We discuss the distribution of property taxes to the various types of California local governments.

Understanding Your Property Tax Bill December 9, 2015

What are the different charges on a California property tax bill?

Fiscal Outlook: Property Taxes More Steady Than Home Prices November 18, 2015

Our Fiscal Outlook assumes continued growth in assessed values.

Ending the Triple Flip February 3, 2015

With the upcoming end of the "triple flip," a complex, decade-old mechanism affecting state and local finances in California, we have received several inquiries seeking a basic understanding of what the triple flip is and how its end will work exactly. This note addresses those issues.

Counties, Cities, Special Districts Receive Variety of Revenues December 16, 2014

The property tax is the largest source of local tax revenue for all local governments combined.

Allocation of Property Tax Has Varied Over Time December 16, 2014

Since passage of Proposition 13 in 1978, the allocation of local property taxes has changed several times.

California Governments Rely on a Variety of Taxes December 16, 2014

The state government and local governments, respectively, rely on different tax revenue sources.

Local Governments Getting Some Taxes Formerly Allocated to Redevelopment December 8, 2014

In February 2012, over 400 redevelopment agencies were dissolved, and the process of unwinding their financial affairs began.